Back To Basics

Key Points

- Global private equity activity continued to fall with quarterly investment and exit activity more than half the levels of one year ago.

- While PE performance has generally remained flat so far this year, we expect to see downward valuation adjustments across the market in the quarters ahead with VC, growth and large cap to show the biggest drops, while mid-market valuations should only fall moderately.

- With investors needing to rebalance their portfolios, we expect to see a range of secondary opportunities in the coming 12 to 18 months.

Overview

As we approach the final weeks of the year, the frothiness of 2021 seems a lifetime ago. Indeed, private equity activity has continued to fall steeply, with both investment and exit activity in Q3 2022 more than half the levels of one year ago. Fundraising has also slowed, but not enough to stop dry powder from reaching an unprecedented level. This is one reason why private equity entry multiples have not yet shown any downward movement. Meanwhile, despite the fall in public markets and adverse macro indicators, many private equity funds are surprisingly showing at least flat performance so far this year. This is likely to change as we go into 2023.

For investors, it is more important than ever to consider the basic fundamentals when assessing new investments: resilient business models, sensible entry valuations based on the current reality, robust cash flows, strong balance sheets and multiple value creation levers.

The Market Succumbs to Gravity

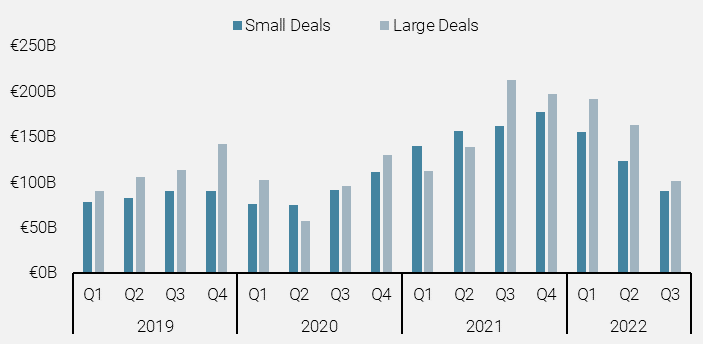

The global aggregate value of private equity deals closed during Q2 was €193bn, 49% down on the same quarter last year[1]. This was driven by similar falls across North America (-50%), Europe (-48%) and APAC (-46%).

Likely driven by debt becoming more expensive, investments in large cap companies (defined as deals with an enterprise value greater than €500m) showed a larger fall (-52%) than investments in mid-market companies (-44%).

Figure 1: Small vs Large Deals

Source: Pitchbook, October 2022.

Similarly, exit activity was significantly down versus the same quarter of 2021. The global aggregate value of exits was €139bn, a decrease of 53% versus the same quarter last year. Steep declines were seen in North America (-61%) and Europe (-61%) while APAC bucked the trend by showing an increase (+16%).

Private equity fundraising remains frail with only $72bn raised globally for buyout funds in Q3, taking the total to $215bn for the year to date[2]. This might be just 28% down on the same period last year but only 43 funds raised in that quarter, the lowest number since Q1 2013. Thus, the fundraising numbers are being propped up by the mega funds, such as Francisco Partners, Baring Asia and Hg Saturn, who between them accounted for almost 50% of the total amount raised.

Spare a thought for the mid-market and emerging managers who are clearly having a much tougher time fundraising in this environment. Large and mega funds[2] currently in the market are in aggregate chasing almost $600bn of capital, potentially diverting LP allocations away from the smaller end of the market. However, if you consider the glass half full perspective, those midmarket and emerging managers who successfully fundraise will be able to deploy in a materially less competitive environment.

Nevertheless, it is clear that private equity investors must apply the strictest of criteria when selecting investments in this environment. For us, we continue to seek companies which can demonstrate consistent growth irrespective of macro conditions. We are able to keep the bar extremely high and only pursue investments in resilient companies which are aligned with our investment themes. Importantly, valuations should be clearly based on the current macroeconomic reality: higher interest rates, higher input costs and lower consumer spending. Finally, we underwrite investments using basic fundamentals such as strong business models, experienced management teams, multiple value creation levers and robust cash flows.

In September, we invested in Bradford Health Services, a leading substance use disorder treatment provider with over 40 facilities across five states in the Southeast US. The market is growing and is significantly underpenetrated with only c10% of diagnosed substance addicts currently seeking help via treatment centres. Furthermore, there has been a material shift towards outcome-based care, coupled with the addition of mental health services. A clear leader in the space, Bradford has a robust pipeline of 15 potential acquisition targets as well as the expectation of adding 12 de novo locations. This investment plays our Mental Health sub-theme and provides a measurable contribution to SDG 3, Good Health and Well-being.

This is the first investment for Unigestion Direct III, our latest direct private equity fund which had its first close on 31 August 2022. We have an attractive pipeline of deals and, notwithstanding the current environment, expect to close further investments in the coming months. The next close of the fund will be before the end of the year.

In July, we invested in a sidecar fund formed by LEA Partners, a German enterprise software investor, to finance identified add-on acquisitions for two of its existing portfolio companies, Zvoove and Craft Group. Both of these companies operate in growing but fragmented specialised B2B software sub-sectors. Zvoove is already one of the largest software provides in the temporary staffing space and is in a good position to further consolidate the European market. Craft Group is one of the leading software providers for craftsmen in the DACH (Germany, Austria and Switzerland) region. This investment plays our Service Efficiency theme.

The Elephant in the Room: PE Valuations

In Q2, we saw positive performance across nearly all our programmes, although this was mainly driven by exits at higher multiples with the valuations of unrealised companies remaining largely flat. Anecdotally, most private equity firms also showed at least flat performance in their funds in Q2, especially in small and mid-market funds. Meanwhile, for the six months to 30 June 2022, the S&P 500 fell by 21%.

Why is there such a disparity? This is not a new phenomenon but, with liquid asset valuations falling materially, the yawning valuation gap is causing no end of headaches for investors who are seeing big swings in their asset allocation.

The valuation guidelines put forward by IPEV (International Private Equity and Venture Capital) state that the valuation multiple at entry should be calibrated to an identified public peer group. This allows the calculation of an “implied discount” to the peer group which should be consistently applied to valuations going forward, suggesting that valuations should in theory move in tandem with public market valuations. However, in practice, the guidelines also allow flexibility. Thus, managers can argue to decrease or increase the implied discount for a variety of reasons.

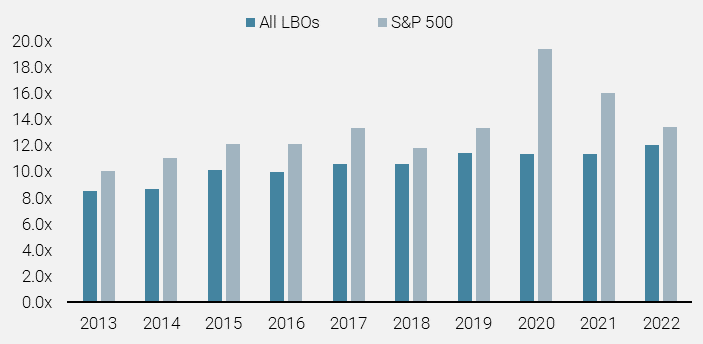

As figure 2 shows, the average discount between PE entry multiples and public multiples has fluctuated a great deal in the last few years. For example, a private equity firm entering an investment in 2020 may have recorded a large discount of 40% – 50% to a public peer group (depending on the sector). Fast forward to 2022 and the investment’s public peer multiples would have fallen c20% – 30%. However, given that private transaction multiples (which after all are the best proxy for the valuation of a private company) have in the meantime hardly moved, the private equity firm has a reasonable argument to keep the valuation multiple at a similar level.

Figure 2: PE Entry vs Public Valuations (EV/EBITDA)

Source: S&P LCD Comps LBO Review Q2 22 and Capital IQ, data as at 30 June 2022.

A second reason for stable performance so far this year is that private equity backed companies are continuing to show growth. For example, in Unigestion Direct II, the vast majority of portfolio companies have recorded positive EBITDA growth for the 12 months to 30 June 2022 versus the same period a year ago. In addition, the companies are typically highly cash generative and able to pay down debt. Thus, even with multiples going down in certain sectors (e.g. Technology), overall performance remains positive.

Finally, private equity investors argue that valuations can only be considered wholly accurate on two occasions: at entry and at exit. The objective of providing valuations of portfolio companies in the interim is to give as accurate a valuation as possible while remaining sufficiently conservative. As a result of the embedded conservatism in our valuations, we are consistently able to show a premium at exit vs. the quarter prior to the exit being announced. This is demonstrated below with the exits we have achieved from our direct portfolios in the last two years.

| Fund | Deal | Valuation Prior to Exit | Valuation at Exit | Premium | % |

| ECD | 1.64x | 1.68x | 0.04x | 2% | |

| ECD | 3.26x | 4.37x | 1.11x | 34% | |

| ECD | 1.40x | 2.14x | 0.74x | 53% | |

| ECD | 2.50x | 4.40x | 1.90x | 76% | |

| UDO | 2.04x | 2.69x | 0.65x | 32% | |

| UDO | 1.80x | 3.14x | 1.34x | 74% | |

| UDO | 2.65x | 3.49x | 0.84x | 70% | |

| UDO | 2.68x | 4.56x | 1.88x | 70% | |

| UDII | 1.89x | 3.30x | 1.41x | 75% | |

| Average | 2.21x | 3,31x | 1.10x | 50% |

Source: Unigestion as of October 2022.

Importantly, this premium has hardly changed irrespective of public market valuations.

Should we expect positive PE performance to continue? With discounts to public valuations now wafer thin, any further drop in public markets will eventually push down private equity valuations. In addition, as consumers and businesses start to feel the pinch of higher costs, higher energy prices and higher interest rates, this will ultimately translate into slower growth at the portfolio company level. The extent and timing of such downward valuation adjustments will vary substantially. We expect the worst hit areas to be venture capital, growth capital, large buyouts as well as more cyclical sectors (which historically are also the most correlated to public valuations within the private equity space). Meanwhile, mid-market buyouts and non-cyclical sectors will see more modest downward valuation movements. It is thus likely that investors will see negative performance in the quarters ahead. However, given that transaction multiples are typically slow to adjust, the timing of valuation adjustments in general may be slower than investors expect.

Is It Time for Secondaries Yet?

There is nothing like a downturn to generate attractive secondaries opportunties. Or so the conventional wisdom goes. Nevertheless, there is no doubt that certain investors already need to rebalance their portfolios away from private equity due to the fall in value of their other asset holdings and/or will run into liquidity issues due to exits drying up. One of their only remedies is to seek solace in the secondary market.

Where do we think the most attractive secondaries opportunities will be in the coming 12 to 18 months?

LP stakes in mid-market portfolios. So far, LPs have been unwilling to sell their interests in funds at material discounts to NAV. However, as NAVs of certain portfolios fall and LPs become even more motivated to sell, the bid-ask spread between buyers and sellers will narrow. For secondaries investors, despite falling valuations, the fundamentals of portfolio companies in the best mid-market funds will remain the same: resilient business models, low leverage, leaders in niche spaces, robust cash flows, etc. Currently, demand is still driven mainly by portfolio rebalancing rather than imminent cash needs. This provides attractive opportunities for the use of structures such as deferred payments of up to 12 to 18 months so that the seller does not have to show too large a valuation hit on their portfolio.

Venture capital portfolios. The sky high tech valuations of 2021 are a distant memory. It is clear that many venture capital backed companies will now need to undertake financing rounds at much lower valuations. Many others will go out of business. Investors who came into venture capital funds at the peak of the market will now be regretting it, and will be seeking a swift exit. For certain savvy secondaries investors, this will create attractive opportunities – either by buying heavily discounted stakes in otherwise solid portfolios or by providing later stage funding, through sidecar funds for example, to the best companies at much lower valuations.

Single asset continuation funds. If the market does swing back to LP stakes, many are predicting the demise of single asset continuation funds. However, GPs have seen how effective these are in allowing them to continue backing their best performing portfolio companies. As the exit markets close, GPs will prefer going down the single asset continuation fund route in order to increase liquidity for investors. For us, this provides access to market-leading companies in defensive sectors that come with attractive risk mitigating features: a company that the GP knows well, tangible and credible value creation plans, and strong alignment.

The comeback of mult-asset continuation funds. These were the original “GP-led” deals only to be usurped by their single asset brethren, which in the last two years have been favoured by GPs preferring the more selective approach. However, given the combination of the lower liquidity environment and the general oversupply of secondary opportunities, GPs will be more likely to package together their best performing companies with different liquidity profiles in order to attract secondary investors.

In general, it is clear that the balance continues to shift in favour of secondaries investors. For GP-led deals, secondaries investors are more critical about valuation, the reason for doing the deal in the first place and GP alignment. Indeed, we are not only seeing attractive discounts on high quality companies, but are also able to negotiate strong alignment features such as higher carried interest hurdles, stricter adherence to liquidity timing and active board seats for us as the lead investor.

During Q3 2022, we approved the investment in a multi-asset continuation fund managed by Capiton, a German-based manager. The fund contains two assets: AEMtec, a provider of engineering and electron manufacturing services, and Raith, a global developer and manufacturer of nanofabrication systems and software. Both companies are exhibiting strong growth, have stable, long-standing customer relationships and benefit from long-term sector tailwinds. We were able to negotiate an attractive entry discount of 10% and a staggered carry scheme (only delivering fully carry if our target multiple and IRR returns are met). The deal will close later in Q4 2022.

We have been successfully investing in secondaries for over two decades. Some of our best deals have come during difficult economic periods. However, irrespective of macro conditions, the key features of our secondaries strategy have remained constant over time: target concentrated portfolios of high quality companies, seek returns driven by growth rather than leverage and demand downside protection in every deal.

Unigestion Private Equity Activity

Here are the highlights of some of the investments and exits that we completed in Q3:

In July, Kester Capital sold Avania to private equity investor Astorg. Avania Clinical (www.avaniaclinical.com), headquartered in the Netherlands, is a full service Clinical Research Organization (“CRO”) for medical devices, IVDs, biological and cell-based products. The company has a global service offering and is present in Europe, the US and Australia and generated sales of EUR 34 million in 2021 with more than 173 employees. The company benefits from long term contracts and a loyal customer base as well as strong market tailwinds such as regulatory changes (e.g. the new Medical Device Regulation by the European Commission), an increased outsourcing trend and an increasing complexity of medical devices (e.g. digital devices).

The sale has resulted in 3.3x TVPI and 95% IRR for Unigestion Direct II. Given the attractive market positioning, resilient business and favorable long-term market tailwinds, Unigestion Direct II has rolled over its initial investment in Avania and remains an investor alongside Kester Capital (who has done the same) and Astorg.

Also in July, Lee Equity sold Captive Resources to KKR. Captive Resources (www.captiveresources.com) is by far the largest captive insurance (insurance owned and controlled by its own members) consultant, providing its members with insurance coverage for workers’ compensation, general liability, automobile, property and health insurance. The company has an

80%+ market share, and manages 44 group captives covering 5,500 companies and USD 3.3 billion in premiums. The sale has resulted in a TVPI of 3.2x and 50% IRR for Unigestion Direct Opportunities 2015.

Given the compelling core business fundamentals and strong competitive moats that Captive Resources has constructed over its operating history, Unigestion invested again in Captive Resources on behalf of Unigestion Direct II. Captive has room to grow organically through continued market penetration, launch of new products, and by increasing awareness of group captive solutions.

In August, Unigestion completed an investment in Matec. Matec is active in the design and construction of plants for the filtration of wastewater from industrial processes. The company has grown significantly over the past years by expanding to larger projects and has consequently become the world number six player in its core market. Through its newly opened 20,000 m2 production site in Mulazzo (Italy), Matec has laid the foundations for an ambitious growth plan. The company should benefit from a growing market with a strong ESG tailwind, mainly driven by an increase in sustainable practices in the mining and aggregate industry.

In August, Unigestion acquired an LP stake in Limerston Fund I. Limerston Fund I (2016 vintage) consists of a well-diversified portfolio of six companies in the UK. The portfolio is supported by long-term trends and downside protection. It is expected that ongoing market volatility could benefit the portfolio in terms of buy and build opportunities and attractive valuations. The portfolio is managed by Limerston, a UK based fund manager focusing on lower middle-market buyouts with a buy and build approach, which has accomplished 20 add-ons across eight platforms.

Also in August, Unigestion committed to Lee Equity IV. Lee Equity is an established New York-based private equity firm that targets US mid-market businesses. The firm focuses on three core sectors: financial services, healthcare services and business services. It specifically targets growth opportunities, corporate carve-outs, public to privates, and buy-and-build platforms. Unigestion has built a strong relationship with Lee Equity since 2016 through a secondary and stapled primary investment, and several co-investments (including its recent exit of Captive Resources at 3.2x TVPI) over the years.

During July, Swedish fund manager Systematic Growth exited Voff (www.voff.pet) to Denmark-based private equity manager Axcel Partners. Voff is Europe’s leading provider of natural premium pet food. The sale generated a return of 4.1x TVPI and 40% IRR. With total proceeds of over EUR 120 million for Euro Choice Secondary II, Unigestion Secondary Opportunity IV, Unigestion Secondary Opportunity III and a mandate, this was one of the largest exits in Unigestion’s programmes to date.

At the end of August, Unigestion invested in Paua Ventures 2. Paua focuses on early stage (Seed & Series A) investments in Deep Tech, Enterprise Software & Industry 4.0 in Europe, with a strong focus on the DACH region. The firm employs a proactive approach to working with portfolio companies, actively promoting and orchestrating collaboration between corporates and portfolio companies. The team is well anchored in the German entrepreneurial community which is evidenced by prominent co-investors and LPs, allowing them to see deals earlier than the competition. Paua 2 has already backed 10 companies, two of which have now raised follow-on rounds and have been up-valued.

In September, Unigestion invested in Avataar Ventures II. Avataar is one of the very few early growth investors focused on tech-enabled B2B & SaaS companies in India led by seasoned investor Mohan Kumar (ex-Managing Partner of Norwest India) and operator Nishant Rao (ex-global COO of Freshworks). The firm focuses on companies generating USD 10-30 million of annual recurring revenue which offer either horizontal and vertical SaaS with global expansion potential or B2B technology within integrated marketplace and transaction platforms. The fund has made its first investment in an insure-tech company, InsuranceDekho, which provides Point of Sales Persons (PoSP) insurance distribution to tier 2+ cities in India.

Also in September, Afinum sold Empolis, a portfolio company in a multi-asset continuation fund in Euro Choice Secondary II, resulting in a multiple of 11.9x to the fund. Empolis (www.empolis.com) is a provider of AI-based decision support software. With this exit, all four portfolio companies of the secondary transaction have been realised within two years, resulting in a return for Euro Choice Secondary II of 3.6x TVPI and 112% IRR.

Unigestion also completed an investment during September in FINTECH Group, the leading provider for credit management software in the DACH region. The group currently consists of three platform companies and is soon to be complemented by another acquisition, with additional target companies shortlisted to further grow the group. FINTECH Group’s end-to-end platform thus provides its customers with the digitisation of the entire credit lifecycle, from customer initiation and credit approval to refinancing and repayment monitoring. FINTECH Group should benefit from rising reporting requirements and efficiency pressure, that will drive banks to upgrading their existing software suite.

[1] Pitchbook, October 2022.

[2] Preqin, October 2022.

[3] Large funds are defined as between USD 1,500 and 5,000 million, while Mega funds are defined as greater than USD 5,000 million.

Important information

This document is provided to you on a confidential basis and must not be distributed, published, reproduced or disclosed, in whole or part, to any other person.

The information and data presented in this document may discuss general market activity or industry trends but is not intended to be relied upon as a forecast, research or investment advice. It is not a financial promotion and represents no offer, solicitation or recommendation of any kind, to invest in the strategies or in the investment vehicles it refers to. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment.

The investment views, economic and market opinions or analysis expressed in this document present Unigestion’s judgement as at the date of publication without regard to the date on which you may access the information. There is no guarantee that these views and opinions expressed will be correct nor do they purport to be a complete description of the securities, markets and developments referred to in it. All information provided here is subject to change without notice. To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks.

Data and graphical information herein are for information only and may have been derived from third party sources. Although we believe that the information obtained from public and third party sources to be reliable, we have not independently verified it and we therefore cannot guarantee its accuracy or completeness. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. Unless otherwise stated, source is Unigestion. Past performance is not a guide to future performance. All investments contain risks, including total loss for the investor.

Unigestion SA is authorised and regulated by the Swiss Financial Market Supervisory Authority (FINMA). Unigestion (UK) Ltd. is authorised and regulated by the UK Financial Conduct Authority (FCA) and is registered with the Securities and Exchange Commission (SEC). Unigestion Asset Management (France) S.A. is authorised and regulated by the French “Autorité des Marchés Financiers” (AMF). Unigestion Asset Management (Canada) Inc., with offices in Toronto and Montreal, is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario, Quebec and Newfoundland & Labrador. Its principal regulator is the Ontario Securities Commission. Unigestion Asset Management (Düsseldorf) SA is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Bundesanstalt für Finanzdienstleistungsaufsicht” (BAFIN).

Document issued September 2022.