When The Wind Blows

Key Points

- In Q2 2022, the private equity market continued to show signs of softening, though overall levels of investment activity are on par with those pre-Covid (2019).

- Despite geopolitical concerns, rising inflation and turbulent stock markets, we continue to see a high level of compelling opportunities through our global network of over 700 investment partners.

- In H1 2022, the Unigestion private equity team committed EUR 528m to investments, including EUR 138m invested in seven secondary transactions and EUR 178m invested in seven direct investments and various add-ons.

Overview

In Q2 2022, the private equity market continued to show signs of softening across most metrics. Yet, while investment activity was materially lower in Q2 vs one year ago, overall levels are on par with pre-Covid (2019) investment activity. Notably, since last quarter, the pendulum has swung from North America to Europe, likely related to a catch-up effect after geopolitical uncertainty initially delayed European deal closings in Q1. In addition, exit activity significantly dropped across all regions, suggesting that fund managers are waiting for better conditions to exit. Meanwhile, with the combination of lower liquidity and denominator effect issues due to falling public markets, investors are showing clear signs of restraint. The fewest number of funds raised capital in the first half of 2022 than any six-month period since 2013. On the positive side, this is leading to less dry powder, as fund managers are deploying more capital than they are raising. This, combined with lower public market valuations, will likely lead to lower private equity valuations in the coming quarters.

Europe Catches Up

The global aggregate value of private equity deals closed during Q2 was EUR 229bn, 23% down on the same quarter last year[1] . This was driven by a big drop in North America (-39%) as well as APAC (-24%), while Europe (+10%) bucked the trend, bouncing back after a slow Q1.

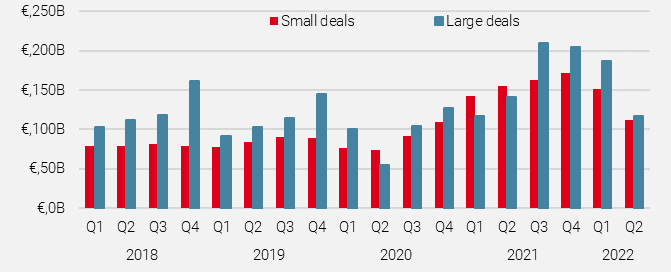

The last two years since the beginning of the pandemic has clearly been an unusual period. The market momentarily slowed down in the middle of 2020 and then, in the following 18 months, there was a huge tidal wave of activity. While there has been a slowdown in the last two quarters compared to a year ago, overall investment activity is now back in line with 2018 and 2019 levels.

However, there remains an interesting difference between the pre- and post-Covid era. Investments in mid-market companies (defined as deals with an enterprise value of less than EUR 500m) for the last two years have made up around 50% of total investment activity. This is a step up compared to the two years prior to Covid, when mid-market companies consistently represented around 40% of activity.

The reasons behind this shift might be several, including increased opportunities at the lower end of the market, and a reduced number of attractive targets at the large end (especially public-to-privates which tend to be a large proportion by value of large deals). Notably, despite the volatile macro and geopolitical environment over the last few years, deal volume has been particularly stable at the smaller end of the market.

Figure 1: Small vs Large Deals

Source: Pitchbook, July 2022.

Meanwhile, exit activity was significantly down in every region in Q2 vs the same quarter one year ago. As a result, exit activity was the lowest for the first half of a year since 2014. The global aggregate value of exits was EUR 123bn, a decrease of 55% on the same quarter last year. Declines were seen in North America (-50%), Europe (-66%) and APAC (-56%).

While this suggests that private equity owners are waiting for better conditions to sell, high quality businesses with resilient growth profiles can still be sold for attractive prices in this environment.

From our 2016 vintage direct programme, we recently sold Captive Resources, the largest captive insurance (insurance owned and controlled by its own members) consultant. The company provides its members insurance coverage for workers’ compensation, general liability, automobile, property, and health insurance. Captive Resources has successfully secured an 80%+ market share, managing 44 group captives covering 5,500 companies and USD 3.3bn in premiums. The company was acquired by KKR for USD 2.25bn, leading to a 3.4x multiple for our fund.

Private equity fundraising remains lacklustre with only USD 110bn raised globally for buyout funds in the first half of 2022, less than half of the amount raised compared to the first half of 2021 and the weakest six month period since 2013[1]. Nevertheless, against this backdrop, certain mega buyout funds have still been replenishing their coffers. Advent International closed on its USD 25bn fund, the second biggest of all time, while KKR was not far behind with a USD 19bn fund. This suggests that investors are still finding comfort in the big names, despite the challenging environment.

Within this context, we nevertheless continue to source attractive opportunities globally for our investors through the dedicated application of our investment themes, which lead us to areas of high growth, irrespective of the macro environment. In addition, we focus heavily on companies which display robust fundamentals, such as recurring revenues, pricing power through market leadership and strong balance sheets (see discussion later).

Despite more difficult market conditions, we continue to source attractive opportunities globally through the dedicated application of our investment themes.

In April, we invested in Freightwise, a US-based logistics technology company that helps its clients navigate logistics with an easy-to-use cloud-based software that streamlines processes, automates tasks, provides cost-saving insights, and ultimately reduces the carbon emissions related to shipping. The significant cost savings that can be achieved lead to real benefits for customers. This company plays our Service Efficiency investment theme and has a measurable positive contribution to SDG 13 – Climate Action.

In the same month, we invested in Buckaroo, a Netherlands-based online payment solution provider. The company is a leader in the Dutch market with clients ranging from top merchants with strong online presence, utility companies to government bodies. Thanks to its scalable model, the company has achieved healthy growth rates (c. 30% p.a.) and increasing EBITDA margins over the last few years. The underlying double-digit growth of e-commerce still has a long runway potential in the Netherlands and adjacent countries like Belgium. Buckaroo plays our Personal/Financial Wellbeing investment theme.

In May, we committed to the second fund of LEA Partners, a German-based specialist investor in enterprise software and tech-enabled service businesses. The team has developed a proven approach to source deals and create value with a clear focus on growth initiatives through accessibility / cloud usage, revenue model optimisation and team development. This fits our typical emerging manager investment profile: (i) we have good visibility on the first few investments, with three already having been closed, (ii) we negotiated a co-investment in the first deal (10 months after closing and the completion of two add-on acquisitions), and (iii) we have been able to improve the LPA terms and GP commitment.

Overall, despite geopolitical concerns, rising inflation and turbulent stock markets, we continue to see a high level of compelling opportunities through our global network of over 700 investment partners.

After Inflation, Recession?

The first half of 2022 ended on a truly sour note for financial markets, with central banks aggressively tightening while economies continue to weaken. In the past, any sign of a marked slowdown in the developed world would have been met and resolved by the (in)famous Greenspan “put”, a quick and convenient fix to calm the markets and revive the economy via lower rates or quantitative easing, or a combination of both.

This time around is very different, as runaway inflation has basically tied the hands of policy makers, now desperately trying to tame the inflationary beast they themselves unleashed by keeping rates too low and for too long. This in turn has spooked the markets, leading to a broad sell-off in equities and bonds. In June, however, the recessionary theme made a comeback, as witnessed by some distinct rotations across and within asset classes.

The recessionary theme has made a comeback, as witnessed by some distinct rotations across and within asset classes.

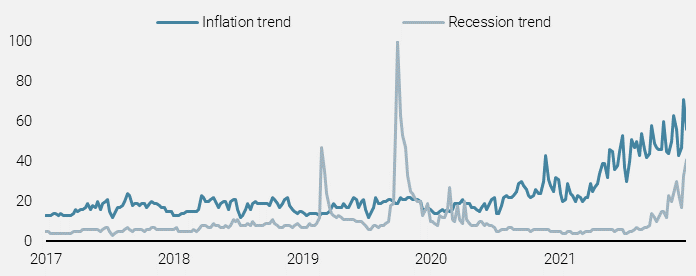

Figure 2 compares the Google searches of “inflation” versus “recession”. As can be seen, the latter has made a pronounced comeback with the consequences of across the board inflation starting to take its toll on the real economy. Indeed, worsening negative disposable income for households and lower margins hurting corporate profits have considerably elevated the risk of recession back towards the top of the list of concerns with which most economic agents have to contend.

Figure 2: Google Searches for Inflation vs. Recession in Google Trends

Source: Google Trends. Data as at 30 June 2022.

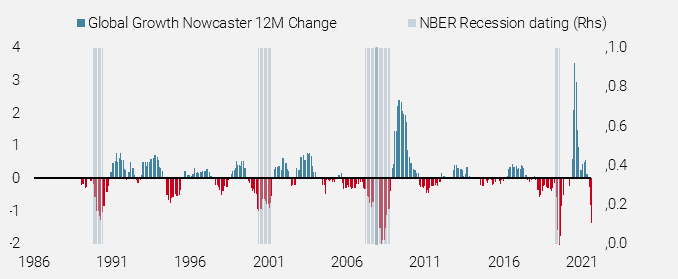

Our Global Growth Nowcaster, which monitors more than 80% of the world’s GDP in near real-time, confirms this trend; its one-year rate of change consistently declining over the first half of this year and now negative for most countries. Figure 3 shows the recession periods (shaded) over the last 35 years as determined by the National Bureau of Economic Research (NBER). Interestingly, any decline of our Growth Nowcaster to its current depths was historically accompanied by a recession, as witnessed in 1990/91, 2001, 2007/2008 and 2020.

In addition, this kind of deceleration is concurrent with low or declining inflation. On average, the decline of -0.7 in our Global Growth Nowcaster over the last 12 months should correspond to a Global Inflation Nowcaster average of -0.36, but it is currently at 1.5. As for momentum, the aforementioned -0.7 decline in our growth indicator usually equates to a fall of -0.6 in our Inflation Nowcaster over 12 months. It is still positive at +0.2, despite the negative readings for our Growth Nowcasters. This suggests that inflation should come down in the near term.

Figure 3: One-year Change in our Global Growth Nowcaster and NBER Recession

Source: Unigestion, NBER. Data as at 30 June 2022.

Robust Portfolios for Uncertain Times

For private equity investors wishing to commit capital in this environment, it is not obvious how to proceed. The combination of an unprecedented market environment coupled with the need to continue to maintain private equity exposure means that many LPs are finding it difficult to move forward with much confidence. Should we expect a soft landing, or rather prepare for a hard landing? The question one needs to answer is how to build a top-performing portfolio in the face of extreme uncertainty – one that is able to withstand the current headwinds. At Unigestion, this is a question we ask ourselves every day.

With over 30 years of private equity investing experience, we have developed a robust and proven investment strategy that is well-suited to all market scenarios.

With over 30 years of private equity investing experience, we have developed a robust and proven investment strategy that is well-suited to all market scenarios. For our direct investment programme, we aim to build exciting portfolios of top-performing, hard-to-access, mid-market companies.

The first step of our strategy is to clearly define our investment themes. We pursue a theme-based, top-down analysis in which themes are defined to give our target investments a structural “tailwind”, making them less dependent on the general economic environment. Our seven core investment themes include Healthcare Reengineered, Personal Wellbeing, Future of Work, Service Efficiency, Sustainable Cities, Resource Efficiency and Climate Transition.

We also apply our investment themes using “bottom-up” local regional knowledge. For each region, we prioritise the themes which are most relevant and impactful on performance, leading us to the most compelling opportunities. In times of uncertainty, it is even more important to have a strong global view as different regions will be affected in different ways, requiring a tailored response.

In a second step, we look for companies within these investment themes with specific characteristics. Using our proactive bottom-up sourcing process, our focus is on companies we expect to thrive in any macro environment.

The three main risks we are currently trying to address include:

Slowing economic growth rates. With growth rates in decline globally, it would be unwise to invest in companies where the investment case is based mainly on GDP growth. Our approach has long been to look for companies where growth is uncorrelated to GDP and rather driven by long-term sector trends and increased efficiencies.

A good example is Freightwise in the US, a deal mentioned previously. In today’s e-commerce-driven world, shipping is no longer just a function, but can become a competitive advantage. The significant cost savings that Freightwise delivers to its customers drives demand for the company’s solutions, irrespective of the general macro environment.

Inflationary pressures. Another current risk is global inflation. The combined effects of the Covid pandemic and the conflict in Ukraine are posing a huge challenge to energy prices, commodities and overall supply chains, leading to rising prices pretty much across the board. This poses a significant threat to many business plans. We aim to counter this risk by focusing on innovative, service-oriented companies who are leaders in their niche markets leading to strong pricing power.

Avania, with headquarters in Europe, is a good example. As a leading full service outsourced Clinical Research Organsiation (CRO) for medical devices, IVDs, biological and cell-based products, Avania’s core offering spans regulatory and strategy consulting, reimbursement, clinical operations, data management, medical writing, and medical services to the fast-growing medical devices sector. Tightening regulations and outsourcing trends are supporting attractive growth and making Avania’s services highly sought after. This is a trend very much in line with our Healthcare Reengineered theme, as the medical devices industry is fast converging toward the pharma industry business model where larger, branded players focus on marketing and distribution, preferring to outsource various clinical research activities to companies like Avania.

Increasing interest rates. The third major risk we see is rising interest rates. After having been spoiled with unprecedentedly low rates, we are now facing rates that are on the rise – and it might be just the beginning. However, the use of leverage has never been a core part of our investment strategy, rather we focus on finding truly exceptional businesses with strong balance sheets where we can create value without needing to rely on financial engineering.

Kindred in the UK illustrates this well. In an effort to avoid additional balance sheet stress while initially strengthening the group and making the first acquisitions, we ensured that Kindred did not take on any leverage. This helped the company to navigate the pandemic and allowed for a more flexible and friendly stance towards staff and clients, meaning no layoffs and the ability to offer large discounts in monthly tuition fees during Covid lockdowns. Once the lockdowns ended, the fully-staffed nurseries were immediately back in business, and today have quickly attained pre-Covid enrollment levels. Furthermore, the group has resumed its acquisition strategy, taking advantage of a multitude of attractive opportunities.

We have been successfully executing our private equity strategy since the 1990s and know what it takes to invest and protect against higher inflation and interest rate environments.

We have been successfully executing our private equity strategy since the 1990s. While some of our team members have been with the firm longer than others, the combined knowledge and intelligence has become ingrained in our culture, giving us a collective long-term memory. We have learned how to manage companies through prior turbulent periods such as the dotcom crash or the GFC. And we remember how to invest and protect against higher inflation and interest rate environments like those we last saw 15 years ago.

This collective experience has allowed us to develop extremely resilient portfolios which have been particularly tested in recent periods of uncertainty and make us well-equipped to face any challenges that may lie ahead.

Unigestion Private Equity Activity

In the first half of 2022, the Unigestion private equity team committed EUR 528m to investments, including EUR 138m invested in seven secondary transactions and EUR 178m invested in seven direct investments and various add-ons. Here are the highlights of some of the investments and exits that we completed in Q2:

In April, Unigestion invested in EQT Ventures III. EQT Ventures is a European Venture Capital firm, part of the globally integrated alternative investment firm EQT, and has a team of 30+ entrepreneurs and operators. It focuses on early stage (seed and series A/B) investments across four industry verticals: Enterprise Tech, Con/Prosumer Tech, Health Tech and Climate Tech. With its proprietary AI-enabled platform Motherbrain, EQT Venture deploys a categorical, data-driven approach across the entire process, above all in deal origination and due diligence. EQT is a pioneer among private equity firms with its purpose-driven approach aiming to make a positive global impact. Back in 2010, EQT was the first Nordic private equity firm to sign up to PRI and since then has been very active in defining ESG industry best practices.

In May, Unigestion invested in J-STAR 5. After approximately six months in the market, the fund was oversubscribed, reaching a size of JPY 75bn (EUR 550m) at the final closing. J-STAR was founded in 2006 by members of the buyout team at JAFCO Co. Ltd., one of the earliest private equity firms in Japan. The firm has a “solution capital” approach, which seeks to create custom-made investment solutions for Japanese small and medium-sized enterprises with enterprise values principally below JPY 10bn (EUR 75m). The firm targets situations such as succession, management buyouts, carve-outs, growth capital, and / or shareholder exits, and will secure controlling or co-controlling positions to best effect operational value-add post-investment. The key target sectors are manufacturing, healthcare, environment, business services, consumer and TMT.

In the same month, Unigestion invested in Ergon V. Ergon is a pan-European manager with several offices across Europe and a team of 20 investment professionals. Ergon V targets mid-market buyouts of family-owned companies headquartered in the Benelux, France, Germany, Italy, and Spain, primarily in the niche industrials, healthcare, retail, consumer, and media & services sectors. In 2018, Unigestion co-invested with Ergon to acquire Opseo (second largest intensive care provider in Germany with over 4,000 employees) and SVT (passive fire protection systems). Opseo is currently valued at 1.5x MOI, while SVT was realised in 2021 delivering a 34% net IRR to Unigestion. The net TVPI (total value to paid-in capital) for SVT was 2.1x.

In June, Unigestion completed an investment in Zeit für Brot, a premium bakery concept with numerous locations in major cities throughout Germany. The company brings the bakery craft back into cities such as Berlin and Frankfurt, offering customers an authentic experience. Since 2009, it has developed a unique concept based on organic products, locally sourced ingredients, on-site open bakeries, craftsmanship, and sustainability in combination with a modern appeal. The combination of these factors has led to ongoing high demand, strong customer satisfaction, and loyalty. In addition, the company sees tangible growth potential in its B2B business and selective acquisition opportunities.

In the same month, Unigestion closed an investment into a single-asset continuation vehicle consisting of Init AG (www.init.de) managed by German-based fund manager Emeram Capital Partners. Init is a provider of digital transformation solutions for German public clients at a Federal and State level. Established in Germany in 1995, the company’s unique end-to-end offering includes digital strategy definition, consulting, content creation and management, software development and hosting through its own datacentres. Due to lower complexity and a better holistic service delivery, customers increasingly favour full-service solutions. Init operates in a large and growing addressable market, supported by multi-billion euro government programmes. Public IT services spend is expected to more than triple by 2025 compared to 2015, fueled by a strong digitisation agenda in the German public sector.

Also in June, Unigestion invested in Resource Eastern European Equity Partners III. Resource Partners was established in 2009 by the core group of the former Carlyle CEE office. Resource Partners is a consumer sector-specialised fund manager active in the CEE region. The manager focuses on investment opportunities predominantly in Poland, and opportunistically in other EU-member countries in the CEE. The manager focuses on founder-owned businesses with growth potential. The firm creates value in its portfolio companies through market consolidation, product extension, professionalisation, implementation of structured budgeting & monitoring processes, and strategic capex investments to strengthen market positions and create sizeable players.

[1] Pitchbook, July 2022.

[2] Preqin, July 2022.

Important information

Past performance is no guide to the future, the value of investments, and the income from them change frequently, may fall as well as rise, there is no guarantee that your initial investment will be returned. This document has been prepared for your information only and must not be distributed, published, reproduced or disclosed (in whole or in part) by recipients to any other person without the prior written consent of Unigestion. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation.

This is a promotional statement of our investment philosophy and services only in relation to the subject matter of this presentation. It constitutes neither investment advice nor recommendation. This document represents no offer, solicitation or suggestion of suitability to subscribe in either the investment vehicles to which it refers or to any securities or financial instruments described herein. Any such offer to sell or solicitation of an offer to purchase shall be made only by formal offering documents, which include, among others, a confidential offering memorandum, limited partnership agreement (if applicable), investment management agreement (if applicable), operating agreement (if applicable), and related subscription documents (if applicable). Such documentation contains additional information material to any decision to invest. Please contact your professional adviser/consultant before making an investment decision.

Where possible we aim to disclose the material risks pertinent to this document. The views expressed in this document do not purport to be a complete description of the securities, markets and developments referred to in it. Reference to specific securities should not be considered a recommendation to buy or sell. Unigestion maintains the right to delete or modify information without prior notice.

Investors shall conduct their own analysis of the risks (including any legal, regulatory, tax or other consequences) associated with an investment and should seek independent professional advice. Some of the investment strategies or financial instruments described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment. These are not suitable for all types of investors. Unigestion has the ability in its sole discretion to change the strategies described herein.

To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks. Actual results could differ materially from those in the forward-looking statements. As such, forward looking statements should not be relied upon for future returns. Targeted returns reflect subjective determinations by Unigestion based on a variety of factors, including, among others, internal modeling, investment strategy, prior performance of similar products (if any), volatility measures, risk tolerance and market conditions. Targeted returns are not intended to be actual performance and should not be relied upon as an indication of actual or future performance.

No separate verification has been made as to the accuracy or completeness of the information herein. Data and graphical information herein are for information only and may have been derived from third party sources. Unigestion takes reasonable steps to verify, but does not guarantee, the accuracy and completeness of information from third party sources. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. All information provided here is subject to change without notice. It should only be considered current as of the date of publication without regard to the date on which you may access the information. Rates of exchange may cause the value of investments to go up or down. An investment with Unigestion, like all investments, contains risks, including total loss for the investor.

Additional Information for US Investors

For US investors, Unigestion is relying on SEC Rule 15a-6 under the Securities Exchange Act of 1934 regarding exemptions from broker-dealer registration for foreign broker dealers. Foreside Global Services, LLC is acting as the chaperoning broker dealer for Unigestion for the purposes of soliciting and effecting transactions with or for U.S. institutional investors or major U.S. institutional investors

The performance figures are based on estimated fees and expenses as well as on the underlying strategy’s estimated performances given by fund managers, administrators, custodians and third party sources at a given date. Where performance is reflected gross of fees, potential investors should be aware that the inclusion of fees, costs and charges will reduce the overall value of performance. Unless otherwise stated, the performance data source are Unigestion, Bloomberg and Compustat.

This information is provided to you solely to give you background information relating to Unigestion, certain strategies it implements and currently offers. Before making an investment decision with respect to the strategy discussed herein, potential investors are advised to consult with their tax, legal, ERISA and financial advisors. Note that not all strategies may be available or suitable for investment by U.S. investors.

This document may contain forward-looking statements, including observations about markets and industry and regulatory trends as of the original date of this document. Forward-looking statements may be identified by, among other things, the use of words such as “expects,” “anticipates,” “believes,” or “estimates,” or the negatives of these terms, and similar expressions. Forward-looking statements reflect Unigestion’s views as of such date with respect to possible future events. Actual results could differ materially from those in the forward-looking statements as a result of factors beyond a strategy’s or Unigestion’s control. Readers are cautioned not to place undue reliance on such statements. No party has an obligation to update any of the forward-looking statements in this document

Return targets or objectives, if any, are used for measurement or comparison purposes and only as a guideline for prospective investors to evaluate a particular investment program’s investment strategies and accompanying information. Performance may fluctuate, especially over short periods. Targeted returns should be evaluated over the time period indicated and not over shorter periods.

The past performance of Unigestion, its principals, shareholders, or employees is not indicative of future returns.

Except where otherwise specifically noted, the information contained herein, including performance data and assets under management, relates to the entire affiliated group of Unigestion entities over time including that of Unigestion UK. Such information is intended to provide the reader with background regarding the services, investment strategies and personnel of the Unigestion entities. No guarantee is made that all or any of the individuals involved in generating the performance on behalf the other Unigestion entities will be involved in managing any client account on behalf of Unigestion U.K. More specific information regarding Unigestion UK is set forth herein where indicated and is available on request.

There is no guarantee that Unigestion will be successful in achieving any investment objectives. An investment strategy contains risks, including the risk of complete loss.

The risk management practices and methods described herein are for illustrative purposes only and are subject to modification.

Legal Entities Disseminating This Document

UNITED KINGDOM

This material is disseminated in the United Kingdom by Unigestion (UK) Ltd., which is authorized and regulated by the Financial Conduct Authority (“FCA”). This information is intended only for professional clients and eligible counterparties, as defined in MiFID directive and has therefore not been adapted to retail clients.

UNITED STATES

This material is disseminated in the United States by Unigestion (UK) Ltd., which is registered as an investment adviser with the U.S. Securities and Exchange Commission (“SEC”). All inquiries from investors present in the United States should be directed to Clients@unigestion.com at Unigestion (UK) Ltd. This information is intended only for institutional clients and qualified purchasers as defined by the SEC and has therefore not been adapted to retail clients.

EUROPEAN UNION

This material is disseminated in the European Union by Unigestion Asset Management (France) SA which is authorized and regulated by the French “Autorité des Marchés Financiers” (“AMF”).

This information is intended only for professional clients and eligible counterparties, as defined in the MiFID directive and has therefore not been adapted to retail clients.

CANADA

This material is disseminated in Canada by Unigestion Asset Management (Canada) Inc. which is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario, Quebec and Newfoundland & Labrador. Its principal regulator is the Ontario Securities Commission (“OSC”). This material may also be distributed by Unigestion SA which has an international advisor exemption in Quebec, Saskatchewan and Ontario. Unigestion SA’s assets are situated outside of Canada and, as such, there may be difficulty enforcing legal rights against it.

SWITZERLAND

This material is disseminated in Switzerland by Unigestion SA which is authorized and regulated by the Swiss Financial Market Supervisory Authority (“FINMA”).

Document issued September 2022.