Active risk management in a changing market environment: be brave but be prepared

ACTIVE RISK MANAGEMENT IN A CHANGING MARKET ENVIRONMENT: BE BRAVE BUT BE PREPARED

Overview

In investment, as in life, taking risk is unavoidable; it is necessary to perform and grow. For us, intelligent risk-taking is about being brave but prepared. This means taking on risks we like, using appropriate measures to assess them, combining them to achieve effective diversification and, finally, being able to adapt quickly to changing market conditions.

We believe that in today’s financial markets, we are experiencing a paradigm shift in terms of economic conditions, central bank policy and investors’ perception. In our view, a true understanding of the risk-reward potential of each investment and the contribution it can make in a portfolio context will be more essential than ever as we move into the next phase of the market cycle.

Adapting Risk Allocation to a Changing Macro Environment

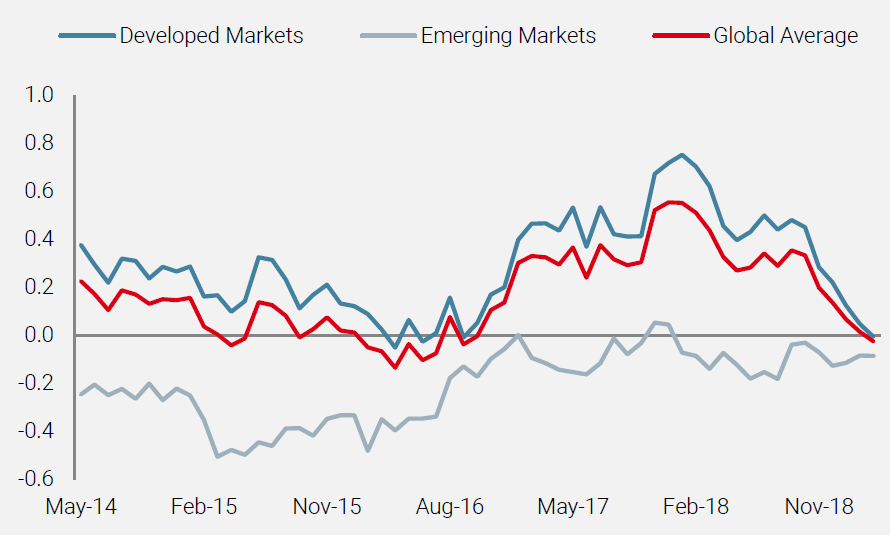

A legitimate question our investors are facing is whether we are late in the economic cycle or moving into a recession. We closely monitor the evolution of economic growth using our proprietary Nowcaster indicators, which aggregate a large number of real-time data series into a gauge of current economic activity. According to our Nowcasters, global growth is now uneven between regions and heading towards below potential growth or even potentially recession. Since February 2018, most developed economies have been in a period of slowdown, which is particularly pronounced in the Eurozone and now visible in the US. This explains the change of stance of major central banks to dovish.

Figure 1: Unigestion Growth Nowcaster

At this stage in an ageing macroeconomic cycle, spikes of market volatility are likely to become more frequent and severe, as we saw in the fourth quarter of 2018, which was the worst quarter for equity markets in decades. Following strong performance at the start of this year, equity markets are back to fair value, but it is worth noting that with economic activity slowing, there is an increased risk of a valuation correction.

Trade wars are also a source of uncertainty. World trade is an essential portion of global GDP growth. A recent study by the World Economic Forum estimates that a 25% increase in US tariffs could reduce global GDP growth by as much as 0.7%. Finally, China remains a source of concern as its debt pile is mounting while its growth is deteriorating, offering little room to manoeuvre in the event of more severe shocks.

The current macroeconomic environment requires a significantly different approach to investing than the one that has prevailed over the last 10 years.

Changing Macroeconomic Conditions Require a Different Approach to Risk Allocation

In the current economic regime, our indicators call for cautiousness, given that the road to market turning points can be long and difficult to time. As our strategies remain fully invested, we look for investment opportunities that offer attractive upside potential with compelling downside protection. This means taking on risks we like, using appropriate measures to assess them, combining them to achieve effective diversification and, finally, being able to adapt quickly to changing market conditions.

The current macroeconomic environment requires a significantly different approach to investing than the one that has prevailed over the last 10 years. In the goldilocks environment of low inflation, synchronised growth and loose monetary policy, investors’ preferred allocation was to be strongly overweight in growth assets. However, in a period where economic growth is decelerating, assets such as equities, private equity and credit should be treated with care as their risk-reward profile is deteriorating. Credit looks particularly vulnerable, as credit spreads are at historic lows and credit tends to fall ahead of equities, notably as companies increase their debt to maintain their profitability.

Distinguishing between slowdown and recession phases is critical: our historical models show that performance between asset classes varies significantly between periods of growth and recession. During the late stages of an expansion, stocks typically outperform bonds. However, during the early stages of a recession, bonds tend to outperform stocks. Furthermore, we anticipate greater market volatility and less stable stock-bond correlations, which are typical when recession risk is increasing.

Diversification Will Be Paramount

During previous slowdowns, government bonds have acted as a powerful diversifier, but their hedging capabilities are now more limited as yields are already at very low levels (at least in Europe). Investors need to broaden the tools they use to diversify their portfolios to include a different exposure to equity and a larger allocation to alternative asset classes.

More generally, given the wide range of possible future outcomes, we believe investors should not focus on a single scenario. Rather, they should aim to construct a strategic asset allocation with the potential to outperform in a variety of environments and be resilient in downturns. In an uncertain macroeconomic environment, where market stress events are likely to be more prevalent, we believe adding a dynamic element to asset allocation models will be essential. It will be important to have the flexibility to tactically dial risk up or down around specific market events, such as central bank announcements or political elections, while remaining invested.

Finally, we believe that now, more than ever, investors need to look beyond conventional measures of risk, such as volatility, when setting asset allocation. Investors should not consider low volatility as a proxy for calm markets, as other risks are lurking beneath the surface. We therefore take a multi-dimensional view and define risk in terms of potential loss of capital, which is the true measure of risk investors face. Our proprietary Expected Shortfall model aims to incorporate risks that are ignored by volatility-based analysis, such as valuation, asymmetry, tail risk and liquidity. By focusing on different aspects of risk, we are less dependent on individual measures, which helps us achieve a more robust risk allocation across our portfolios.

Not All Risks Are Created Equal: Finding Value in Today’s Markets

In this changing and less certain market context, we believe it is time for investors to focus on quality, but with some discerning filters. It will be crucial to be selective and to have the flexibility to adapt. Given our late-cycle view, we expect corporate credit to underperform as lower profitability margins could affect debt repayments. We are particularly concerned about credit market liquidity and prefer to invest with caution in equities to maintain exposure to economic growth.

Allocating to Equities at this Stage of the Cycle

Timing the equity market is difficult. We prefer to remain cautiously invested in equities through diversified portfolios of quality stocks with reasonable valuations.

We expect increasing market volatility to dampen investor appetite for pure market beta exposure in the years ahead. Indeed, the combination of slower profit growth and higher volatility is likely to create more differentiation in returns.

In this environment, we believe equity investors have two choices: attempt to time the market or maintain a constant allocation to equities with a focus on reducing drawdown risks. In our view, timing the equity market is difficult. Instead, we prefer to remain cautiously invested in the asset class through diversified portfolios of quality stocks with reasonable valuations. We believe that this defensive investment style can provide protection during challenging market environments. In contrast to passive low volatility strategies, which are essentially backward-looking, we believe that our focus on quality fundamentals is a more effective way to ensure downside resilience in a changing macroeconomic environment.

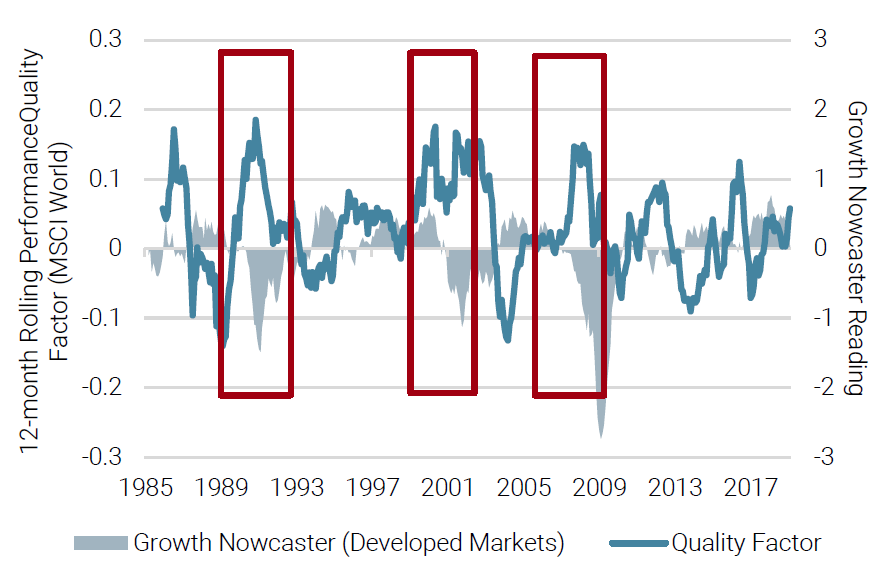

During the late stages of an expansion, equity markets tend to rotate towards high quality companies to defend against the growing risk of a slowdown, rising margin pressure and increased volatility. Companies with high and stable levels of profitability therefore tend to be better positioned as the cycle moves from expansion to recession.

However, here again, investors will need to be selective, as some quality stocks have enjoyed excellent performance and may not offer the protection required in the event of a valuation correction. It will be important to choose not only fairly valued quality stocks, but also to diversify those stocks between sectors, as some areas of the market are less expensive and tend to perform better in a weaker economic environment.

Figure 2: High Quality Companies Tend to Outperform During Periods of Recession

We believe that active equity management will be essential to navigate the market transition. Passive strategies are too prone to excesses (bubbles), as they make no provision for risk allocation: all risks, good and bad, are inherent in the benchmark. In addition, market-cap weighted strategies, which maximise exposure to stocks that have been successful in the past, are more likely to be invested in overvalued and overcrowded positions that are vulnerable to sharp corrections when investors start to sell these stocks.

We recommend dynamically implementing hedges using futures and options to reduce equity exposure when the probability of market stress events increases. We believe that this disciplined risk budgeting approach allows us to lower overall portfolio risk while capturing the equity return premia, increasing the positive asymmetry of returns we aim to deliver for our clients.

However, traditional assets are likely to generate lower returns and become more volatile and correlated going forward. Investors therefore need to find alternative, uncorrelated sources of return to diversify their portfolios.

Diversification into alternative risk premia strategies makes perfect sense at this time of the cycle for investors looking for liquid alternative sources of return.

Alternative Risk Premia Offer a Compelling Source of Diversification

For investors seeking cost-efficient and transparent portfolio diversification, liquid alternative risk premia strategies (ARP) offer a compelling solution, having delivered positive long-term returns with a very low correlation to equities and bonds.

Effective diversification means not just investing in many different assets, but in assets that respond differently to common factors. In that context, diversification into ARP strategies makes perfect sense at this time in the cycle for investors looking for liquid alternative sources of return.

At the heart of risk premia investing is the idea that investors are compensated for accepting risks rather than buying assets: a risk premium is the reward for taking on a specific investment risk. The advantage of ARP strategies is that they remove most market directionality by taking long/short positions to gain a purer exposure to the desired risk premia, thereby enhancing diversification benefits.

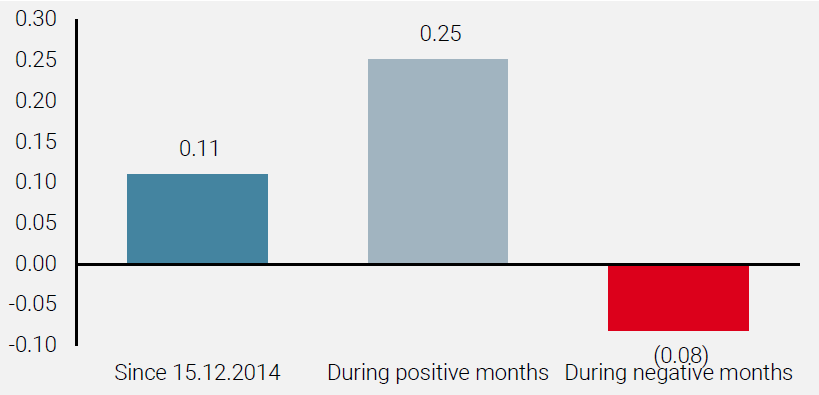

The diversification benefits of ARP strategies, especially during market downturns, are illustrated below.

Figure 3: ARP Exhibit Low Sensitivity to Equities (as measured by Beta to the MSCI World Index)

Over the short term, risk premia can be volatile and ARP are no exception. Performance of ARP strategies in 2018 was disappointing, hampered by a rare combination of factors, including an unfavourable macroeconomic backdrop, inflation fears, heightened market volatility, high dispersion between US stocks and a lack of long-term trends. However, ARP strategies have recovered well from similar, short-term setbacks in the past and indeed in 2019 to date, they have recouped part of last year’s losses. In addition, the diversification benefits still held true in 2018, with the SG Multi Alternative Risk Premia index delivering a 0.1 beta to MSCI AC World USD index and a 0.2 beta to the Bloomberg Global Aggregate USD-hedged index.

Allocate Selectively to Private Equity as a Performance Booster

We also believe that a selective allocation to private equity offers strong potential to enhance overall portfolio performance as well as diversification in an environment of lower returns from traditional assets. Historically, private equity has performed well in late-cycle environments and has been an effective hedge against rising (or unexpected spikes in) inflation. While private company valuations may fall during an economic slowdown, the declines are usually less pronounced than in public markets. In addition, private equity is one of the few asset classes forecast to deliver high single digit returns in the next cycle.

That said, some caution is needed. Volatility in equity markets could weigh on private equity, as correlation analysis shows that private equity does tend to move somewhat in line with public equity, although it is less subject to market sentiment. Private equity, especially buyouts, also shows some correlation to the high yield market as it needs leverage and capital-efficient structures to generate required returns.

Private equity offers strong potential to enhance overall portfolio performance as well as diversification.

For these reasons, our private equity allocation will be highly selective. The breadth of the market today allows investors to carefully manage their exposure to favour more defensive sectors or those benefiting from long-term secular trends, including the ageing population or the decarbonisation of our economy. We therefore favour sectors such as education, healthcare and renewable energy.

It will be important to invest in companies that are resilient in their own right thanks to strong market position, management and financials and can therefore deliver the required base case return through revenue growth and operational improvements. We will continue to avoid companies with excessive leverage, with the average company debt multiples in our portfolios currently below 3x EBITDA. We will also maintain price discipline in a competitive environment where there are record amounts of committed, but not invested, capital (’dry powder’).

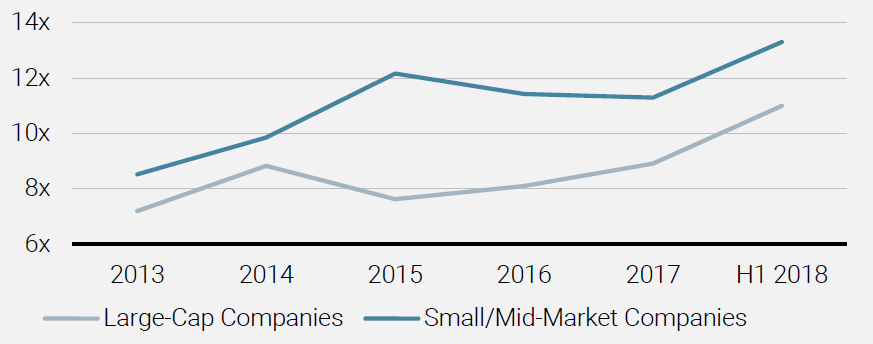

On a multiple of EBITDA basis, valuations of small and mid-market deals in North America and Europe can be significantly lower than those of large-cap deals.

Given the level of competition, we continue to favour strategies that allow sourcing deals outside of large auctions, such as small and mid-market buyouts. Smaller deals require specialist local knowledge and strong operational capabilities. They are by nature less competitive than larger deals. Furthermore, the small and mid-market is less correlated to GDP growth and currently enjoys lower valuations, as shown in Figure 4. On a multiple of EBITDA basis, valuations of small and mid-market deals in North America and Europe can be significantly lower than those of large-cap deals.

Figure 4: Valuations of Small/Mid-Market Vs Large-Cap Companies (Price to EBITDA Multiples)

Based on analysis of Unigestion’s historical investments, approximately 50% of value creation in small and mid-market companies is driven by EBITDA growth. For large companies, almost 80% of value creation came from the use of leverage, while 10% came from EBITDA growth.

Long-term Trends That Are Likely To Influence Active Risk-Taking

A number of trends are emerging that we believe are likely to increasingly influence the way investors take risk in the future.

Increasing Investor Homogeneity Will Reward a Longer-term, Contrarian Approach

Too much homogeneity in market participant actions can lead to a more fragile investment environment where trends tend to persist longer, but often reverse more brutally.

Financial markets are complex: they are highly interconnected, non-linear and adaptive. Market behaviour is driven by investor behaviour, but investor behaviour itself is shaped by market behaviour. This recursive relationship, known as reflexivity, can play a role in creating and sustaining positive feedback loops. Furthermore, financial markets are influenced by the macroeconomic environment, which in turn is shaped to a certain extent by central bank policy, and vice versa.

Boom and bust cycles are not inconsistencies in this complex world. Rather, they are a natural consequence of a system in which the interactions between the participants are more significant than the actions of any participant in isolation. Financial markets are an ecosystem much like the natural world. Booms and busts are the enduring forces that allow markets to move back into equilibrium.

However, this self-regulating mechanism could be put at risk by exponential growth in rules-based investment strategies, notably passive, smart beta, risk parity and target volatility strategies. These can create self-fulfilling phenomena because of too much homogeneity in market participant actions. This can lead to a more fragile investment environment where trends tend to persist longer, but often reverse more brutally.

So what does that mean for investors and the way they manage risk? In our view, one consequence is that investors will have to take a longer-term view when allocating to risk and be capable of being contrarian for longer. This will mean accepting higher tracking error and longer periods of relative underperformance in order to build outperformance over the long term. Investors should not forget that the real investment risk they face is losing capital, not tracking error, and that they need to take active decisions in order to avoid permanent loss of capital.

While many investors claim they invest for the long term, it is very rare that short-term performance – and short-term benchmark comparisons – does not come into consideration. Adopting a truly long-term approach to investment is one of the few genuine opportunities investors can hope to exploit. However, it may require investors to go against the crowd and to look far enough ahead.

In order to adapt their portfolios for longer lives and retirements, we believe investors will need to take on more – not less – risk.

Demographic Trends Could Paradoxically Increase Demand for Higher Risk Assets

Increasing life expectancy worldwide is likely to influence the global economy and therefore the way investors allocate their capital. In order to adapt their portfolios for longer lives and retirements, we believe investors will need to take on more – not less – risk.

Traditional theory dictates that, as retirement nears, investors should not only save more, but should also allocate a greater proportion of their savings to lower risk assets, such as government bonds. However, investing too much, too soon in bonds is not sustainable in the long term, as it is unlikely to deliver the necessary returns to fund longer retirements, particularly given the low levels of real bond yields in most major markets.

Consequently, we believe that the asset allocation model of the future will be different than today. One way to address this problem would be to invest in higher risk assets, including equities and illiquid assets. As longer lifespans prolong investment horizons, we believe that investors’ attitude toward private assets could change, as the liquidity profile of such investments are aligned with longer retirement periods.

Managing ESG Creates Risks and Opportunities For Active Managers

Our fiduciary duty to our clients is to deliver long-term sustainable returns. This means investing responsibly in companies, industries and assets where there is an objective to create a sustainable future for society, as this kind of investment should generate better long-term performance going forward for our investors. We believe that integrating ESG criteria into our investment decision-making processes is essential to better manage the risk of our investments.

Companies that do not pursue sustainable practices on a day-to-day basis create operational and reputational risks within their businesses and to their business model. Regulation can make or break entire industries. Whether it is about tax, cutting emissions in polluting industries or regulating digital companies, these can have a direct impact on the companies in which we invest. Anticipating and avoiding these risks will be key.

Sustainability will be a long-term driver of change in markets, countries, sectors and companies that will create not only risks, but also opportunities for fruitful investment.

Sustainability will be a long-term driver of change in markets, countries, sectors and companies that will create not only risks, but also opportunities for fruitful investment. As the global community seeks to address the numerous environmental and social challenges it faces, companies that can demonstrate forward thinking in tackling these issues are more likely to spot trends early and adapt accordingly. We therefore seek to invest in companies with meaningful sustainable business practices, which are more likely to be leaders and innovators over time.

The Way Forward

Active risk management will be more important than ever as we move into the next phase of the economic cycle. In an environment where macroeconomic conditions are oscillating between late-cycle growth and recession, investors need to adopt a selective approach to risk allocation.

For us, intelligent risk-taking is about being brave but prepared. It requires a multi-dimensional view that looks beyond traditional risk measures, to truly understand the risks worth taking and those to avoid. This allows us to take risks with an asymmetric return profile where upside potential is greater than the downside risk. The goal is then to combine them to achieve effective diversification and, finally, be able to adapt quickly to changing market conditions.

After a decade of strong, relatively uninterrupted growth, traditional asset classes are unlikely to deliver as they have in the past and investors will need to diversify their portfolios with alternative sources of return. However, the road to market turning points can be long and punctuated by more frequent market stress events. While it will be important to remain cautiously invested in growth assets, a more selective and dynamic approach will be essential to adjust portfolio risk opportunistically as the probability of market stress rises and the macroeconomic environment moves toward potential recession. As risk is constantly evolving, investors will also need to look far enough ahead. We believe that actively anticipating and managing risk, having the courage to stand against the crowd and adopting a truly long-term approach is the best way to deliver the investment returns our investors expect.

APPENDIX

Unigestion Alternative Risk Premia (USD)

31 December 2016 Through 31 December 2018

| Year | Composite Return Gross of Fees |

Composite Net Return | Benchmark Return | Number of Accounts | Internal Dispersion | Composite 3-Yr Std Dev | Benchmark 3-Yr Std Dev | Composite AUM (M) | Firm AUM (M) |

| 2017 | 10.24% | 8.59% | 1 | – | – | – | 135.31 | 22,340.80 | |

| 2018 | -4.88% | -6.30% | – | 2 | – | – | – | 254.21 | 21,403.49 |

Special Disclosure: During March 2019, it was discovered that the 2018 composite gross return was stated incorrectly. It has since been corrected. For presentations prior to 31.03.2018 the strategy was measured against the LIBOR 3M USD+7%. Beginning April 2018 the firm determined that the benchmark did not accurately reflect the strategy mandate and the benchmark was removed.

Definition of the Firm: For the purposes of applying the GIPS Standards, the firm is defined as Unigestion. Unigestion is responsible for managing assets on the behalf of institutional investors. Unigestion invests in several strategies for institutional clients: Equities, Hedge Funds, Private Assets and the solutions designed for the clients of our Cross Asset Solution department. The GIPS firm definition excludes the Fixed Income Strategy Funds, which started in January 2001 and closed in April 2008, and the accounts managed for private clients. Unigestion defines the private clients as High Net Worth Families and Individual investors.

Policies: Unigestion policies for valuing portfolios, calculating performance, and preparing compliant presentations are available upon request.

Composite Description: The Alternative Risk Premia composite consists of accounts which aim to deliver high risk-adjusted returns of cash +7% gross over 3 to 5 year investment horizon, while protecting capital during market downturns. The accounts within the composite select the universe components presenting best positioning according to quantitative criteria including but not restricted to Macro directional, Yield captureCarry, Trend following or Equity factors. In order to reduce exposure to general trends in markets and to seek to maximize the absolute return to risk ratio, the accounts essentially rely on systematic long-short strategies.

Benchmark: Because the composites strategy is absolute return and investments are permitted in all asset classes, no benchmark can reflect this strategy accurately.

Fees: Returns are presented gross of management fees, administrative fees but net of all trading costs and withholding taxes. The maximum management fee schedule is 1.5% per annum. Net returns are net of model fees and are derived by deducting the highest applicable fee rate in effect for the respective time period from the gross returns each month.

List of Composites: A list of all composite descriptions is available upon request.

Minimum Account Size: The minimum account size for this composite is 5’000’000.- USD.

Valuation: Valuations are computed in US dollars (USD). Performance results are reported in US dollars (USD).

Internal Dispersion & 3YR Standard Deviation: The annual composite dispersion presented is an asset-weighted standard deviation calculated for the accounts in the composite the entire year. When internal dispersion is not presented it is as a result of an insufficient number of portfolios in the composite for the entire year. When the 3 Year Standard Deviation is not presented it is as a result of an insufficient period of time.

Compliance Statement Unigestion claims compliance with the Global Investment Performance Standards(GIPS®) and has prepared and presented this report in compliance with the GIPS standards. Unigestion has been independently verified for the periods 1 January 2003 to 31 December 2016. The verification report(s) is/are available upon request. Verification assesses whether (1) the firm has complied with all the composite construction requirements of the GIPS standards on a firm-wide basis and(2) the firms policies and procedures are designed to calculate and present performance in compliance with the GIPS standards. Verification does not ensure the accuracy of any specific composite presentation.

Unigestion Global Equity Risk Premia Market Neutral (USD)

31 May 2016 Through 31 December 2018

| Year | Composite Return Gross of Fees |

Composite Net Return | Benchmark Return | Number of Accounts | Internal Dispersion | Composite 3-Yr Std Dev | Benchmark 3-Yr Std Dev | Composite AUM (M) | Firm AUM (M) |

| 2016¹ | -2.19% | -2.76% | 0.23% | 1 | – | – | – | 75.54 | 18’144.46 |

| 2017 | 5.54% | 4.48% | 1.06% | 1 | – | – | – | 19.67 | 22’340.80 |

| 2018 | -5.92% | -6.86% | 1.94% | 1 | – | – | – | 41.03 | 21’403.49 |

1: This year is incomplete, it starts in May.

Definition of the Firm: For the purposes of applying the GIPS Standards, the firm is defined as Unigestion. Unigestion is responsible for managing assets on the behalf of institutional investors. Unigestion invests in several strategies for institutional clients: Equities, Hedge Funds, Private Assets and the solutions designed for the clients of our Cross Asset Solution department. The GIPS firm definition excludes the Fixed Income Strategy Funds, which started in January 2001 and closed in April 2008, and the accounts managed for private clients. Unigestion defines the private clients as High Net Worth Families and Individual investors.

Policies: Unigestion policies for valuing portfolios, calculating performance, and preparing compliant presentations are available upon request.

Composite Description: The Equity Global Risk Premia Market Neutral composite was defined on 31.05.2016. The strategy offers investment opportunities in Global equity markets through a selection made by the manager based on qualitative criteria such as “Valuation”, “Momentum”, “Small Caps” or “Quality”, while relying on a long/short-type strategy to minimise equity market risk.

Benchmark: The benchmark is the ICE LIBOR USD 1 Week, which is designed to measure the average rate at which a LIBOR contributor bank can obtain unsecured funding in the London interbank market for a week, in USD. Benchmark returns are net of withholding taxes.

Fees: Returns are presented gross of all fees: management fees, performance fees, custodian fees but net of withholding taxes and transaction costs. The maximum management fee schedule is 1% per annum. Net returns are net of model fees and are derived by deducting the highest applicable fee rate in effect for the respective time period from the gross returns each month.

List of Composites: A list of all composite descriptions is available upon request.

Minimum Account Size: The minimum account size for this composite is 5’000’000.- USD.

Valuation: Valuations are computed in US dollars (USD). Performance results are reported in US dollars (USD).

Internal Dispersion & 3YR Standard Deviation: The annual composite dispersion presented is an asset-weighted standard deviation calculated for the accounts in the composite the entire year. When internal dispersion is not presented it is as a result of an insufficient number of portfolios in the composite for the entire year. When the 3 Year Standard Deviation is not presented it is as a result of an insufficient period of time.

Compliance Statement Unigestion claims compliance with the Global Investment Performance Standards(GIPS®) and has prepared and presented this report in compliance with the GIPS standards. Unigestion has been independently verified for the periods 1 January 2003 to 31 December 2016. The verification report(s) is/are available upon request. Verification assesses whether (1) the firm has complied with all the composite construction requirements of the GIPS standards on a firm-wide basis and(2) the firms policies and procedures are designed to calculate and present performance in compliance with the GIPS standards. Verification does not ensure the accuracy of any specific composite presentation.

Unigestion Multi Asset Risk-Targeted (USD)

31 December 2014 Through 31 December 2018

| Year | Composite Return Gross of Fees |

Composite Net Return | Benchmark Return | Number of Accounts | Internal Dispersion | Composite 3-Yr Std Dev | Benchmark 3-Yr Std Dev | Composite AUM (M) | Firm AUM (M) |

| 2015 | -1.61% | -2.80% | – | 1 | – | – | – | 127.24 | 15’550.31 |

| 2016 | 5.05% | 3.79% | – | 1 | – | – | – | 129.66 | 18’144.46 |

| 2017 | 11.16% | 9.82% | – | 1 | – | – | – | 169.51 | 22,340.80 |

| 2018¹ | -2.91% | -4.08% | – | 1 | – | – | – | 286.93 | 21,403.49 |

Special Disclosure: For presentations prior to 31.03.2018 the strategy was measured against the LIBOR 3M USD + 4%. Beginning April 2018 the firm determined that the benchmark did not accurately reflect the strategy mandate and the benchmark was removed.

Definition of the Firm: For the purposes of applying the GIPS Standards, the firm is defined as Unigestion. Unigestion is responsible for managing assets on the behalf of institutional investors. Unigestion invests in several strategies for institutional clients: Equities, Hedge Funds, Private Assets and the solutions designed for the clients of our Cross Asset Solution department. The GIPS firm definition excludes the Fixed Income Strategy Funds, which started in January 2001 and closed in April 2008, and the accounts managed for private clients. Unigestion defines the private clients as High Net Worth Families and Individual investors.

Policies: Unigestion policies for valuing portfolios, calculating performance, and preparing compliant presentations are available upon request.

Composite Description: The Multi Risk Targeted (Medium) composite was defined on 15 December 2014. It consists of accounts which aim to deliver consistent smooth returns of cash + 5% gross of fees across all market conditions over a 3-year rolling period. It seeks to achieve this by capturing the upside during bull markets while protecting capital during market downturns.

Benchmark: Because the composites strategy is absolute return and investments are permitted in all asset classes, no benchmark can reflect this strategy accurately.

Fees: Returns are presented gross of management fees, administrative fees but net of all trading costs and withholding taxes. The maximum management fee schedule is 1.2% per annum. Net returns are net of model fees and are derived by deducting the highest applicable fee rate in effect for the respective time period from the gross returns each month.

List of Composites: A list of all composite descriptions is available upon request.

Minimum Account Size: The minimum account size for this composite is 5’000’000.- USD.

Valuation: Valuations are computed in US dollars (USD). Performance results are reported in US dollars (USD).

Internal Dispersion & 3YR Standard Deviation: The annual composite dispersion presented is an asset-weighted standard deviation calculated for the accounts in the composite the entire year. When internal dispersion is not presented it is as a result of an insufficient number of portfolios in the composite for the entire year. When the 3 Year Standard Deviation is not presented it is as a result of an insufficient period of time.

Compliance Statement Unigestion claims compliance with the Global Investment Performance Standards(GIPS®) and has prepared and presented this report in compliance with the GIPS standards. Unigestion has been independently verified for the periods 1 January 2003 to 31 December 2016. The verification report(s) is/are available upon request. Verification assesses whether (1) the firm has complied with all the composite construction requirements of the GIPS standards on a firm-wide basis and(2) the firms policies and procedures are designed to calculate and present performance in compliance with the GIPS standards. Verification does not ensure the accuracy of any specific composite presentation.

Important Information

This document is for the use of professional investors only and not for use by retail investors.

Past performance is no guide to the future, the value of investments can fall as well as rise, there is no guarantee that your initial investment will be returned.

This document has been prepared for your information only and must not be distributed, published, reproduced or disclosed by recipients to any other person.

This is a promotional statement of our investment philosophy and services only in relation to the subject matter of this presentation. It constitutes neither investment advice nor recommendation. This document represents no offer, solicitation or suggestion of suitability to subscribe in the investment vehicles it refers to. Please contact your professional adviser or consultant before making an investment decision. Where possible we aim to disclose the material risks pertinent to this document, and as such these should be noted on the individual document pages. Please contact Unigestion for a complete list of all the applicable risks.

Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment. These are not suitable for all types of investors. To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks. As such, forward looking statements should not be relied upon for future returns.

Data and graphical information herein are for information only and may have been derived from third party sources. Unigestion takes reasonable steps to verify, but does not guarantee, the accuracy and completeness of this information. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. All information provided here is subject to change without notice. It should only be considered current as of the date of publication without regard to the date on which you may access the information. Rates of exchange may cause the value of investments to go up or down. An investment with Unigestion, like all investments, contains risks, including total loss for the investor.

Backtested or simulated performance is not an indicator of future actual results. The results reflect performance of a strategy not currently offered to any investor and do not represent returns that any investor actually attained. Backtested results are calculated by the retroactive application of a model constructed on the basis of historical data and based on assumptions integral to the model which may or may not be testable and are subject to losses.

Changes in these assumptions may have a material impact on the backtested returns presented. Certain assumptions have been made for modelling purposes and are unlikely to be realized. No representations and warranties are made as to the reasonableness of the assumptions. This information is provided for illustrative purposes only. Backtested performance is developed with the benefit of hindsight and has inherent limitations. Specifically, backtested results do not reflect actual trading or the effect of material economic and market factors on the decision-making process. Since trades have not actually been executed, results may have under- or over-compensated for the impact, if any, of certain market factors, such as lack of liquidity, and may not reflect the impact that certain economic or market factors may have had on the decision-making process. Further, backtesting allows the security selection methodology to be adjusted until past returns are maximized. Actual performance may differ significantly from backtested performance.

Unigestion SA is regulated by the Swiss Financial Market Supervisory Authority (FINMA). Unigestion (UK) Ltd is authorised and regulated by the Financial Conduct Authority (FCA) and SEC registered. Unigestion Asset Management (France) SA is regulated by the “Autorité des Marchés Financiers” (AMF). Unigestion (Luxembourg) SA is an Alternative Investment Fund Manager authorised by the Commission de Surveillance du Secteur Financier (CSSF) under the Luxembourg law of 12 July 2013 on AIFM. Unigestion Asset Management (Canada) Inc., with offices in Toronto and Montreal, is regulated in Canada by the securities regulatory authorities in Ontario, Quebec; Alberta, Manitoba, Saskatchewan, Nova Scotia, New Brunswick and British Columbia. Its principal regulator is the Ontario Securities Commission. Unigestion Asia Pte Ltd is regulated in Singapore by the MAS, as Capital Market Services (CMS) license holder and Exempt Financial Adviser under the Securities and Futures Act and Financial Advisers Act.

Document issued April 2019.