Alternative risk premia strategies: why the results are so different?

The popularity of alternative risk premia (ARP) is growing and strategies that focus on ARP are increasingly being incorporated into institutional portfolios. The attraction of this approach is that ARP can mimic strategies that have historically only been available through hedge fund vehicles, but with more favourable liquidity and cost characteristics. However, as investors familiarise themselves with this newer universe of investment strategies, the disparity of results that is being delivered by these solutions in practice is raising some questions. This paper aims to highlight some of these variations, provide an explanation for them and to also provide some suggestions for investors considering this exciting new investment approach. In our view, there are three elements an investor should consider: 1-It is important to scrutinise a manager’s definition of individual risk premia; despite being broadly categorised under the same name, we have found that risk premia can have significantly different performances across investment solutions. 2-The methodology that managers use to allocate between risk premia should be closely scrutinised; our observations have shown that even portfolios managed using “equal risk contributions” can be defined in a number of ways, which can have implications on the end result. 3-The benefits of diversifying across several alternative risk premia managers should be considered, as the resulting low correlation could help investors obtain improved risk-adjusted performance without significantly increasing their portfolio’s beta to traditional equity markets.

Not all alternative risk premia are born equal

In theory, a risk premium should be rule-based, transparent and replicable, so that an investor might expect consistent behaviour across investment solutions (see [1] in the References section). However, we have found that in practice the devil is in the detail.

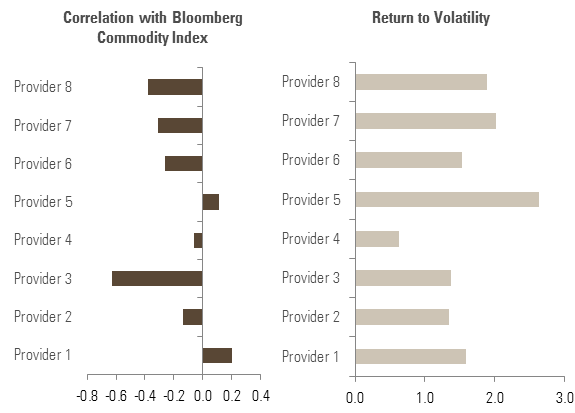

In Figure 1, we have updated the results from a study that was featured in one of our previous papers “Alternative risk premia investing: from theory to practice” ([2]). Here, we compared the return to risk, and correlation with an underlying market index, for a set of commodity carry solutions offered by different providers (such as banks). All solutions that focus on this area use the same name, share a very similar definition of commodity carry (i.e. the maximisation of roll-yield across a set of commodity futures), but the results are highly diverse and can lead to very different portfolio outcomes.

Figure 1: Commodity Carry: illustrating the dispersion of performances

We have found that small differences in the way individual alternative risk premia are defined can lead to very different results among providers

A recent study ([1]) relates this finding to a larger set of strategies in the ARP space. It illustrates that while a few strategies display reasonably consistent behaviour across providers – such as G10 foreign exchange carry – the dissimilarity for most risk premia is substantial.

A strategy that appears to be particularly inconsistent across providers is equity value. Our findings here echo that of other research articles ([3], [4]) which suggest that even the canonical Fama-French definition of value is subject to some considerable questions around its robustness. Most investors would accept that equity value is a promising investment style, but it seems that there is much less agreement on how to define “value”.

As mentioned in our previous paper ([2]), small differences in the way individual alternative risk premia are defined can lead to very different results among providers, particularly as these strategies often apply long-short trading, as well as leverage. These portfolio construction techniques can magnify the nuances of seemingly small differences in approach. In this light, alternative risk premia often inherit some of the characteristics of their hedge fund heritage: the broader the universe, and the more complex and idiosyncratic the strategy, the bigger the resulting differences. As a counter example, given the universe for G10 foreign exchange carry is well-defined and opportunities are largely based on simplistic short-term interest rate differentials versus a base currency (such as US dollar), there is little room for significant differences in definition.

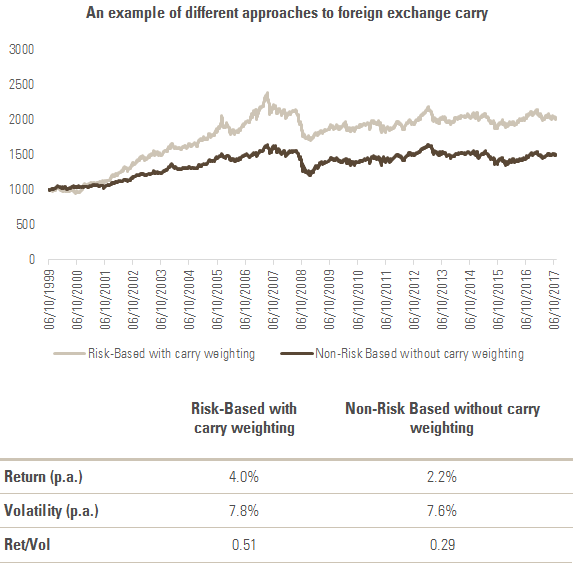

However, even for seemingly homogeneous strategies, we have found that there can be inherent characteristics that have the potential to significantly impact the end result. For example, the way in which the underlying components of a portfolio are scaled can purely be equal weighted or can also be risk-based and incorporate the strength of a perceived opportunity (i.e. the magnitude of potential carry among carry strategies or the strength of past returns for trend-following strategies) this can have meaningful impact on the end result. In Figure 2, we consider foreign exchange carry and the impact of these different portfolio construction approaches.

Figure 2: Portfolio construction matters even for simple strategies

At Unigestion, we apply a rigorous validation methodology across all of our individual risk premia strategies

This illustrates the importance of understanding how managers construct individual risk premia, as results can be quite different.

In practice, the difference in results of individual risk premia can be exacerbated by overfitting bias in their design – i.e. that providers are frequently tempted to implement the strategies that have the best backtested results. There is ample evidence that most portfolios designed this way result in very poor real-life results ([1] and [5]).

At Unigestion, we apply rigorous validation methodologies across all of our individual risk premia strategies. Moreover, we never invest in a strategy unless we understand its rationale and we get a sense of when it is expected to lose money (i.e. which economic and market conditions). This means that among the current risk premia we are using, the vast majority have Sharpe Ratios well below 1 in our backtests. Accordingly, we believe it is wise to apply a level of conservatism regarding return expectations and to understand when a strategy can underperform.

Allocation matters much more than people think

As we have shown, the fact that individual alternative risk premia can behave very differently is a source of disparity for investment results. In practice, this is amplified further when we seek to combine different types of risk premia in a diversified portfolio.

In our view the topic of allocation across alternative risk premia has been largely overlooked. One reason for this could be that many think it is not worth the effort, as “timing” the evolution of risk premia is very difficult. Conversely, we have devoted a lot of time and effort to study this topic and our analysis has shown us that there is a benefit to managing portfolios of risk premia dynamically – you can learn more of our findings on this topic in our separate paper, ‘A Macro Risk-Based Approach to Alternative Risk Premia Allocation’ ([10]).

No matter what one thinks of the virtues of tactical allocation, we believe the way strategic allocation is defined, when considering allocations across alternative risk premia, is important. Research has shown that the common approach in the industry is to build strategic allocation among risk premia based on the equal risk contribution principle (ERC, [6]). ERC, and its cousins, such as equal weighted volatility ([7] [8]*), have strong academic backing and have proven very popular for practitioners. One of the reasons is that, unlike the Markowitz allocation approach, they do not require investors to formulate views on the long-term returns of strategies. Hence, it is a more agnostic approach, relying on just a few parameters and is fairly simple to apply.

We believe allocation across alternative risk premia has been largely overlooked, yet we have found that there is a benefit to managing portfolios of risk premia dynamically

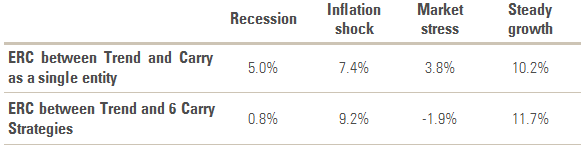

However, we believe there is a practical issue with this approach as it is sensitive to the way risk is defined – for example the use of a volatility measure would lead to a different portfolio to one focusing on drawdown. Furthermore, the way in which ERC is applied can also have a significant impact on the portfolio outcome, particularly during periods of recession and market stress episodes. In Table 1, we illustrate this by looking at two ERC portfolios which have been based on the same universe of trend-following and carry strategies. The difference is that in one portfolio, the six individual carry strategies are considered as a single risk entity, hence both the trend and carry elements of the portfolio are given the same risk budget; in the other portfolio, each of the six carry strategies are considered individually, hence the bulk of the portfolio’s total risk budget ([6/7]) has been assign to these carry strategies.

Table 1: Average annualised returns during different macroeconomic regimes

Performance is generally more balanced across key macroeconomic regimes in the first case, and importantly provides protection during periods of recession and market stress. Therefore, while this example is admittedly extreme, it shows that contrary to some beliefs or assertions, a “neutral” allocation to alternative risk premia is not easy to define and requires active choices.

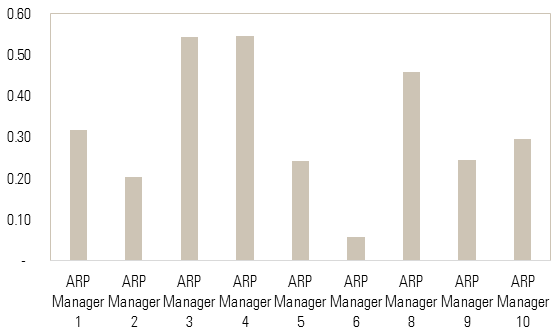

In practice, we have found that the providers of combined alternative risk premia strategies do make active choices. To illustrate this, Figure 3 shows the beta of ten real-life alternative risk premia strategies to trend-following risk premia, using simple regressions. We have chosen to use trend-following risk premia as a basis for this analysis as not only is it a commonly held strategy within this universe, but it can also hold a considerable portfolio weighting.

Figure 3: Beta of alternative risk premia funds to trend-following

In our view, the composition of an alternative risk premia portfolio needs careful implementation, such as the frequency of rebalancing and the consideration of cost efficiencies

This analysis shows that some funds exhibit significant exposure to trend-following risk premia, while others showed very little exposure. Given trend-following is, in most applications, a high risk target and directional strategy there is little doubt that this difference will foster a wide dispersion of portfolio returns.

Not sleeping on slippage and other real-life costs

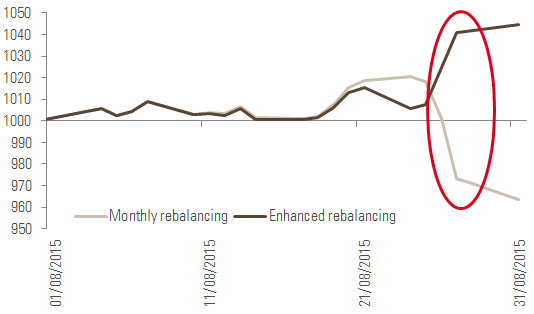

Once the investor has defined their theoretical portfolio of alternative risk premia, it still needs to be brought to market. In our view, the composition of such a portfolio needs careful implementation and many parameters enter into this equation. Firstly, the frequency of how often the portfolio will be rebalanced matters. On the cost-side, the frequency of rebalancing can affect high turnover strategies, such as equity momentum. Moreover, rebalancing based around the refreshed signals or risk adjustments can lead to significant differences in performance, particularly in times of market volatility. In Figure 4, we illustrate the impact of rebalancing volatility carry premia during August 2015, a month characterised by violent shifts in the VIX Index, as well as term-structures.

Figure 4: Rebalancing of volatility carry – strategy performance

At Unigestion, we evaluate all the components of our portfolio on a daily basis (individual signals, active allocation signals, risk estimates, etc), but only trade when the tracking error between current and target allocations moves above a defined threshold. This is assessed at the individual risk premia and at the portfolio level. This constant evaluation of our portfolio allows us to rebalance as often and as quickly as needed, while avoiding trading market noise by not rebalancing when signals and market conditions have not significantly changed.

We believe investors should hold a range of diversified alternative risk premia strategies, as the correlation between them is often low and can significantly improve riskadjusted returns

Finally, portfolios investing in multiple ARP strategies can benefit from the netting of positions in individual risk premia. Whereas, a solution formed of strategies bought individually, often from banks, would not have such cost savings benefits. On that note, the imposition of performance fees – which is fairly unusual in this space – can add further complexity.

So how should investors approach alternative risk premia?

We have seen that there are several structural reasons why alternative risk premia solutions differ in terms of practical results. In our view, this is something investors should take into consideration. So what exactly should they do?

Firstly, we believe investors should conduct due diligence at the same level as they would for a systematic hedge fund programme. While alternative risk premia strategies may bring better liquidity, higher transparency and lower fees, the managers use similar techniques to those used by systematic hedge funds and should be evaluated in a similar way.

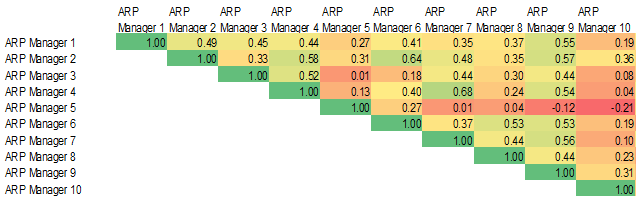

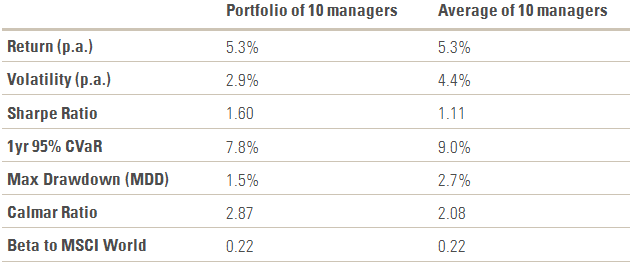

Secondly, we believe investors should view ARP strategies as an opportunity to further diversify their portfolios. In many asset classes, adding too high a number of actively managed strategies can lead to the diversification benefits being cancelled out. Figure 5 illustrates that this is not necessarily the case for alternative risk premia managers as the correlation between key strategies is intrinsically low. Table 2 shows that this low correlation also significantly improves the risk-adjusted returns of a diversified portfolio of managers compared to the average for each of these managers on an individual basis, without substantially increasing the beta to traditional markets (in this case, equities).

In short, there is a reason why alternative risk premia strategies are garnering such interest at present – their steady risk-return potential alongside a lower correlation profile should add value to most diversified portfolios. However, as we have shown there is a lot of variety residing under the ARP umbrella and, in our view, investors need to look under the bonnet to make sure their chosen strategies have the potential to deliver what is required of them.

Figure 5: Correlation among alternative risk premia solutions and with MSCI World

Table 2: Performance statistic comparison

References

[1] Naya F., Tuchschmid N. (2017), Alternative risk premia: Is the selection process important?, SSRN working paper.

[2] Blin O., Lee J., Teiletche J. (2017), Alternative risk premia investing: from theory to practice, Unigestion research paper.

[3] Asness C., Frazzini A. (2013), The devil in HML’s details, The Journal of Portfolio Management, Vol 39, No.4, pp. 49-68.

[4] Israel R., Jiang S., Ross A. (2017), Craftsmanship alpha: An application to style investing, SSRN working paper.

[5] Suhonen A., Lennkh M., Perez F. (2017), Quantifying backtest overfitting in alternative beta strategies, The Journal of Portfolio Management, Vol 43, No 2, pp. 91-105.

[6] Maillard S., Roncalli T., Teiletche J. (2010), The properties of equally weighted risk contribution portfolios, The Journal of Portfolio Management, Vol. 36, No. 4, pp. 60-70.

[7] Kirby C., Ostdiek B. (2012), It’s all in the timing: simple active portfolio strategies that outperform Naïve diversification, The Journal of Financial and Quantitative Analysis, Vol. 47, No 2, pp. 437-467.

[8] Moreira A., Muir T. (2017), Volatility-managed portfolios, The Journal of Finance, Vol. 72, No. 4, pp. 1611-1644.

[9] Jurczenko E., Michel T., Teiletche J. (2015), A unified framework for risk-based investing, The Journal of Investment Strategies, Vol. 4, No. 4, pp. 1-29.

[10] Blin O., Ielpo F., Lee J., Teiletche J. (2017), A Macro Risk-Based Approach to Alternative Risk Premia Allocation, Unigestion research paper.

* ERC and Equal weighted volatility are equal when correlation is constant across the universe ([9]), which is the case for alternative risk premia that tend to post near zero correlation among them.

Important Information

Unless otherwise stated, all figures and illustrations shown in this document have been sourced by Unigestion as at 15 November 2017. This document is addressed to professional investors, as described in the MiFID directive and has therefore not been adapted to retail clients.

It is a promotional statement of our investment philosophy and services. It constitutes neither investment advice nor an offer or solicitation to subscribe in the strategies or in the investment vehicles it refers to. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment. These are not suitable for all types of investors. The views expressed in this document do not purport to be a complete description of the securities, markets and developments referred to in it. To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks. Data and graphical information herein are for information only. No separate verification has been made as to the accuracy or completeness of these data which may have been derived from third party sources, such as fund managers, administrators, custodians and other third party sources. As a result, no representation or warranty, express or implied, is or will be made by Unigestion as regards the information contained herein and no responsibility or liability is or will be accepted. All information provided here is subject to change without notice. It should only be considered current as of the date of publication without regard to the date on which you may access the information. Past performance is not a guide to future performance. You should remember that the value of investments and the income from them may fall as well as rise and are not guaranteed. Rates of exchange may cause the value of investments to go up or down. An investment with Unigestion, like all investments, contains risks, including total loss for the investor. Document issued on: 28 November 2017. Ref: 00025