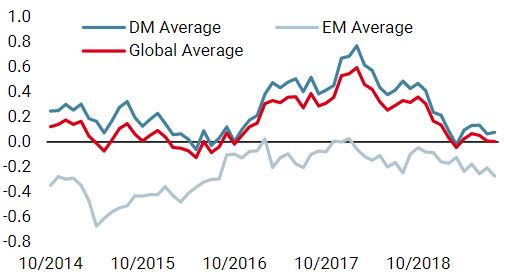

August has been a difficult month for risky assets thus far. In total return terms, the MSCI All Country World index is down 4%, with the Emerging Market index down 6%. The Bloomberg Commodity index is down nearly 3% and the Barclays Global High Yield index is down 2%. Hedging assets have provided some cushion, with the Barclays Global Aggregate index up 2%, gold up 7% and the Japanese yen up 3% against a trade-weighted basket, while the Swiss franc rose about 2% against the euro. Investors are clearly concerned about the possibility of an oncoming recession, and with central banks unlikely to announce new policy for a few weeks, sentiment will be in the driver’s seat. Until this dynamic changes and we see central bank policy or macro fundamentals reassert themselves, we will be waiting. For most of this year, investors have largely dismissed a deteriorating macro picture, taking comfort in the dovish pivot by most central banks. Bad news was good news since it made the case clearer for more accommodative monetary policy. The month of August however has seen some of this sky-high faith in the ability of central banks to reverse a downturn come down to earth. A plethora of evidence points to investor sentiment turning more sceptical on the prospects for global growth: As we have previously communicated, global growth has been steadily declining since early 2018. For the last few months, we have seen a stabilisation around potential levels, but with important divergences: The developed world has seen a small bounce (driven mostly by the US), while the emerging world has seen a modest decline (due mostly to China). Typically, the economy does not stay at potential levels for long, especially after a strong deterioration, as pressure to support the expansion leads to fiscal and/or monetary stimulus or the downward trend is too strong and recession follows.„I’ll Be Waiting“ – Adele, 2011

What’s Next?

Is bad news finally bad news?

What are the prospects for global growth?

Today, there is a clear tension between the US economy and the rest of the world, and the future path of the global economy depends on how this tension is resolved. Our proprietary Nowcasters, which incorporate hundreds of data series across the various facets of the economy, point to growth in the US being rather healthy. Although the US economy is not expanding as quickly as it was a year ago, it still looks to be growing above potential levels, supported by investment, employment, and consumption. Financing conditions do not appear restrictive, despite the rise of the Fed funds target rate. Thus, in our view, the likelihood of an imminent recession in the US remains rather low, despite the inversion of the yield curve.

The Eurozone is at much greater risk, however. We have highlighted for some time that the region has been close to recessionary levels, according to our Nowcaster, dragged down by employment, consumption, and production. Given the Eurozone’s strong link to global growth via external trade, the broader global growth slowdown, as well as trade uncertainty, has hit these economies hard. Importantly, financing conditions are not a drag and, in our view, the supply of credit in the region is not an issue. This is one of the reasons we are sceptical that a lower deposit rate, refinancing operations, or quantitative easing will be sufficient to shake the Eurozone’s real economy out of its malaise (though the impact on its financial markets would be quite positive).

The Chinese economy also appears to be at risk, in our view. It has been hit by both weaker housing and external demand, the latter a natural consequence of global trade uncertainty. While policymakers have many tools at their disposal to stimulate domestic demand, they have little control over the uncertainty emanating from the White House, as the past week (and year) has shown. Indeed, we have seen a strong deterioration in our Chinese Growth Nowcaster over the last few months, which fell from around potential to levels indicative of a significant slowdown at end of last month. On a positive note, consumption, production, and financing conditions are still decent.

The central macro question is whether easier Fed policy and a resilient US economy will be able to pull up the global economy or whether trade uncertainty and weak rest-of-world demand will drag the US down with the others into recession. It is difficult to say which of these is likely to transpire, and with a host of central bank meetings behind us, the ebb and flow of investor sentiment will drive markets. Valuations have retraced somewhat, but there are few obvious opportunities and hedging assets remain expensive. While we think central banks will continue responding to the economic slowdown with more accommodation, thereby buoying markets, we have become more cautious in our exposures. Markets will likely focus on sentiment, which remains challenging for many assets. In particular, we are largely neutral on equity markets, underweight credit, and slightly overweight sovereign bonds. We also continue to implement option strategies that will benefit from a large equity correction. Until we perceive that the market is ready to shift its focus from rather negative sentiment to a central bank-backed positive macro momentum, we think it is best to remain cautious.Where do we go from here?

I’ll Be Waiting

Our medium-term views remain cautious, and we are pairing an overweight in government bonds with an underweight in high yield corporate credit. We are also complementing our equity exposure with options to protect the portfolio in the case of equity drawdowns. Over the month of August, the Uni-Global – Cross Asset Navigator fund is down 0.4% while the MSCI AC World Index lost 3.8% and the Barclays Global Aggregate (USD hedged) is up 1.9%. Year-to-date, the Uni-Global – Cross Asset Navigator has returned 7.9% versus 12.1% for the MSCI AC World index, while the Barclays Global Aggregate (USD hedged) index is up 8.9%.Strategy Behaviour

Performance Review

Unigestion Nowcasting

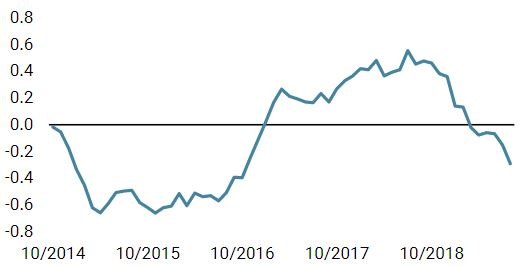

World Growth Nowcaster

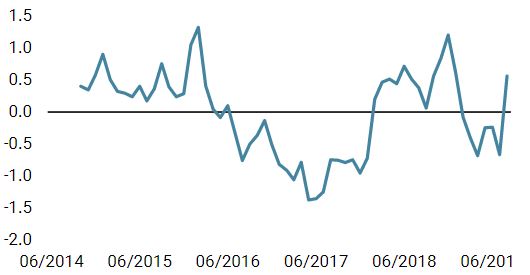

World Inflation Nowcaster

Market Stress Nowcaster

Weekly Change

- Our world Growth Nowcaster dropped marginally over the past week, driven by lower growth conditions in both developed and emerging markets.

- Our world Inflation Nowcaster decreased sharply this week once again, mainly driven by the lower inflation prospects in the US.

- Market stress remained unchanged at very high levels.

Sources: Unigestion. Bloomberg, as of 19 August 2019.

Navigator Fund Performance

|

Performance, net of fees |

2018 | 2017 | 2016 | 2015 |

| Navigator (inception 15 December 2014) | -3.6% | 10.6% | 4.4% |

-2.2% |

Past performance is no guide to the future, the value of investments can fall as well as rise, there is no guarantee that your initial investment will be returned.

Important Information

Past performance is no guide to the future, the value of investments, and the income from them change frequently, may fall as well as rise, there is no guarantee that your initial investment will be returned. This document has been prepared for your information only and must not be distributed, published, reproduced or disclosed by recipients to any other person. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. This is a promotional statement of our investment philosophy and services only in relation to the subject matter of this presentation. It constitutes neither investment advice nor recommendation. This document represents no offer, solicitation or suggestion of suitability to subscribe in the investment vehicles to which it refers. Any such offer to sell or solicitation of an offer to purchase shall be made only by formal offering documents, which include, among others, a confidential offering memorandum, limited partnership agreement (if applicable), investment management agreement (if applicable), operating agreement (if applicable), and related subscription documents (if applicable). Please contact your professional adviser/consultant before making an investment decision.

Where possible we aim to disclose the material risks pertinent to this document, and as such these should be noted on the individual document pages. The views expressed in this document do not purport to be a complete description of the securities, markets and developments referred to in it. Reference to specific securities should not be considered a recommendation to buy or sell. Investors shall conduct their own analysis of the risks (including any legal, regulatory, tax or other consequences) associated with an investment and should seek independent professional advice. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment. These are not suitable for all types of investors.

To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks. Actual results could differ materially from those in the forward-looking statements. As such, forward looking statements should not be relied upon for future returns. Targeted returns reflect subjective determinations by Unigestion based on a variety of factors, including, among others, internal modeling, investment strategy, prior performance of similar products (if any), volatility measures, risk tolerance and market conditions. Targeted returns are not intended to be actual performance and should not be relied upon as an indication of actual or future performance.

Data and graphical information herein are for information only and may have been derived from third party sources. Unigestion takes reasonable steps to verify, but does not guarantee, the accuracy and completeness of this information. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. All information provided here is subject to change without notice. It should only be considered current as of the date of publication without regard to the date on which you may access the information. Rates of exchange may cause the value of investments to go up or down. An investment with Unigestion, like all investments, contains risks, including total loss for the investor.

Uni-Global – Cross Asset Navigator is a compartment of the Luxembourg Uni-Global SICAV Part I, UCITS IV compliant. This compartment is currently authorised for distribution in Austria, Belgium, Denmark, Finland, France, Germany, Ireland, Italy, Luxembourg, Netherlands, Norway, Spain, UK, Sweden, and Switzerland. In Italy, this compartment can be offered only to qualified investors within the meaning of art.100 D. Leg. 58/1998. Its shares may not be offered or distributed in any country where such offer or distribution would be prohibited by law.

No prospectus has been filed with a Canadian securities regulatory authority to qualify the distribution of units of these funds and no such authority has expressed an opinion about these securities. Accordingly, their units may not be offered or distributed in Canada except to permitted clients who benefit from an exemption from the requirement to deliver a prospectus under securities legislation and where such offer or distribution would be prohibited by law. All investors must obtain and carefully read the applicable offering memorandum which contains additional information needed to evaluate the potential investment and provides important disclosures regarding risks, fees and expenses.

All investors must obtain and carefully read the prospectus which contains additional information needed to evaluate the potential investment and provides important disclosures regarding risks, fees and expenses. Unless otherwise stated performance is shown net of fees in USD and does not include the commission and fees charged at the time of subscribing for or redeeming shares.

Unigestion UK, which is authorised and regulated by the UK Financial Conduct Authority, has issued this document. Unigestion SA authorised and regulated by the Swiss FINMA. Unigestion Asset Management (France) S.A. authorised and regulated by the French Autorité des Marchés Financiers. Unigestion Asia Pte Limited authorised and regulated by the Monetary Authority of Singapore. Performance source: Unigestion, Bloomberg, Morningstar. Performance is shown on an annualised basis unless otherwise stated and is based on Uni Global – Cross Asset Navigator RA-USD net of fees with data from 15 December 2014 to 19 August 2019.