The Upside of a Downturn – Secondaries in 2023

Head of Investment Solutions, Private Equity

Partner, Private Equity

Key Points

- Current market uncertainty and reduced liquidity in the PE market will lead to a rapid growth in secondary supply in 2023

- We expect PE valuations to decline in the coming quarters, in some areas more than others, leading to attractive secondary buying opportunities

- For Unigestion, the key areas of interest will be LP stakes in mid-market funds, venture/growth portfolios, single asset continuation deals and the comeback of multi-asset continuation deals

Overview

After arguably the longest running bull market in history, punctuated only by a brief Covid-induced correction, we are now entering a new era of great uncertainty. The frothiness of 2021 seems a lifetime ago. Private equity markets show signs of weakening across most metrics, faced with the triple challenge of a difficult macro environment, global geopolitical unrest, and a steep fall in public markets. There has been an immediate impact on capital raising, with fewer funds raised in the first half of 2022 than in any six-month period since 2013. But we have faced similar situations in the past and while there is a lot of uncertainty for investors, there will also be new opportunities. The secondary market is known to benefit from market dislocation and may be well positioned to emerge as a winner.

Secondary Market Dynamics

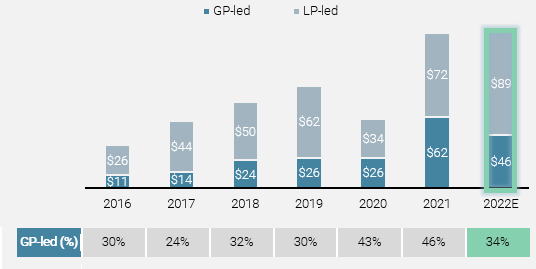

There is nothing like a downturn to generate attractive secondaries opportunities. Or so the conventional wisdom goes. And in fact, the picture for the secondary market looks rather more positive than the private equity picture overall. Based on market data from Greenhill, H1 2022 was a record-setting period, with transaction volume setting a new record (USD 58bn) and full year numbers expected to approximately match or even exceed last year’s (USD 130bn -140bn). While the result of this high level of investment activity has been a slight dip in capital overhang, current and projected secondary fundraising is expected to remain strong, reflecting positive sentiment on both expected LP demand as well as the expectation of attractive investment opportunities. Even if volumes do come in a bit lower than in 2021, this will likely be due to processes being held back in the current environment which then could lead to a rebound in H1 2023. The secondary market still represents only a fraction (10 – 20%) of the overall private equity market in volume and has substantial room for growth.

* Actual data until 30.06.22; full year estimate by Unigestion

Source: Greenhill, as at August 2022.

One interesting observation in 2022 has been the slight decline of GP-led deals and the re-emergence of LP portfolio sales. Where GP-leds made up a record 46% of transaction volume in 2021, the expected 2022 level of 34% looks more in line with what we saw back in 2018/19, implying a shift back to more traditional LP stake secondary deals. There is no doubt some investors are under pressure to rebalance their portfolios away from private equity due to the fall in value of their public market asset holdings (the “denominator effect”), liquidity issues caused by the decline in exit activity, or simply wanting to free up capacity in order to support their core private equity relationships that are in fundraising. That being said, we have not yet seen big volumes, in part because liquidity pressure is still moderate and rebalancing will not be done at any price. But if LPs need liquidity, one of their only remedies is to seek solace in the secondary market, which could be a strong source of deal flow in the year to come.

And what about secondary pricing? The biggest hit was experienced by Venture and Growth funds where we see discounts of about 35 – 45% on average. The Buyout space has held up well to date, although it is also declining this year; with average discounts currently around 10 – 25%. Large buyouts account for most of this decline.

The Elephant in the Room: Private Equity Valuations

However, the major sticking point for secondary buyers, and most investors for that matter, is the credibility of private equity valuations. While public markets have fallen by roughly 20% in H1 2022, many private equity firms have reported at least flat performance, especially small and mid-market managers. This has been driven mainly by exits at higher multiples, with the valuations of unrealised companies remaining largely unchanged. At the other end of the spectrum, the large and mega funds seem to have reached their peak, with the first markdowns coming through, although these are still far from the falls observed on the public markets. This obvious disconnect between public and private valuations is causing headaches for LPs and creates uncertainty around whether – and by how much – private valuations will eventually fall. In the meantime, these assets are growing in proportion to their overall portfolios, further increasing scrutiny and leaving some LPs uncomfortable with their illiquid assets.

For the secondary market this has implications – especially for supply – with some LPs currently reluctant to sell with headline discounts that need to be explained. While Q3 valuations look to be broadly flat, Q4 may see some downward revisions as portfolio companies start to feel the pinch of higher costs, higher energy prices, and higher interest rates. The extent and timing of these downward adjustments will vary substantially, but we expect the worst hit areas to be venture capital, growth capital, large buyouts, and more cyclical sectors. Meanwhile, mid-market buyouts and non-cyclical sectors such as healthcare and technology may be impacted less based on observations from previous crises – thanks in large part to private equity’s inherently more stable focus on long term growth. For secondaries investors, this will be an interesting space to watch.

Is It Time for Secondaries Yet?

One thing is certain – the secondary market has been excellent at adapting to changing conditions. Not so long ago secondaries were a rare event, undertaken mainly when an LP was in extreme distress and were generally dealt with in private. Fast forward to today, secondaries are a standard part of the portfolio management toolbox. Moreover, compared to the origins of the market when the focus was on discounted LP stakes, today there are many types of secondary transactions that are adapted to every environment. In short, it’s always time for secondaries.

That being said, where do we think the most attractive secondaries opportunities will be in the coming 12 to 18 months?

High quality LP stakes in mid-market portfolios. So far, LPs have been unwilling to sell their interests in funds at material discounts to NAV. However, as NAVs of certain portfolios fall and LPs become even more motivated to sell, the bid-ask spread between buyers and sellers will narrow. For secondaries investors the fundamentals of portfolio companies in the best mid-market funds will remain the same, despite falling valuations: resilient business models, low leverage, leaders in niche spaces, robust cash flows, etc. This is particularly relevant for investors like Unigestion given our focus on mature LP stakes of specialist managers with high quality assets, as opposed to tail end offerings. Currently, demand is still driven mainly by portfolio rebalancing rather than imminent cash needs. This provides attractive opportunities for the use of structures such as deferred payments of up to 12 to 18 months so that the seller does not have to show too large a valuation hit on their portfolio.

Case study – Project Dee

Region: Europe

Transaction: Two profitable, fast-growing assets acquired at attractive valuations

Angle: Known GP and access through Unigestion’s emerging manager platform

- Deal type: Concentrated “inflexion” LP stake (portfolio of 2 companies)

- Investment theme: Service Efficiency

- Access: Club Deal

- Status: Fully derisked after one year

Source: Unigestion as at November 2022.

Venture / Growth Capital portfolios. The sky high tech valuations of 2021 are a distant memory. It is clear that many venture-capital backed companies will now need to undertake financing rounds at much lower valuations. Many others will go out of business. Investors who came into venture capital funds at the peak of the market will now be regretting it and will be seeking a swift exit. For certain savvy secondaries investors this will create attractive opportunities – who will be able to buy heavily discounted stakes in otherwise solid portfolios or by providing later stage funding, through sidecar funds for example, to the best companies at much lower valuations.

Single asset continuation funds. If the market does swing back to LP stakes, many are predicting the demise of single asset continuation funds. However, GPs have seen how effective these are – allowing them to continue backing their best performing portfolio companies. As the exit markets close, GPs will prefer going down the single asset continuation fund route in order to increase liquidity for investors. In addition, less attractive debt markets mean change of control clauses that trigger restructuring of the leverage package will become a risk to be avoided. For us, this provides access to market-leading companies in defensive sectors with increasingly attractive valuations and increasingly discounts as opposed to par pricing over the past few years. Further attractive risk mitigating features are: a company that the GP knows well, tangible and credible value creation plans and, strong alignment.

Case study – Project Recycling

Region: USA

Transaction: Rapidly growing solid waste hauling and processing company in southern Florida

Angle: Accessing a strong platform poised for growth through M&A

- Deal type: Single asset restructuring

- Investment theme: Circular Economy

- Access: Club Deal

- Status: After 18 months, buy and build plan executed and ready to be sold

Source: Unigestion as at November 2022.

The comeback of multi-asset continuation funds and complex GP-led transactions. These original “GP-led” deals were usurped by single asset continuation funds over the past two years as GPs opted for the more selective approach. Specifically, secondaries investors today are more critical about valuation, the reason for doing the deal in the first place and alignment. Indeed, we are not only seeing attractive discounts on high quality companies, but are also able to negotiate strong alignment features such as higher carried interest hurdles, stricter adherence to liquidity timing and active board seats for us as the lead investor. However, given the combination of the lower liquidity environment and the general oversupply of secondary opportunities, GPs will be more likely to package together their best performing companies with different liquidity profiles in order to attract secondary investors.

Case study – Project Woof

Region: Europe

Transaction: Three attractive buy and build opportunities in the Nordics

Angle: Providing a liquidity solution for the GP’s non-institutional investors

- Deal type: Complex fund restructuring

- Investment theme: Service Efficiency

- Access: Club Deal – Unigestion as lead investor

- Status: All companies fully exited within 4 year at strong multiples

Source: Unigestion as at November 2022.

Additional opportunities, such as direct secondaries and tender offers. The increased need for liquidity or for additional capital to support further value creation means that we continue to see a strong flow of direct secondaries, which involves buying directly held ownership in privately held companies. The current market environment provides plenty of good opportunities for consolidation via ‘buy and build’ and ‘merger’ strategies, fuelled by correcting valuations. We are able to source these proprietary, off-market transactions through the broader Unigestion platform. These deals often have no or very attractive fees and economics, providing an additional driver of performance. Tender offers are another area where we expect to see strong deal flow in 2023. This is when GPs initiate the sale of several fund interests by existing LPs to secondary investors (therefore part of the GP-led category).

Building a Balanced Portfolio

The secondary market has come a long way from its origins in the 1980s. With the move from a market based predominantly on LP stakes to the diverse secondary strategies available today, there have also been subtle changes to the strategies of secondary investors and the role they play in the private equity ecosystem. Different secondary strategies, varying from LP stake deals targeting quick exits and high IRRs or on single asset deals with tangible value creation plans and a high target TVPI but with a longer duration, can lead to significant differences in the risk and return profile. At Unigestion we aim to build a balanced portfolio targeting a diversified cash flow profile in line with what investors expect from secondaries, while at the same time maintaining a strong focus on optimised TVPI and a low total expense ratio.

Back to Basics

For investors, it is more important than ever to consider the basic fundamentals when assessing new investments: resilient business models, strong balance sheets, and multiple value creation levers. We have been successfully investing in secondaries for over two decades, with some of our best deals having been completed during difficult economic periods. However, irrespective of macro conditions, the key features of our secondaries strategy have remained constant over time:

- Targeting concentrated portfolios of high quality, mid-market companies,

- Seeking returns driven by growth rather than leverage, and

- Demanding downside protection in every deal.

While there may not be many positive aspects of an economic downturn, new and attractive opportunities created for sophisticated secondaries investors may indeed be the silver lining.

Important Information

Past performance is no guide to the future, the value of investments, and the income from them change frequently, may fall as well as rise, there is no guarantee that your initial investment will be returned. This document has been prepared for your information only and must not be distributed, published, reproduced or disclosed (in whole or in part) by recipients to any other person without the prior written consent of Unigestion. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation.

This is a promotional statement of our investment philosophy and services only in relation to the subject matter of this presentation. It constitutes neither investment advice nor recommendation. This document represents no offer, solicitation or suggestion of suitability to subscribe in either the investment vehicles to which it refers or to any securities or financial instruments described herein. Any such offer to sell or solicitation of an offer to purchase shall be made only by formal offering documents, which include, among others, a confidential offering memorandum, limited partnership agreement (if applicable), investment management agreement (if applicable), operating agreement (if applicable), and related subscription documents (if applicable). Such documentation contains additional information material to any decision to invest. Please contact your professional adviser/consultant before making an investment decision.

Where possible we aim to disclose the material risks pertinent to this document. The views expressed in this document do not purport to be a complete description of the securities, markets and developments referred to in it. Reference to specific securities should not be considered a recommendation to buy or sell. Unigestion maintains the right to delete or modify information without prior notice.

Investors shall conduct their own analysis of the risks (including any legal, regulatory, tax or other consequences) associated with an investment and should seek independent professional advice. Some of the investment strategies or financial instruments described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment. These are not suitable for all types of investors. Unigestion has the ability in its sole discretion to change the strategies described herein.

To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks. Actual results could differ materially from those in the forward-looking statements. As such, forward looking statements should not be relied upon for future returns. Targeted returns reflect subjective determinations by Unigestion based on a variety of factors, including, among others, internal modeling, investment strategy, prior performance of similar products (if any), volatility measures, risk tolerance and market conditions. Targeted returns are not intended to be actual performance and should not be relied upon as an indication of actual or future performance.

Information about any indices shown herein is provided to allow for comparison of the performance of the strategy to that of certain well-known and widely recognized indices. There is no representation that such index is an appropriate benchmark for such comparison. You cannot invest directly in an index and the indices represented do not take into account trading commissions and/or other brokerage or custodial costs. The volatility of the indices may be materially different from that of the strategy. In addition, the strategy’s holdings may differ substantially from the securities that comprise the indices shown.

No separate verification has been made as to the accuracy or completeness of the information herein. Data and graphical information herein are for information only and may have been derived from third party sources. Unigestion takes reasonable steps to verify, but does not guarantee, the accuracy and completeness of information from third party sources. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. All information provided here is subject to change without notice. It should only be considered current as of the date of publication without regard to the date on which you may access the information. Rates of exchange may cause the value of investments to go up or down. An investment with Unigestion, like all investments, contains risks, including total loss for the investor.

Unigestion Secondary VI (USec VI) will be created as a SCS-SICAV-RAIF in Luxembourg and will qualify as an Alternative Investment Fund (AIF) within the meaning of the law dated 12 July 2013 on Alternative Investment Fund Managers implementing the Directive 2011/61/EU (AIFMD). As a result, units of this vehicle may be offered only to professional investors and may not be distributed on a public basis in or from any country where such distribution would be prohibited by law. This document contains a preliminary summary of the purpose and principal business terms of an investment in Unigestion Secondary VI. This summary does not purport to be complete and is qualified in its entirety by reference to the more detailed discussion to take place with the AIF. Unigestion Secondary VI will have the ability in its sole discretion to change the strategies described herein. Before making a decision to invest in Unigestion Secondary VI, you are advised to consult with your tax, legal and financial advisors.

Additional Information for U.S. Investors

The performance figures are based on estimated fees and expenses as well as on the underlying strategy’s estimated performances given by fund managers, administrators, custodians and third party sources at a given date. Where performance is reflected gross of fees, potential investors should be aware that the inclusion of fees, costs and charges will reduce the overall value of performance. Unless otherwise stated, the performance data source are Unigestion, Bloomberg and Compustat.

This information is provided to you solely to give you background information relating to Unigestion, certain strategies it implements and currently offers. Before making an investment decision with respect to the strategy discussed herein, potential investors are advised to consult with their tax, legal, ERISA and financial advisors. Note that not all strategies may be available or suitable for investment by U.S. investors.

This document may contain forward-looking statements, including observations about markets and industry and regulatory trends as of the original date of this document. Forward-looking statements may be identified by, among other things, the use of words such as “expects,” “anticipates,” “believes,” or “estimates,” or the negatives of these terms, and similar expressions. Forward-looking statements reflect Unigestion’s views as of such date with respect to possible future events. Actual results could differ materially from those in the forward-looking statements as a result of factors beyond a strategy’s or Unigestion’s control. Readers are cautioned not to place undue reliance on such statements. No party has an obligation to update any of the forward-looking statements in this document

Return targets or objectives, if any, are used for measurement or comparison purposes and only as a guideline for prospective investors to evaluate a particular investment program’s investment strategies and accompanying information. Performance may fluctuate, especially over short periods. Targeted returns should be evaluated over the time period indicated and not over shorter periods.

The past performance of Unigestion, its principals, shareholders, or employees is not indicative of future returns.

Except where otherwise specifically noted, the information contained herein, including performance data and assets under management, relates to the entire affiliated group of Unigestion entities over time including that of Unigestion UK and Unigestion US. Such information is intended to provide the reader with background regarding the services, investment strategies and personnel of the Unigestion entities. No guarantee is made that all or any of the individuals involved in generating the performance on behalf the other Unigestion entities will be involved in managing any client account on behalf of Unigestion UK There is no guarantee that Unigestion will be successful in achieving any investment objectives. An investment strategy contains risks, including the risk of complete loss.

The risk management practices and methods described herein are for illustrative purposes only and are subject to modification.

Legal Entities Disseminating This Document

UNITED KINGDOM

This material is disseminated in the United Kingdom by Unigestion (UK) Ltd., which is authorized and regulated by the Financial Conduct Authority („FCA“). This information is intended only for professional clients and eligible counterparties, as defined in MiFID directive and has therefore not been adapted to retail clients.

UNITED STATES

In the United States, Unigestion is present and offers its services in the United States as Unigestion (US) Ltd, which is registered as an investment advisor with the U.S. Securities and Exchange Commission (“SEC”) and/or as Unigestion (UK) Ltd., which is registered as an investment advisor with the SEC. All inquiries from investors present in the United States should be directed to clients@unigestion.com. This information is intended only for institutional clients that are qualified purchasers as defined by the SEC and has therefore not been adapted to retail clients.

EUROPEAN UNION

This material is disseminated in the European Union by Unigestion Asset Management (France) SA which is authorized and regulated by the French “Autorité des Marchés Financiers” („AMF“). This information is intended only for professional clients and eligible counterparties, as defined in the MiFID directive and has therefore not been adapted to retail clients.

CANADA

This material is disseminated in Canada by Unigestion Asset Management (Canada) Inc. which is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario, Quebec and Newfoundland & Labrador. Its principal regulator is the Ontario Securities Commission („OSC“). This material may also be distributed by Unigestion SA which has an international advisor exemption in Quebec, Saskatchewan and Ontario. Unigestion SA’s assets are situated outside of Canada and, as such, there may be difficulty enforcing legal rights against it.

SWITZERLAND

This material is disseminated in Switzerland by Unigestion SA which is authorized and regulated by the Swiss Financial Market Supervisory Authority („FINMA“).

Document issued December 2022.