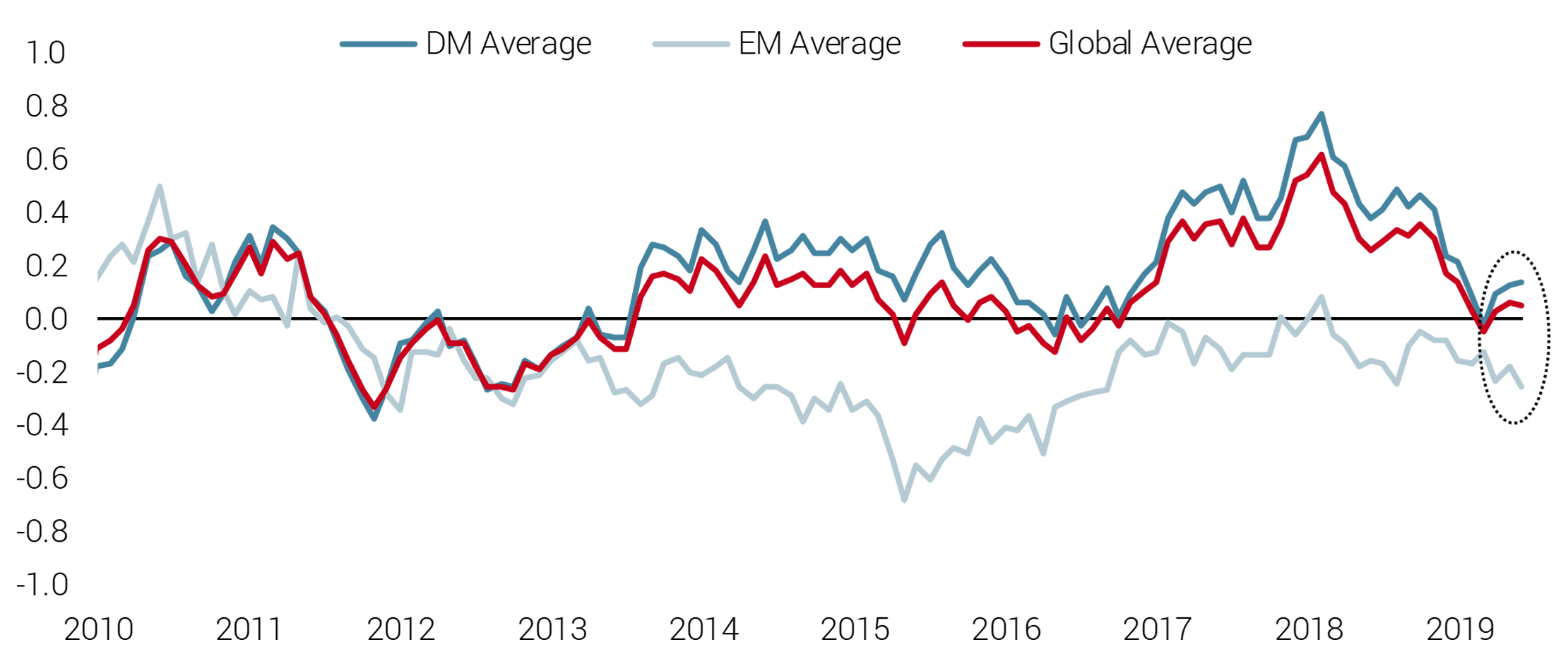

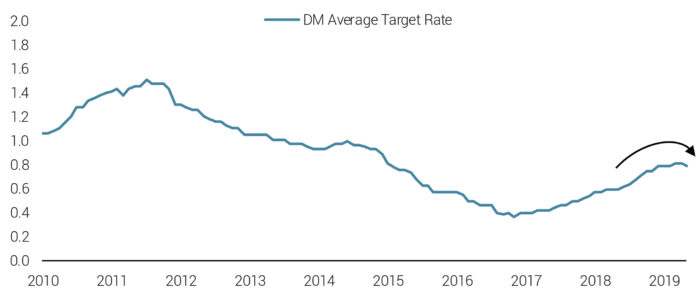

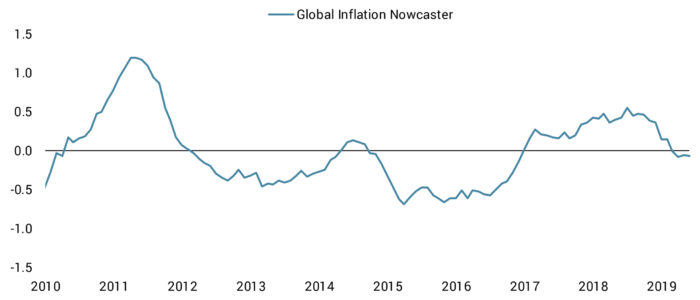

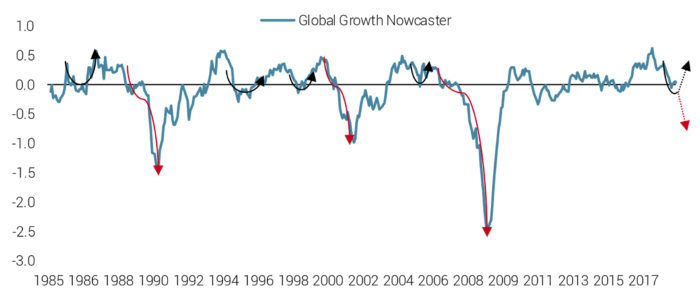

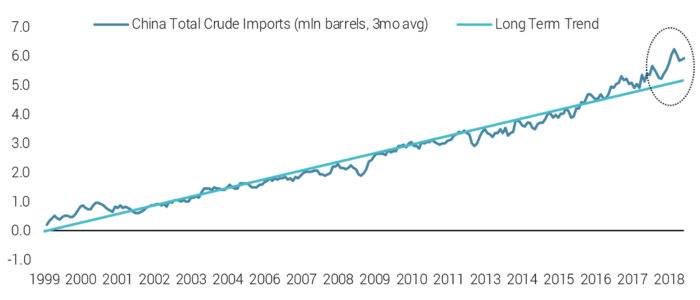

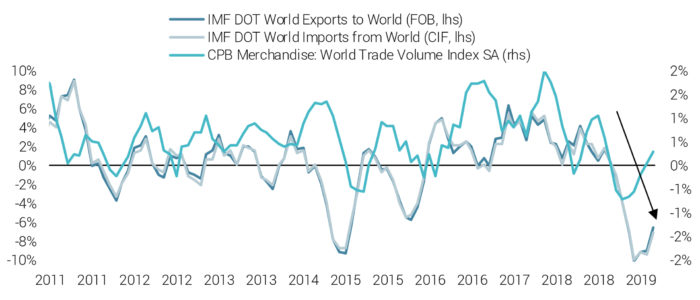

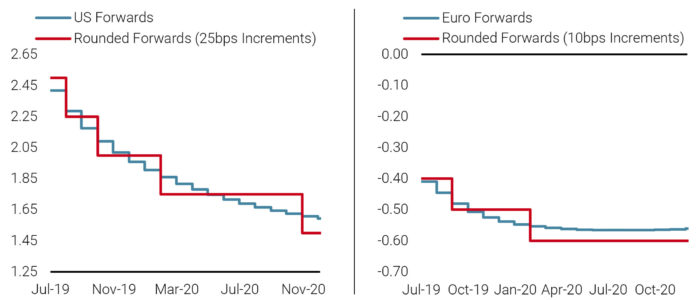

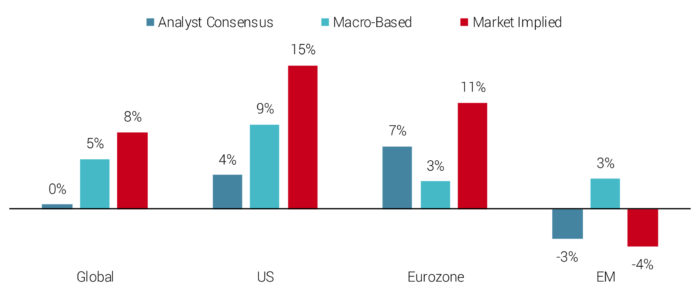

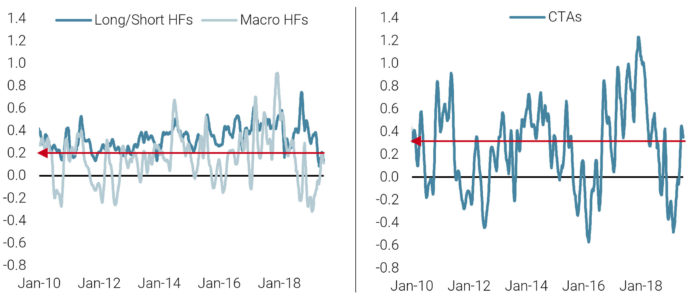

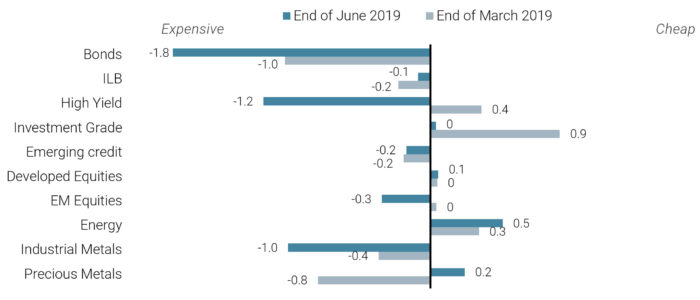

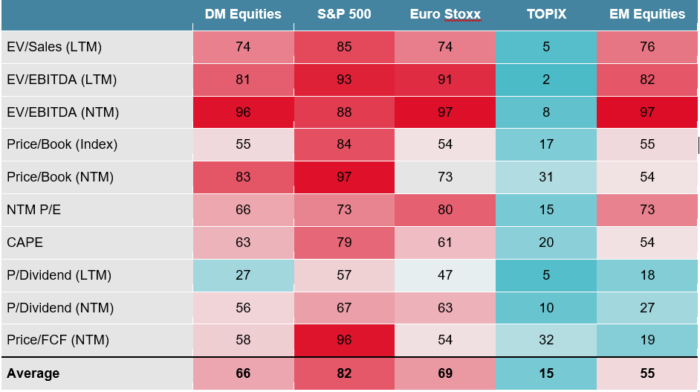

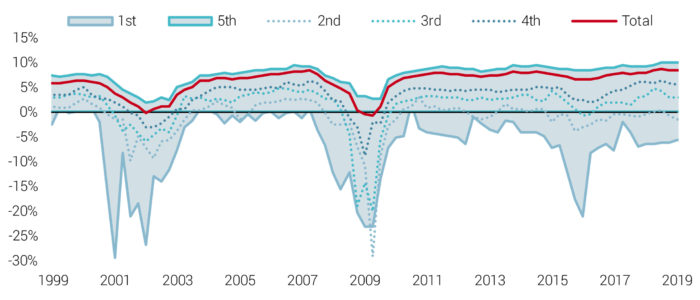

Risk is multidimensional and managing it effectively demands diversification of perspectives and metrics, as well as return sources. We believe there are three key drivers of risk for multi-asset investment portfolios: macroeconomic conditions, market sentiment, and asset valuation. Viewing global financial markets through this framework, we observe that some of the most concerning risks around macroeconomic slowdown have abated. Conditions have stabilised over the last few months and central banks have made it clear that they are ready to step in with their full suite of tools if needed. Nonetheless, geopolitical uncertainty, especially around US-China trade relations, are reminders that investors should remain alert and not be lulled into complacency in light of the recent market rally. Indeed, from a cross-asset valuation perspective, there are few obvious opportunities and traditional hedges like sovereign bonds are very expensive. Nonetheless, with few signs of imminent recession, muted inflation pressures, and accommodative monetary policy, the global expansion looks likely to continue, to the benefit of risky assets. One of our major themes of the last 12 to 18 months has been the slowdown in global economic growth. This perspective was based mainly on our proprietary set of economic indicators that assess in real-time the current risk of recession across more than 80% of the world’s GDP. These “Growth Nowcasters” aggregate and analyse more than 600 economic data series across 21 economies in both the developed and emerging world. Chart 1 shows the evolution of the Growth Nowcasters at a global level, as well as broken down by developed and emerging markets (DM and EM, respectively). After peaking in early 2018, global growth saw a sustained downward trend, hitting the zero level in March of this year. This indicated that the global economy had decelerated significantly and was growing around its potential. A continuation of this trend would have been quite concerning, as it would suggest the economy was tipping toward recession. However, since that low point in March, the global economy has shown signs of stabilisation around this potential level, not further deterioration, as highlighted by the circle region. While it is still too early to say the economy has bounced back and will likely re-accelerate into 2019, we can say that the likelihood of a global recession is much less probable than it seemed just a few months back. Chart 1: Growth Nowcasters Across Regions Source: Bloomberg, Unigestion (as of 28 June 2019). Importantly, this chart highlights the divergent growth dynamic between DM and EM economies: while DM economies broadly saw a strong resurgence of growth starting in early 2017 that has now fallen back to potential, growth in the EM world has been stagnant at just under potential over the same period. The developed world has central banks, led by the Federal Reserve (Fed) in the US, to thank for stemming the economic deceleration. After spending 2017 and 2018 tightening monetary policy, central banks pivoted in early 2019 to a more accommodative stance. As Chart 2 demonstrates, this shift in tone is now becoming evident in policy actions, with a levelling off and even a slight reduction in the average target rate across developed central banks. In mid-June, President of the European Central Bank (ECB) Mario Draghi made it clear that further interest rate cuts were available to policymakers if needed. This time last year, the ECB was talking about a possible rate hike toward the end of 2019. And following Draghi’s comments, the Fed made clear at their June meeting that the US tightening cycle is over and they are ready to cut interest rates to support the economy. Chart 2: Developed Central Bank Target Rates Reflect a More Accommodative Policy Stance Source: Bloomberg, Unigestion (as of 28 June 2019). Of course, a key reason that central banks can afford to make this shift is that inflation pressures have retreated significantly along with the growth deceleration. Chart 3 shows our global Inflation Nowcaster, which assesses the risk of inflation surprising to the upside or downside. In line with the stabilisation in the Growth Nowcaster, over the last couple of months our Inflation Nowcaster has stabilised around zero. This level indicates that inflationary and deflationary pressures are broadly offsetting each other, allowing central bankers to focus less on keeping prices stable and more on supporting the economic expansion. Chart 3: Developed Central Bank Target Rates Reflect a More Accommodative Policy Stance Source: Bloomberg, Unigestion (as of 28 June 2019). To be clear, the economy rarely stays at these potential levels for long. Looking over the last 35 years, we can see that in four cases (’97, ’95, ’99, ’05) the economy re-accelerated after decelerating to potential, while in three cases (’90, ’00, ’07), it fell into recession (see Chart 4). Monitoring the evolution of the economy from here in real-time will be critical in assessing which trajectory we are likely to be on in the months and years ahead. However, this economic stabilisation and a synchronised turn toward accommodative monetary policy should provide macro support to risky assets in the near-term. Chart 4: Historically, Growth at Potential is Not a Steady State for the Economy Source: Bloomberg, Unigestion (as of 28 June 2019). While the macro context is no longer a drag, fragile market sentiment is concerning and points us toward ensuring downside protection on our growth-oriented asset positions. The fragility is largely due to ongoing trade tensions between the US and its major trading partners, especially China. On the back of indications that a US-China trade deal was imminent, equity markets rallied strongly during the year with the S&P 500 hitting a new high of 2945 at the end of April. Alas, it seems that the more deeply entrenched differences were not fully addressed during the negotiations and these resurfaced to derail the agreement. These issues are at the core of the dispute: the role of state-owned enterprises (SOEs) in China’s economy, enforcement mechanisms to ensure compliance, and insistence by both sides on a fair deal (in their eyes) and respect. Until these thorny issues are addressed, tensions will persist and continue to roil markets. Interestingly, despite clear signs of slowing demand and restrictions on US crude oil imports, China has been accelerating its total oil imports, suggesting they may be stockpiling reserves and preparing themselves for a protracted conflict (see Chart 5). Chinese President Xi Jinping’s call for his country to prepare for a new “long march” further suggests that Chinese leaders do not see a resolution in the near term. The US is also sending a clear signal that they have other tools at their disposal in addition to tariffs, such as sanctions and export controls, and are willing to use trade to achieve other policy objectives (e.g., immigration). Chart 5: China Has Accelerated Crude Imports Source: Bloomberg, Unigestion (as of 28 June 2019). In the meantime, the impacts of the trade war are now evident in data. Until recently, soft data such as surveys and spending projections had shown the drag of trade tensions on sentiment. But over the last few months, hard data on world trade has sharply declined. Chart 6 shows the average three-month change for a few different measures of trade (import and export data from the IMF as well as trade volume data from the CBP), demonstrating the contraction in global trade over the last few months. This risk to external conditions is at the forefront many central bankers’ minds, justifying to a degree their policy stance. On a positive note, the CPB data is showing early signs of trade expansion again. Chart 6: Global Trade Has Contracted since the Third Quarter of 2018 Source: Bloomberg, Unigestion (as of 28 June 2019). While investors have been closely watching for any signals on US-China trade negotiations, other geopolitical risks have festered. In the UK, Boris Johnson has taken a commanding lead to replace Theresa May as Prime Minister. Johnson has made it clear that he aims to take the UK out of the European Union by October 31st, even if that means a ‘no-deal’ Brexit. While he may backtrack on that pledge and push back the deadline, the risk of a no-deal Brexit has risen significantly. In the Middle East, tensions between Iran and the US are boiling up as Iran threatens to breach the limit on the low-enriched uranium (used for nuclear power plants) it can stockpile under the 2015 deal. In response to this threat, as well as the attacks on oil tankers for which the US blames Iran, more US troops have been deployed to the region. While our core scenario for risky assets is supportive, sources of uncertainty such as these point us toward some cautiousness as we endeavour to provide smooth, consistent returns for our clients. In additional to geopolitics, two key dimensions of risk to assess market sentiment are pricing and investor positioning. Regarding pricing, money markets have priced in significant cuts in target interest rates, as Chart 7 shows for the Fed and the ECB. In the US, three cuts are expected by early 2020 and four by the end of the year. In the Eurozone, markets are expecting a more cautious ECB to cut rates this fall and again in late 2019 or early 2020. With the Eurozone hovering just above recessionary levels and uncertainty on tariffs and trade restrictions hanging over the region, one to two cuts seems reasonable to us. On the other hand, the pricing of 75bps in cuts in just over six months in the US looks stretched. At this point, the macro data is simply not supportive of such an aggressive policy shift. Rather, the uncertainty generated by the trade war is pushing the Fed’s hands to help smooth the economic impacts of this uncertainty. Thus, it seems to us that cuts from the Fed would be insurance cuts, which could be reversed if the uncertainty passes (the 1995 mid-cycle easing is the prototypical example). Until we see a significant deterioration in the US macro picture, it seems unlikely to us the Fed would pre-emptively cut rates to head off a potential recession. Indeed, if the Fed were to follow through with market expectations, we would be quite concerned about what sort of state the US economy would be in at that point. Chart 7: Market Pricing Aggressive Easing Cycle, Especially in the US Bloomberg, Unigestion (as of 28 June 2019). Equity markets, which have been buoyed by the central bank pivot, are pricing in significant earnings growth for the developed world, as shown in Chart 8. These expectations are at odds with the analyst consensus and our macro-based estimate, both of which see broadly muted earnings growth (mid-single digits). Interestingly, there is closer agreement between analysts, our estimates, and market pricing for EM equities, which are expected to see stable to slightly negative earnings growth over the next year. This suggests that if there were a resurgence of growth in the emerging world, driven possibly by further easing measures in China, a more accommodative Fed, or a trade deal, EM equities would strongly benefit as markets readjust their expectations to earnings expansion. Chart 8: Divergent Pricing in Developed Equity Markets but Agreement on EM Source: Bloomberg, Unigestion (as of 28 June 2019). A supportive sentiment factor is investor positioning, which remains relatively light despite a strong market rally. Chart 9 examines the implied beta to equities for a few key investor types as a proxy for their positioning. From this, we can see that Equity Long/Short Hedge Funds (HF) are at the lower end of their exposure to equities since 2010, while Macro HFs are relatively neutral. Commodity Trading Advisors (CTAs), which generally employ systematic trend-following strategies, have been active in increasing their equity exposure since the beginning of the year as markets rallied, but they remain far from overly-exposed at this point and seem to have room for additional buying if markets rise further. Chart 9: Implied Equity Betas Suggest Positioning is Light Source: Bloomberg, Unigestion (as of 28 June 2019). Finally, investment portfolios are exposed to valuation risk: “expensive” assets should underperform “cheap” assets, all else being equal. Our preferred measure to assess valuation across assets is carry, i.e., the return an asset holder receives if prices evolve in line with market expectations. By examining carry across assets, both with respect to each other and to their own histories, we can see that valuations right now are quite mixed, as shown in Chart 10. Bonds have continued to get even more expensive as yield curves flatten, while high yield credit and industrial metals are also looking rich. Most other growth-oriented assets, such as global equities, investment grade and EM credit, and energy commodities have fairly neutral valuations by this metric. Chart 10: Unigestion CAS’s Cross-Asset Valuation Indicator Source: Bloomberg, Unigestion (as of 28 June 2019) Looking closer at global equities via standard valuation measures, we see that, at the aggregate level, neither DM nor EM equities are particularly over-valued (Chart 11). Though some metrics are high, such as forward-looking Enterprise Value (EV) to Earnings Before Interest/Taxes/Depreciation/Amortisation (EBITDA), on average the metrics show these markets to be hovering a tad above their long-term levels. The case of the S&P 500 is more concerning, as nearly all valuation metrics are significantly elevated. Whether you consider the underlying assets, earnings, dividends, or cash flows you get for the price you pay for US stocks, you are getting much less today than you would have historically. On the other end of the spectrum, stocks in Japan’s TOPIX index are cheap by any measure we monitor, reflecting uncertainty around the planned consumption tax, trade tensions with the US, pressure on firms’ top-line due to the global economic slowdown, and tight labour markets squeezing margins. Chart 11: Unigestion CAS’s Cross-Asset Valuation Indicator Reading note: NTM denotes next twelve months, while LTM denotes last twelve months. CAPE is the cyclically adjusted P/E ratio. Source: Bloomberg, Unigestion (as of 28 June 2019) One justification for the high valuations of US firms is their strong profitability, especially after margins recovered in 2010 and then re-accelerated in 2016 to new highs. If we dig underneath the surface however, we see that there is strong dispersion between small, mid, and large-cap stocks. Chart 12 depicts the range of profit margins for firms in the Russell 3000 aggregated by market cap quintile (1st quintile are the smallest firms, 5th quintile are the largest firms), along with the total aggregate profit margin. Historically, it is not surprising to see the aggregate total close to the largest firms. However, what is interesting is how the spread, i.e., the range of margins between the smallest and largest firms, has grown since 2010 (shaded region of the chart). Typically, this band has remained narrow (around 10%) outside of recessions, when the spread widens significantly as small firms come under pressure and see their margins turn negative while large firms are able to ride out the storm. However, in the post-financial crisis recovery, the spread has widened. Indeed, 60% of firms currently have margins of 5% or below. Looking at balance sheets raises additional causes for concern: While we do not see this divergent corporate picture as an imminent risk since growth remains strong and monetary policy is easing, we are worried that when the cycle turns, this hidden dispersion will surface and reinforce the sell-off. Chart 12: The Spread of Profit Margins across US Firms Has Expanded Since 2010 Source: Bloomberg, Unigestion (as of 28 June 2019) For most of this year, we have maintained a cautious stance for a few key reasons: the pace and breadth of the macro deceleration, our doubts around the likelihood of a US-China trade deal, and the closing of the valuation gap that helped drive up markets at the beginning of the year. Taking a look where we are today, we believe the case for risky assets, or broad beta, is strong: the global economy is expanding in aggregate at around potential with little risk of an inflation overshoot and central banks ready to step in if (or even before) needed. Akin to the ‘goldilocks’ period of 2017 (though importantly at lower growth levels), the context should benefit equities, credit, and sovereign nominal bonds. Nonetheless, the skies are not completely clear and geopolitical uncertainty remains a primary source of risk. Market pricing and valuations are also not compelling, especially in bonds, the hedging asset of choice for most investors. Thus we continue to protect against an equity sell-off via options and make use of alternative return sources like low volatility equities and defensive FX strategies. Important Information This document is provided to you on a confidential basis and must not be distributed, published, reproduced or disclosed, in whole or part, The information and data presented in this document may discuss general market activity or industry trends but is not intended to be relied upon as a forecast, research or investment advice. It is not a financial promotion and represents no offer, solicitation or recommendation of any kind, The investment views, economic and market opinions or analysis expressed in this document present Unigestion’s judgement as at the date of publication without regard to the date on which you may access the information. There is no guarantee that these views and opinions expressed will be correct nor do they purport to be a complete description of the securities, markets and developments referred to in it. All information provided here is subject to change without notice. To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks. Data and graphical information herein are for information only and may have been derived from third party sources. Although we believe that the information obtained from public and third party sources to be reliable, we have not independently verified it and we therefore cannot guarantee its accuracy or completeness. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. Unless otherwise stated, source is Unigestion. Past performance is not a guide to future performance. All investments contain risks, including total loss for the investor. Unigestion SA is regulated by the Swiss Financial Market Supervisory Authority (FINMA). Unigestion (UK) Ltd is authorised and regulated by the Financial Conduct Authority (FCA) and SEC registered. Unigestion Asset Management (France) SA is regulated by the “Autorité des Marchés Financiers” (AMF). Unigestion (Luxembourg) SA is an Alternative Investment Fund Manager authorised by the Commission de Surveillance du Secteur Financier (CSSF) under the Luxembourg law of 12 July 2013 on AIFM. Unigestion Asset Management (Canada) Inc., with offices in Toronto and Montreal, is regulated in Canada by the securities regulatory authorities in Ontario, Quebec; Alberta, Manitoba, Saskatchewan, Nova Scotia, New Brunswick and British Columbia. Its principal regulator is the Ontario Securities Commission. Unigestion Asia Pte Ltd is regulated in Singapore by the MAS, as Capital Market Services (CMS) license holder and Exempt Financial Adviser under the Securities and Futures Act and Financial Advisers Act. Document issued: July 2019.MIVIEWS Q3 2019: AND THE BEAT GOES ON… FOR NOW

OVERVIEW

MACRO CONDITIONS ARE SHOWING SIGNS OF STABILISATION

GEOPOLITICAL TENSIONS CONTINUE TO WEIGH ON SENTIMENT

VALUATIONS PRESENT FEW OBVIOUS OPPORTUNITIES

WE ARE CONSTRUCTIVE BUT ATTENTIVE TO LATENT RISKS

to any other person.

to invest in the strategies or in the investment vehicles it refers to. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment.

Ihr Land:

Der Inhalt dieser Website wird von Unigestion SA veröffentlicht.

Bitte beachten Sie die nachstehenden RECHTLICHEN INFORMATIONEN zu den Nutzungsbedingungen der Website von Unigestion („Website”)

1. Zugriff auf die Website

Der Zugriff auf die Website ist Personen nicht gestattet, die (aufgrund ihres Wohnsitzes, ihrer Staatsangehörigkeit oder aus sonstigen Gründen) Rechtsgebieten unterstehen, in denen die Veröffentlichung oder Verfügbarkeit der Website einen Gesetzesverstoß darstellen würde. Insbesondere richtet sich die Website nicht an Einwohner der Vereinigten Staaten. Falls Sie einem solchen Rechtsgebiet unterstehen, sind Sie nicht befugt fortzufahren und werden aufgefordert, die Website unverzüglich zu verlassen. Falls Sie keinem derartigen Rechtsgebiet unterstehen, dürfen Sie nach der Lektüre und Annahme der nachstehenden Bedingungen auf die Website zugreifen.

2. Kein Angebot

Die auf der Website veröffentlichten Informationen stellen weder ein Angebot noch eine Empfehlung für die Durchführung oder die Liquidation einer Anlage noch für die Durchführung einer anderen Transaktion dar. Jede Anlageentscheidung muss auf der Basis einer Analyse der mit der Anlage verbundenen Risiken (einschließlich aller rechtlichen, aufsichtsrechtlichen, steuerlichen oder sonstigen Folgen) sowie einer geeigneten, diesbezüglichen Beratung durch einen unabhängigen Experten getroffen werden.

3. Keine Garantie

Die auf der Website veröffentlichten Informationen und Meinungen werden von Unigestion auf der Grundlage von öffentlichen Informationen, intern erstellten Daten sowie anderen, für zuverlässig gehaltenen Quellen bereitgestellt. Unigestion hat sich bemüht, dafür zu sorgen, dass diese Informationen zum Zeitpunkt ihrer Veröffentlichung möglichst zutreffend und vollständig sind. Dennoch kann diesbezüglich weder ausdrücklich noch stillschweigend eine Garantie abgegeben werden. Der Inhalt der Website kann jederzeit ohne vorherige Ankündigung geändert werden. Nur die aktuellen Fassungen des Verkaufsprospekts, der wesentlichen Informationen für den Anleger (KIID) sowie der Jahres- und Halbjahresberichte der Anlagefonds sind als offizielle Publikation der Fonds anzusehen und können als Grundlage für Anlageentscheidungen dienen.

4. Wertentwicklung und Risiken

Die in der Vergangenheit erzielte Wertentwicklung bietet keine Gewährleistung und keinen Hinweis auf künftige Ergebnisse. Der Wert der Anlagen kann Schwankungen nach oben und nach unten unterworfen sein. Wie alle Investments ist eine Anlage bei Unigestion mit Risiken verbunden, insbesondere dem Risiko, das investierte Kapital zu verlieren.

Die Risikofaktoren der auf dieser Website vorgestellten Finanzinstrumente sind im Verkaufsprospekt des Fonds beschrieben.

5. Rechtliche Einschränkungen auf lokaler Ebene und besondere Hinweise

Die Website ist nicht an Personen gerichtet, welche in einem Staat ansässig sind, in dem der Vertrieb der auf der Website vorgestellten Finanzprodukte gegen das Gesetz und/oder die örtlichen Bestimmungen verstoßen würde. Derartige Personen dürfen nicht auf diese Website zugreifen. Sie sind dafür verantwortlich, dafür zu sorgen, dass Sie zum Zugriff auf die Website berechtigt sind. Diese Website enthält Informationen über eine große Zahl an Finanzinstrumenten, die in unterschiedlichen Rechtsgebieten eingetragen sind und verwaltet werden. So werden Sie aufgefordert, Ihren Wohnort anzugeben, bevor Sie auf Informationen in Bezug auf die besagten Produkte zugreifen können. Bitte beachten Sie, dass der Zugriff von Privatanlegern auf die besagten Informationen auf die Finanzinstrumente beschränkt ist, die in dem Land seines Wohnsitzes für den Verkauf an Privatkunden zugelassen sind.

Vereinigte Staaten von Amerika

Keines der auf dieser Website erwähnten Finanzprodukte ist gemäß dem „United States Securities Act” von 1933 in seiner geänderten Fassung registriert und eine solche Registrierung ist auch nicht vorgesehen. Gleichermaßen sind die auf dieser Website genannten Anlagefonds nicht gemäß dem „United States Investment Company Act” von 1940 in seiner geänderten Fassung registriert und eine solche Registrierung ist auch nicht vorgesehen. Folglich dürfen die nachstehend genannten Anlagefonds keinesfalls (i) auf dem Staatsgebiet der Vereinigten Staaten von Amerika, in einem ihrer Bundesstaaten oder einer anderen politischen Untergliederung der Vereinigten Staaten (ii) an Staatsangehörige der Vereinigten Staaten (gemäß der Begriffsbestimmung in Regulation S des „United States Securities Act” von 1933), auf deren Rechnung oder zu deren Gunsten angeboten oder vertrieben werden.

Schweiz

Der Fondsvertrag, der Verkaufsprospekt, die wesentlichen Anlegerinformationen und die aktuellen Jahres- und Halbjahresberichte von Unigestion Swiss Equities sowie der Verkaufsprospekt, die wesentlichen Anlegerinformationen und die aktuellen Jahres- und Halbjahresberichte der Sicav Uni-Global sind auf Anfrage gebührenfrei bei der Fondsverwaltung, den Vertriebsstellen des Fonds oder der lokalen Vertretung (Unigestion SA, 8c Avenue de Champel, 1206 Genf) erhältlich.

Österreich

Der Verkaufsprospekt, die wesentlichen Anlegerinformationen, die Statuten sowie die aktuellen Jahres- und Halbjahresberichte der Sicav Uni-Global sind auf Anfrage gebührenfrei bei der Verwaltungsgesellschaft, den Vertriebsstellen des Fonds oder der lokalen Vertretung (Erste Bank der österreichischen Sparkassen AG, Brandstätte 7-9/1. Stock A-1010 Wien) erhältlich.

Vereinigtes Königreich

Als eines von der FCA kontrolliertes Unternehmen muss Unigestion (UK) Ltd über ein schriftlich festgehaltenes Verfahren zur effektiven Berücksichtigung und ordnungsgemässen Behandlung von Beschwerden und Interessenkonflikten verfügen. Die Richtlinien der Unigestion UK Limited zur Behandlung von Beschwerden und Interessenkonflikten sowie die zugehörigen Verfahren werden in den folgenden Dokumenten erläutert: Unigestion UK Complaints Policy and Unigestion UK Limited Conflicts of Interest Policy (auf Englisch).

Frankreich

Im Rahmen ihrer rechtlichen und aufsichtsrechtlichen Verpflichtungen hat Unigestion Asset Management (France) SA eine Politik für das Beschwerdemanagement eingerichtet.

Wenn Sie mehr über diese Politik erfahren möchten, verweisen wir Sie auf das Dokument Politik für das Beschwerdemanagement (auf Englisch).

Kanada

Die Unigestion Group operiert in Kanada über die Unigestion Asset Management (Canada) Inc. (UAMC). Diese ist in allen kanadischen Provinzen (mit Ausnahme von Neufundland und Labrador sowie Prince Edward Island) als Portfoliomanager und in den Provinzen Ontario und Quebec als Anlagefondsverwalter registriert. Die in diesem Dokument beschriebenen Leistungen und Produkte werden nur in Ländern und nur gegenüber Personen angeboten, bei denen dies gesetzlich zulässig ist.

Wenn Sie in Kanada domiziliert sind, bestätigen Sie durch den Zugriff auf diese Website insbesondere, dass Sie ein zugelassener Anleger sind oder zu den Anlegern gehören, für die gemäß dem Verkaufsprospekt Ausnahmeregelungen gelten.

6. Steuerliche Aspekte

Die steuerliche Behandlung hängt von der persönlichen Situation des einzelnen Anlegers ab und kann Änderungen unterworfen sein. Vor dem Treffen einer Anlageentscheidung wird jedem Anleger empfohlen, den speziellen Rat eines Branchenexperten einzuholen.

7. Geistiges Eigentum

Sofern nicht anderweitig angegeben, ist Unigestion Eigentümerin oder Rechtsinhaberin an allen Bestandteilen der Website, insbesondere den Daten, Grafiken und Abbildungen. Jegliche Vervielfältigung, Wiedergabe, Verteilung oder Weitergabe des Inhalts dieser Website mit Hilfe eines beliebigen Verfahrens ist ganz oder in Teilen ohne die ausdrückliche, vorherige Genehmigung von Unigestion untersagt.

8. Verlinkung auf andere Internetsites

Diese Website kann Verlinkungen zu anderen Internetsites enthalten. Das Aufrufen dieser Links erfolgt auf eigene Gefahr. Unigestion lehnt jegliche Verantwortung für den Inhalt und eventuelle Schäden ab, die durch den Besuch von Internetsites entstehen, auf die diese Website durch Verlinkungen verweist. Der Benutzer besucht die anderen Internetsites auf eigene Verantwortung und auf eigenes Risiko.

9. Cookies

Der Benutzer wird darauf hingewiesen, dass bei seinen Besuchen auf der Website automatisch ein Cookie installiert und vorübergehend in seinem Speicher oder auf seiner Festplatte hinterlegt werden kann. Ein Cookie ist eine Datei, die nicht die Identifikation des Benutzers ermöglicht, aber dazu dient, Informationen über dessen Navigationsverhalten auf der Internetsite zu erfassen.

Die Benutzer der Website bestätigen, dass sie über dieses Vorgehen informiert wurden und gestatten Unigestion dessen Anwendung. Sie können dieses Cookie mittels der in ihrer Navigationssoftware enthaltenen Funktionen deaktivieren.

Diese Website nutzt Google Analytics, einen Internetanalysedienst von Google, Inc. („Google“). Google Analytics verwendet „Cookies“. Dabei handelt es sich um Textdateien, die auf Ihrem Computer gespeichert werden, um auf einer Website das Verhalten von Besuchern analysieren zu können. Die von dem Cookie erzeugten Informationen über Ihr Nutzungsverhalten auf der Website (einschließlich Ihrer IP-Adresse) werden an Server in den USA übermittelt und dort von Google gespeichert. Google wird diese Informationen zur Bewertung Ihres Nutzungsverhaltens, zur Erstellung von Berichten für die Betreiber der Website über die Websiteaktivitäten und zur Erbringung sonstiger Dienstleistungen in Bezug auf die Websiteaktivitäten und Internetnutzung verwenden. Google kann diese Informationen auch an Dritte weiterleiten, falls dies gesetzlich erforderlich ist oder falls Dritte die Informationen im Auftrag von Google verarbeiten. Google wird Ihre IP-Adresse nicht mit anderen von Google gespeicherten Daten in Verbindung bringen. Sie können Cookies ablehnen, indem Sie die entsprechenden Einstellungen in Ihrem Browser wählen. Denken Sie jedoch daran, dass Ihnen in diesem Fall dann eventuell nicht die volle Funktionalität dieser Website zur Verfügung steht. Mit der Nutzung dieser Website stimmen Sie der Verarbeitung Ihrer Daten durch Google in der oben genannten Weise und zu den oben beschriebenen Zwecken zu.

Sie können verhindern, dass Google Daten (Cookies und IP-Adressen) erfasst und verwendet, indem Sie das unter https://tools.google.com/dlpage/gaoptout erhältliche Browser-Plugin herunterladen und installieren. Weitere Informationen zu den Nutzungsbedingungen und zum Datenschutz finden Sie unter: https://www.google.com/analytics/terms/gb.html.

10. Allgemeine Geschäftsbedingungen

Die Nutzer werden darüber informiert, dass persönliche Angaben, die sie an Unigestion SA weitergeben, zur Erbringung von Dienstleistungen verwendet werden, für welche sie sich angemeldet oder abonniert haben. Diese Daten werden nicht anderweitig verwendet. Um den Nutzern diese Dienste zur Verfügung zu stellen, können diese Daten mit Drittparteien, einschliesslich Tochterunternehmen und externen Dienstleistungsanbietern, welche Datenverarbeitungs-, Datenspeicherung-s, Marketing-, Statistik- oder Verwaltungsdienstleistungen innerhalb der Schweiz, den Mitgliedstaaten der Europäischen Union oder anderer ausländischer Jurisdiktionen anbieten. Die Daten können ebenfalls in Jurisdiktionen zur Verfügung gestellt werden, die möglicherweise nicht das gleiche Datenschutzniveau anbieten wie die Schweiz oder die Europäische Union, z. B. die Vereinigten Staaten, Kanada oder Singapur. Unigestion SA hat interne Datenschutzvorschriften auf hohem Niveau eingeführt, um die Übereinstimmung mit den geltenden Datenschutzgesetzen sicherzustellen und, in diesem Zusammenhang, einen angemessenen Schutz gewährleisten zu können.

Die Nutzer werden darüber informiert, dass sie ihre Einwilligung jederzeit widerrufen können, indem sie den Link zur ABMELDUNG für diese Dienstleistung nutzen oder eine E-Mail senden an: clients@unigestion.com.

Der Inhalt dieser Website wird von Unigestion SA veröffentlicht.

Bitte beachten Sie die nachstehenden RECHTLICHEN INFORMATIONEN zu den Nutzungsbedingungen der Website von Unigestion („Website”)

1. Zugriff auf die Website

Der Zugriff auf die Website ist Personen nicht gestattet, die (aufgrund ihres Wohnsitzes, ihrer Staatsangehörigkeit oder aus sonstigen Gründen) Rechtsgebieten unterstehen, in denen die Veröffentlichung oder Verfügbarkeit der Website einen Gesetzesverstoß darstellen würde. Insbesondere richtet sich die Website nicht an Einwohner der Vereinigten Staaten. Falls Sie einem solchen Rechtsgebiet unterstehen, sind Sie nicht befugt fortzufahren und werden aufgefordert, die Website unverzüglich zu verlassen. Falls Sie keinem derartigen Rechtsgebiet unterstehen, dürfen Sie nach der Lektüre und Annahme der nachstehenden Bedingungen auf die Website zugreifen.

2. Kein Angebot

Die auf der Website veröffentlichten Informationen stellen weder ein Angebot noch eine Empfehlung für die Durchführung oder die Liquidation einer Anlage noch für die Durchführung einer anderen Transaktion dar. Jede Anlageentscheidung muss auf der Basis einer Analyse der mit der Anlage verbundenen Risiken (einschließlich aller rechtlichen, aufsichtsrechtlichen, steuerlichen oder sonstigen Folgen) sowie einer geeigneten, diesbezüglichen Beratung durch einen unabhängigen Experten getroffen werden.

3. Keine Garantie

Die auf der Website veröffentlichten Informationen und Meinungen werden von Unigestion auf der Grundlage von öffentlichen Informationen, intern erstellten Daten sowie anderen, für zuverlässig gehaltenen Quellen bereitgestellt. Unigestion hat sich bemüht, dafür zu sorgen, dass diese Informationen zum Zeitpunkt ihrer Veröffentlichung möglichst zutreffend und vollständig sind. Dennoch kann diesbezüglich weder ausdrücklich noch stillschweigend eine Garantie abgegeben werden. Der Inhalt der Website kann jederzeit ohne vorherige Ankündigung geändert werden. Nur die aktuellen Fassungen des Verkaufsprospekts, der wesentlichen Informationen für den Anleger (KIID) sowie der Jahres- und Halbjahresberichte der Anlagefonds sind als offizielle Publikation der Fonds anzusehen und können als Grundlage für Anlageentscheidungen dienen.

4. Wertentwicklung und Risiken

Die in der Vergangenheit erzielte Wertentwicklung bietet keine Gewährleistung und keinen Hinweis auf künftige Ergebnisse. Der Wert der Anlagen kann Schwankungen nach oben und nach unten unterworfen sein. Wie alle Investments ist eine Anlage bei Unigestion mit Risiken verbunden, insbesondere dem Risiko, das investierte Kapital zu verlieren.

Die Risikofaktoren der auf dieser Website vorgestellten Finanzinstrumente sind im Verkaufsprospekt des Fonds beschrieben.

5. Rechtliche Einschränkungen auf lokaler Ebene und besondere Hinweise

Die Website ist nicht an Personen gerichtet, welche in einem Staat ansässig sind, in dem der Vertrieb der auf der Website vorgestellten Finanzprodukte gegen das Gesetz und/oder die örtlichen Bestimmungen verstoßen würde. Derartige Personen dürfen nicht auf diese Website zugreifen. Sie sind dafür verantwortlich, dafür zu sorgen, dass Sie zum Zugriff auf die Website berechtigt sind. Diese Website enthält Informationen über eine große Zahl an Finanzinstrumenten, die in unterschiedlichen Rechtsgebieten eingetragen sind und verwaltet werden. So werden Sie aufgefordert, Ihren Wohnort anzugeben, bevor Sie auf Informationen in Bezug auf die besagten Produkte zugreifen können. Bitte beachten Sie, dass der Zugriff von Privatanlegern auf die besagten Informationen auf die Finanzinstrumente beschränkt ist, die in dem Land seines Wohnsitzes für den Verkauf an Privatkunden zugelassen sind.

Vereinigte Staaten von Amerika

Keines der auf dieser Website erwähnten Finanzprodukte ist gemäß dem „United States Securities Act” von 1933 in seiner geänderten Fassung registriert und eine solche Registrierung ist auch nicht vorgesehen. Gleichermaßen sind die auf dieser Website genannten Anlagefonds nicht gemäß dem „United States Investment Company Act” von 1940 in seiner geänderten Fassung registriert und eine solche Registrierung ist auch nicht vorgesehen. Folglich dürfen die nachstehend genannten Anlagefonds keinesfalls (i) auf dem Staatsgebiet der Vereinigten Staaten von Amerika, in einem ihrer Bundesstaaten oder einer anderen politischen Untergliederung der Vereinigten Staaten (ii) an Staatsangehörige der Vereinigten Staaten (gemäß der Begriffsbestimmung in Regulation S des „United States Securities Act” von 1933), auf deren Rechnung oder zu deren Gunsten angeboten oder vertrieben werden.

Schweiz

Der Fondsvertrag, der Verkaufsprospekt, die wesentlichen Anlegerinformationen und die aktuellen Jahres- und Halbjahresberichte von Unigestion Swiss Equities sowie der Verkaufsprospekt, die wesentlichen Anlegerinformationen und die aktuellen Jahres- und Halbjahresberichte der Sicav Uni-Global sind auf Anfrage gebührenfrei bei der Fondsverwaltung, den Vertriebsstellen des Fonds oder der lokalen Vertretung (Unigestion SA, 8c Avenue de Champel, 1206 Genf) erhältlich.

Österreich

Der Verkaufsprospekt, die wesentlichen Anlegerinformationen, die Statuten sowie die aktuellen Jahres- und Halbjahresberichte der Sicav Uni-Global sind auf Anfrage gebührenfrei bei der Verwaltungsgesellschaft, den Vertriebsstellen des Fonds oder der lokalen Vertretung (Erste Bank der österreichischen Sparkassen AG, Brandstätte 7-9/1. Stock A-1010 Wien) erhältlich.

Vereinigtes Königreich

Als eines von der FCA kontrolliertes Unternehmen muss Unigestion (UK) Ltd über ein schriftlich festgehaltenes Verfahren zur effektiven Berücksichtigung und ordnungsgemässen Behandlung von Beschwerden und Interessenkonflikten verfügen. Die Richtlinien der Unigestion UK Limited zur Behandlung von Beschwerden und Interessenkonflikten sowie die zugehörigen Verfahren werden in den folgenden Dokumenten erläutert: Unigestion UK Complaints Policy and Unigestion UK Limited Conflicts of Interest Policy (auf Englisch).

Frankreich

Im Rahmen ihrer rechtlichen und aufsichtsrechtlichen Verpflichtungen hat Unigestion Asset Management (France) SA eine Politik für das Beschwerdemanagement eingerichtet.

Wenn Sie mehr über diese Politik erfahren möchten, verweisen wir Sie auf das Dokument Politik für das Beschwerdemanagement (auf Englisch).

Kanada

Die Unigestion Group operiert in Kanada über die Unigestion Asset Management (Canada) Inc. (UAMC). Diese ist in allen kanadischen Provinzen (mit Ausnahme von Neufundland und Labrador sowie Prince Edward Island) als Portfoliomanager und in den Provinzen Ontario und Quebec als Anlagefondsverwalter registriert. Die in diesem Dokument beschriebenen Leistungen und Produkte werden nur in Ländern und nur gegenüber Personen angeboten, bei denen dies gesetzlich zulässig ist.

Wenn Sie in Kanada domiziliert sind, bestätigen Sie durch den Zugriff auf diese Website insbesondere, dass Sie ein zugelassener Anleger sind oder zu den Anlegern gehören, für die gemäß dem Verkaufsprospekt Ausnahmeregelungen gelten.

6. Steuerliche Aspekte

Die steuerliche Behandlung hängt von der persönlichen Situation des einzelnen Anlegers ab und kann Änderungen unterworfen sein. Vor dem Treffen einer Anlageentscheidung wird jedem Anleger empfohlen, den speziellen Rat eines Branchenexperten einzuholen.

7. Geistiges Eigentum

Sofern nicht anderweitig angegeben, ist Unigestion Eigentümerin oder Rechtsinhaberin an allen Bestandteilen der Website, insbesondere den Daten, Grafiken und Abbildungen. Jegliche Vervielfältigung, Wiedergabe, Verteilung oder Weitergabe des Inhalts dieser Website mit Hilfe eines beliebigen Verfahrens ist ganz oder in Teilen ohne die ausdrückliche, vorherige Genehmigung von Unigestion untersagt.

8. Verlinkung auf andere Internetsites

Diese Website kann Verlinkungen zu anderen Internetsites enthalten. Das Aufrufen dieser Links erfolgt auf eigene Gefahr. Unigestion lehnt jegliche Verantwortung für den Inhalt und eventuelle Schäden ab, die durch den Besuch von Internetsites entstehen, auf die diese Website durch Verlinkungen verweist. Der Benutzer besucht die anderen Internetsites auf eigene Verantwortung und auf eigenes Risiko.

9. Cookies

Der Benutzer wird darauf hingewiesen, dass bei seinen Besuchen auf der Website automatisch ein Cookie installiert und vorübergehend in seinem Speicher oder auf seiner Festplatte hinterlegt werden kann. Ein Cookie ist eine Datei, die nicht die Identifikation des Benutzers ermöglicht, aber dazu dient, Informationen über dessen Navigationsverhalten auf der Internetsite zu erfassen.

Die Benutzer der Website bestätigen, dass sie über dieses Vorgehen informiert wurden und gestatten Unigestion dessen Anwendung. Sie können dieses Cookie mittels der in ihrer Navigationssoftware enthaltenen Funktionen deaktivieren.

Diese Website nutzt Google Analytics, einen Internetanalysedienst von Google, Inc. („Google“). Google Analytics verwendet „Cookies“. Dabei handelt es sich um Textdateien, die auf Ihrem Computer gespeichert werden, um auf einer Website das Verhalten von Besuchern analysieren zu können. Die von dem Cookie erzeugten Informationen über Ihr Nutzungsverhalten auf der Website (einschließlich Ihrer IP-Adresse) werden an Server in den USA übermittelt und dort von Google gespeichert. Google wird diese Informationen zur Bewertung Ihres Nutzungsverhaltens, zur Erstellung von Berichten für die Betreiber der Website über die Websiteaktivitäten und zur Erbringung sonstiger Dienstleistungen in Bezug auf die Websiteaktivitäten und Internetnutzung verwenden. Google kann diese Informationen auch an Dritte weiterleiten, falls dies gesetzlich erforderlich ist oder falls Dritte die Informationen im Auftrag von Google verarbeiten. Google wird Ihre IP-Adresse nicht mit anderen von Google gespeicherten Daten in Verbindung bringen. Sie können Cookies ablehnen, indem Sie die entsprechenden Einstellungen in Ihrem Browser wählen. Denken Sie jedoch daran, dass Ihnen in diesem Fall dann eventuell nicht die volle Funktionalität dieser Website zur Verfügung steht. Mit der Nutzung dieser Website stimmen Sie der Verarbeitung Ihrer Daten durch Google in der oben genannten Weise und zu den oben beschriebenen Zwecken zu.

Sie können verhindern, dass Google Daten (Cookies und IP-Adressen) erfasst und verwendet, indem Sie das unter https://tools.google.com/dlpage/gaoptout erhältliche Browser-Plugin herunterladen und installieren. Weitere Informationen zu den Nutzungsbedingungen und zum Datenschutz finden Sie unter: https://www.google.com/analytics/terms/gb.html.

10. Allgemeine Geschäftsbedingungen

Die Nutzer werden darüber informiert, dass persönliche Angaben, die sie an Unigestion SA weitergeben, zur Erbringung von Dienstleistungen verwendet werden, für welche sie sich angemeldet oder abonniert haben. Diese Daten werden nicht anderweitig verwendet. Um den Nutzern diese Dienste zur Verfügung zu stellen, können diese Daten mit Drittparteien, einschliesslich Tochterunternehmen und externen Dienstleistungsanbietern, welche Datenverarbeitungs-, Datenspeicherung-s, Marketing-, Statistik- oder Verwaltungsdienstleistungen innerhalb der Schweiz, den Mitgliedstaaten der Europäischen Union oder anderer ausländischer Jurisdiktionen anbieten. Die Daten können ebenfalls in Jurisdiktionen zur Verfügung gestellt werden, die möglicherweise nicht das gleiche Datenschutzniveau anbieten wie die Schweiz oder die Europäische Union, z. B. die Vereinigten Staaten, Kanada oder Singapur. Unigestion SA hat interne Datenschutzvorschriften auf hohem Niveau eingeführt, um die Übereinstimmung mit den geltenden Datenschutzgesetzen sicherzustellen und, in diesem Zusammenhang, einen angemessenen Schutz gewährleisten zu können.

Die Nutzer werden darüber informiert, dass sie ihre Einwilligung jederzeit widerrufen können, indem sie den Link zur ABMELDUNG für diese Dienstleistung nutzen oder eine E-Mail senden an: clients@unigestion.com.