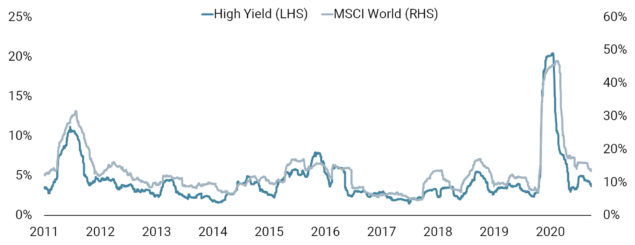

Volatility has strongly receded in high yield, diverging meaningfully with the trajectory in equity volatility that remains well above historical lows. This is another indication of rising complacency and a disconnection between typically very correlated risk premia. Beta to equities has decreased materially too, which also explains the divergence in volatility compression between the two asset classes.

Stocks have room to expand multiples further, driven by flows and the lack of decent alternatives, while current pricing and positioning in credit leaves little room for further spread compression. Credit is also vulnerable to macro shocks and global deleveraging, but lower liquidity in the asset class makes it more sticky and typically less impacted by technical sell-offs than equities. During the last week of January, the MSCI World index dropped by 4% but major high yield indices only lost 75bps, less than half the loss historical correlations would have implied.

Consequently, we believe that positioning and sentiment in credit has reached extremely high levels, leaving it vulnerable to the high macro volatility environment and inflation risk that we expect in the year ahead. Spreads have bottomed over the short term and we expect little spread compression, if not widening.

Source: Bloomberg, Unigestion. Data as at 22 February 2021.

Important Information

The information and data presented in this page may discuss general market activity or industry trends but is not intended to be relied upon as a forecast, research or investment advice. It is not a financial promotion and represents no offer, solicitation or recommendation of any kind, to invest in the strategies or in the investment vehicles it refers to. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment.

The investment views, economic and market opinions or analysis expressed in this page present Unigestion’s judgement as at the date of publication without regard to the date on which you may access the information. There is no guarantee that these views and opinions expressed will be correct nor do they purport to be a complete description of the securities, markets and developments referred to in it. All information provided here is subject to change without notice. To the extent that this page contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks.

Data and graphical information herein are for information only and may have been derived from third party sources. Although we believe that the information obtained from public and third party sources to be reliable, we have not independently verified it and we therefore cannot guarantee its accuracy or completeness. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. Unless otherwise stated, source is Unigestion.

Past performance is not a guide to future performance. All investments contain risks, including total loss for the investor.