In September 2020, Unigestion Direct II invested in Infobip through a USD 200m pre-IPO first equity raise led by One Equity Partners (OEP) with terms that confer significant downside protection. Infobip is a closely-held, profitable business in a high-growth, B2B technology services sector underpinned by increasing demand for effective customer messaging and online security solutions.

This case study provides an insight into our direct private equity investment strategy and approach. It illustrates the typical characteristics of companies in which we invest and how we aim to create value.

About Infobip

Infobip is a leading communication platform as a service (CPaaS) company that delivers secure customer engagement applications to major enterprises, enabling them to manage and execute customer communications.

For example, Infobip’s platform allows banks and financial services firms to send “one time passcode” SMS’s to clients in order to authenticate secure access to online accounts. In addition, since the COVID-19 crisis, Infobip has enabled food delivery service providers to meet increasing demand using messaging services.

Core services include “Transactional” communications such as alerts, notifications, authentication and marketing, delivered through both application-to-person (A2P) and person-to-application (P2A) channels. These include SMS, voice, RCS, email and chat applications. Infobip has also launched “Conversational” services, including human-to-human and human-to-bot communication solutions.

Since it was founded in 2006, Infobip has expanded organically to become a leading global CPaaS company. Today, the company has 2,400 employees in 60 offices globally serving over 9,500 corporate clients with the capacity to reach 7bn mobile devices in 190 countries.

Why did Unigestion choose to invest in Infobip?

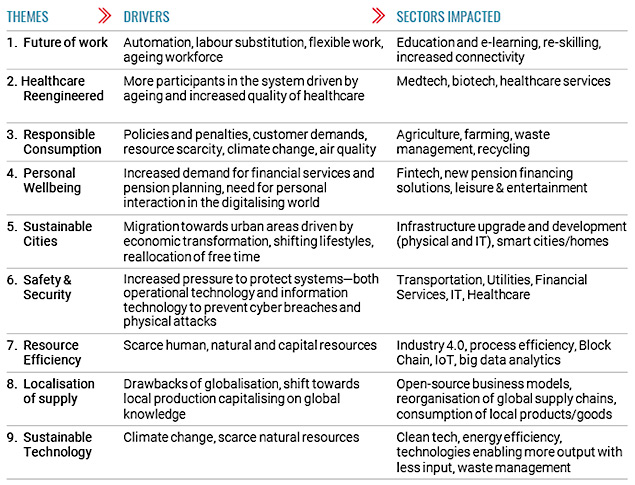

Unigestion targets investments in resilient companies with superior value propositions, strong management teams and attractive financial metrics. A key criteria for evaluating a potential investment in a company is whether it fits one of our investment themes, as detailed in Figure 1. In this case, Infobip meets the criteria of our “Safety and Security” and “Services Efficiency” themes. In particular, the company benefits from the increasing demand for cybersecurity and technology-enabled business services.

The company’s core market, CPaaS, is a fast-growing market, expected to grow by up to 2.5 times (20% CAGR) to reach USD 38bn by 2023. Applications around SMS communication are expanding in response to increasing adoption from traditional, non-technology-led sectors such as banks. However, new communication channels such as WhatsApp, Viber, Facebook Messenger and RCS in particular also represent significant growth opportunities.

Figure 1: Private Equity Themes, Drivers and Impacted Sectors

Source: Unigestion, November 2020.

Infobip has an advanced and truly global CPaaS offering with the single largest market share (3.5%) for its core market and leadership in the highest growth markets (Asia, LATAM, Africa). It has the widest connectivity reach with direct access to more than 600 operator connections, a complete, omni-channel CPaaS offering supported by its own infrastructure and hosted on a private cloud, and 28 data centres. Its technology edge is maintained by an 850-strong engineering team.

Thanks to the exceptional leadership of its management team and founders, Infobip’s growth has outpaced the CPaaS market with a 48% revenue CAGR over the last 10 years. Management has led the firm to profitability and global scale with no equity fundraising to date and only EUR 20m net debt outstanding at the closing of our investment. The founders, who will remain majority owners in the business, are committed to lead the business towards an IPO in the next three years.

Did the COVID-19 crisis impact the fundamentals of this transaction?

Infobip’s performance has accelerated this year in the wake of the crisis. Travel and hospitality, the two sectors most heavily impacted by the crisis, account for just 0.5% of revenue, while 67% comes from telecom and tech industries, 9% from logistics and 7% from financial services. The firm was therefore able to weather the crisis well thanks to the strong non-cyclical tilt of its customer base.

Furthermore, we have seen a clear acceleration in the digitalisation of client communication strategies. Technology-enabled businesses have been fast adopters of digital communication channels but traditional sectors with slower adoption rates have had to adapt quickly to meet the growing need for remote client engagement. We believe this trend will continue as a tailwind for Infobip.

How do you plan to create value in this investment?

Our investment proceeds will be used primarily to fund M&A opportunities in the US which will drive gross margin growth by increasing market share in the largest and most profitable CPaaS market in the world and by acquiring additional higher margin channel capabilities.

We are delighted to invest alongside OEP in Infobip’s first capital raise. A founder-led, self-funded business, it now has a global footprint in the high-growth CPaaS market where demand for more connected customer engagement is accelerating. Investors and management have a shared vision to further Infobip’s pre-IPO growth both organically and by acquisition.

Infobips’s core addressable market remains fragmented, presenting a range of accretive M&A opportunities. OEP is in active discussions with potential M&A target companies with two opportunities already sourced and one in live negotiations. Indeed, shortly after our investment, the company has already announced its acquisition of OpenMarket from Amdocs for USD 300m. OpenMarket is the leading provider of automated SMS solutions in the US.

The transaction with OEP, Unigestion and other co-investors is the first round of institutional investment and the three founders (who previously owned 100% of equity) are aligned with investors, having taken only EUR 10m cash out. Moreover, deal terms confer significant downside protection: Infobip is valued at a material discount to its peer group while Unigestion’s equity position in the capital stack is senior to management’s shareholding.

Infobip’s stated goal is to list on either the NYSE or NASDAQ in the next three years. This will enable it to continue growing through highly accretive M&A post-IPO. Other exit options include a trade sale to a public competitor – Twilio, currently valued atUSD 30bn, has made 10 acquisitions since 2017 – or a sale to a large cap PE sponsor.

Why did Unigestion choose to co-invest with OEP?

OEP is a US private equity firm with over USD 6bn in assets under management and a particular focus on mid-market industrial, healthcare and technology sectors in North America and Europe. OEP has a proven track record in transformative ‘buy-and-build’ private equity transactions in the technology-enabled business services space, thus Infobip’s M&A strategy in the US is well aligned with OEP’s core competence.

Unigestion has a strong relationship with OEP, having invested in two of their programs to date as well as two previous co-investments. Unigestion was therefore offered a ‘first look’ to invest into Infobip alongside OEP.

Important Information

Past performance is no guide to the future, the value of investments, and the income from them change frequently, may fall as well as rise, there is no guarantee that your initial investment will be returned. This document has been prepared for your information only and must not be distributed, published, reproduced or disclosed by recipients to any other person. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation.

This is a promotional statement of our investment philosophy and services only in relation to the subject matter of this presentation. It constitutes neither investment advice nor recommendation. This document represents no offer, solicitation or suggestion of suitability to subscribe in the investment vehicles to which it refers. Any such offer to sell or solicitation of an offer to purchase shall be made only by formal offering documents, which include, among others, a confidential offering memorandum, limited partnership agreement (if applicable), investment management agreement (if applicable), operating agreement (if applicable), and related subscription documents (if applicable). Please contact your professional adviser/consultant before making an investment decision.

Where possible we aim to disclose the material risks pertinent to this document, and as such these should be noted on the individual document pages. The views expressed in this document do not purport to be a complete description of the securities, markets and developments referred to in it. Reference to specific securities should not be considered a recommendation to buy or sell. Unigestion maintains the right to delete or modify information without prior notice. Unigestion has the ability in its sole discretion to change the strategies described herein.

Investors shall conduct their own analysis of the risks (including any legal, regulatory, tax or other consequences) associated with an investment and should seek independent professional advice. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment. These are not suitable for all types of investors.

To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks. Actual results could differ materially from those in the forward-looking statements. As such, forward looking statements should not be relied upon for future returns. Targeted returns reflect subjective determinations by Unigestion based on a variety of factors, including, among others, internal modeling, investment strategy, prior performance of similar products (if any), volatility measures, risk tolerance and market conditions. Targeted returns are not intended to be actual performance and should not be relied upon as an indication of actual or future performance.

No separate verification has been made as to the accuracy or completeness of the information herein. Data and graphical information herein are for information only and may have been derived from third party sources. Unigestion takes reasonable steps to verify, but does not guarantee, the accuracy and completeness of information from third party sources. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. All information provided here is subject to change without notice. It should only be considered current as of the date of publication without regard to the date on which you may access the information. Rates of exchange may cause the value of investments to go up or down. An investment with Unigestion, like all investments, contains risks, including total loss for the investor.

Unigestion Direct II (UDII) has been created as a SCS-SICAV-RAIF in Luxembourg and qualifies as an Alternative Investment Fund (AIF) within the meaning of the law dated 12 July 2013 on Alternative Investment Fund Managers implementing the Directive 2011/61/EU (AIFMD). As a result, units of this vehicle may be offered only to professional investors and may not be distributed on a public basis in or from any country where such distribution would be prohibited by law. This document contains a preliminary summary of the purpose and principal business terms of an investment in UDII. This summary does not purport to be complete and is qualified in its entirety by reference to the more detailed discussion to take place with the AIF. UDII has the ability in its sole discretion to change the strategies described herein. Before making a decision to invest in UDII, you are advised to consult with your tax, legal and financial advisors.

Additional Information for US Investors

The performance figures are based on estimated fees and expenses as well as on the underlying strategy’s estimated performances given by fund managers, administrators, custodians and third party sources at a given date. Where performance is reflected gross of fees, potential investors should be aware that the inclusion of fees, costs and charges will reduce the overall value of performance. Unless otherwise stated, the performance data source are Unigestion, Bloomberg and Compustat.

This information is provided to you solely to give you background information relating to Unigestion, certain strategies it implements and currently offers. Before making an investment decision with respect to the strategy discussed herein, potential investors are advised to consult with their tax, legal, ERISA and financial advisors. Note that not all strategies may be available or suitable for investment by U.S. investors.

This document may contain forward-looking statements, including observations about markets and industry and regulatory trends as of the original date of this document. Forward-looking statements may be identified by, among other things, the use of words such as “expects,” “anticipates,” “believes,” or “estimates,” or the negatives of these terms, and similar expressions. Forward-looking statements reflect Unigestion’s views as of such date with respect to possible future events. Actual results could differ materially from those in the forward-looking statements as a result of factors beyond a strategy’s or Unigestion’s control. Readers are cautioned not to place undue reliance on such statements. No party has an obligation to update any of the forward-looking statements in this document

Return targets or objectives, if any, are used for measurement or comparison purposes and only as a guideline for prospective investors to evaluate a particular investment program’s investment strategies and accompanying information. Performance may fluctuate, especially over short periods. Targeted returns should be evaluated over the time period indicated and not over shorter periods.

The past performance of Unigestion, its principals, shareholders, or employees is not indicative of future returns.

Except where otherwise specifically noted, the information contained herein, including performance data and assets under management, relates to the entire affiliated group of Unigestion entities over time including that of Unigestion UK. Such information is intended to provide the reader with background regarding the services, investment strategies and personnel of the Unigestion entities. No guarantee is made that all or any of the individuals involved in generating the performance on behalf the other Unigestion entities will be involved in managing any client account on behalf of Unigestion U.K. More specific information regarding Unigestion UK is set forth herein where indicated and is available on request.

There is no guarantee that Unigestion will be successful in achieving any investment objectives. An investment strategy contains risks, including the risk of complete loss.

The risk management practices and methods described herein are for illustrative purposes only and are subject to modification.

Legal Entities Disseminating This Document

UNITED KINGDOM

This material is disseminated in the United Kingdom by Unigestion (UK) Ltd., which is authorized and regulated by the Financial Conduct Authority („FCA“).

This information is intended only for professional clients and eligible counterparties, as defined in MiFID directive and has therefore not been adapted to retail clients.

US

This material is disseminated in the U.S. by Unigestion (UK) Ltd., which is registered as an investment adviser with the U.S. Securities and Exchange Commission (“SEC”). This information is intended only for institutional clients and qualified purchasers as defined by the SEC and has therefore not been adapted to retail clients.

EU

This material is disseminated in the European Union by Unigestion Asset Management (France) SA which is authorized and regulated by the French “Autorité des Marchés Financiers” („AMF“).

This information is intended only for professional clients and eligible counterparties, as defined in the MiFID directive and has therefore not been adapted to retail clients.

CANADA

This material is disseminated in Canada by Unigestion Asset Management (Canada) Inc. which is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario, Quebec and Newfoundland & Labrador. Its principal regulator is the Ontario Securities Commission („OSC“).

This material may also be distributed by Unigestion SA which has an international advisor exemption in Quebec, Saskatchewan and Ontario. Unigestion SA’s assets are situated outside of Canada and, as such, there may be difficulty enforcing legal rights against it.

SWITZERLAND

This material is disseminated in Switzerland by Unigestion SA which is authorized and regulated by the Swiss Financial Market Supervisory Authority („FINMA“).

Document issued November 2020.