- Der Sekundärmarkt kam mit Beginn der COVID-19-Pandemie zum Stillstand, aber die Aktivität nimmt jetzt wieder zu, vor allem am kleineren Ende des Marktes.

- Liquiditätsprobleme sowohl für GPs als auch LPs schaffen eine einzigartige Opportunität bei strukturierten und GP-geführten Transaktionen am kleineren Ende des Marktes.

- Unigestion ist gut positioniert diese Chance zu nutzen, da wir dieses Jahr bereits mehrere komplexe, GP-geführte Transaktionen erfolgreich abgeschlossen haben.

Überblick

COVID-19 war für den Sekundärmarkt ein Schock. Transaktionsvolumen fielen massiv im 2. Quartal 2020, insbesondere am größeren Ende des Marktes, wo LP-Portfolioverkäufe völlig zum Erliegen kamen.

Am kleineren Ende des Sekundärmarktes erholte sich die Aktivität jedoch schneller und bietet nun mehr Opportunitäten. Einerseits haben kleinere Verkäufer, wie z. B. Family Offices, Positionen rasch auf dem Sekundärmarkt verkauft, um Liquiditätsbedürfnisse zu decken oder ihre Portfolios nach den ersten COVID-19-Lockdowns umzuschichten. Zum anderen gab es angesichts des Rückgangs der Exits eine große Anzahl kleinerer GP-geführter Transaktionen wie Fondsumstrukturierungen und Sidecar-Fonds – GPs versuchen, sowohl Liquidität für ihre LPs zu generieren als auch ihre Portfoliounternehmen zu unterstützen. Darüber hinaus hat die anhaltende Pandemie die Fristen für das Fundraising der GPs verlängert und somit den Bedarf an alternativen Finanzierungslösungen am Sekundärmarkt verschärft.

Unigestion konzentriert sich auf kleine, komplexe Sekundärmarkttransaktionen, die in der Regel GP-geführt sind. Dank der zahlreichen Opportunitäten, die wir am kleineren Ende des Marktes sehen, haben wir in den letzten Monaten mehrere einzigartige Deals erfolgreich abgeschlossen. Im Folgenden erörtern wir die aktuelle Lage auf dem Sekundärmarkt und warum sich unseres Erachtens am kleinen Ende des Marktes so attraktive Opportunitäten für GP-geführte Transaktionen ergeben.

COVID-19 – ein Schock für den Sekundärmarkt

Mit dem Ausbruch von COVID-19 in den westlichen Volkswirtschaften kam der Sekundärmarkt völlig zum Stillstand und das Transaktionsvolumen in Q2 2020 fiel auf ein Rekordtief.

Der unmittelbare starke Kurseinbruch an den öffentlichen Märkten führte zu einer Diskrepanz zwischen den NIWs der Referenzfonds (insbesondere den Bewertungen für Q4 2019) und den Marktbewertungen im neuen, nach COVID-19 entstandenen Marktumfeld. Negative Marktbewegungen und wirtschaftliche Ungewissheit haben daher im zweiten Quartal viele Sekundärmarktprozesse gestört. Infolgedessen wurden die meisten Transaktionen auf Eis gelegt, um eine Stabilisierung der Märkte abzuwarten und die Auswirkungen der Krise auf die Zielunternehmen zu erfassen.

Einige Käufer haben angesichts der Ungewissheit über das Ausmaß und die Dauer der Auswirkungen der Pandemie ein Moratorium für neue Transaktionen verhängt. Bei den bereits abgeschlossenen Deals zeichneten aktive Käufer meist höhere Abschläge und gingen von einem konservativen EBITDA Wachstum und Exit Timing aus. Allerdings taten sich die nicht notleidenden potenziellen Verkäufer schwer, höhere Abschläge zu akzeptieren, was zu großen Geld-Brief Spannen und rekordniedrigen Transaktionsvolumina in Q2/Anfang Q3 führte.

Anzeichen einer Erholung

Käufer und Verkäufer warteten zunächst die NIWs für Q1 ab, bevor sie wieder Transaktionen tätigten. Meist wurde sogar auf die Bewertungen des 2. Quartals gewartet, um einen klareren Überblick über die vollen Auswirkungen der ersten Welle von COVID-19 zu erhalten.

Gleichzeitig wurden die LPs von den Fondsmanagern über die Auswirkungen auf Einnahmen, finanziellen Spielraum und revidierte Prognosen für die Portfoliounternehmen, einschließlich des Exit-Timings, informiert. Dies ermöglichte es Sekundärmarkt Anlegern, Transaktionen wieder zu bepreisen.

In den meisten Fällen erreichten die Portfoliobewertungen in Q1 und/oder Q2 einen Tiefpunkt. Nun ist in allen Portfolios ein Stabilisierungstrend erkennbar. Allerdings sind die COVID-19-Fallzahlen in Europa und Nordamerika in den letzten Wochen deutlich angestiegen, was erneut ein hohes Maß an Unsicherheit auf den Sekundärmärkten erzeugt.

Eine schnellere Erholung am kleineren Ende

Im Gegensatz zum breiteren Markt hat sich in den ersten Monaten der Pandemie (d.h. im 2. und 3. Quartal des letzten Jahres) das Zeitfenster für kleinere Sekundärtransaktionen viel schneller wieder geöffnet.

Bei größeren LP-Portfolioverkäufen legten die meisten potenziellen Verkäufer – in der Regel große institutionelle Investoren – die Verhandlungen im zweiten und dritten Quartal auf Eis und warteten auf eine Verbesserung der Markt- und Bewertungslage. Außerdem sind bisher keine großen notleidenden Verkäufer aufgetaucht (wenn überhaupt), wie es in den Jahren 2008/09 der Fall war (damals waren es hauptsächlich Banken und Finanzinstitute).

Kleinere Investoren (z.B. Family Offices) haben demgegenüber viel schnellere und einfachere Entscheidungsprozesse und sind tendenziell weniger preissensibel. Im Zuge der COVID-19 führten Rebalancing- und Liquiditätsanforderungen zu einer Reihe von Verkaufsentscheidungen einzelner LP-Positionen oder kleiner Portfolios sowie zu einer größeren Bereitschaft, angesichts der anhaltenden Marktvolatilität erhebliche Abschläge zu akzeptieren.

Ein ähnliches Bild ergibt sich im GP-geführten Bereich, einschließlich Fondsumstrukturierungen und (Single- oder Multi-Asset) Continuation Fonds. In den meisten Fällen wurden größere GP-geführte Deals (über USD 180 Mio.) auf Eis gelegt, werden aber nun langsam aber sicher wieder aufgenommen. Am kleineren Ende hat Unigestion eine Reihe von GP-geführten Deals mit einer Größe von bis zu USD 100 Mio. durchgeführt. Dies ist ein Segment, das von Vermittlern weniger abgedeckt wird, mit kürzeren Entscheidungsprozessen und der Bereitschaft, kleinere Club-Deals anstelle von größeren, wettbewerbsintensiveren Syndication-geführten Deals zu tätigen. Darüber hinaus ist es für Käufer bei kleinen GP-geführten Deals einfacher, die besten Portfoliounternehmen auszuwählen, als ganze Portfolios mit einem Mix aus guten und schlechten Unternehmen zu akzeptieren.

Am kleineren Ende hat Unigestion zahlreiche GPgeführte Deals von bis zu EUR 80 Mio. durchgeführt.

Verlangsamte Exit-Aktivität führt zu alternativen Finanzierungsmöglichkeiten

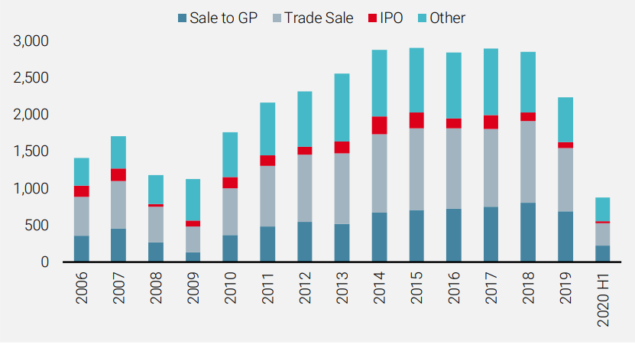

Im Verlauf der Pandemie haben sich die traditionellen Exit-Märkte deutlich verlangsamt, wie in Abbildung 1 dargestellt. Weltweit gab es in H1 2020 nur 874 Exits, verglichen mit 1.238 Exits in H1 2019.

Abbildung 1: Private Equity Exits (Deals pro Quartal)

Quelle: Pitchbook. Daten zum 30. Juni 2020.

Aufgrund der COVID-bedingten Sorgen mussten viele LPs jedoch mit einer hohen Nachfrage nach Kapitalabrufen kämpfen, um belastete Portfolios zu stützen oder GPs zu ermöglichen, Deal-Chancen in einem Krisenumfeld zu nutzen. Dieser Anstieg der Nettomittelabflüsse für LPs führt bei bestimmten Anlegern zu Liquiditätsproblemen und einem Bedarf an Portfolio-Rebalancing. Daher erwarten wir ab Q1 2021 eine erhöhte Anzahl von LP Einzel- und Portfolioverkäufen.

Gleichzeitig suchen GPs, die mit geringer Aktivität in den traditionellen Exit-Märkten konfrontiert sind, nach alternativen Liquiditätslösungen für ihre Fonds, um ihre Cash-hungrigen Investoren zu befriedigen, was zu einer steigenden Zahl von Continuation Funds und Fondsumstrukturierungen führt.

GPs, die mit geringer Aktivität in traditionellen Exit-Märkten konfrontiert sind, suchen nach alternativen Liquiditätsoptionen für ihre Fonds.

Da die Zahl der kleinen und mittleren GPs im Vergleich zu den Large Cap GPs viel größer ist, gibt es einfach mehr kleine GPs mit Tail-End Fonds und reifenden Portfolios. Dies schafft einen fruchtbaren Boden für kleinere strukturierte Transaktionen, die unter dem Radar der großen sekundären Intermediäre und Investoren fallen.

Bedarf an Portfoliounterstützung

Zusätzlich zu den reduzierten Fundraising- und Exit Aktivitäten müssen GPs auch ihre bestehenden Portfolios sorgfältig verwalten. Die aktuelle Krise bringt sowohl Herausforderungen als auch Opportunitäten mit sich. Erstens benötigen bestimmte Portfoliounternehmen – meist solche in zyklischen Branchen, die gegenüber der COVID-Krise empfindlicher sind und einen hohen Investitionsbedarf haben – möglicherweise mehr Liquidität. Zweitens könnten die stärkeren Portfoliounternehmen – entweder resistent oder sogar positiv von der COVID-Pandemie beeinflusst – weitere Finanzierungen erfordern, um die Expansion zu unterstützen oder selektive Add-on-Akquisitionen zu tätigen.

Dies schafft eine bedeutende Opportunität für strukturierte und GP-geführte Transaktionen am kleineren Ende des Marktes, wo Deals problemlos maßgeschneidert werden können, um sich nur auf die leistungsstärksten Portfoliounternehmen zu konzentrieren. So kann ein GP beispielsweise innovative Sidecar- oder Bridge-Fonds-Strukturen einrichten, meist in Verbindung mit Vorzugskonditionen für die zugrunde liegenden Finanzinstrumente. In den ersten Monaten der Pandemie hat Unigestion verschiedene Lösungen zur Portfoliounterstützung am kleineren Ende des Marktes eingerichtet. So haben wir beispielsweise einen Sidecar-Fonds aufgelegt, um gemeinsam mit einem skandinavischen Wachstumskapitalmanager zwei Unternehmen zu unterstützen, die von COVID positiv beeinflusst wurden und zusätzliches Kapital benötigten, um ihren steilen Wachstumspfad fortzusetzen.

Das Argument für COVID-19 widerstandsfähige und profitierende Unternehmen

Die Zukunft ist zwar höchst ungewiss, aber die Pandemie wird sich voraussichtlich weiterhin unterschiedlich und ungleich auf die verschiedenen Branchen und Sektoren auswirken:

- Stark betroffene Sektoren: z. B. Transport, Hotel- und Gaststättengewerbe, Reisebranche

- Moderat betroffene Sektoren: z. B. Finanzdienstleister, Unternehmensdienstleistungen

- Neutral betroffene Sektoren (COVID-Resilienz): z. B. Gesundheitsdienste, Lebensmittel & Getränke, Technologie/Software

- Positiv betroffene Sektoren (COVID-Gewinner): z. B. E-Commerce-Geschäftsmodelle, Produkte, die Lösungen für COVID-19 bedingte Probleme bieten

Anleger werden wahrscheinlich erhebliche Abschläge für Portfolios von Unternehmen in stark betroffenen Sektoren erhalten. Die sekundäre Strategie von Unigestion behält jedoch einen klaren Fokus auf Portfolios von Unternehmen in neutralen oder positiv beeinflussten Sektoren, d.h. COVID-resistenten oder profitierenden Unternehmen. Angesichts der anhaltenden Ungewissheit bezüglich der Pandemie sind wir der Meinung, dass dies die einzigen Kategorien sind, in denen die Aussichten vernünftig bewertet werden können.

Unigestions Sekundärmarktstrategie konzentriert sich auf Portfolios von Unternehmen in neutralen oder positiv beeinflussten Sektoren.

Erfolgreiche Positionierung in einem hart umkämpften Markt

Wie erwartet, hat die Pandemie einen Rückgang der Sekundärmarkt Deal Aktivitäten bewirkt, insbesondere am größeren Ende des Marktes. Darüber hinaus waren große Sekundärmarkttransaktionen, die trotz der Krise zustande kamen, angesichts der hohen Bestände an Dry Powder unter den großen Teilnehmern hart umkämpft.

Weniger erwartet sind die einzigartigen Opportunitäten, die die Pandemie am unteren Ende des Marktes geschaffen hat. Der Bedarf von schnellen und opportunistischen Verkäufern sowie ein starker Strom von GP-geführten/strukturierten Opportunitäten, um LPs Liquidität zu geben und bestehende Portfolios zu unterstützen, sind viel früher als erwartet aufgetreten.

Ein flexibler und dynamischer Sekundärmarktansatz sowie ein außergewöhnlicher Zugang zum Dealflow sind jedoch unerlässlich, um die aktuellen Opportunitäten am kleinen Ende des Sekundärmarktes voll auszuschöpfen.

Wichtige Informationen

Die Wertentwicklung in der Vergangenheit liefert keinen Hinweis auf die Zukunft. Der Wert einer Anlage und ihre Erträge ändern sich häufig und können fallen oder steigen. Es gibt keine Garantie, dass Sie den ursprünglich angelegten Betrag zurückerhalten. Dieses Dokument wurde lediglich zu Informationszwecken erstellt. Seine Verteilung, Veröffentlichung, Vervielfältigung oder Weitergabe an Dritte durch den Empfänger ist untersagt. Es ist nicht dazu erstellt oder bestimmt, von einer natürlichen oder juristischen Person verbreitet oder verwendet zu werden, die Bürger oder Einwohner eines Ortes, eines Staates, eines Landes oder einer Gerichtsbarkeit ist, in denen eine solche Verbreitung, Veröffentlichung, Verfügbarkeit oder Verwendung gegen geltende Gesetze oder Vorschriften verstößt.

Dieses Dokument stellt eine Werbung für die Investmentphilosophie und die Dienstleistungen von Unigestion dar und bezieht sich ausschließlich auf den Gegenstand dieser Präsentation. Es stellt weder eine Anlageberatung noch eine Anlageempfehlung dar. Dieses Dokument stellt keinerlei Angebot, Aufforderung oder Vorschlag der Eignung zur Zeichnung in den von ihm genannten Anlageinstrumenten dar. Ein Verkaufsangebot oder die Anforderung eines Kaufangebots dürfen nur über formelle Angebotsdokumente erfolgen, die u.a. ein vertrauliches Angebotsmemorandum, einen Kommanditgesellschaftsvertrag (falls zutreffend), einen Anlageverwaltungsvertrag (falls zutreffend), einen Betriebsvertrag (falls zutreffend) und zugehörige Zeichnungsdokumente (falls zutreffend) umfassen. Vor jeder Anlageentscheidung wenden Sie sich bitte an Ihren professionellen Finanzberater.

Nach Möglichkeit legen wir die hierfür relevanten Risiken in diesem Dokument offen, die auf den entsprechenden Seiten zur Kenntnis zu nehmen sind. Die in diesem Dokument zum Ausdruck gebrachten Überzeugungen stellen keine vollständige Beschreibung der betreffenden Wertpapiere, Märkte und Entwicklungen dar. Verweise auf bestimmte Wertpapiere sind nicht als Empfehlung zu deren Kauf oder Verkauf aufzufassen.

Anleger müssen ihre eigene Risikoanalyse (unter Berücksichtigung rechtlicher, steuerlicher und anderer Konsequenzen) zu einer Anlage durchführen und sollten unabhängigen, professionellen Rat einholen. Einige der Anlagestrategien, die hierin beschrieben sind oder auf die verwiesen wird, gelten als hochriskante und nicht leicht realisierbare Anlagen, die wesentlichen und plötzlichen Verlusten unterworfen sein können, einschließlich eines kompletten Verlusts des Anlagewerts. Diese Strategien eignen sich nicht für alle Arten von Anlegern.

Sofern vorliegendes Dokument Aussagen über die Zukunft enthält, handelt es sich um zukunftsgerichtete Informationen, die mehreren Risiken und Unwägbarkeiten unterliegen, einschließlich der Auswirkungen von Konkurrenzprodukten, Marktakzeptanz- und sonstiger Risiken, wobei diese Aufzählung keinen Anspruch auf Vollständigkeit erhebt. Die tatsächlichen Ergebnisse könnten erheblich von den Ergebnissen in den zukunftsgerichteten Aussagen abweichen. Zukunftsgerichtete Aussagen sind deshalb nicht als Garantie für künftige Renditen zu verstehen. Anvisierte Renditen spiegeln subjektive Annahmen von Unigestion basierend auf einer Vielzahl von Faktoren wider, darunter interne Modelle, Anlagestrategie, bisherige Performance ähnlicher Produkte (falls vorhanden), Volatilitätsmaßnahmen, Risikotoleranz und Marktbedingungen. Anvisierte Renditen sollen nicht die tatsächliche Performance darstellen und sollten nicht als Indikator für tatsächliche oder zukünftige Performance betrachtet werden.

Die Daten und grafischen Informationen in diesem Dokument dienen ausschließlich Hinweiszwecken und stammen unter Umständen aus externen Quellen. Unigestion ergreift alle angemessenen Maßnahmen, um die Richtigkeit und Vollständigkeit dieser Informationen zu überprüfen, übernimmt diesbezüglich jedoch keine Gewähr. Folglich übernimmt Unigestion diesbezüglich weder eine ausdrückliche noch eine stillschweigende Gewährleistung oder Garantie, so dass jedwede Haftung hierfür ausgeschlossen ist. Alle an dieser Stelle zur Verfügung gestellten Informationen können ohne Vorankündigung geändert werden. Sie sind nur zum Zeitpunkt ihrer Veröffentlichung aktuell, unabhängig davon, wann der Empfänger sie zur Kenntnis nimmt. Veränderungen der Wechselkurse können dazu führen, dass der Wert der Anlagen steigt oder sinkt. Eine Investition bei Unigestion birgt Risiken wie alle anderen Investitionen, einschließlich des Totalverlustes für den Investor.

Unigestion Secondary V wird als SCS-SICAV-RAIF in Luxemburg gegründet und als alternativer Investmentfond (AIF) gemäß dem Gesetz vom 12. Juli 2013 zu Verwaltern alternativer Investmentfonds zur Umsetzung der Richtlinie 2011/61/EU (AIFMD) zugelassen werden. Daher dürfen Anteile an diesem Vehikel nur professionellen Anlegern angeboten werden. Ein öffentlicher Verkauf von Anteilen ist in Ländern, in denen ein derartiger Verkauf gesetzlich untersagt ist, nicht vorgenommen werden. Dieses Dokument enthält eine vorläufige Zusammenfassung des Zwecks und der Hauptgeschäftsbedingungen einer Investition in Unigestion Secondary V. Diese Zusammenfassung erhebt keinen Anspruch auf Vollständigkeit. Es wird auf die ausführlichen Gespräche verwiesen, die mit dem AIF stattfinden und im Zweifelsfall statt dieser Zusammenfassung gelten. Unigestion Secondary V wird nach alleinigem Ermessen die hierin beschriebenen Strategien ändern können. Bevor Sie eine Entscheidung zur Investition in Unigestion Secondary V treffen, sollten Sie bei Ihren Steuer-, Rechts- und Finanzberatern Rat einholen.

AN DER VERBREITUNG DIESES DOKUMENTS BETEILIGTE JURISTISCHE PERSONEN

Vereinigtes Königreich

Dieses Material wird im Vereinigten Königreich von Unigestion (UK) Ltd., die durch die Financial Conduct Authority („FCA“) zugelassen und von dieser reguliert wird, verbreitet.

Diese Informationen richten sich ausschließlich an professionelle Kunden und zulässige Gegenparteien im Sinne der Definition in der MiFID-Richtlinie und wurden daher nicht zur Verwendung durch Privatkunden angepasst.

Europäische Union

Dieses Material wird in der Europäischen Union durch Unigestion Asset Management (France) S.A., die durch die französische Autorité des Marchés Financiers („AMF“) zugelassen und reguliert wird, verbreitet.

Diese Informationen richten sich ausschließlich an professionelle Kunden und zulässige Gegenparteien im Sinne der Definition in der MiFID-Richtlinie und wurden daher nicht zur Verwendung durch Privatkunden angepasst.

Kanada

Dieses Material wird in Kanada durch Unigestion Asset Management (Canada) Inc. verbreitet, die in neun kanadischen Provinzen als Portfoliomanager und/oder befreiter Markthändler und in Ontario und Quebec als Verwalter von Investmentfonds zugelassen ist. Die Hauptaufsichtsbehörde ist die Ontario Securities Commission („OSC“).

Dieses Material kann auch von Unigestion SA verteilt werden, die eine Ausnahmeregelung für internationale Berater in Ontario, Quebec und Neufundland & Labrador in Anspruch nimmt. Die Vermögenswerte von Unigestion SA befinden sich außerhalb Kanadas, sodass es schwierig sein kann, Rechtsansprüche gegen Unigestion SA durchzusetzen.

Schweiz

Dieses Material wird von Unigestion SA, die durch die Eidgenössische Finanzmarktaufsicht („FINMA“) zugelassen und von dieser reguliert wird, verbreitet.