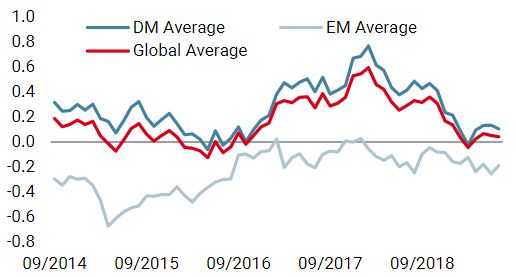

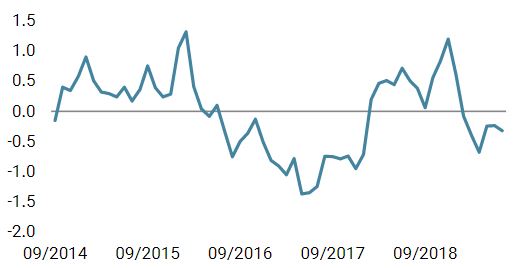

Corporate earnings season for the second quarter of 2019 has begun and will kick into high gear over the next two weeks. Following a significant turn in monetary policy and continuing geopolitical risks such as a trade war and tensions with Iran, investors seem to have a fairly subdued assessment of earnings results. The mood has changed notably since the 3Q 2018 earnings season, when aggregate earnings-per-share (EPS) growth for firms in the S&P 500 was 27% year-on-year, beating lofty expectations. Despite the current dour mood, with Q2 2019 EPS growth for US firms expected to decline by 2% compared to a year ago, this earnings season is an important one to follow, and we are closely monitoring this moment of truth for an indication of the likely direction ahead for the economy and asset returns. As investors know, the global economy has slowed significantly from its highs in early 2018. By our measures, growth hit potential levels in the early part of this year and over the last few months has shown signs of stabilisation. However, any coincident measure of economic activity is imperfect, and the earnings season provides an additional point of triangulation to confirm how deep the slowdown has been and its future direction. Looking at sales growth, we see a clear peak for US and Eurozone firms in mid-2018. Since that time, sales growth has slowed for S&P 500 companies toward the post-2009 average of 5%, while sales for firms in the Euro Stoxx 50 have fallen from their 2017-2018 levels. Given this context, a key question is to what extent the stabilisation in growth has helped to support corporate sales growth. For much of 2018, firms in the US and, to a lesser extent, Europe had been able to combat slowing sales growth with margin expansion. But margins are showing signs of flattening in the US and contraction in Europe as many of the tailwinds that had supported margin growth – globalisation, consolidation, moderate wage pressures, and lower taxes to name a few – are fading. The logical result is that firms’ bottom lines have been under pressure, and earnings growth has declined meaningfully. Firms in the S&P 500 are now seeing EPS expand by about 7% in aggregate, whereas EPS for firms in the Euro Stoxx 50 is contracting. Will this trend continue, or will we see a stabilisation and perhaps a modest recovery in earnings growth?„MOMENT OF TRUTH“ – Earth, Wind & Fire, 1971

What’s Next?

Corporate profitability reveals much about the economy

Declining profitability is a useful presage of oncoming recession: as firms contend with lower income and pressures on their free cash, they typically cut back spending and hiring. These cutbacks, in turn, negatively impact other businesses, whose sales take the hit, and households, who lose their jobs or see their take-home pay reduced. And the cycle continues, with sales and profitability falling further, causing the slowdown to deepen and transform into a recession. Indeed, declining profitability preceded nearly every US recession. To be clear, we do not believe we are at this point now, but we will be tracking this earnings season closely to see how resilient profits have been in the face of the economic slowdown thus far.

Importantly, the reporting season should also give a clearer picture into how tariffs and the trade war more broadly are impacting corporates. We have seen the impact of trade tensions on global trade, but so far it seems much of the increase in imported goods’ prices has been absorbed by margins (see “You Spin Me Round”, 28 May 2019). Can firms continue to bear these costs, and how are they adapting their investment plans given the uncertainty they face? These and other second-round impacts of tariffs and trade tensions are very difficult to quantify, but we should get a better sense when firms hold earnings calls over the next couple of weeks.

There is a lagged affect in financial markets to a turn in earnings growth. Typically, equities continue to rally higher as investors extrapolate the recent past forward. And even though earnings growth moderates, it remains strong, supporting valuations and the case for a long equities bias. Corporate credit also reaps these benefits with attractive yields relative to sovereign bonds and de minimis probability of default given strong earnings. Once the turn in earnings growth becomes clearer and its decline becomes more entrenched, investors reprice their expectations for future earnings growth, typically from much too optimistic levels to much too pessimistic. They reduce the growth bias of their portfolios and increase their allocation to defensive sectors and hedging assets, such as sovereign nominal bonds that have typically underperformed equities and credit and now offer relatively attractive yields (though in the current context, nominal yields are already quite low). This shift aligns yields closer to the “Fed model,” narrows the relative performance gap between equities/credit and bonds, and eventually reverses it months after the turn in earnings growth. Clearly, easier monetary policy can stimulate demand and ease financing costs, supporting earnings growth and outperformance of growth assets, but lower yields are not always a panacea for a deteriorating operating environment. Thus, declining earnings growth has an important bearing on the relative performance of equities and credit versus nominal bonds. Credit tends to have a longer lag than equities since earnings growth needs to decline sufficiently to cause investors to reassess their assessment of firms’ probability of default. But historically this relationship takes between six to twelve months to transpire. As EPS growth in the US peaked in late 2018 and valuations there are high, the forward guidance will be important. If it is poor, then a quick recovery in earnings becomes less likely, as does the prospect of a continuation in the outperformance of equities/credit since the beginning of the year. And if the negative guidance extends beyond export-focused firms to the broader universe, concerns about trade contagion and a deeper slowdown will grow. We do not believe these risks are sufficient to adapt the portfolio to a more defensive posture, but it does motivate our relatively light overweight in equities and more positive view on credit.Pay close attention to forward guidance

Moment of Truth by Earth

Our medium-term views remain cautious, and we prefer to get exposure to growth via high yield corporate credit. We are also complementing our modest equity exposure with options to protect the portfolio in the case of equity drawdowns. Over the month of July thus far, the Uni-Global – Cross Asset Navigator fund is up 0.8% versus 0.8% for the MSCI AC World Index and 0.4% for the Barclays Global Aggregate (USD hedged). Year-to-date, the Uni-Global – Cross Asset Navigator has returned 8.0% versus 17.1% for the MSCI AC World index, while the Barclays Global Aggregate (USD hedged) index is up 6.4%.Strategy Behaviour

Performance Review

Unigestion Nowcasting

World Growth Nowcaster

World Inflation Nowcaster

Market Stress Nowcaster

Weekly Change

- Our world Growth Nowcaster remained unchanged this week, as an improvement in India was offset by broad weakness elsewhere, particularly Brazil.

- Our world Inflation Nowcaster decreased further this week, mainly driven by continued disinflationary prospects in the US.

- Market stress picked up modestly this week, as tighter liquidity conditions pushed up our indicator.

Sources: Unigestion. Bloomberg, as of 19 July 2019.

Past performance is no guide to the future, the value of investments can fall as well as rise, there is no guarantee that your initial investment will be returned. Important Information Past performance is no guide to the future, the value of investments, and the income from them change frequently, may fall as well as rise, there is no guarantee that your initial investment will be returned. This document has been prepared for your information only and must not be distributed, published, reproduced or disclosed by recipients to any other person. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. This is a promotional statement of our investment philosophy and services only in relation to the subject matter of this presentation. It constitutes neither investment advice nor recommendation. This document represents no offer, solicitation or suggestion of suitability to subscribe in the investment vehicles to which it refers. Any such offer to sell or solicitation of an offer to purchase shall be made only by formal offering documents, which include, among others, a confidential offering memorandum, limited partnership agreement (if applicable), investment management agreement (if applicable), operating agreement (if applicable), and related subscription documents (if applicable). Please contact your professional adviser/consultant before making an investment decision. Where possible we aim to disclose the material risks pertinent to this document, and as such these should be noted on the individual document pages. The views expressed in this document do not purport to be a complete description of the securities, markets and developments referred to in it. Reference to specific securities should not be considered a recommendation to buy or sell. Investors shall conduct their own analysis of the risks (including any legal, regulatory, tax or other consequences) associated with an investment and should seek independent professional advice. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment. These are not suitable for all types of investors. To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks. Actual results could differ materially from those in the forward-looking statements. As such, forward looking statements should not be relied upon for future returns. Targeted returns reflect subjective determinations by Unigestion based on a variety of factors, including, among others, internal modeling, investment strategy, prior performance of similar products (if any), volatility measures, risk tolerance and market conditions. Targeted returns are not intended to be actual performance and should not be relied upon as an indication of actual or future performance. Data and graphical information herein are for information only and may have been derived from third party sources. Unigestion takes reasonable steps to verify, but does not guarantee, the accuracy and completeness of this information. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. All information provided here is subject to change without notice. It should only be considered current as of the date of publication without regard to the date on which you may access the information. Rates of exchange may cause the value of investments to go up or down. An investment with Unigestion, like all investments, contains risks, including total loss for the investor. Uni-Global – Cross Asset Navigator is a compartment of the Luxembourg Uni-Global SICAV Part I, UCITS IV compliant. This compartment is currently authorised for distribution in Austria, Belgium, Denmark, Finland, France, Germany, Ireland, Italy, Luxembourg, Netherlands, Norway, Spain, UK, Sweden, and Switzerland. In Italy, this compartment can be offered only to qualified investors within the meaning of art.100 D. Leg. 58/1998. Its shares may not be offered or distributed in any country where such offer or distribution would be prohibited by law. No prospectus has been filed with a Canadian securities regulatory authority to qualify the distribution of units of these funds and no such authority has expressed an opinion about these securities. Accordingly, their units may not be offered or distributed in Canada except to permitted clients who benefit from an exemption from the requirement to deliver a prospectus under securities legislation and where such offer or distribution would be prohibited by law. All investors must obtain and carefully read the applicable offering memorandum which contains additional information needed to evaluate the potential investment and provides important disclosures regarding risks, fees and expenses. All investors must obtain and carefully read the prospectus which contains additional information needed to evaluate the potential investment and provides important disclosures regarding risks, fees and expenses. Unless otherwise stated performance is shown net of fees in USD and does not include the commission and fees charged at the time of subscribing for or redeeming shares. Unigestion UK, which is authorised and regulated by the UK Financial Conduct Authority, has issued this document. Unigestion SA authorised and regulated by the Swiss FINMA. Unigestion Asset Management (France) S.A. authorised and regulated by the French Autorité des Marchés Financiers. Unigestion Asia Pte Limited authorised and regulated by the Monetary Authority of Singapore. Performance source: Unigestion, Bloomberg, Morningstar. Performance is shown on an annualised basis unless otherwise stated and is based on Uni Global – Cross Asset Navigator RA-USD net of fees with data from 15 December 2014 to 22 July 2019.Navigator Fund Performance

Performance, net of fees

2018

2017

2016

2015

Navigator (inception 15.12.2014)

-3.6%

10.6%

4.4%

-2.2%