- Global private equity investment activity recovered strongly in all regions in 2021, led by mid-market companies.

- Although 2022 is likely to be a year of consolidation, we expect the secondary market will remain strong, driven by LP stakes.

- In 2021, we committed EUR 806m to investments, including EUR 356m invested in 21 secondary transactions and EUR 240m invested in 15 direct investments and various add-ons.

Overview

Now that 2021 has drawn to a close, we can reflect on an extremely busy year in the private equity market where the bar was progressively raised from one quarter to the next. Although we began the year with record dry powder and positive investor sentiment, no-one would have predicted that global investment activity would ultimately reach EUR 1.2tn in 20211. more than 60% higher than 2020. The exit markets also roared back to life, after a subdued 2020, reaching EUR 860bn, more than 90% higher than 20202. Fundraising was more measured, with only a small increase on 2020. As a result, aggregate dry powder in the market reduced for the first time in many years as private equity managers were clearly too busy investing to focus on fundraising.

Trillion Euro Club

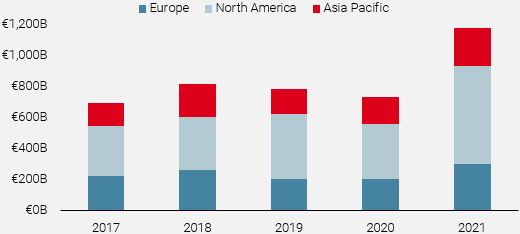

For the first time, investment activity went over the trillion euro mark. It was strong in all regions with North America posting the highest increase (+83%), given that the fall in this region had been most dramatic in 2020. At the same time, Europe (+48%) and Asia Pacific (+38%) both showed healthy rises.

Following the trend since the beginning of the pandemic, investment activity in mid-market companies (defined as deals with an enterprise value of less than EUR 500m) showed the biggest increase in 2021. The aggregate value of these deals increased by almost 70% in 2021, compared to 56% for large deals. It is notable that mid-market deals continue to account for 50% of the market given that they only took less than 40% of deal volume in the years leading up to the pandemic.

Figure 1: Investment Activity by Deal Size (EUR bn)

Source: Pitchbook. Data as at October 2021.

While exit activity is now back to pre-COVID (i.e. 2019) levels, the backlog of exits put on hold by the pandemic does not yet seem to have been fully cleared.

In 2021, the Unigestion Direct II strategy made 15 investments, taking the portfolio to 25 in total. While we saw more deals than ever, we have remained disciplined and have been able to invest in high quality, high growth companies playing our key investment themes at attractive valuations.

In November 2021, we invested in ReLife, a waste management and recycling company. ReLife is the only vertically integrated Italian leader in the recycling of paper, cardboard and plastic, a highly fragmented market ripe for consolidation. Having followed the company for several years, we acquired a minority stake alongside Italian GP, Xenon. The company plays our Resource Efficiency investment theme and has a measurable positive contribution to SDG 12 – Responsible Consumption and Production.

In December 2021, we invested in Yaneng Biosciences, a molecular diagnostics company in China. The company is the clear leader in the development and production of HPV tests for cervical cancer screening, thalassemia genetic tests as well as other diagnostics-related products and services. Yaneng is aligned with our Healthcare Reengineered investment theme and has a measurable positive contribution to SDG 3 – Good Health and Well-Being. We partnered on this deal with CBC Group, a leading healthcare-focused buyout/growth firm in China.

After a lacklustre 2020, private equity exit activity came back strongly in 2021. Although there was a fair amount of regional variation quarter on quarter last year, both Europe (+102%) and North America (+90%) showed equally strong increases for the full year, with Asia Pacific (+74%) slightly behind. While exit activity is now back to pre-COVID (i.e. 2019) levels, the backlog of exits put on hold by the pandemic does not yet seem to have been fully cleared.

We believe that the secondary market continues to have an important role to play in creating additional liquidity options for both GPs and LPs. For GPs, instead of exiting into a crowded market at potentially unfavourable valuations, they can seek the support of secondary investors to continue owning their best performing assets while giving existing LPs the option to take liquidity.

For LPs who would rather not wait for one or two more years for delayed exits to eventualise, the secondary market offers an efficient way for them to crystallise their gains. It is therefore no surprise that the secondary market reached USD 134bn in 2021, almost 50% of which was driven by GP-led transactions3.

In December, we led a single asset restructuring in Orbis Education & Care, a UK-based provider of special care services for children and adults associated with autism and other social, emotional and mental health needs. We obtained exclusive access to the transaction thanks to our strong, long-term relationship with the GP, August Equity. August has successfully grown Orbis both organically and through acquisitions underpinned by the company’s high quality services and long term patient relationships. Having built a strong footprint in Wales, August now sees the opportunity to further grow Orbis’ offering in England.

Our latest secondary strategy, Unigestion Secondary V, is now over 50% committed to 23 transactions (including those in closing). The final closing took place on 31 January 2022, with over EUR 840m raised.

In our view, the Fed’s plans to combine tapering, hiking and quantitative tightening in the same year raises the risk of policy mistake.

From “Behind the Curve” to “Policy Mistake”?

As 2022 has progressed, central banks have changed their tune, confirming that fighting inflation has become their top priority. To correct its mistake in assessing both the scale and sustainability of the inflation shock, the Fed is now set to normalise its monetary policy by combining tapering, hiking and quantitative tightening in the same year. Although normalising financial conditions via tightening makes sense, the timing and calibration has surprised financial markets and raised the risk of policy mistake.

Assessing the current outlook, our multi-dimensional monitoring of macro risk factors points to a number of positive signals. For example, our Growth Nowcasters for both developed and emerging countries show a global economy growing above its potential. At the same time, we are seeing an already well-priced tightening cycle for the next two years, in line with previous ones in terms of scale and timing.

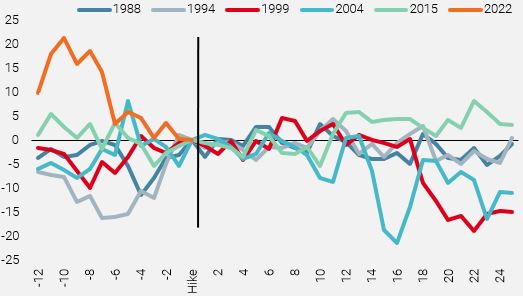

Nevertheless, the global picture is more mixed on a medium-term horizon. If the Fed delivers on inflation, we believe that real rates could return to neutral faster than currently priced, and this would imply a new injection of volatility and lead to further corrections in risky assets. A flatter forward US yield curve and an inverted VIX curve at the front end historically points to an economic slowdown and a rising risk of recession. It should also be noted that the Fed would start hiking while US consumers are struggling with the headwinds of negative real income, no more fiscal boost and a lower cushion, while saving rates have also normalised from 16% to 7% in 2021. It would be the first time since 1988 that the Fed hikes in parallel with declining US consumer confidence.

Figure 2: Michigan Confidence Ahead of First Fed Hike

Source: Bloomberg, Unigestion. Data as at 31 January 2022.

While the strength and speed of the recovery in private equity markets surprised even us, we were correct on nearly all of our 2021 predictions.

Our PE Outlook for 2022

As broadly expected, the private equity market had a much stronger year in 2021 than the COVID-afflicted prior year. While the strength and speed of the recovery surprised even us, we were correct on nearly all of our six 2021 predictions. First, the secondaries market did resume its strong pre-COVID growth, as predicted. Indeed, as previously mentioned, the market surpassed the USD 100bn milestone for the first time. Second, following this theme, GP-led transactions also hit a record high (USD 62bn in 2021 vs USD 26bn in 2020)4.

Third, while fundraising for small and mid-market private equity firms was 27% higher in 2021 than in 2020, it was not a record year and behind the pre-COVID high set in 20175. Nevertheless, given the frenetic investment activity at the lower end of the market, we still expect a large number of small and mid-market firms to fill up their coffers imminently.

Fourth, while it is difficult to confirm that a record was set, 46% of buyout funds in the market at the end of 2021 were being raised by first time managers or teams. However, as we said at the time, the bar will be very high for these funds and not all will be successful.

Fifth, driven by record investment volume in 2021, there has been a concurrent, strong uptick in co-investment and co-underwriting opportunities. This has certainly been true for us: in 2021, we saw more than 500 direct investment opportunities, a record for us and a strong indication that mid-market managers, fundless sponsors and founder management teams more than ever want to partner with experienced co-investors in order to co-lead or co-underwrite attractive global investment opportunities.

Finally, as already mentioned, investment activity rebounded strongly in 2021 to well beyond its pre-COVID level. In fact, investment activity in 2021 was 51% above the level set in 2019.

It is difficult to make predictions when it already feels like we are close to a market peak. Nonetheless, we hope that our 2022 outlook provides some interesting reading and insight into the market trends in both the short and long term.

2022 will be a year of consolidation for private equity managers. After hardly pausing for breath in 2021, private equity managers will slow down investment activity and focus more on portfolio management in 2022. This will express itself through a higher number of add-on acquisitions as managers look to strengthen existing portfolio companies, and increased exit activity as managers seek to crystallise high valuations.

The secondaries market will break further records, this time driven by LP stakes. In 2021, while the secondary market was more than 50% above its previous high in 2019 driven by the surge in GP-led transactions, the volume of LP-stake transactions was only just above its pre-COVID levels. Given that global aggregate AUM across all buyout funds has more than doubled in the last four years and investors still have significant exposure to pre-2011 vintage funds, the pressure to rebalance portfolios will be greater than ever. Consequently, we predict that LP-stakes will account for more than 60% of secondary volume in 2022.

Private equity interest will move away from IT and healthcare in favour of financial services and climate impact. In the last few years, the IT and healthcare sectors have taken an increasing share of deal activity (e.g. 37% of buyout volume in the US in 20215), helped especially by their strength during the pandemic. Driven by the search for attractively valued opportunities, we predict that sectors such as financial services (less than 10% of buyout volume in the US in 2021) and climate impact will materially rise in prominence in 2022. In financial services, private equity investors will be on the lookout for innovative fintech companies to challenge the incumbent players. While in climate impact, generalist investors will be enticed by the supply of opportunities created by current tailwinds (see next prediction).

A record amount of capital will be raised for impact funds. The introduction of SFDR (Sustainable Financial Disclosure Regulations) in March 2021 was a big step towards the standardisation of ESG integration, measurement and reporting for all EU-based financial firms. This has particularly given investors the requisite comfort to invest in impact. In addition, initiatives coming out of the COP26, such as commitments to achieve carbon net-zero by 2050, have encouraged investors to increase their exposure to climate impact sectors. Indeed, the confluence of governments, companies and consumers now fully focusing on carbon emission reduction has created highly attractive investment opportunities across multiple climate-related sub-sectors. Consequently, investors will seek to invest record amounts in impact funds in 2022.

The confluence of governments, companies and consumers now fully focusing on carbon emission reduction has created highly attractive investment opportunities across multiple climate-related sub-sectors.

There will be a step up in the demand and supply of retail private equity products. Anecdotally, there was a huge increase in demand for private equity from high net worth individuals (HNWIs) in 2021. However, traditional closed-end funds are not ideal for such investors given that they often need shorter term liquidity. Meanwhile, smaller, “retail” investors have difficulty accessing private equity due to large minimum ticket size requirements, high costs and the limited liquidity options. Recently, one or two private equity evergreen platforms designed precisely for retail investors have emerged (including one which Unigestion launched in Canada). As innovative private equity firms continue to develop low cost, scalable digital platforms, we believe the number of retail private equity products will proliferate in 2022. These solutions will become the preferred investment route for retail investors, as well as HNWIs.

Whatever is in store for the private equity market in 2022, it will certainly not be boring. We look forward to another year of innovative deal making.

Unigestion Private Equity Activity

In 2021, the Unigestion private equity team committed EUR 806m to investments, including EUR 356m invested in 21 secondary transactions and EUR 240m invested in 15 direct investments and various add-ons. Here are the highlights of some of the investments and exits that we completed in Q4:

At the beginning of October, Unigestion closed a structured secondary transaction in Euroknights VII, a 2017 vintage fund consisting of a well-diversified portfolio of 14 companies across France, Benelux, Germany and Italy. The fund is managed by Argos Wityu, an experienced fund manager and an existing Unigestion relationship focusing on middle-market buyouts in countries where it has local offices. They specialise in value investing by resolving complex situations at entry and further enhancing value through professionalisation, operational improvements and new growth initiatives.

At the beginning of October, Unigestion closed a structured secondary transaction in Euroknights VII, a 2017 vintage fund consisting of a well-diversified portfolio of 14 companies across France, Benelux, Germany and Italy. The fund is managed by Argos Wityu, an experienced fund manager and an existing Unigestion relationship focusing on middle-market buyouts in countries where it has local offices. They specialise in value investing by resolving complex situations at entry and further enhancing value through professionalisation, operational improvements and new growth initiatives.

During October, Unigestion also closed an investment in Metrodora Education alongside Magnum Industrial Partners. Metrodora is a leading education group in healthcare sciences across Spain and Portugal, created by Magnum via the acquisition of three private schools: CESIF, ISEP, and CEEP. Metrodora will look to grow by launching new programmes and by continuing to acquire add-ons, taking advantage of Spain’s highly fragmented healthcare education market, and by extracting commercial and cost synergies from group integration.

During October, Unigestion also closed an investment in Metrodora Education alongside Magnum Industrial Partners. Metrodora is a leading education group in healthcare sciences across Spain and Portugal, created by Magnum via the acquisition of three private schools: CESIF, ISEP, and CEEP. Metrodora will look to grow by launching new programmes and by continuing to acquire add-ons, taking advantage of Spain’s highly fragmented healthcare education market, and by extracting commercial and cost synergies from group integration.

Also in October, we exited ACTINEO, the German market leader for the digitization and medical assessment of bodily injury claims. The group operates in Germany, Austria, France, Spain and Italy and provides holistic data management and software-based solutions to support insurance companies in managing the entire bodily injury claims process.

Also in October, we exited ACTINEO, the German market leader for the digitization and medical assessment of bodily injury claims. The group operates in Germany, Austria, France, Spain and Italy and provides holistic data management and software-based solutions to support insurance companies in managing the entire bodily injury claims process.

Unigestion invested in ACTINEO alongside The Riverside Company in June 2019. During the holding period, ACTINEO built out its technology platform and capabilities to significantly extend the range of services and claim processing support it offers clients. Through the launch of ANTEVIS, the company also expanded its business into the French, Spanish and Italian markets, further strengthening its positioning as the leading European InsurTech platform in the market for bodily injury claims. The transaction resulted in a gross TVPI of 2.2x and 37% gross IRR with further upside through an earn-out mechanism.

In the same month, Unigestion invested in LipoClinic alongside Invision. LipoClinic is a leader in the treatment of lipedema, carrying out more than 3,000 surgeries per year. Besides the advisory of patients, the company also focuses on the operational treatment of lipedema. With a well-trained team of surgeons as well as the latest technological equipment, LipoClinic offers first-class medical know-how, innovative treatment methods and a proven service quality. The company has two clinics in Germany, Mülheim an der Ruhr and Hamburg, and one in Salzburg, Austria.

In the same month, Unigestion invested in LipoClinic alongside Invision. LipoClinic is a leader in the treatment of lipedema, carrying out more than 3,000 surgeries per year. Besides the advisory of patients, the company also focuses on the operational treatment of lipedema. With a well-trained team of surgeons as well as the latest technological equipment, LipoClinic offers first-class medical know-how, innovative treatment methods and a proven service quality. The company has two clinics in Germany, Mülheim an der Ruhr and Hamburg, and one in Salzburg, Austria.

During November, we invested in Evolution Technology II. Evolution Equity Partners is a global venture capital firm focusing on cybersecurity and related sectors. Founded in 2008, Evolution has been investing in cybersecurity companies in the US and Europe for more than 15 years and has developed a hands-on approach across its portfolio. Evolution’s presence in both the US and Europe supports international growth and cross-border access to key partners which is critical for entrepreneurs seeking to achieve a high growth trajectory. Evolution Technology II has already made 11 investments to date and is valued at 2.1x gross MOI as of Q3 2021.

During November, we invested in Evolution Technology II. Evolution Equity Partners is a global venture capital firm focusing on cybersecurity and related sectors. Founded in 2008, Evolution has been investing in cybersecurity companies in the US and Europe for more than 15 years and has developed a hands-on approach across its portfolio. Evolution’s presence in both the US and Europe supports international growth and cross-border access to key partners which is critical for entrepreneurs seeking to achieve a high growth trajectory. Evolution Technology II has already made 11 investments to date and is valued at 2.1x gross MOI as of Q3 2021.

Also in November, Unigestion led an investment in Home Instead. The company has over 8,000 employees and specialises in caring for seniors in their own homes. It is headquartered in Rheinfelden, Switzerland and is active in Switzerland, Austria, Ireland, Holland and France. Recently, following an acquisition, it has also moved into the Australian market. Services range from everyday care, night services, 24-hour care and dementia care to provide support in palliative situations. The company is market leader in non-medical home care in Switzerland and Ireland, and the third largest provider in Holland. It has achieved consistent growth since 2013, making 22 acquisitions. The European home care market is expected to grow at a compound annual growth rate of 7% to 9% over the next five years.

Also in November, Unigestion led an investment in Home Instead. The company has over 8,000 employees and specialises in caring for seniors in their own homes. It is headquartered in Rheinfelden, Switzerland and is active in Switzerland, Austria, Ireland, Holland and France. Recently, following an acquisition, it has also moved into the Australian market. Services range from everyday care, night services, 24-hour care and dementia care to provide support in palliative situations. The company is market leader in non-medical home care in Switzerland and Ireland, and the third largest provider in Holland. It has achieved consistent growth since 2013, making 22 acquisitions. The European home care market is expected to grow at a compound annual growth rate of 7% to 9% over the next five years.

In the same month, Unigestion invested in Unovis NCAP II. Unovis is the global leader in the alternative protein sector. The team provides seed funding to entrepreneurs developing innovative plant-based and cultivated replacements for animal products, including meat, seafood, dairy and eggs. Unovis’s goal is to transform the global food system by investing in solutions that facilitate sustained behavioural change and eliminate the consumption of animal protein products, which will have a positive impact on the environment, human health and society as a whole.

In the same month, Unigestion invested in Unovis NCAP II. Unovis is the global leader in the alternative protein sector. The team provides seed funding to entrepreneurs developing innovative plant-based and cultivated replacements for animal products, including meat, seafood, dairy and eggs. Unovis’s goal is to transform the global food system by investing in solutions that facilitate sustained behavioural change and eliminate the consumption of animal protein products, which will have a positive impact on the environment, human health and society as a whole.

In November, Unigestion also invested in Capiton VI. Capiton, based in Berlin, Germany, focuses on investments in profitable medium-sized companies in Germany, Austria and Switzerland that are looking for succession solutions or spin-off opportunities. The fund focuses on control investments in companies which generate revenues of EUR 50-250m. In addition to organic growth initiatives, Capiton has successfully created value through multiple buy-and-build concepts. As of 30 September 2021, Capiton VI had already invested in seven target companies.

In November, Unigestion also invested in Capiton VI. Capiton, based in Berlin, Germany, focuses on investments in profitable medium-sized companies in Germany, Austria and Switzerland that are looking for succession solutions or spin-off opportunities. The fund focuses on control investments in companies which generate revenues of EUR 50-250m. In addition to organic growth initiatives, Capiton has successfully created value through multiple buy-and-build concepts. As of 30 September 2021, Capiton VI had already invested in seven target companies.

Also in December, Unigestion invested in Polara Enterprises (www.polara.com) alongside Vance Street Capital. Polara is a US manufacturer of Accessible Pedestrian Signals (APS) that are installed in crosswalk and intersection traffic safety systems. The company is the US market leader with over 50% market share and benefits from regulatory tailwinds supporting the increasing prevalence of APS systems, which only 10% of US intersections currently have installed. Polara plans to continue its strong organic growth, expand its product portfolio into IoT and smart traffic products, and acquire smaller players around the traffic ecosystem.

Also in December, Unigestion invested in Polara Enterprises (www.polara.com) alongside Vance Street Capital. Polara is a US manufacturer of Accessible Pedestrian Signals (APS) that are installed in crosswalk and intersection traffic safety systems. The company is the US market leader with over 50% market share and benefits from regulatory tailwinds supporting the increasing prevalence of APS systems, which only 10% of US intersections currently have installed. Polara plans to continue its strong organic growth, expand its product portfolio into IoT and smart traffic products, and acquire smaller players around the traffic ecosystem.

In the same month, Unigestion closed an investment in a single-asset continuation vehicle for Verisma Systems (www.verisma.com) alongside New Spring Capital. Verisma manages the complex, end-to-end locating, validating and release of protected health information (PHI) through proprietary software and services sold to a blue-chip roster of health systems. The company operates in a market with significant industry tailwinds – continued demand for accurate, timely, and efficient PHI systems. Currently, 55% of the US healthcare market remains whitespace for PHI providers. Verisma will benefit from a strong pipeline of new client bookings in 2021 and historic client retention of 99%.

In the same month, Unigestion closed an investment in a single-asset continuation vehicle for Verisma Systems (www.verisma.com) alongside New Spring Capital. Verisma manages the complex, end-to-end locating, validating and release of protected health information (PHI) through proprietary software and services sold to a blue-chip roster of health systems. The company operates in a market with significant industry tailwinds – continued demand for accurate, timely, and efficient PHI systems. Currently, 55% of the US healthcare market remains whitespace for PHI providers. Verisma will benefit from a strong pipeline of new client bookings in 2021 and historic client retention of 99%.

In December, Unigestion also closed a direct investment in SuanFarma (www.suanfarma.com) alongside Archimed. Founded in 1993 in Spain, SuanFarma supplies all types of pharmaceutical and nutraceutical companies with active ingredients, acting as a vertically integrated distributor and manufacturer of selected molecules and an emerging developer and manufacturer of selected Active Pharmaceutical Ingredients (APIs). The company manages a highly diversified ingredient portfolio of around 890 APIs and around 1,100 nutraceutical ingredients and is one of only a few independent players with its own manufacturing sites in Europe. Besides its own production, SuanFarma sources APIs from all over the world, which on top of managing timely deliveries, provides the company’s customers with regulatory and technical support.

In December, Unigestion also closed a direct investment in SuanFarma (www.suanfarma.com) alongside Archimed. Founded in 1993 in Spain, SuanFarma supplies all types of pharmaceutical and nutraceutical companies with active ingredients, acting as a vertically integrated distributor and manufacturer of selected molecules and an emerging developer and manufacturer of selected Active Pharmaceutical Ingredients (APIs). The company manages a highly diversified ingredient portfolio of around 890 APIs and around 1,100 nutraceutical ingredients and is one of only a few independent players with its own manufacturing sites in Europe. Besides its own production, SuanFarma sources APIs from all over the world, which on top of managing timely deliveries, provides the company’s customers with regulatory and technical support.

1,Pitchbook

2,ibid

3,Greenhill, September 2021

4,Greenhill

5,Preqin

6,Pitchbook

Important information

Past performance is no guide to the future, the value of investments, and the income from them change frequently, may fall as well as rise, there is no guarantee that your initial investment will be returned. This document has been prepared for your information only and must not be distributed, published, reproduced or disclosed (in whole or in part) by recipients to any other person without the prior written consent of Unigestion. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation.

This is a promotional statement of our investment philosophy and services only in relation to the subject matter of this presentation. It constitutes neither investment advice nor recommendation. This document represents no offer, solicitation or suggestion of suitability to subscribe in either the investment vehicles to which it refers or to any securities or financial instruments described herein. Any such offer to sell or solicitation of an offer to purchase shall be made only by formal offering documents, which include, among others, a confidential offering memorandum, limited partnership agreement (if applicable), investment management agreement (if applicable), operating agreement (if applicable), and related subscription documents (if applicable). Such documentation contains additional information material to any decision to invest. Please contact your professional adviser/consultant before making an investment decision.

Where possible we aim to disclose the material risks pertinent to this document. The views expressed in this document do not purport to be a complete description of the securities, markets and developments referred to in it. Reference to specific securities should not be considered a recommendation to buy or sell. Unigestion maintains the right to delete or modify information without prior notice.

Investors shall conduct their own analysis of the risks (including any legal, regulatory, tax or other consequences) associated with an investment and should seek independent professional advice. Some of the investment strategies or financial instruments described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment. These are not suitable for all types of investors. Unigestion has the ability in its sole discretion to change the strategies described herein.

To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks. Actual results could differ materially from those in the forward-looking statements. As such, forward looking statements should not be relied upon for future returns. Targeted returns reflect subjective determinations by Unigestion based on a variety of factors, including, among others, internal modeling, investment strategy, prior performance of similar products (if any), volatility measures, risk tolerance and market conditions. Targeted returns are not intended to be actual performance and should not be relied upon as an indication of actual or future performance.

No separate verification has been made as to the accuracy or completeness of the information herein. Data and graphical information herein are for information only and may have been derived from third party sources. Unigestion takes reasonable steps to verify, but does not guarantee, the accuracy and completeness of information from third party sources. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. All information provided here is subject to change without notice. It should only be considered current as of the date of publication without regard to the date on which you may access the information. Rates of exchange may cause the value of investments to go up or down. An investment with Unigestion, like all investments, contains risks, including total loss for the investor.

Unigestion Direct II (UDII) has been created as a SCS-SICAV-RAIF in Luxembourg and qualifies as an Alternative Investment Fund (AIF) within the meaning of the law dated 12 July 2013 on Alternative Investment Fund Managers implementing the Directive 2011/61/EU (AIFMD). As a result, units of this vehicle may be offered only to professional investors and may not be distributed on a public basis in or from any country where such distribution would be prohibited by law. This document contains a preliminary summary of the purpose and principal business terms of an investment in UDII. This summary does not purport to be complete and is qualified in its entirety by reference to the more detailed discussion to take place with the AIF. UDII has the ability in its sole discretion to change the strategies described herein. Before making a decision to invest in UDII, you are advised to consult with your tax, legal and financial advisors.

Unigestion Secondary V (USec V) has been created as a SCS-SICAV-RAIF in Luxembourg and will qualify as an Alternative Investment Fund (AIF) within the meaning of the law dated 12 July 2013 on Alternative Investment Fund Managers implementing the Directive 2011/61/EU (AIFMD). As a result, units of this vehicle may be offered only to professional investors and may not be distributed on a public basis in or from any country where such distribution would be prohibited by law. This document contains a preliminary summary of the purpose and principal business terms of an investment in Unigestion Secondary V. This summary does not purport to be complete and is qualified in its entirety by reference to the more detailed discussion to take place with the AIF. Unigestion Secondary V will have the ability in its sole discretion to change the strategies described herein. Before making a decision to invest in Unigestion Secondary V, you are advised to consult with your tax, legal and financial advisors..

Additional Information for US Investors

The performance figures are based on estimated fees and expenses as well as on the underlying strategy’s estimated performances given by fund managers, administrators, custodians and third party sources at a given date. Where performance is reflected gross of fees, potential investors should be aware that the inclusion of fees, costs and charges will reduce the overall value of performance. Unless otherwise stated, the performance data source are Unigestion, Bloomberg and Compustat.

For US investors, Unigestion is relying on SEC Rule 15a-6 under the Securities Exchange Act of 1934 regarding exemptions from broker-dealer registration for foreign broker dealers. Foreside Global Services, LLC is acting as the chaperoning broker dealer for Unigestion for the purposes of soliciting and effecting transactions with or for U.S. institutional investors or major U.S. institutional investors

This information is provided to you solely to give you background information relating to Unigestion, certain strategies it implements and currently offers. Before making an investment decision with respect to the strategy discussed herein, potential investors are advised to consult with their tax, legal, ERISA and financial advisors. Note that not all strategies may be available or suitable for investment by U.S. investors.

This document may contain forward-looking statements, including observations about markets and industry and regulatory trends as of the original date of this document. Forward-looking statements may be identified by, among other things, the use of words such as “expects,” “anticipates,” “believes,” or “estimates,” or the negatives of these terms, and similar expressions. Forward-looking statements reflect Unigestion’s views as of such date with respect to possible future events. Actual results could differ materially from those in the forward-looking statements as a result of factors beyond a strategy’s or Unigestion’s control. Readers are cautioned not to place undue reliance on such statements. No party has an obligation to update any of the forward-looking statements in this document

Return targets or objectives, if any, are used for measurement or comparison purposes and only as a guideline for prospective investors to evaluate a particular investment program’s investment strategies and accompanying information. Performance may fluctuate, especially over short periods. Targeted returns should be evaluated over the time period indicated and not over shorter periods.

The past performance of Unigestion, its principals, shareholders, or employees is not indicative of future returns.

Except where otherwise specifically noted, the information contained herein, including performance data and assets under management, relates to the entire affiliated group of Unigestion entities over time including that of Unigestion UK. Such information is intended to provide the reader with background regarding the services, investment strategies and personnel of the Unigestion entities. No guarantee is made that all or any of the individuals involved in generating the performance on behalf the other Unigestion entities will be involved in managing any client account on behalf of Unigestion U.K. More specific information regarding Unigestion UK is set forth herein where indicated and is available on request.

There is no guarantee that Unigestion will be successful in achieving any investment objectives. An investment strategy contains risks, including the risk of complete loss.

The risk management practices and methods described herein are for illustrative purposes only and are subject to modification.

Legal Entities Disseminating This Document

UNITED KINGDOM

This material is disseminated in the United Kingdom by Unigestion (UK) Ltd., which is authorized and regulated by the Financial Conduct Authority („FCA“). This information is intended only for professional clients and eligible counterparties, as defined in MiFID directive and has therefore not been adapted to retail clients.

UNITED STATES

This material is disseminated in the U.S. by Unigestion (UK) Ltd., which is registered as an investment adviser with the U.S. Securities and Exchange Commission (“SEC”). This information is intended only for institutional clients and qualified purchasers as defined by the SEC and has therefore not been adapted to retail clients.

EUROPEAN UNION

This material is disseminated in the European Union by Unigestion Asset Management (France) SA which is authorized and regulated by the French “Autorité des Marchés Financiers” („AMF“).

This information is intended only for professional clients and eligible counterparties, as defined in the MiFID directive and has therefore not been adapted to retail clients.

CANADA

This material is disseminated in Canada by Unigestion Asset Management (Canada) Inc. which is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario, Quebec and Newfoundland & Labrador. Its principal regulator is the Ontario Securities Commission („OSC“). This material may also be distributed by Unigestion SA which has an international advisor exemption in Quebec, Saskatchewan and Ontario. Unigestion SA’s assets are situated outside of Canada and, as such, there may be difficulty enforcing legal rights against it.

SWITZERLAND

This material is disseminated in Switzerland by Unigestion SA which is authorized and regulated by the Swiss Financial Market Supervisory Authority („FINMA“).

Document issued February 2022.