BUILDING A CLIMATE TRANSITION PORTFOLIO

Head of Responsible Investment Portfolio Manager, Equities

Portfolio Manager, Equities

Key Points

- Climate transition investing covers a broad array of sub-thematic investment opportunities.

- Unlocking the growth potential lies in understanding inherent biases, linking thematic activity to traditional risks.

- We propose a climate transition strategy that delivers strong alignment, ensuring thematic diversification and strong risk control.

Overview

Climate transition investing provides an opportunity to access the growth potential associated with the journey to a lower carbon world. This potential is found both in solution providers (‘enablers’) and those companies seeking to reduce their own carbon footprint (‘mitigators’). The nature of the economic activities represented by these groups brings with it inherent biases across regions, industries and factors. By carefully constructing custom datasets and thematic definitions, we are able to fully leverage our suite of quantitative risk management tools to access the growth opportunity where reward potential compensates us for these risks. By doing so we ensure diversification and risk control across traditional and climate transition specific risk factors.

Identifying Growth Potential In The Climate Transition

As discussed in the first paper* of this four-part series, climate investing can be viewed from two perspectives: mitigation and enabling the climate transition. Mitigators contribute to the transition to a low carbon economy through self-decarbonisation, while enablers provide decarbonisation solutions for sectors of the economy where GHG emissions are difficult to reduce. This two-pronged view is required to address the challenges posed by climate change: without enabling technologies, the economy will not be able to transition at a rate that is consistent with the goals of the Paris Agreement.

Recent global policy measures, such as the EU Action Plan on Sustainable Finance, aim to shift capital flows towards sustainable investments. At the same time, we are seeing demand-side shifts. The energy shock from the war in Ukraine was a wake-up call – a reminder of the urgent need to support the green transition and build sustainable and reliable energy supply. Thus, while the regulatory landscape of financial markets is rapidly evolving to support the transition, demand-side changes are also taking place, as demand for green financial instruments increases.

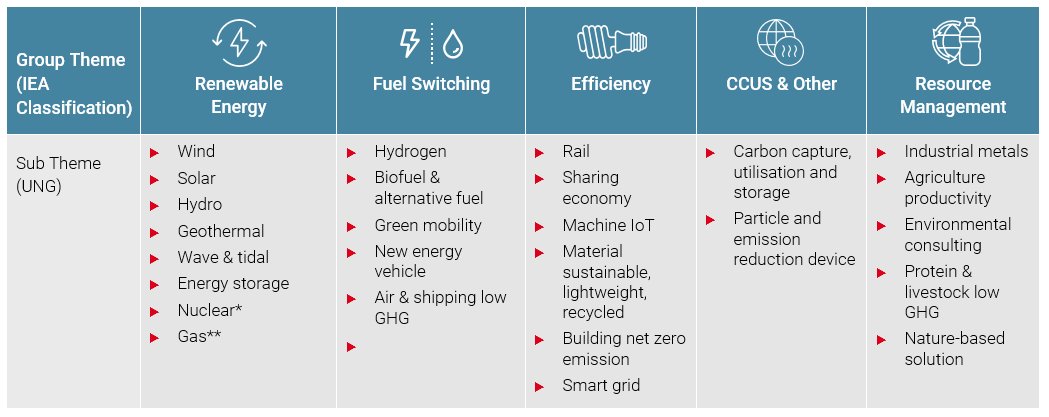

Climate investing involves addressing various commonly-known themes as identified by the International Energy Agency (IEA) and many other organisations; renewable energy, fuel switching, energy and production efficiency, carbon capture, utilisation and storage, as well as resource management.

In order to closely target investment opportunities, we have split these themes into sub-themes which allows us to study each vertically considering the value chain. We seek to identify companies best placed, in terms of scalability or offering technology, to have the most significant impact on the transition process.

Sub-themes encompass both enablers and mitigators which include, but are not limited to, the list below:

As explained in the second paper* of our climate investing series, we can rely on data available from public reports of the companies and scientific estimations when looking for investment opportunities among the mitigators. The expertise in data processing and management is quite valuable as there are quite a number of data dimensions to identify, collect and properly use from scopes 1, 2 and 3 of GHG emissions of companies and their progress, to their contributions to the Paris alignment objectives and the relevance of activities in light of regulatory definitions.

Identifying enabling opportunities is a different kind of challenge. These companies are mainly young and their purpose is developing new solutions and applying existing products to new problems. They are delivering growth opportunities in the most traditional sense: new products, new markets and new revenue streams. But finding them cannot be achieved in the same way.

To do so, we employ artificial intelligence (AI) and more specifically Natural Language Processing (NLP). NLP is a valuable new accessory in the analytical toolkit o investment managers, enabling us to analyse the news, financial filings or social media, look for associations within a certain topic of interest and conduct sentiment analysis. as such it can identify newer solutions that have strong potential but have not yet delivered significant revenue streams for companies.

Natural Biases

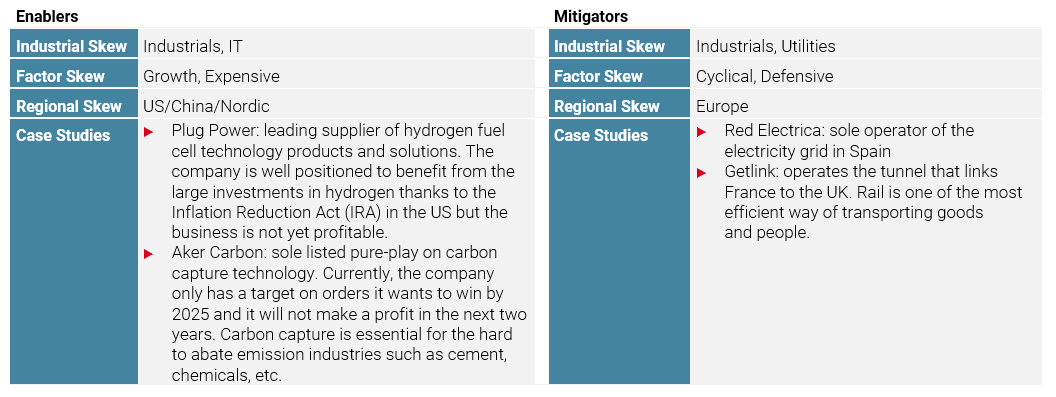

Due to the nature of the activities represented by enablers and mitigators, we observe natural biases across region, industry and factor exposures. Many of these biases are intuitive and reflect the relative progress of climate transition in different parts of the world. Beyond the high level enabler/mitigator split we can see they vary considerably across and within sub-themes.

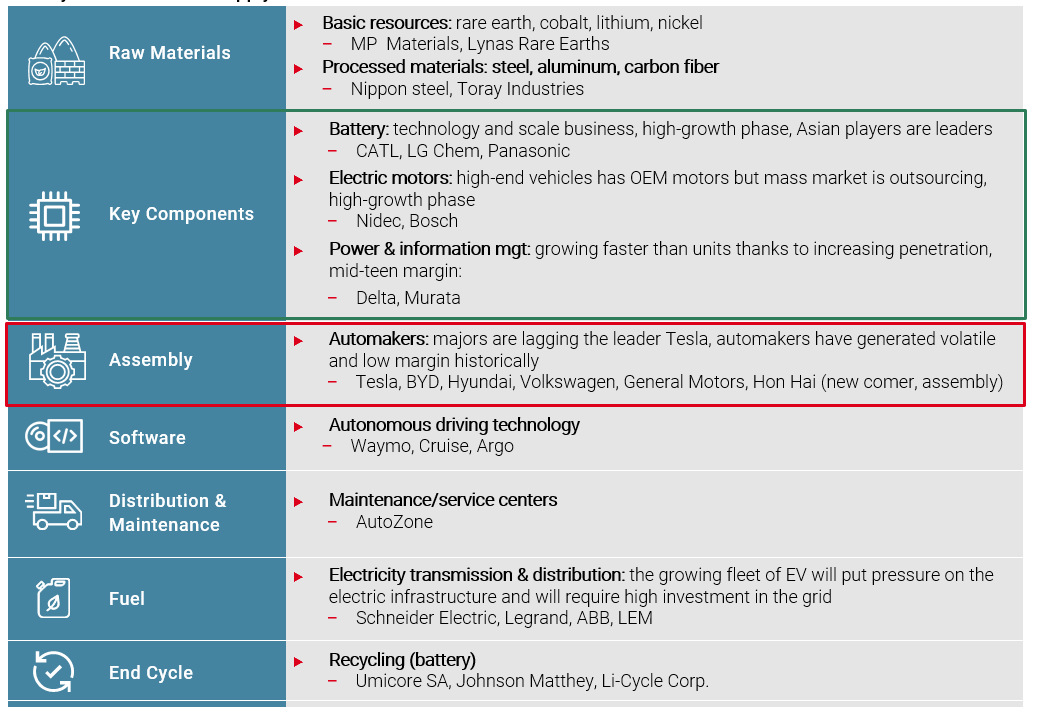

Even within prominent sub-themes, the exact position in the value chain can be significant in determining natural biases. Electric Vehicles (EV) provide a good example of how focusing on different elements of this sector can dramatically change the nature of the economics exposure. Key components, such as batteries or power management systems, already enjoy a supply side that is consolidated, has good profitability and benefits from the growing penetration of EV. By contrast, Assembly, while the post-covid period provided something of a tailwind for automakers, the business model will remain volatile and low-margin while EVs are cannibalising internal combustion engine vehicles.

Battery Electric Vehicle Supply Chain

The inherent differences between the enabler and mitigator groups already help us achieve some form of natural diversification and we can tilt exposure between the two to manage the exposure of the portfolio overall. However, as highlighted above, there are more dimensions to consider between and within sub-themes and we can use our existing suite of quantitative tools to better manage portfolio exposures.

Harnessing the quantitative toolkit

From one perspective, quantitative investing is the exercise of balancing the exposure you desire for return purposes, with the risks associated with those exposures. An important task is to map the exposures to ensure you understand the risk factors they present.

For the traditional consideration of risk – such as regional, sector and factor exposure – this has become a relatively simple exercise, with a plethora of high quality data sources available. The task is more complex for climate transition investing given the recent European regulation taxonomy has introduced two new definitions: taxonomy compliance and thematic alignment. In order to make full use of the quantitative toolkit, you need to be able to link these desired exposures to the traditional risk factors.

To tackle this problem, we have created two datasets to map our investment universe to taxonomy activities, and our own definition of sub-theme exposure:

- Taxonomy-consistent investment relies on high quality data which is in short supply from third parties. As a result, we need to create internal datasets and rely on human validation.

- Analysing across new and existing risk dimensions – i.e. specific industrial themes

(e.g. solar) not just traditional definitions (e.g. NLP).

This mapping unlocks our wider suite of risk management and portfolio construction tooling. Our approach can then consider balancing thematic exposure with investment risk.

The EU Taxonomy is a green classification system that translates the EU’s climate and environmental objectives into criteria for specific economic activities for investment purposes. It recognises as green, or ‘environmentally sustainable’, those economic activities which make a substantial contribution to at least one of the EU’s climate and environmental objectives, while at the same time not significantly harming any of these objectives and meeting minimum social safeguards.

Source: Sustainable finance taxonomy FAQ.

Portfolio construction from mixed underlying sources

Portfolio construction needs to account for three key components: the uncertainty associated with earlier stage investments; the desire to retain broad thematic diversification; and controlling traditional risk factors such as region, sector and factor concentration.

Capturing uncertainty is a key topic due to the early stage the world is at in its transition to a lower carbon economy. When considering the enabling sub-themes in particular, certain of these technologies and services are either entirely novel or novel-in-application. The potential for growth is considerable but the timing and certainty of that growth is less obvious. To address this we consider our position size as a function of the visibility to future growth for these stocks. This visibility is itself a function of market volatility (higher is worse); valuation (more expensive is worse); and growth trajectory (longer dated is worse).

The temptation when building a climate transition portfolio is to focus on pure-play sub-themes such as renewable energy. However, as highlighted above, this neither covers the full breadth of carbon reduction opportunities nor provides suitable levels of diversification to the thematic drivers and natural biases. By holding associated stocks with taxonomy activities and sub-themes, we are able to control directly the level of portfolio exposure to sub-themes. This control can be used as an active, return-seeking mechanism by varying exposure to certain themes over time; as well as a risk management tool, ensuring there is not over exposure to a given sub-theme. By insisting on diversification we are able to chart a smooth course in the journey to a lower carbon future, by balancing and varying exposure.

Portfolio construction

Identifying thematic exposure is key to ensuring the portfolio is well aligned with the goal of supporting climate transition. Balancing this alignment with traditional risk management becomes an important portfolio construction task. Relying once more on our datasets associating activity and thematic exposure, we are able to better understand traditional risk factors. To some extent, control of traditional risk exposures will be achieved by combining the differing natural biases of the sub-themes. The quantification of those risks allows the full suite of quantitative investment tools to be utilised. This is not to say the final portfolio is without biases – indeed, properly pursuing climate transition should come with intuitive sector biases toward Industrials and Utilities and factor biases towards Growth. However, understanding and moderating those biases where they are not rewarded by alignment with the climate transition objective remains key.

Climate transition can be adapted to risk appetite

Despite the importance of climate transition for the majority of investors, the current processes and rules in place for many can make it difficult for them to consider pure climate investments. This is due to higher tracking errors and being inherently benchmark agnostic due to lack of proper and purely-built indices in the market. Many investors still judge their investments against current global indices which are not suitable when thinking of a future low carbon economy. Moreover, investing in themes would mean focusing on certain activities while not considering others, which differs from the current all-inclusive nature of indices. Finally, current market indices are based on current market capitalisation and do not reflect the future shift required to align them with a low carbon future.

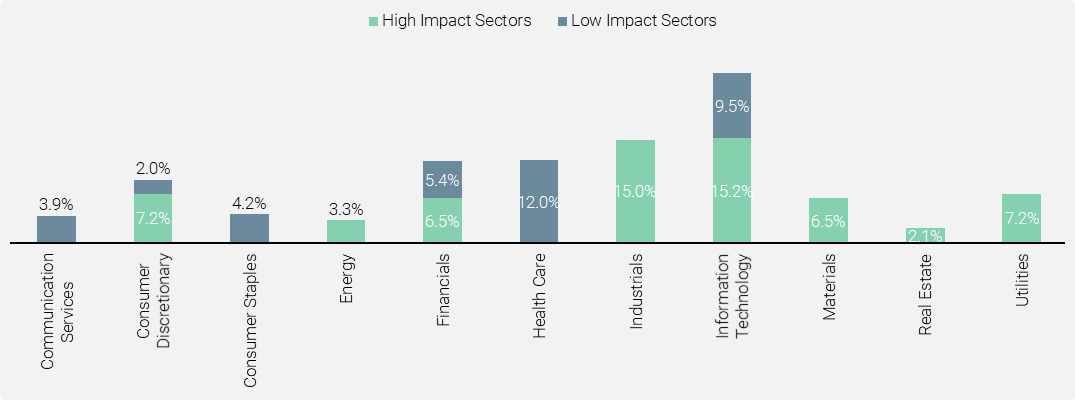

To strike the balance between strong alignment with climate transition opportunities while capturing the wider economic drivers represented by the index, we propose a framework which seeks to focus active risk on thematic alignment. This splits economic and industrial exposures into high impact potential activities (i.e., those covered by the enabler and mitigator definitions) and low impact potential activities. Areas of high impact potential are used to gain exposure to climate transition themes while those with low impact potential are judged on broader ESG considerations.

Energy provides a good example of a High Impact Sector. As discussed in the third paper in this series*, energy transition is a core element of the climate transition story. The journey progresses through less emitting fuel options – such as natural gas and bio-fuels – to support the increased use of renewables while large-scale storage solutions remain elusive. In allocating to these transition sources, we retain robust exposure to the overall economics of the sector.

This approach allows investors to address their climate transition investment targets while remaining within their required risk budget. It would enable them to remain almost neutral with respect to certain biases such as sector allocations and factor biases. Given the significance of the decarbonisation story in reshaping the world economy, the result could be considered the expected future shape of the index.

Conclusion

Climate transition investing gives access to a broad swathe of sub-themes, each representing a set of natural biases across the dimensions of sector, region and factors. Portfolio construction becomes an exercise in balancing these biases so as to achieve high thematic alignment while controlling excessive risk exposures. We combine mind and machine to select the most attractive investments, leveraging a bespoke activity dataset to unlock our existing suite to quantitative tools. With this approach we are able to analyse the portfolio across thematic and traditional risk dimensions. This understanding also provides portability, allowing investor risk appetite to dictate the level of thematic intensity in the investment solution.

Important information

Past performance is no guide to the future, the value of investments, and the income from them change frequently, may fall as well as rise, there is no guarantee that your initial investment will be returned. This document has been prepared for your information only and must not be distributed, published, reproduced or disclosed by recipients to any other person. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. This is a promotional statement of our investment philosophy and services only in relation to the subject matter of this presentation. It constitutes neither investment advice nor recommendation. This document represents no offer, solicitation or suggestion of suitability to subscribe in the investment vehicles to which it refers. Any such offer to sell or solicitation of an offer to purchase shall be made only by formal offering documents, which include, among others, a confidential offering memorandum, limited partnership agreement (if applicable), investment management agreement (if applicable), operating agreement (if applicable), and related subscription documents (if applicable). Please contact your professional adviser/consultant before making an investment decision.

Where possible we aim to disclose the material risks pertinent to this document, and as such these should be noted on the individual document pages. The views expressed in this document do not purport to be a complete description of the securities, markets and developments referred to in it. Reference to specific securities should not be considered a recommendation to buy or sell. Investors shall conduct their own analysis of the risks (including any legal, regulatory, tax or other consequences) associated with an investment and should seek independent professional advice. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment. These are not suitable for all types of investors.

To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks. Actual results could differ materially from those in the forward-looking statements. As such, forward looking statements should not be relied upon for future returns. Targeted returns reflect subjective determinations by Unigestion based on a variety of factors, including, among others, internal modeling, investment strategy, prior performance of similar products (if any), volatility measures, risk tolerance and market conditions. Targeted returns are not intended to be actual performance and should not be relied upon as an indication of actual or future performance.

Data and graphical information herein are for information only and may have been derived from third party sources. Unigestion takes reasonable steps to verify, but does not guarantee, the accuracy and completeness of this information. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. All information provided here is subject to change without notice. It should only be considered current as of the date of publication without regard to the date on which you may access the information. Rates of exchange may cause the value of investments to go up or down. An investment with Unigestion, like all investments, contains risks, including total loss for the investor.

Backtested or simulated performance: Backtested or simulated performance is not an indicator of future actual results. The results reflect performance of a strategy not currently offered to any investor and do not represent returns that any investor actually attained. Backtested results are calculated by the retroactive application of a model constructed on the basis of historical data and based on assumptions integral to the model which may or may not be testable and are subject to losses.

Changes in these assumptions may have a material impact on the backtested returns presented. Certain assumptions have been made for modeling purposes and are unlikely to be realized. No representations and warranties are made as to the reasonableness of the assumptions. This information is provided for illustrative purposes only. Backtested performance is developed with the benefit of hindsight and has inherent limitations. Specifically, backtested results do not reflect actual trading or the effect of material economic and market factors on the decision-making process. Since trades have not actually been executed, results may have under-or over-compensated for the impact, if any, of certain market factors, such as lack of liquidity, and may not reflect the impact that certain economic or market factors may have had on the decision-making process. Further, backtesting allows the security selection methodology to be adjusted until past returns are maximized. Actual performance may differ significantly from backtested performance.

Unigestion SA is authorised and regulated by the Swiss Financial Market Supervisory Authority (FINMA). Unigestion (UK) Ltd. is authorised and regulated by the UK Financial Conduct Authority (FCA) and is registered with the Securities and Exchange Commission (SEC). Unigestion (US) Ltd is registered as an investment adviser with the U.S. SEC. Unigestion Asset Management (France) S.A. is authorised and regulated by the French “Autorité des Marchés Financiers” (AMF). Unigestion Asset Management (Canada) Inc., with offices in Toronto and Montreal, is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario, Quebec and Newfoundland & Labrador. Its principal regulator is the Ontario Securities Commission. Unigestion Asset Management (Düsseldorf) SA is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Bundesanstalt für Finanzdienstleistungsaufsicht” (BAFIN).

Document issued in November 2022.