The Challenges of Benchmarking Private Equity Performance

Analyst, Private Equity

Partner, Private Equity

Key Points

- The constituents of default peer groups are often a mix of funds with different strategies.

=> Create your own peer group.

- Performance data is self-reported, leading to data scarcity, data inconsistency and material survivorship bias.

=> Aggregate data from different databases, use reported cash flows to validate performance metrics and cross-check data with other sources (PE managers’ quarterly reports, if available).

- IRR and TVPI are easily distorted and should not be considered on their own when benchmarking.

=> Consider all performance metrics available: TVPI, IRR, DPI and PIC.

- In summary, use benchmarks responsibly!

Overview

Investors put increasing emphasis on benchmarking private equity (PE) funds using specialised PE performance databases, with the aim of backing only managers with top or second quartile funds. Being a subscriber and a regular user of these databases, we obviously find significant value in them. However, we have experienced numerous pitfalls that may lead investors to distorted conclusions if they take the information as read.

For example, when performance data is voluntarily reported, the so-called survivorship bias is one of the most common hazards of benchmarking analyses. Our research shows that the best performing funds report performance data (hence are part of the benchmarks) more systematically than the worst performing funds[1]. The survivorship bias, as well as other biases described in this paper, are common issues in private equity.

The goal of this paper is to raise awareness amongst PE investors and advocate for a critical eye when interpreting benchmarking results. To do so, we highlight concrete examples of the inherent pitfalls of benchmarking funds if solely considering data from PE performance databases. Accurate benchmarking requires a meaningful and representative data sample as well as mathematically accurate metrics in the first place. That being said, we should clarify that the goal of this paper is not to discredit one or several PE performance databases (hence why we do not name the databases and use “Database X” to represent them). Rather, our intention is to highlight the shortcomings of voluntarily reported data and limited datasets.

We first explain how PE benchmarks are constructed and uncover that the constituents of peer groups are often a mix of funds with quite different strategies. Secondly, we show the biases and data inconsistencies resulting from the voluntarily reported nature of the benchmarking dataset. Third, we discuss the commonly used PE performance metrics, highlight their pitfalls and demonstrate how they can be distorted through the timing of cash flows and/or use of credit lines. At the end of each section, we make recommendations to overcome the challenges discussed in such section.

How are Benchmarks Constructed

Before using a benchmark, it is important to understand how such benchmark is constructed and how peer group constituents are selected. Below we illustrate how Database X determines peer groups and calculates quartile ranking.

How Databases Determine Peer Groups and Calculate Quartile Ranking

Determining a Peer Group

While PE performance databases typically allow users to build bespoke peer groups, they publish quartile rankings on the basis of their own peer grouping. In Database X, a 2010 vintage Europe-focused growth capital fund, for example, will be mapped to a peer group composed of at least eight funds reporting a performance metric for the last five quarters. The default peer group will be the most granular one, i.e. “2010/Europe/Growth”. If there are fewer than eight funds in the peer group, the mapping will be expanded first to “2010/All Regions/Growth”, then to “2010/Europe/PE” and up to “2010/All Regions/Private Capital” if needed, until eight funds are found.

The distribution of quartile rankings within a peer group may not be split in four equal sets.

Following the above, a “2010/Europe/Growth” fund may be benchmarked against the broader “2010/All Regions/Growth” peer group which includes funds that are themselves benchmarked against the narrower “2010/US/Growth” peer group. This explains why the distribution of quartile rankings within a peer group may not be split in four equal sets. Simply put, if we consider a group of 20 funds made of 7 European and 13 US funds, chances are that quartiles 1-2-3-4 are not made of 5 funds each (as they should be), but rather of, say, 7 funds in quartile 1, 5 funds in quartile 2, 4 funds in quartile 3 and 4 funds in quartile 4

Calculating Default Quartile Ranking

By default, all funds are ranked within a peer group by the Internal Rate of Return (IRR) and the Total Value to Paid-In (TVPI) – please refer to the ILPA definitions in the “Glossary” section on page 11:

- Sorting funds according to IRR and recording the rank of each fund (1 for the best, 2 for the second best, and so on).

- Sorting funds according to TVPI and recording the rank of each fund.

- Finding the “Total Rank” by summing the IRR and the TVPI rank for each fund.

- The quartile ranking is then based on the “Total Rank” number.

Note that If the IRR is missing, the rank of the TVPI will be weighted according to: Total rank = TVPI rank + (# funds reporting IRR in the peer group/# funds reporting TVPI in the peer group) * TVPI rank. If the TVPI is missing, the rank of the IRR will be weighted according to: Total rank = IRR rank + (# funds reporting TVPI in the peer group/# funds reporting IRR in the peer group) * IRR rank.

Adjusting Quartile Ranking

As a final step, Database X may manually adjust some of the quartile rankings. For example, if a fund is 2nd quartile in TVPI and 2nd quartile in IRR, Database X will adjust the quartile ranking to 2nd quartile even if, following the above methodology, the fund is 3rd quartile overall.

Peer Group Relevance

Assessing if peers in a peer group are comparable is a crucial step. We previously highlighted how the mapping of peer groups is expanded in case there are less than eight funds in the group. This raises concerns on the relevance of peer groups.

We analysed the peer groups against which our own funds are benchmarked and observed that close to 50% of the peers are not comparable.

We analysed the peer groups against which our own funds are benchmarked in Database X. We observed that close to 50% of the peers are not comparable, mostly because the peer i) follows a very different investment strategy, ii) has a much narrower geographic focus, iii) is a duplicate – typically a sleeve – of a fund already in the peer group or iv) has a fund size of less that USD 25 million that makes it not investable by institutional investors. For example, a European Fund-of-Funds (FoF) investing in buyout cannot be accurately compared to a US FoF investing in venture capital.

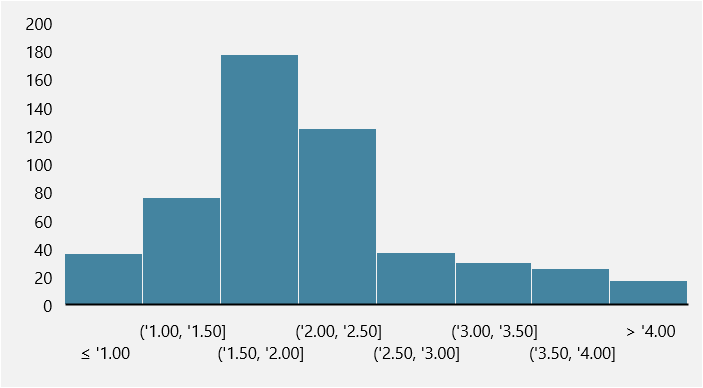

In order to benchmark our own FoFs (focus on buyout primaries), we analysed the performance of all the FoFs with vintages 2010 to 2018 which report data in Database X (as at 13.05.2022). Figure 1 shows the dispersion of TVPI for the aforementioned data set.

Figure 1: TVPI Dispersion – All FoFs – Vintage 2010 to 2018

Source: Unigestion and Database X, as at 13.05.2022

What directly stands out is that 236 out of 493 FoFs (48%) report a TVPI higher than 2.0x and, even more surprisingly, 74 out of 493 FoF (15%) report a TVPI higher than 3.0x. Database X requires managers to report performance “net to investors”. Thus, to generate a 3.0x TVPI, a FoF must generate a gross TVPI of c. 4.0x at portfolio level, before any fees and expenses. Such a performance is very rare, except maybe in a few concentrated venture capital FoFs amid bull market conditions.

45% of the FoFs with a TVPI higher than 3.0x either report a size below USD 100 million or do not report any fund size.

This is confirmed by the following findings:

- None of the FoFs with a TVPI higher than 3.0x focuses on buyout primaries.

- 85% of the FoFs with a TVPI higher than 3.0x invest mostly in venture capital. One of these even invests only in blockchain with a fund size of USD 8 million. The remaining 15% are either i) local FoFs, ii) FoFs with a significant proportion of growth capital, secondaries and co-investments, iii) sleeves of a larger FoF programme – e.g. Emerging Fund II-A as a sleeve of the Emerging Fund II, or iv) managed accounts, possibly evergreen with recycling mechanisms (e.g. Fund X Separate Account A).

- 45% of the FoFs with a TVPI higher than 3.0x either report a size below USD 100 million or do not report any fund size. The smallest fund in the sample is a USD 5 million fund (with a stunning 4.4x TVPI and 110% IRR).

All the above lead to large discrepancies in the way PE performance databases determine peer groups and calculate quartile rankings. For a user, there is little possibility to systematically filter out funds that are not comparable. Such a filtering process requires time-consuming analysis as well as insights on all peer group constituents.

Recommendations

- At the very least, seek to identify the constituents of the peer group proposed by the database and eliminate the obvious “odd ones out”.

- Better, create your own bespoke peer group with funds that have truly comparable strategies and represent real investment alternatives for you.

Data Biases

Alternative investments, including PE as well as hedge funds, are well known for having biases in their datasets, mainly because of their illiquid and private nature. In their paper, Fung and Hsieh (2009) “Perspectives: Measurement Biases in Hedge Fund Performance Data: An Update” elaborate on the survivorship bias, the backfill bias (when an index provider adds a new fund to their index and “fills in” prior returns of that fund) and warn investors to be “mindful of how much of the hedge fund industry one is observing before passing judgment on the performance statistics of the hedge fund industry as a whole”. We have encountered similar biases within PE.

Discretion in Reporting

PE managers enjoy a large amount of discretion when it comes to reporting performance in databases.

PE managers can decide whether to report figures in a specific quarter or not and to report only TVPI or only IRR.

- PE managers can request performance data contributed by one of their LPs to be removed.

- PE managers can decide whether to report figures in a specific quarter or not and to report only TVPI or only IRR. As explained previously, a standalone TVPI or IRR measure may be highly misleading.

- PE managers are required to report performance figures on a “net to investors” basis. “Net to investors” means net of: i) management fees and other fund expenses, ii) realised carried interest and, importantly, iii) carried interest provisions (i.e. the carried interest that the manager would receive if the unrealised portfolio of the fund was liquidated at current valuation). This is however not always the case. We came across numerous examples where performance is reported as gross of one (or more) of these three items.

Data Inconsistency

The best way to verify whether a fund’s performance is accurately reported would be to compare the reported metrics to the Capital Account Statements or Investor Quarterly Reports of the funds. These documents are unfortunately not available unless one is an investor in the fund or has close ties with its fund manager.

One of the PE performance databases however allows users to access the underlying cash flows of a specific fund (if available). Whilst this does not guarantee the accuracy of the data, it is of great help to understand how TVPI and IRR derive from the quarterly cash flows and NAV development. In some instances, we could not reconcile reported performance metrics with quarterly cash flows. For example, “Fund V”, a 2018 fund, reports an IRR of 33% whilst calculating the IRR from the cash flows and residual NAV gives an IRR or 22%. This represents a difference of 11%. Surprisingly, both reported and calculated TVPIs are identical, at 1.35x.

Data Scarcity

Clearly, no PE performance database can give access to a complete dataset, due to the private nature of the asset class. Still, it is surprising to see the limited performance data coverage as compared to the size of the overall PE universe.

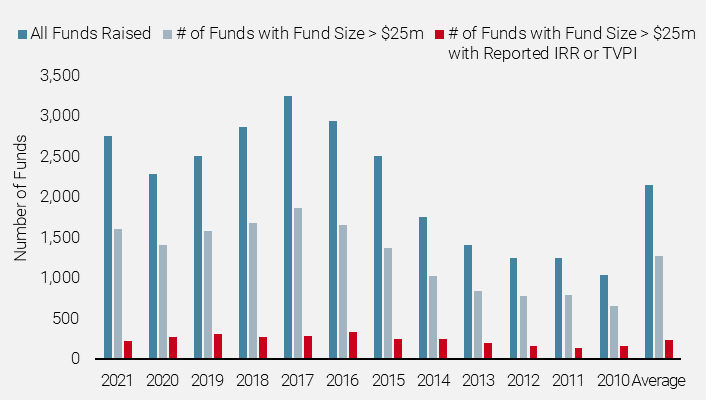

Out of the 25’818 funds raised, only 2’890 (11%) have reported at least a TVPI or an IRR over the last four quarters

Figure 2 shows the number of funds raised from 2010 to 2021 versus the number of such funds reporting performance data in Database X as at May 2022. Out of the 25’818 funds raised, only 2’890 (11%) have reported at least a TVPI or an IRR over the last four quarters. The percentage grows from 11% to 19% if we only consider funds having raised more than USD 25 million.

A sample size of about one-fifth of the size of the whole universe can only be fully representative if the sample is the result of a random selection.

A sample size of about one-fifth of the size of the whole universe can only be fully representative if the sample is the result of a random selection. However, in our case, the sample cannot be the result of a random selection because it derives from voluntary reporting.

Figure 2: Number of Funds Raised vs. Number of Funds Reporting Performance

Source: Unigestion and Database X, as at 13.05.2022.

Data Scarcity

As mentioned in the Overview section, we have witnessed a trend whereby worst performing funds tend to be less represented than best performing funds in PE performance databases. This suggests some form of survivorship bias.

Worst performing funds tend to be less represented than best performing funds in PE performance databases. This suggests some form of survivorship bias.

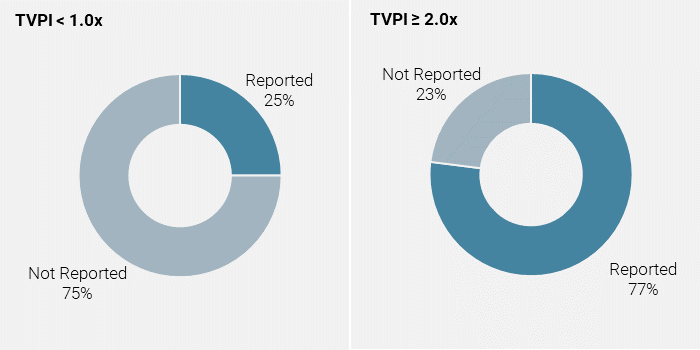

In Figure 3, we show the result of an analysis based on one of our most diversified evergreen PE programmes, which has made over 100 fund investments over 20 years. 77% of the funds with a TVPI above 2.0x reported at least one performance metrics in Database X over the last five quarters (as at May 2022). Conversely, only 25% of the funds with a TVPI below 1.0x reported at least one of performance metrics[2]. Therefore, the average performance of funds which report performance metrics is likely higher than the average performance of the whole universe of funds.

The average performance of funds which report performance metrics is likely higher than the average performance of the whole universe of funds.

Figure 3: Proportion of Funds Reporting Performance Based on their TVPI

Source: Unigestion and Database X, as at 13.05.2022.

Recommendations

- Verify that the PE managers in the peer group systematically report performance, i.e. every quarter, for all their funds (Fund I, Fund II, Fund III, etc.).

- Use reported cash flows to validate performance metrics.

- Ensure that reported performance is truly “net to investors” by cross-checking with other sources (for example quarterly reports if available).

- Aggregate and cross-check data from multiple databases

Which Metrics are Used to Measure PE Performance?

The most commonly used performance metrics in PE are the TVPI and the IRR. Nonetheless, these metrics are prone to misinterpretation and are easy to manipulate through timing of cash flows and/or credit line usage.

Beware of IRR Pitfalls

This IRR and multiple combination indicates that the rate of return experienced by investors is likely to be much lower than 46%

Various academics have researched the dangers of using IRR as a performance measure. One of the best known research papers on the subject was written by Phalippou (2008) “The Hazards of Using IRR to Measure Performance: The Case of Private Equity”. In the paper, Phalippou highlighted two of the best performing funds in Calpers’ portfolio, according to the Calpers Performance Report as at June 2007: (1) Media Communication Partners II, L.P. (vintage 1992) with a TVPI of 4.5x and an IRR of 39% and (2) Doughty Hanson Fund II, L.P. (vintage 1995) with a TVPI of 2.0x and an IRR of 46%. Phalippou rightly pointed out that, in a simplified scenario where the fund contributes all of its capital on day 1 and receives all proceeds through one distribution, the capital would need to be invested for 4½ years compounding at an IRR of 39% in order to generate a TVPI of 4.5x. However, the capital would only need to be invested for less than 2 years compounding at an IRR of 46% in order to generate a TVPI of 2.0x. Whilst it can happen that some deals are exited after a short holding period of 2 years, it is highly unlikely that the overall portfolio of a PE fund is exited in an average of 2 years. In the case of Doughty Hanson Fund II, the short holding period implied by the combination of its TVPI and IRR somewhat contradicts the fact that the fund is still up and running after 12 years of existence. As Phalippou puts it: “(…) this IRR and multiple combination indicates that the rate of return experienced by investors is likely to be much lower than 46%.”

Applying Phalippou’s approach, we picked a more recent “real life” example, the one already mentioned on page 4. Fund V (intentionally kept anonymous), a 2018 vintage fund, reported a TVPI of 1.35x and an IRR of 33% at 31.12.2021 in Database X. Based on the combination of TVPI and IRR, Fund V has an implied duration[3] of slightly more than 1 year. In other words, a little over a year is required to reach a TVPI of 1.35x with a rate of return of 33%. Looking at it another way, the rate of return of 33% compounded over three years (the life of this fund so far) would lead to a TVPI of 2.4x, much more than the reported 1.35x. For a fund with 3 years of existence (vintage 2018), the implied duration of slightly more than a year suggests at least one of the following:

- the fund used a credit line;

- the fund was raised in 2018 but only started investing in 2020 in deals rapidly valued upwards;

- the fund received a large early distribution coming from either a quick exit, a dividend financed by debt, or a return of capital call inaccurately classified as a distribution

These three actions can artificially inflate the IRR, especially in the first years of a fund’s life.

Any one of these three actions can artificially inflate the IRR, especially in the first years of a fund’s life. Knowing that TVPI and IRR are usually considered together (with equal weight) in the construction of default quartile benchmarks in PE performance databases, an artificially inflated IRR can materially reduce the relevance of a given benchmark. Worse, if a fund only reports its IRR (and no TVPI), some databases will solely consider such IRR (with double weight) in their default quartile benchmarks, making the benchmarking exercise even less accurate.

The combination of TVPI and IRR does not tell the full story.

Thus, without further information, the combination of TVPI and IRR does not tell the full story and sometimes, simply does not make mathematical sense.

The Distorting Effect of Credit Lines

Credit lines were initially introduced to simplify the cash flow management of PE funds. A credit line allows new portfolio acquisitions to be closed and/or fund expenses to be paid without the need to issue multiple capital calls to investors upfront. This feature of “grouping” capital calls is generally appreciated by investors as it simplifies their operational burden. Propelled by the low interest rate environment post-Global Financial Crisis, PE managers have been incentivised to maximise credit line usage.

TVPI and IRR can be astronomical.

In our study, we came across a wide range of PE managers having issued very few capital calls in the first 18–24 months following the first closing of their funds, while reporting an ever-increasing NAV. Most probably, these managers finance their first acquisitions with credit lines rather than with capital from their investors. In such cases, TVPI and IRR can be astronomical. This is because, if unrealised gains exceed the cost of the credit line and limited investors’ capital has been drawn down, net gains have been generated using next to no capital. Hence, funds using large and long dated credit lines generate very different performance compared to funds not using credit lines, especially during the early years of their life. Obviously, credit line usage is not reported and the associated risk cannot be assessed: the default risk increases with credit line usage, as credit line providers are typically more senior than fund investors with respect to first recourse on distributions. In an ideal world, details on credit lines should be available in PE performance databases, in order for investors to make performance metrics more comparable.

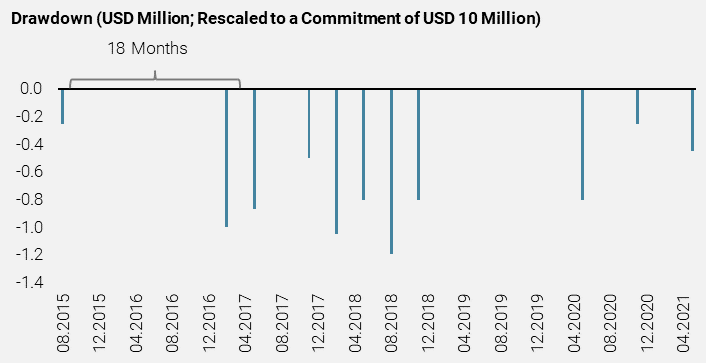

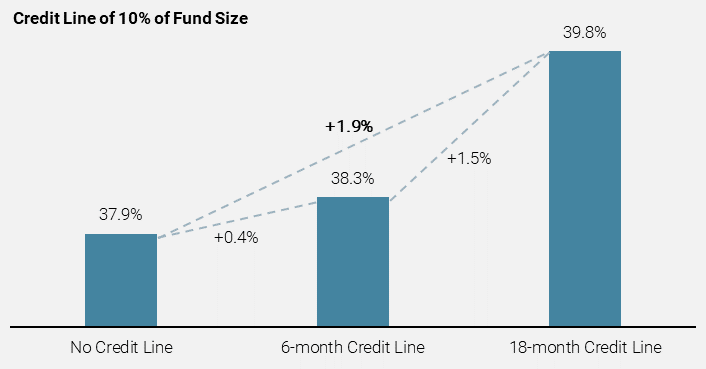

In Figure 4, we show the cash flows of Fund Y, a 2015 vintage fund (intentionally kept anonymous), as reported in Database X as at May 2022. In Figure 5, we analyse the impact of a credit line of only 10% of fund size on the IRR of Fund Y, in three scenarios: i) no credit line, ii) 6-month credit line and iii) 18-month credit line. It appears that using an 18-month credit line improves the fund IRR by 1.9% as compared to using no credit line.

Using an 18-month credit line of only 10% of fund size improves the IRR by 1.9%.

IRR is therefore very sensitive to the use of a credit line. Hence, PE managers who are predominantly benchmarked on IRR are incentivised to use credit lines to optimise IRR, rather than relying on the merits of “old fashioned” portfolio performance.

Figure 4: Cash Flows of Fund Y – Aug 2015 to Sep 2021

Source: Unigestion and Database X, as at 13.05.2022.

Figure 5: Impact of Credit Line Maturity on IRR of Fund Y (vintage 2015)

Source: Unigestion and Database X, as at 13.05.2022.

The Distorting Effect of Recycling Distributions

“A relevant indicator of reinvestment level is the Distributed to Paid-In (DPI) ratio.

Another point to consider when analysing a fund TVPI is the reinvestment level, also known as the recycling level. This mechanism enables PE managers to reinvest all or part of the distribution proceeds received during the fund investment period into new investments, in lieu of having to call additional capital from investors. These reinvestments will likely produce gains and thus boost the TVPI by increasing the numerator (Total Value) while keeping the denominator (Paid-In) unchanged. It is difficult to judge the extent to which a fund has recycled capital without comparing the fund size to the total amount invested in underlying portfolio companies. This information is unfortunately not easily available. However, a relevant indicator of reinvestment level is the Distributed to Paid-In (DPI) ratio. If the DPI of a fund remains low after 4-5 years of fund existence, it is likely that the fund manager reinvested rather than distributed proceeds to investors.

The Importance of Taking PIC into Account

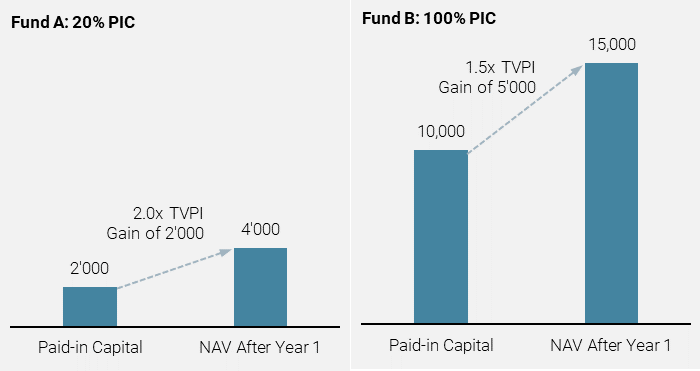

A TVPI provides more information on the performance of a PE fund than an IRR, provided it is associated with the level of paid-in capital (PIC)

From our point of view, a TVPI provides more information on the performance of a PE fund than an IRR, provided it is associated with the level of Paid-In Capital (PIC) from investors relative to commitment. On a standalone basis, a TVPI of 2.0x does not provide sufficient information about the return of a PE fund from an investor standpoint. However, combining TVPI with PIC provides a clearer picture of performance in terms of absolute gain, as illustrated in Figure 6.

Figure 6: Absolute Gain for a USD 10 Million Commitment

Source: Unigestion, based on a commitment of USD 10 million for both Fund A and Fund B.

In Figure 6, we highlight the relationship between TVPI and PIC, and the associated gain. By benchmarking on TVPI (as well as on IRR), Fund A beats Fund B hands down. However, when accounting for PIC and the related absolute gain, Fund B looks much more attractive. An investor should therefore prefer Fund B, if it aims at maximising return on committed capital.

An accurate benchmarking should at least consider the following metrics: TVPI, IRR, DPI and PIC

In summary, an accurate benchmarking should at least consider the following metrics: TVPI, IRR, DPI and PIC. Adding DPI and PIC is crucial to understand the potential usage of credit lines and reinvestment level. PIC also provides information on whether a fund called capital in an efficient manner. A fund which has for example called only 60-70% of committed capital after 10 years of existence would not optimally use the capital of its investors. Indeed, the investors would have likely recorded the entire committed amount as a liability and they would have likely paid management fees on the entire committed amount, not just on what was called. Finally, DPI also provides important information on how much “locked-in” value is contained within the TVPI.

Recommendations

- Consider all performance metrics available: TVPI, IRR, DPI and PIC.

- Calculate absolute gains to remove the distorting effect of credit lines on TVPI.

- Identify the amount of recycled distributions and adjust the TVPI accordingly to remove the distorting effect of recycling distributions.

- Complement performance benchmarking by considering a range of factors such as team size and experience, consistency of track record over time, quality of investment process and depth of ESG approach.

Conclusion

While benchmarking is an important component in any PE due diligence and selection process, there are many caveats to consider.

First, in any benchmarking process, the constituents of peer groups should be analysed in details to verify whether such groups are constructed with relevant peers or not. In addition, investors should be aware of the methodology used to calculate quartile ranking and it should reflect the objectives of the investor.

Second, benchmarks may not be wholly representative due to i) data inconsistencies in the self-reported data, ii), data scarcity where only a small proportion of the fund universe reports performance metrics and iii) survivorship bias. Specifically, there is clear evidence that the performance metrics of the best performing funds are more diligently reported than those of worst performing funds.

Finally, TVPI and IRR, the most commonly used performance metrics, are easily distorted by the use of credit lines or the recycling of distributions proceeds. Therefore, DPI and PIC should also be considered as they provide important additional insights.

That being said, we do not mean to discard the benchmarking exercise through PE performance databases. We rather intend to raise awareness of the common pitfalls and reiterate the following in order to conduct more robust benchmarking exercises:

- At the very least, seek to identify the constituents of the peer group proposed by the database and eliminate the obvious “odd ones out”.

- Better, create your own bespoke peer group with funds that have truly comparable strategies and represent real investment alternatives for you.

- Verify that the PE managers in the peer group systematically report performance, i.e. every quarter, for all their funds (Fund I, Fund II, Fund III, etc.).

- Use reported cash flows to validate performance metrics.

- Ensure that reported performance is truly “net to investors” by cross-checking with other sources (for example quarterly reports if available).

- Aggregate and cross-check data from multiple databases.

- Consider all performance metrics available: TVPI, IRR, DPI and PIC.

- Calculate absolute gains to remove the distorting effect of credit lines on TVPI.

- Identify the amount of recycled distributions and adjust the TVPI accordingly to remove the distorting effect of recycling distributions.

- Complement performance benchmarking by considering a range of factors such as team size and experience, consistency of track record over time, quality of investment process and depth of ESG approach.

- In summary, use benchmarks responsibly!

[2] Source: Unigestion, based on data in Database X, as at May 2022.

[3] Implied duration is calculated by solving for ‘d’ where (1+IRR)d = TVPI, interpreted as the number of years over which to compound the IRR in order to reach the TVPI. For example, the implied duration of a fund valued at a TVPI of 2.25x with an IRR of 50% is 2.0 years, i.e. (1+50%)2 = 2.25.

For the Interested Reader: Academic Research on Related Topics

- Phalippou (2008): The Hazards of Using IRR to Measure Performance: The Case of Private Equity, SSRN 1111796

- Larocque, S. Shive, J. S. Stevens (2021): PE Performance and the Effects of Cash Flow Timing, SSRN 3188867

- Schillinger, R. Braun, J. Cornel (2020): Distortion or Cash Flow Management? Understanding Credit Facilities in PE Funds, SSRN 3434112

- F. Albertus, M. Denes (2020): PE Fund Debt: Capital Flows, Performance, and Agency Costs, SSRN 3410076

- Korteweg (2019): Risk Adjustment in PE Returns, Annual Review of Financial Economics

| IRR | Internal Rate of Return. The discount rate at which the present value of future cash flows of an investment equals to the cost of the investment. It is determined when the net present value of the cash outflows (the cost of the investment) and the cash inflows (returns on the investment) equal zero, with the discount rate equal to the IRR. |

| TVPI | Total Value to Paid-In. Also called investment multiple. The ratio of the current value of remaining investments within a fund, plus the total value of all distributions to date, relative to the total amount of capital paid into the fund to date. As defined in the current GIPS Standards, any recallable distributions should be included in the numerator of this ratio. Any reinvested capital (resulting from recallable distributions) should be included in the denominator. |

| PIC | Paid-In Capital. The amount of committed capital a Limited Partner has actually transferred to a fund. Also known as the cumulative takedown amount, or cumulative contributions. |

| DPI | Distributed to Paid-In. The ratio of money distributed to Limited Partners by the fund, relative to contributions. As defined in the current GIPS Standards, any recallable distributions should be included in the numerator of this ratio. Any reinvested capital (resulting from recallable distributions) should be included in the denominator. |

| FOF | Fund-of-Funds. A professionally managed intermediary vehicle where-in individual and institutional investors allocate or pool assets for subsequent commitment to PE funds. |

Source: ILPA Private Equity Glossary

Important information

Past performance is no guide to the future, the value of investments, and the income from them change frequently, may fall as well as rise, there is no guarantee that your initial investment will be returned. This document has been prepared for your information only and must not be distributed, published, reproduced or disclosed by recipients to any other person. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation.

This is a promotional statement of our investment philosophy and services only in relation to the subject matter of this presentation. It constitutes neither investment advice nor recommendation. This document represents no offer, solicitation or suggestion of suitability to subscribe in the investment vehicles to which it refers. Any such offer to sell or solicitation of an offer to purchase shall be made only by formal offering documents, which include, among others, a confidential offering memorandum, limited partnership agreement (if applicable), investment management agreement (if applicable), operating agreement (if applicable), and related subscription documents (if applicable). Please contact your professional adviser/consultant before making an investment decision.

Where possible we aim to disclose the material risks pertinent to this document, and as such these should be noted on the individual document pages. The views expressed in this document do not purport to be a complete description of the securities, markets and developments referred to in it. Reference to specific securities should not be considered a recommendation to buy or sell. Unigestion maintains the right to delete or modify information without prior notice. Unigestion has the ability in its sole discretion to change the strategies described herein.

Investors shall conduct their own analysis of the risks (including any legal, regulatory, tax or other consequences) associated with an investment and should seek independent professional advice. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment. These are not suitable for all types of investors.

To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks. Actual results could differ materially from those in the forward-looking statements. As such, forward looking statements should not be relied upon for future returns. Targeted returns reflect subjective determinations by Unigestion based on a variety of factors, including, among others, internal modeling, investment strategy, prior performance of similar products (if any), volatility measures, risk tolerance and market conditions. Targeted returns are not intended to be actual performance and should not be relied upon as an indication of actual or future performance.

No separate verification has been made as to the accuracy or completeness of the information herein. Data and graphical information herein are for information only and may have been derived from third party sources. Unigestion takes reasonable steps to verify, but does not guarantee, the accuracy and completeness of information from third party sources. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. All information provided here is subject to change without notice. It should only be considered current as of the date of publication without regard to the date on which you may access the information. Rates of exchange may cause the value of investments to go up or down. An investment with Unigestion, like all investments, contains risks, including total loss for the investor.

Legal Entities Disseminating This Document

UNITED KINGDOM

This material is disseminated in the United Kingdom by Unigestion (UK) Ltd., which is authorized and regulated by the Financial Conduct Authority („FCA“). This information is intended only for professional clients and eligible counterparties, as defined in MiFID directive and has therefore not been adapted to retail clients.

UNITED STATES

This material is disseminated in the U.S. by Unigestion (UK) Ltd., which is registered as an investment adviser with the U.S. Securities and Exchange Commission (“SEC”). This information is intended only for institutional clients and qualified purchasers as defined by the SEC and has therefore not been adapted to retail clients.

EUROPEAN UNION

This material is disseminated in the European Union by Unigestion Asset Management (France) SA which is authorized and regulated by the French “Autorité des Marchés Financiers” („AMF“).

This information is intended only for professional clients and eligible counterparties, as defined in the MiFID directive and has therefore not been adapted to retail clients.

CANADA

This material is disseminated in Canada by Unigestion Asset Management (Canada) Inc. which is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario, Quebec and Newfoundland & Labrador. Its principal regulator is the Ontario Securities Commission („OSC“). This material may also be distributed by Unigestion SA which has an international advisor exemption in Quebec, Saskatchewan and Ontario. Unigestion SA’s assets are situated outside of Canada and, as such, there may be difficulty enforcing legal rights against it.

SWITZERLAND

This material is disseminated in Switzerland by Unigestion SA which is authorized and regulated by the Swiss Financial Market Supervisory Authority („FINMA“).

Document issued September 2022.