- The popularity of Value investing has been challenged in recent years, but is once again set to gain traction.

- While Value investing has historically been subject to high levels of volatility, we show Value can be accessed at much reduced risk levels.

- Our analysis shows it is possible to build a long-only Value portfolio which has moderate risk while retaining most of the Value premium.

- Our enhanced Value investing methodology can be readily adapted to an investor’s own risk tolerance by modifying the blend of the underlying signals

Overview

After a torrid 2020, the relative stability of 2021 has left many investors questioning whether the environment is becoming more supportive for Value investing. In this paper, we delve into the Value factor to show its interesting relationship with volatility and identify why the factor is at its most efficient when exposed to more stable stocks. We also discover that the Value factor persists across the volatility spectrum, allowing investors to access the premium at lower levels of absolute risk. Investors can leverage these observations to gain exposure to the Value premium without taking on undesired – and unrewarded – risks.

Introduction

Value is a popular investing style with a long heritage, building from Graham and Dodd’s seminal work Security Analysis (first published in 1934) and exalted by prominent investors such as Warren Buffet. However, Value’s popularity has been challenged in recent years owing to broad underperformance. With investors now beginning to question the dominance of growth stocks, we investigate how best to extract the Value premium.

We are inspired by the vast literature that has identified that conditioning equity portfolios on their realised volatility helps deliver higher risk-adjusted returns (Moreira and Muir, 2017; Barroso and Santa Clara, 2017; Wang and Yan, 2021). Applying this lens of analysis to Value, we uncover the relationship between Value investing and volatility. In doing so, we combine the Value characteristic of stocks with their risk profile to build better portfolios.

We show that while Value investing may be associated with higher risks, investors are able to access the premium at much more moderate levels of volatility. For investors very sensitive to absolute levels of volatility, the Value premium within stable stocks dominates.

How Volatile is Value?

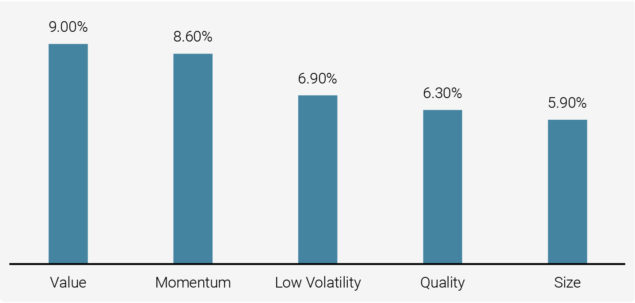

Recent experience has shown that Value investing can be subject to high levels of volatility. In Figure 1 we compare its volatility with those of the four other equity risk premia – Momentum, Quality, Low volatility and Size. Value dominates all in terms of risk.

Figure 1: Volatility of the Five Equity Risk Premia

Source: Unigestion. Long-short, quintile, ex-post Beta-adjusted factors on MSCI World – 31 December 1998 to 31.07.2021.

Our studies show that Value appears more attractive during periods in which its exposure to highly volatile stocks is low.

To better understand the style, we want to consider whether this is a natural positioning of Value, or if the relationship is more dynamic. We wish to uncover whether there are periods where it is more aligned with high volatility stocks than low volatility stocks (and vice versa). In doing so, we can then ask what this means for Value’s performance as it loads more heavily on more- or less-risky areas of the market.

We start by studying the score correlation. This gives an understanding of the extent to which two investment signals are similar. If the score correlation of two signals is 1 then they are identical; at 0, they are unrelated; and at -1 they oppose one another absolutely. Applying this metric to Value and the risk rank of stocks, we can observe whether the factor exposes itself more toward high or low volatility stocks.

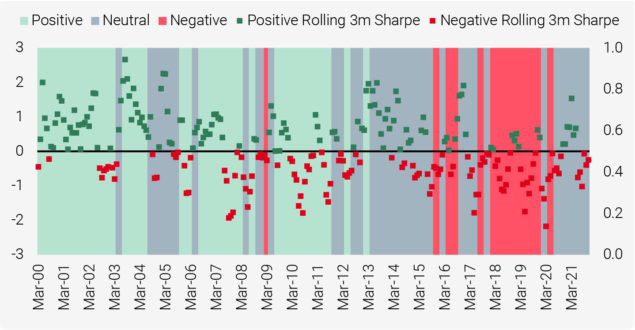

In Figure 2 we show the return to Value investing across time, categorised by the score correlation regime. This begins to give us a qualitative understanding of the relationship between Value investing and volatility.

Figure 2: Rolling 3-month Sharpe Ratio of Value by Score Correlation Regime

Source: MSCI World; Quintiles Long-short Beta Neutral. Data as at 30.11.2021. Reading note: Green positive; grey neutral; pink negative.

We can make two initial observations. Firstly, Value appears more attractive during periods in which its exposure to highly volatile stocks is low. Secondly, the environment of high volatility exposures appears to be waning, as the factor‘s volatility exposure transitions from negative to neutral over the course of 2021. This could mean better prospects for the returns from Value should the trend persist.

Stepping Inside the Value Factor

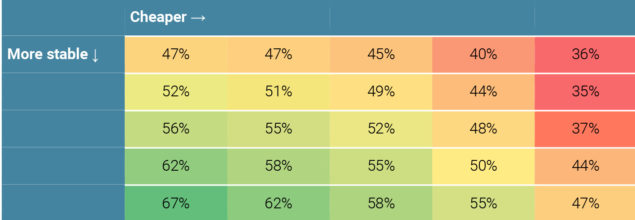

We can better contextualise the previous observations by considering the ‘doublesort.’ This follows a well-established but simplistic methodology which has long been used in factor research, including in the seminal work of Fama and French (1993). The investment universe is first divided into slices of increasing volatility, and then into slices of increasing cheapness. The result is a view on the return associated with cheap stocks for a given level of risk. While this does not represent a complete portfolio construction approach, it allows for the consideration of the conditional relationship between two signals in a well-diversified setting.

In Table 1 we show the risk-adjusted returns, with increasing cheapness as we move right along the table; and reducing volatility as we move down. This highlights the conditional relationship, showing immediately the impact on investment efficiency from increasing the exposure to Value or reducing volatility.

Table 1: Risk-Adjusted Returns for Combined Value/Volatility Portfolios

Source: Unigestion, MSCI World. Data for the period 31.12.1998 to 31.12.2020.

The risk-adjusted returns of the Value factor increase dramatically as one takes greater exposure to less volatile stocks.

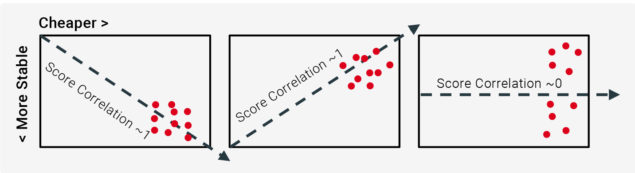

We can readily integrate this view with the score correlation analysis above. An increase in score correlation is associated with the ‘long’ Value portfolio being associated with the bottom right corner of the table; and a decrease, moving toward to the top right. This relationship is shown in Figure 3.

Figure 3: Relating Score Correlation to the Double-Sort Table

Sources: Unigestion

Extracting the Value Premium as a Long-only Investor

The investment efficiency of Value is improved in its exposure to lower volatility stocks. But what does this result mean for the long-only investor? In Table 2a we recast the double-sort table, but looking instead at total returns. If returns increase as we move right, we see a Value premium; as we go down, we see the change in return for reducing volatility.

Table 2a: Returns for Combined Value/Volatility Portfolios

Source: Unigestion, MSCI World. Data for the period 31.12.1998 to 31.12.2020.

Table 2b: Volatility for Combined Value/Volatility Portfolios

Source: Unigestion, MSCI World. Data for the period 31.12.1998 to 31.12.2020.

An investor is not required to take on high levels of risk to substantially capture all of the Value premium.

As expected, we observe a Value premium, with the right hand column dominating the left. However, significantly, we see a Value premium at every level of volatility. Indeed, regardless of the volatility level, the absolute return of the cheapest stocks dominates the return of the average stock.

Considering now Table 2b, here we report the volatility associated with each level of Value. The differences in risk are large. Firstly, this recovers the risk-adjusted observation from the prior section – with moderate improvements in return overwhelmed by large increases in risk. More significantly, it demonstrates how readily an investor may reflect their level of risk-tolerance.

Taking the two tables together, we can see that an investor is not required to take on high levels of risk to substantially capture the Value premium. Further, an investor may modify their exposure to suit their risk tolerance.

Technical Effect – With Fundamental Support

We observe that the Value premium persists across the volatility spectrum. The mechanical consequence of this is that we are able to increase investment efficiency, with volatility falling faster than the size of the premium. But could there be another dimension to the relative attractiveness of lower volatility stocks?

Using the discounted cash flow model, we can build an intuition on the linkage between earnings, certainty and stock volatility. This model posits that the price of a share today reflects the cash flows it will throw off in the future: bigger, more certain cash flows are valuable; while smaller or more distant cash flows are worth less. Under this framework we can expect that a more volatile stock price is the consequence of changing investor expectations about the size, timing or likelihood of future cash flows.

We can combine this intuition with a more explicit measure of fundamental stability, the profitability of the company. Harnessing the double-sort technique again, we can see the variation in company quality across the volatility and Value spectrum. Here, we express the quality of the double-sort portfolios as the equivalent position of a stock within the universe: for example, a score of 50% means better quality than half the universe, while 30% would mean being worse than 70%.

Table 3: Profitability Positioning for Combined Volatility/Value

Source: Unigestion, MSCI World. Data for the period 31.12.1998 to 31.12.2020.

As Table 3 shows it’s certainly the case that you need to pay up for quality in terms of profitability – with the most expensive stocks dominating each strata. However, price stability correlates with profitability even within the cheapest stocks. By considering both volatility and Value, investors are able to enjoy both relative price and corporate stability.

By considering both volatility and Value, investors are able to enjoy both relative price and corporate stability.

Investing in Value While Controlling Risks

The above results suggest that it should be possible to build a long-only Value portfolio which has moderate risk while retaining most, if not all, of the Value premium.

As noted previously, the double-sort is a useful tool to understand the conditional relationship between signals, but does not represent a full portfolio construction solution. To transform the observation into a portfolio-level signal, we make use of an ‘integrated’ score approach. Doing so allows us to express the trade-off between risktolerance and Value.

We construct a portfolio that minimizes country bets and seeks exposure to the top 1/9 of stocks having accounted for both Value and volatility, equally weighting the two signals to construct our integrated score. Our exposure is then akin to that of the bottom right corner of the double sort table. In Table 4 we show the results of a strategy that invests in cheap stocks – having accounted for their risk level.

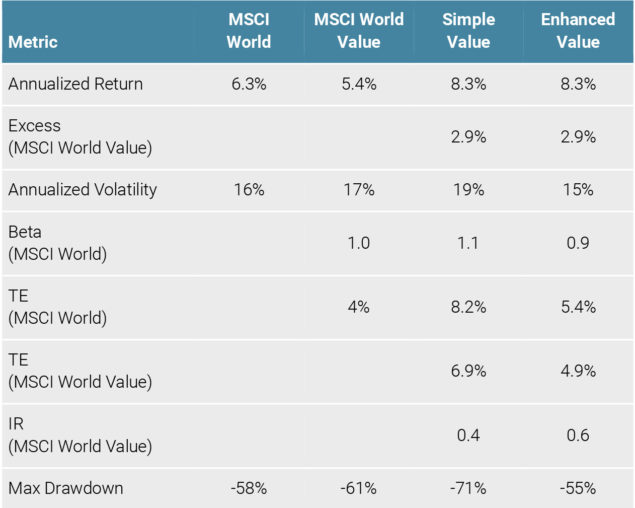

Table 4: Performance and Risk Metrics

Source: Unigestion, MSCI World. Data for the period 31.12.1998 to 30.09.2021. Inclusive of estimated transaction costs.

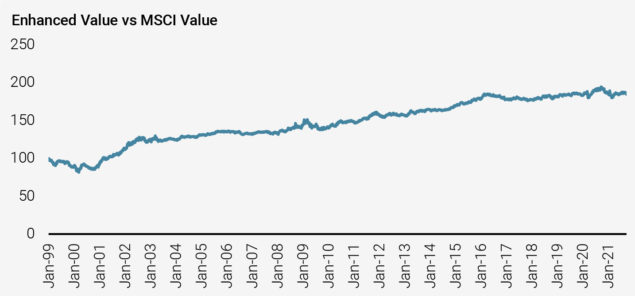

Figure 4: Performance Versus Alternative Implementations

Source: Unigestion, MSCI World. Data for the period 31.12.1998 to 30.09.2021. Inclusive of estimated transaction costs.

With this enhanced Value, we not only improve absolute return, but we also reduce absolute risk compared with a simple implementation. Building on an abstract observation on the nature of the relationship between Value and volatility, through a pragmatic portfolio construction approach we translate the advantage into an implementable, long-only strategy. The result is a more controlled way to gain exposure to Value investing, and one that may be readily adapted to an investor’s own risk tolerance by modifying the blend of the underlying signals.

Our enhanced Value methodology improves absolute returns and reduces absolute risk..

Conclusion

Holistic risk management is crucial to the efficient extraction of investment returns. While highly risky stocks can move in and out of favour, their contribution to portfolio risk is always significant. At Unigestion, we believe that risk management should permeate the entire investment process, from high level asset allocation to stock level decisions.

Simplistic Value investing is associated with elevated risks. However, by looking more closely at the relationship between Value and volatility in risk-adjusted terms, one is better rewarded for accessing cheap stocks outside the most volatile area of the market. This suggests a more supportive environment for Value investing when the strategy lands naturally on these more stable companies.

Taking the thought further, we show that the Value premium persists across the volatility spectrum. Investors may then tailor their Value exposure to be conscious of absolute risk. We show that by actively choosing to allocate to the stable area of the market, investors are able to access the benefits of Value investing with a reduced level of overall risk.

For investors such as us who are now anticipating a more supportive market environment for Value investing, this risk-controlled strategy offers a pragmatic alternative way of accessing the same attractive investment style.

References

Barroso P., Santa Clara P. (2015). Momentum has its Moments. Journal of Financial Economics, Vol. 116 Issue 1, pp 111-120.

Fama E., French K. (1993). Common Risk Factors in the Returns on Stocks and Bonds. Journal of Financial Economics, Vol. 33 Issue 1, pp 3-56.

Moreira A., Muir T. (2017). Volatility-Managed Portfolios. Journal of Finance, Vol. 72 Issue 4, pp 1611-1643.

Wang F., Yan X.S. (2021). Downside Risk and the Performance of Volatility-Managed Portfolios. Journal of Banking and Finance, Vol. 131 Issue C, pp 1-18.

Important information

Past performance is no guide to the future, the value of investments, and the income from them change frequently, may fall as well as rise, there is no guarantee that your initial investment will be returned. This document has been prepared for your information only and must not be distributed, published, reproduced or disclosed by recipients to any other person. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation.

This is a promotional statement of our investment philosophy and services only in relation to the subject matter of this presentation. It constitutes neither investment advice nor recommendation. This document represents no offer, solicitation or suggestion of suitability to subscribe in the investment vehicles to which it refers. Any such offer to sell or solicitation of an offer to purchase shall be made only by formal offering documents, which include, among others, a confidential offering memorandum, limited partnership agreement (if applicable), investment management agreement (if applicable), operating agreement (if applicable), and related subscription documents (if applicable). Please contact your professional adviser/consultant before making an investment decision.

Where possible we aim to disclose the material risks pertinent to this document, and as such these should be noted on the individual document pages. The views expressed in this document do not purport to be a complete description of the securities, markets and developments referred to in it. Reference to specific securities should not be considered a recommendation to buy or sell. Unigestion maintains the right to delete or modify information without prior notice. Unigestion has the ability in its sole discretion to change the strategies described herein.

Investors shall conduct their own analysis of the risks (including any legal, regulatory, tax or other consequences) associated with an investment and should seek independent professional advice. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment. These are not suitable for all types of investors.

To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks. Actual results could differ materially from those in the forward-looking statements. As such, forward looking statements should not be relied upon for future returns. Targeted returns reflect subjective determinations by Unigestion based on a variety of factors, including, among others, internal modeling, investment strategy, prior performance of similar products (if any), volatility measures, risk tolerance and market conditions. Targeted returns are not intended to be actual performance and should not be relied upon as an indication of actual or future performance.

No separate verification has been made as to the accuracy or completeness of the information herein. Data and graphical information herein are for information only and may have been derived from third party sources. Unigestion takes reasonable steps to verify, but does not guarantee, the accuracy and completeness of information from third party sources. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. All information provided here is subject to change without notice. It should only be considered current as of the date of publication without regard to the date on which you may access the information. Rates of exchange may cause the value of investments to go up or down. An investment with Unigestion, like all investments, contains risks, including total loss for the investor.

Legal Entities Disseminating This Document

UNITED KINGDOM

This material is disseminated in the United Kingdom by Unigestion (UK) Ltd., which is authorized and regulated by the Financial Conduct Authority („FCA“). This information is intended only for professional clients and eligible counterparties, as defined in MiFID directive and has therefore not been adapted to retail clients.

UNITED STATES

This material is disseminated in the U.S. by Unigestion (UK) Ltd., which is registered as an investment adviser with the U.S. Securities and Exchange Commission (“SEC”). This information is intended only for institutional clients and qualified purchasers as defined by the SEC and has therefore not been adapted to retail clients.

EUROPEAN UNION

This material is disseminated in the European Union by Unigestion Asset Management (France) SA which is authorized and regulated by the French “Autorité des Marchés Financiers” („AMF“).

This information is intended only for professional clients and eligible counterparties, as defined in the MiFID directive and has therefore not been adapted to retail clients.

CANADA

This material is disseminated in Canada by Unigestion Asset Management (Canada) Inc. which is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario, Quebec and Newfoundland & Labrador. Its principal regulator is the Ontario Securities Commission („OSC“). This material may also be distributed by Unigestion SA which has an international advisor exemption in Quebec, Saskatchewan and Ontario. Unigestion SA’s assets are situated outside of Canada and, as such, there may be difficulty enforcing legal rights against it.

SWITZERLAND

This material is disseminated in Switzerland by Unigestion SA which is authorized and regulated by the Swiss Financial Market Supervisory Authority („FINMA“).

Document issued February 2022.