Unigestion Classic Strategic: A Macro Risk-Based Approach To Building A Balanced Portfolio

- While traditional balanced funds have performed well in the past, episodes of market stress have highlighted their shortcomings.

- Risk parity portfolios go some way to addressing these issues, but they are not without their own problems

- A macro risk-based approach can help deliver a more robust strategic allocation that can generate stronger performance over the long-term.

- 2021 gave investors a glimpse of how an inflationary environment can degrade the value of traditional balanced portfolios. Against this backdrop, the Unigestion Classic Strategic 15 strategy demonstrated its ability to perform well in varying market environments.

- Q1 2022 has been challenging for nearly all assets, but the diversification across macro regimes has aided the strategy in limiting the downside and outperforming other balanced portfolios.

Introduction

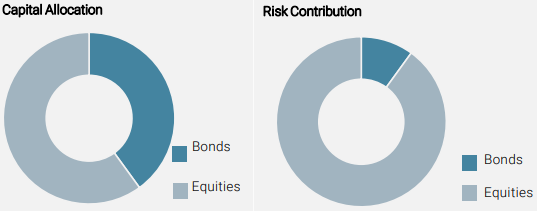

Traditional balanced portfolios, such as the 60/40 portfolio (60% of capital in equity markets, 40% in bonds), have performed well over the past decades. However, several market crashes have highlighted serious shortcomings of this approach. A simple risk analysis reveals that these allocations are extremely concentrated in equity risk despite the large capital allocation to bonds (see Figure 1). In other words, as long as world economies are growing steadily with little inflationary pressures, the 60/40 portfolio should continue to perform well. Unfortunately, large losses can be expected in other scenarios.

Figure 1: Capital vs Risk for a 60/40 Portfolio

Source: Unigestion. As at 31 August 2021.

The insight that these expectedly balanced portfolios are disproportionally geared toward growth assets (namely equities) led to the rise of risk parity allocations. In a nutshell, risk parity aims to balance the allocation of risk, as opposed to capital, across asset classes constituting the portfolio, usually mixing growth assets (equities, credit spreads), recession hedges (government bonds), and inflation hedges (commodities, linkers). Thus, adequately sized exposures should reap diversification benefits and deliver better risk-adjusted returns. They also tend to have a very large proportion of their capital invested in government bonds, as shown by the allocation of the S&P Risk Parity 15 index in Figure 2. This has proven to be a significant tailwind in the context of the secular decline in bond yields, but could present a major headwind going forward.

Figure 2: Capital Allocation for Unigestion Classic Strategic, S&P Risk Parity 15, and 60/40

* 60/40 scaled by 1.6x to achieve a long-term volatility of 15% p.a.

Source: S&P Global, Unigestion. As at 31 August 2021

Our macro risk-based approach is based on the tenet that macro regimes drive asset returns and that one should allocate risk to them in proportion to their likelihood

Our Macro Risk-Based Approach to Strategic Asset Allocation

We believe that both the traditional balanced and risk parity approaches have their merits but can be improved upon. The central principle of risk parity – allocate risk, not capital – is a sound one in terms of portfolio construction and risk management. The implicit recognition of the 60/40 portfolio that the business cycle tends to have more periods of growth than shocks is also valid.

Our view is that the path to a robust strategic allocation that performs over the long-term is through an understanding of macroeconomic regimes and their prevalence, and to reflect this in terms of portfolio construction. We refer to this approach as “macro risk-based”: it is grounded in the tenet that macro regimes drive asset returns and that one should allocate risk to them in proportion to their likelihood.

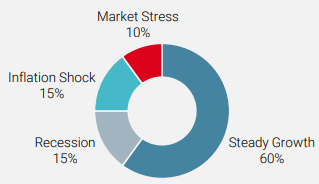

Our framework for macro regimes consists of four components:

- Steady Growth: economies are growing steadily, with little inflationary pressures;

- Recession: contraction in economic activity;

- Inflation Shock: prices in the real economy rise much higher than expected; and

- Market Stress: market turmoil not linked to the real economy.

A rigorous analysis of business cycles using a host of different indicators over the last five decades and across different economies leads to very striking results: the frequency of these four regimes is quite consistent across time and regions. Figure 3 presents our expectations for the long-term frequencies of each of these regimes based on this analysis.

Figure 3: Expected Frequency of Macro Regimes – Global Economy

Source: Bloomberg, OECD, Unigestion. Data As at 31 August 2021.

We note that this insight is conceptually akin to the implicit assumption of the 60/40 portfolio: 60% of the time, economies are growing in a healthy manner while they experience some sort of shock the remaining 40% of the time. Importantly, this result was not the goal of the analysis but rather an outcome that is largely consistent across economies.

As investors, we aim to sublimate our insights into an investable portfolio, proceeding in two key steps:

- Constructing four investable baskets of assets corresponding to each regime. These baskets provide an exposure to precisely those risk premia that are expected to perform well (i.e., consistently positive risk-adjusted returns) in the corresponding macro regime.

- Allocating risk to the four baskets in line with their long-term frequency (as shown in Figure 3).

The resulting allocation represents our macro risk-based portfolio (Figure 4).

Figure 4: From Macro Regimes and Risk Premia to a Macro Risk-Based Portfolio

Source: Unigestion. Data As at 31 August 2021.

At Unigestion, we have translated the four macro regimes into investable baskets to deliver a macro risk-based portfolio

This type of approach also lends itself well to customisation (e.g. investors willing to have a tilt towards one regime or another) and to the inclusion (or removal) of new assets or risk premia to the investment universe. For example, we have recently included an allocation to carbon markets as part of cyclical commodities in order to accrue diversification and gain the added benefit of an ESG tilt to the portfolio. More details can be found in our recent white paper on the topic: Responsible Commodities Investing – Assessing the Options. Finally, the overall level of risk can be tailored to an investor’s objectives via the use of cash-efficient derivative contracts, readily leveraging the portfolio as needed.

A macro risk-based approach easily lends itself to customisation with the inclusion/exclusion of certain risk premia.

Case Study: Performance Over the Last 12 Months

A theory for portfolio construction is only as good as the performance it can provide to investors. While we have previously written about the expected return profile of our approach1, market action from the past 12 months provides an interesting case study to assess the behaviour of our macro risk-based approach.

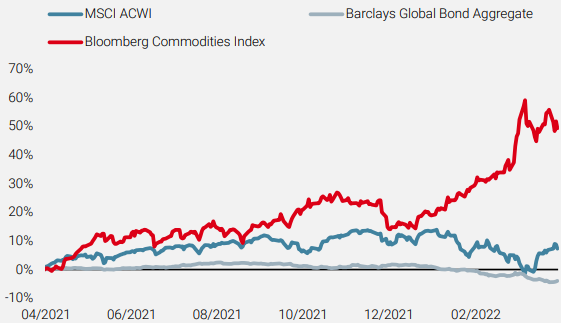

Overall, 2021 saw both equity and commodity markets rise significantly, helped by the reopening of world economies following the Covid-19 pandemic, and in a context where high demand was met with supply chain disruptions. Both asset classes delivered double-digit returns. Bonds’ performance was overall muted, but with a clear downtrend from late summer, as monetary policy expectations began to shift. They ended up delivering their first annual negative return since 2013, and their worst one since 1994.

So far, 2022 has seen a global reckoning of inflation, with households adjusting their spending, corporations contending with higher labour and input costs, and central bankers (in particular the Fed) taking the fight to inflation. Commodity prices have continued to rise strongly due to the Russian invasion of Ukraine and Covid lockdowns in China disrupting supply chains further. Market sentiment has shifted to strongly bearish, with higher market volatility, drying liquidity, and widening spreads. While uncertainty dominated the first quarter of the year, one thing was clear: the era of easy money is coming to an end. This environment was very challenging for traditional asset classes. The Barclays Global Aggregate index suffered its largest drawdown since its inception in 1989, ending the quarter down 5%. Equity markets tumbled, losing as much as 12% in 2022 at the beginning of March, before recovering and ending the quarter down 5%. Finally, commodities skyrocketed, and their prices increased by 25% over the quarter, leading investors to wonder whether inflationary pressures could lead to another global recession.

Figure 5: Last 12 month Cumulative Returns of Major Asset Classes

Source: Bloomberg, Unigestion. Data in USD, from 31 March 2021 to 31 March 2022

The overall market context combined two quite distinct periods: one of relative calm, where traditional beta performed well, and one of high market stress where many markets experienced exceptional gains or losses.

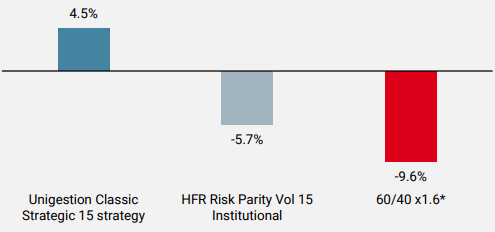

In this ever-changing environment, the Unigestion Classic Strategic strategy – our macro risk-based approach applied to a universe of traditional risk premia, namely duration, inflation, credit, equities, and commodities – behaved as expected: it delivered high returns during good times, while limiting the downside during more difficult periods thanks to diversification across macro regimes as well as assets. As of the end of April 2022, its trailing 12-month performance stood at +4.5% (net of fees). On a relative basis, this performance has outstripped that of both global equities and bonds, along with prototypical 60/40 and risk parity portfolios as proxied by the HFR Risk Parity Vol 15 Institutional index (see Figure 6). Both these benchmarks have actually delivered negative returns over the period.

Figure 6: Trailing 12m Cumulative Performance

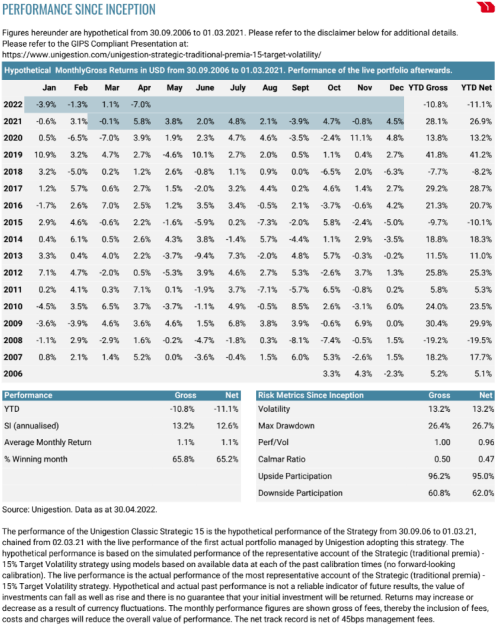

*60/40 scaled by 1.6x to achieve a long term volatility of 15% p.a.. Performance expressed net of fees, in USD. Please refer to the GIPS compliant presentation at: /unigestion-strategic-traditional-premia-15-target-volatility

Source: Bloomberg, Unigestion. Data as at 30 April 2022

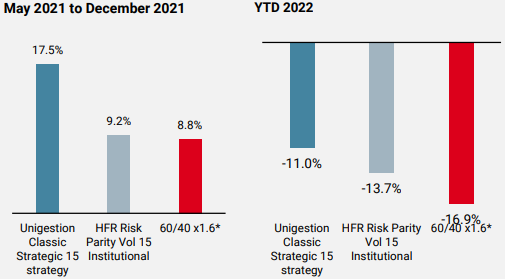

Breaking down the trailing 12 months into the two sub-periods discussed above – relative calm (May – December 2021) and high market stress (YTD 2022) – leads to a few interesting observations, as shown in Figure 7. The Unigestion Classic Strategic strategy delivered almost twice the performance of either the HFR index or the scaled 60/40 portfolio during the former period. In 2022, although the performance of our strategy was negative, it clearly beat the two benchmarks, while capturing less than two thirds of the scaled 60/40 portfolio’s losses. This illustrates how a well-diversified and well-balanced portfolio can achieve better asymmetry of returns than traditional balanced allocations.

Figure 7: May 2021-December 2021 and YTD 2022 performances

* 60/40 scaled by 1.6x to achieve a long-term volatility of 15% p.a. Performance expressed net of fees, in USD. Please refer to the GIPS compliant presentation at: /unigestion-strategic-traditional-premia-15-target-volatility

Source: Bloomberg, Unigestion. As at 30 April 2022.

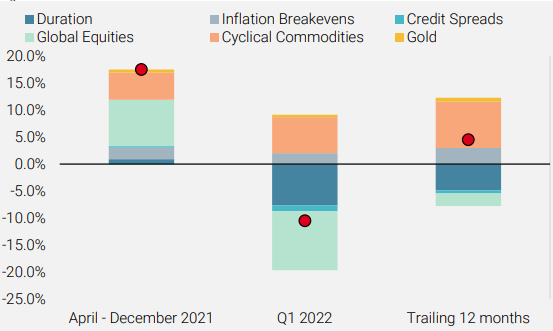

Looking underneath the top-line performance of the strategy, we see that returns from May 2021 to April 2022 came in large part from the exposure to commodities and inflation breakevens i.e. from the inflation basket (Figure 8). Exposures to duration and – to a lesser extent – to equities were negative contributors.

Figure 8: Performance Contributions

Performance expressed net of fees, in USD. Please refer to the GIPS compliant presentation at: /unigestion-strategic-traditional-premia-15-target-volatility.

Source: Bloomberg, Unigestion. As at 30 April 2022..

More interesting patterns appear when bifurcating the performance over the two periods of April – December 2021 and Q1 2022:

- In 2021, most of the gains were made in equities and in cyclical commodities, while other risk premia only contributed modestly. This is to be expected given that the environment was one of accelerating global growth with building inflationary pressures. Importantly, the exposure to duration via government bond futures was not costly.

- In 2022, exposure to both bonds and equities detracted significantly from performance. However, most of these large losses were offset by exposure to inflation-sensitive risk premia such as cyclical commodities and inflation breakevens, which benefited strongly from market participants adjusting their inflation expectations sharply higher.

The specific case of YTD 2022 very vividly highlights the importance of two main pillars of our investment process:

- Broadening exposure beyond traditional assets such as equities and bonds. Traditional balanced portfolios such as the “60/40” are particularly vulnerable to inflation environments, and their returns in 2022 clearly illustrate that.

- Implementing a macro risk-based allocation that carefully considers the probability of occurrence from different macro-economic regimes. Some of the most traditional risk parity allocations might overstate the weight of recession, leading to large, levered allocation to nominal bonds, and too little offsetting exposure to inflation assets.

Spreading risk across a wide range of risk premia and recognising the long-term patterns of the business cycle should help deliver a more robust strategic allocation over the long term

Conclusion

Multi-asset risk parity portfolios, presented as a natural evolution to address shortcomings of traditional 60/40 portfolios, have now entered the mainstream. However, this approach to strategic asset allocation may have swung the pendulum too far: if 60/40 allocations have far too high an exposure to growth, the view that all economic regimes should receive an equal amount of risk in the portfolio is not necessarily in tune with the reality of the business cycle.

Looking at data spanning several decades and multiple regions, we build a macro risk-based portfolio that we believe is more balanced across a large range of risk premia, allocating risk in line with the long-term probabilities of different macro-economic regimes. In practice, this portfolio tends to allocate more risk to growth, and slightly less to recession and inflation risk than traditional risk parity portfolios.

In 2021, the Unigestion Classic Strategic 15 strategy demonstrated its ability to perform well in different market environments, avoiding the concentration in duration risk so often noted for risk parity portfolios while still coping with more difficult periods for equity markets, in contrast to the more growth-concentrated 60/40 portfolios.

Performance over Q1 2022, while negative on an absolute basis, still demonstrates the benefits of the strategy’s diversified approach, aiding it in outperforming other balanced portfolios in a challenging environment for nearly all assets.

The strategy also showed a strong asymmetry with respect to equity markets overall: it captured 150% of their rise in 2021, while only capturing 85% of their downside on a year-to-date basis as of end of March 2022. It also delivered 150% of the performance of the HFR Risk Parity 15 index over the last 12 months.

We believe that any strategic asset allocation scheme embeds views about the business cycle. Failure to recognise this could lead to allocations that are too concentrated in specific risks and hence more dependent on one type of macro-economic regime. Spreading risk across a wide range of risk premia and recognising the long-term patterns of the business cycle as we do in the Unigestion Classic Strategic strategy should make for a much more robust strategic allocation over the long term. In particular, we believe traditional balanced portfolios – and to some extent duration-heavy traditional risk parity allocations as well – could be at risk of underperforming expectations should worldwide economies continue to experience high, sustained inflation or even stagflation, which would be particularly detrimental to both equities and bonds.

1Baig, S., Blin, O. & Teiletche, J. (2020). Building a Better Strategic Allocation: The Macro Risk Diversified Portfolio. Unigestion./new-frontiers-in-investment-research/strategic-asset-allocation/

Important information

Past performance is no guide to the future, the value of investments, and the income from them change frequently, may fall as well as rise, there is no guarantee that your initial investment will be returned. This document has been prepared for your information only and must not be distributed, published, reproduced or disclosed (in whole or in part) by recipients to any other person without the prior written consent of Unigestion. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. This is a promotional statement of our investment philosophy and services only in relation to the subject matter of this presentation. It constitutes neither investment advice nor recommendation. This document represents no offer, solicitation or suggestion of suitability to subscribe in either the investment vehicles to which it refers or to any securities or financial instruments described herein. Any such offer to sell or solicitation of an offer to purchase shall be made only by formal offering documents, which include, among others, a confidential offering memorandum, limited partnership agreement (if applicable), investment management agreement (if applicable), operating agreement (if applicable), and related subscription documents (if applicable). Such documentation contains additional information material to any decision to invest. Please contact your professional adviser/consultant before making an investment decision. Where possible we aim to disclose the material risks pertinent to this document. The views expressed in this document do not purport to be a complete description of the securities, markets and developments referred to in it. Reference to specific securities should not be considered a recommendation to buy or sell. Unigestion maintains the right to delete or modify information without prior notice. Investors shall conduct their own analysis of the risks (including any legal, regulatory, tax or other consequences) associated with an investment and should seek independent professional advice. Some of the investment strategies or financial instruments described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment. These are not suitable for all types of investors. Unigestion has the ability in its sole discretion to change the strategies described herein. To the extent that this report contains statements about the future, such statements are forward looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks. Actual results could differ materially from those in the forward-looking statements. As such, forward looking statements should not be relied upon for future returns. Targeted returns reflect subjective determinations by Unigestion based on a variety of factors, including, among others, internal modelling, investment strategy, prior performance of similar products (if any), volatility measures, risk tolerance and market conditions. Targeted returns are not intended to be actual performance and should not be relied upon as an indication of actual or future performance. No separate verification has been made as to the accuracy or completeness of the information herein. Data and graphical information herein are for information only and may have been derived from third party sources. Unigestion takes reasonable steps to verify, but does not guarantee, the accuracy and completeness of information from third party sources. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. All information provided here is subject to change without notice. It should only be considered current as of the date of publication without regard to the date on which you may access the information. Rates of exchange may cause the value of investments to go up or down. An investment with Unigestion, like all investments, contains risks, including total loss for the investor.

Additional Information for U.S. Investors

The performance figures are based on estimated fees and expenses as well as on the underlying strategy’s estimated performances given by fund managers, administrators, custodians and third party sources at a given date. Where performance is reflected gross of fees, potential investors should be aware that the inclusion of fees, costs and charges will reduce the overall value of performance. Unless otherwise stated, the performance data source are Unigestion, Bloomberg and Compustat. This information is provided to you solely to give you background information relating to Unigestion, certain strategies it implements and currently offers. Before making an investment decision with respect to the strategy discussed herein, potential investors are advised to consult with their tax, legal, ERISA and financial advisors. Note that not all strategies may be available or suitable for investment by U.S. investors. This document may contain forward-looking statements, including observations about markets and industry and regulatory trends as of the original date of this document. Forward-looking statements may be identified by, among other things, the use of words such as “expects,” “anticipates,” “believes,” or “estimates,” or the negatives of these terms, and similar expressions. Forward-looking statements reflect Unigestion’s views as of such date with respect to possible future events. Actual results could differ materially from those in the forward-looking statements as a result of factors beyond a strategy’s or Unigestion’s control. Readers are cautioned not to place undue reliance on such statements. No party has an obligation to update any of the forward-looking statements in this document Return targets or objectives, if any, are used for measurement or comparison purposes and only as a guideline for prospective investors to evaluate a particular investment program’s investment strategies and accompanying information. Performance may fluctuate, especially over short periods. Targeted returns should be evaluated over the time period indicated and not over shorter periods.

The past performance of Unigestion, its principals, shareholders, or employees is not indicative of future returns. Except where otherwise specifically noted, the information contained herein, including performance data and assets under management, relates to the entire affiliated group of Unigestion entities over time including that of Unigestion UK. Such information is intended to provide the reader with background regarding the services, investment strategies and personnel of the Unigestion entities. No guarantee is made that all or any of the individuals involved in generating the performance on behalf the other Unigestion entities will be involved in managing any client account on behalf of Unigestion U.K. More specific information regarding Unigestion UK is set forth herein where indicated and is available on request.

There is no guarantee that Unigestion will be successful in achieving any investment objectives. An investment strategy contains risks, including the risk of complete loss. The risk management practices and methods described herein are for illustrative purposes only and are subject to modification.

Legal Entities Disseminating This Document

UNITED KINGDOM

This material is disseminated in the United Kingdom by Unigestion (UK) Ltd., which is authorized and regulated by the Financial Conduct Authority („FCA“). This information is intended only for professional clients and eligible counterparties, as defined in MiFID directive and has therefore not been adapted to retail clients.

UNITED STATES

This material is disseminated in the United States by Unigestion (UK) Ltd., which is registered as an investment adviser with the United States Securities and Exchange Commission (“SEC”). All inquiries from investors present in the United States should be directed to clients@unigestion.com at Unigestion (UK) Ltd. This information is intended only for institutional clients and qualified purchasers as defined by the SEC and has therefore not been adapted to retail clients.

EUROPEAN UNION

This material is disseminated in the European Union by Unigestion Asset Management (France) SA which is authorized and regulated by the French “Autorité des Marchés Financiers” („AMF“).

This information is intended only for professional clients and eligible counterparties, as defined in the MiFID directive and has therefore not been adapted to retail clients.

CANADA

This material is disseminated in Canada by Unigestion Asset Management (Canada) Inc. which is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario, Quebec and Newfoundland & Labrador. Its principal regulator is the Ontario Securities Commission („OSC“). This material may also be distributed by Unigestion SA which has an international advisor exemption in Quebec, Saskatchewan and Ontario. Unigestion SA’s assets are situated outside of Canada and, as such, there may be difficulty enforcing legal rights against it.

SWITZERLAND

This material is disseminated in Switzerland by Unigestion SA which is authorized and regulated by the Swiss Financial Market Supervisory Authority („FINMA“).

Document issued May 2022.