What Machine Learning Likes: Low Volatility And Quality Exemplifying Pricing Power

- With the big swings in the market in April, Lower Vol stocks outperformed, while the Value factor was also positive.

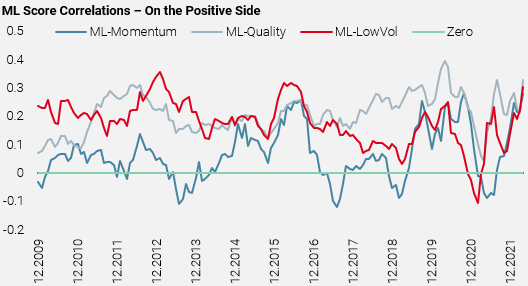

- In developed markets, the correlation of our ML signal’s scores to Quality, Momentum and Low Vol were all positive and above their long-term average.

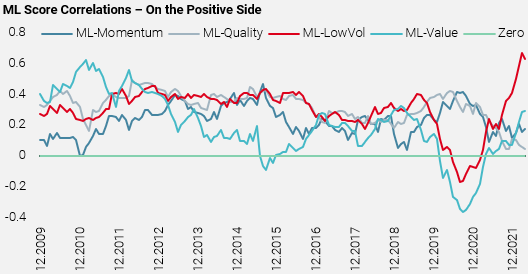

- In emerging markets, ML signals exhibited a positive correlation to Low Vol and Value after a dip from 2020 to early 2021.

Executive Summary

We are very excited to bring to you our inaugural edition of What Machine Learning Likes. There has been an ever growing interest in Machine Learning (ML) over recent times and with this publication our aim is to highlight market trends within ML and assess their impact on our portfolios. The next edition will be published in July and then on a quarterly basis.

ML algorithms digest a large amount of data to identify patterns and build predictability that constantly evolves as it adapts to continuous feedback and market dynamics. At Unigestion, we have worked on developing our ML techniques over the last few years and have uncovered how ML-based stock selection models can successfully enhance the performance of risk-managed portfolios. More recently, we have further enhanced our model and applied it to our active factor investing strategies – training the machine to identify where it has learnt enough to discover ‘alpha’. Specifically, we have implemented ML-based forecasts into our Multi-Factor Equity strategy to take into account the dynamic nature of the ML methodology.

Market Review

Global equities slumped in April amid growth fears, supply chain woes and some disappointing earnings results from the mega tech giants. In the US, the S&P 500 index declined 8.8%, its largest monthly retreat since March 2020. The technology-heavy Nasdaq Composite index fell further into bear market territory, a 13.2% fall in April being its worst monthly decline since October 2008. In less tech-dominated Europe, indices fared slightly better, with the MSCI Europe index dropping 5.3% over the month. Emerging market equities also decreased in April, with the MSCI Emerging Market index declining by 5.6%. In China, factory activity contracted at a steeper pace in April, as widespread Covid-19 lockdowns curbed production and disrupted supply chains. The concerns about the steep cost of China’s zero-tolerance policy continued to weigh on the stock market, with the MSCI China index dipping by 4.1% despite a sharp rally at the end of the month.

Looking at the traditional risk premium factors, with the big swings in the market, we saw Lower Volatility stocks outperform as investors evaluated the macro environment and market dynamics. While the Value factor delivered a positive performance, Growth lagged.

Navigating the Factor Zoo:

Quality Led the Way in Developed Markets

Our ML algorithm gathers ~150 indicators across the spectrum of fundamental, technical, sentiment and alternative data sets to uncover the non-linear relationships between those indicators and the expected returns.

In developed markets, the correlation of our ML signal’s scores to Quality, Momentum and Low Vol were all positive in April and above their long-term average, as Figure 1 demonstrates. Despite Quality lacking its lucrative performance in recent quarters, we believe the rationale behind the ML signal’s fondness for it comes from two fronts.

Firstly, companies with higher quality features tend to fare better during times when economic growth is slowing down, and, as our proprietary macro Nowcasters are indicating, this is exactly what we are experiencing now. Secondly, given the current inflationary regime is expected to be with us for a while, companies with higher profitability are better placed to digest and absorb these cost increases than lower quality (or non-profitable) companies.

Figure 1: ML Score Correlations in Developed Markets

Source: Unigestion, Compustats, CiQ. As at 30 April 2022.

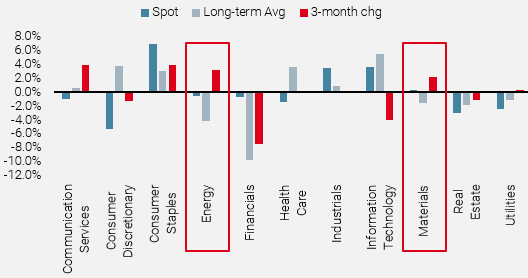

The conflict between Russia and Ukraine has contributed to a significant amount of market uncertainty and its consequences are already having a severe impact on various industries, ranging from energy to food, and from semiconductors to cars. The geopolitical volatility had a clear influence on the ML model, where it not only favours the Low Vol factor but has also started to like Energy and Materials stocks, areas of the market that are generally associated with strong momentum. As illustrated in Figure 2, while we are still slightly underweight Energy and marginally overweight Materials, by -0.6% and 0.4% respectively, the recent market dynamics have prompted our ML model portfolio to increase allocation in both sectors by 3.2% and 2.2% respectively over the last three months.

Figure 2: Growth and Inflation Indicators

Source: Unigestion, Compustats, CiQ. As at 30 April 2022.

ML Likes Low Vol at a Historical High Level in Emerging Markets

In emerging markets, ML signals exhibited a positive correlation to Low Vol and Value after a dip from 2020 to early 2021. More recently, the positive trend between the ML signal and Low Vol reached an all-time high, at above 0.6 in April. This indicates the ML alpha signal is strongly in favour of companies exhibiting lower volatility characteristics.

Figure 3: ML Score Correlations in Emerging Markets

Source: Unigestion, Compustats, CiQ. As at 30 April 2022.

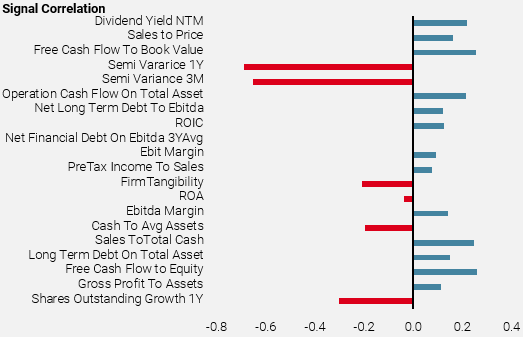

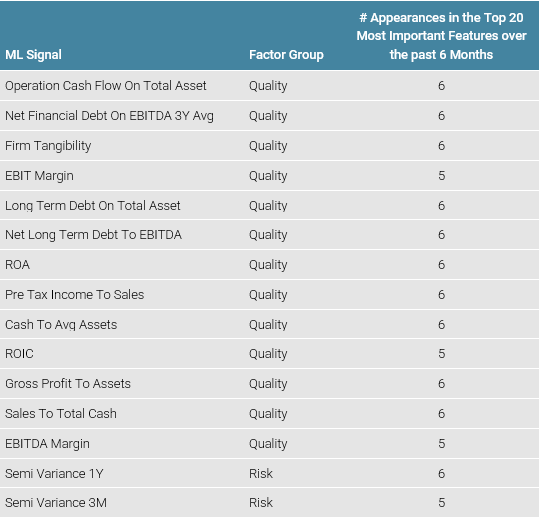

When navigating through the factor zoo, we found that Quality-anchored metrics dominated the top 20 most important features that derive the ML signal forecast scores. As shown in Figure 4a, both profitability-related metrics, such as Operating Cash Flow on Total Assets, EBITDA Margin, Free Cash Flow to Equity, and safety-related features of 3y Average Net Debt to EBITDA exhibited a positive correlation with the ML signal. The highly volatile market environment ensured a spot routinely occupied by the risk features. The strong negative correlation between high-risk features and the ML signal further implied the preference for low volatility characteristics. It is also interesting to see that the current most important features that are being favoured by ML models have consistently appeared at the top of the leader boards over the past few months, as shown in Figure 4b.

Figure 4a: Top 20 Important Features in Emerging Markets

Source: Unigestion, Compustats, CiQ. As at 30 April 2022.

Figure 4b: Appearance in Top 20 Important Features over the past Six Months

Source: Unigestion, Compustats, CiQ. As at 30 April 2022.

Important information

Past performance is no guide to the future, the value of investments, and the income from them change frequently, may fall as well as rise, there is no guarantee that your initial investment will be returned. This document has been prepared for your information only and must not be distributed, published, reproduced or disclosed by recipients to any other person. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation.

This is a promotional statement of our investment philosophy and services only in relation to the subject matter of this presentation. It constitutes neither investment advice nor recommendation. This document represents no offer, solicitation or suggestion of suitability to subscribe in the investment vehicles to which it refers. Any such offer to sell or solicitation of an offer to purchase shall be made only by formal offering documents, which include, among others, a confidential offering memorandum, limited partnership agreement (if applicable), investment management agreement (if applicable), operating agreement (if applicable), and related subscription documents (if applicable). Please contact your professional adviser/consultant before making an investment decision.

Where possible we aim to disclose the material risks pertinent to this document, and as such these should be noted on the individual document pages. The views expressed in this document do not purport to be a complete description of the securities, markets and developments referred to in it. Reference to specific securities should not be considered a recommendation to buy or sell. Unigestion maintains the right to delete or modify information without prior notice. Unigestion has the ability in its sole discretion to change the strategies described herein.

Investors shall conduct their own analysis of the risks (including any legal, regulatory, tax or other consequences) associated with an investment and should seek independent professional advice. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment. These are not suitable for all types of investors.

To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks. Actual results could differ materially from those in the forward-looking statements. As such, forward looking statements should not be relied upon for future returns. Targeted returns reflect subjective determinations by Unigestion based on a variety of factors, including, among others, internal modeling, investment strategy, prior performance of similar products (if any), volatility measures, risk tolerance and market conditions. Targeted returns are not intended to be actual performance and should not be relied upon as an indication of actual or future performance.

No separate verification has been made as to the accuracy or completeness of the information herein. Data and graphical information herein are for information only and may have been derived from third party sources. Unigestion takes reasonable steps to verify, but does not guarantee, the accuracy and completeness of information from third party sources. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. All information provided here is subject to change without notice. It should only be considered current as of the date of publication without regard to the date on which you may access the information. Rates of exchange may cause the value of investments to go up or down. An investment with Unigestion, like all investments, contains risks, including total loss for the investor.

Legal Entities Disseminating This Document

UNITED KINGDOM

This material is disseminated in the United Kingdom by Unigestion (UK) Ltd., which is authorized and regulated by the Financial Conduct Authority („FCA“). This information is intended only for professional clients and eligible counterparties, as defined in MiFID directive and has therefore not been adapted to retail clients.

UNITED STATES

This material is disseminated in the United States by Unigestion (UK) Ltd., which is registered as an investment adviser with the United States Securities and Exchange Commission (“SEC”). All inquiries from investors present in the United States should be directed to clients@unigestion.com at Unigestion (UK) Ltd. This information is intended only for institutional clients and qualified purchasers as defined by the SEC and has therefore not been adapted to retail clients.

EUROPEAN UNION

This material is disseminated in the European Union by Unigestion Asset Management (France) SA which is authorized and regulated by the French “Autorité des Marchés Financiers” („AMF“).

This information is intended only for professional clients and eligible counterparties, as defined in the MiFID directive and has therefore not been adapted to retail clients.

CANADA

This material is disseminated in Canada by Unigestion Asset Management (Canada) Inc. which is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario, Quebec and Newfoundland & Labrador. Its principal regulator is the Ontario Securities Commission („OSC“). This material may also be distributed by Unigestion SA which has an international advisor exemption in Quebec, Saskatchewan and Ontario. Unigestion SA’s assets are situated outside of Canada and, as such, there may be difficulty enforcing legal rights against it.

SWITZERLAND

This material is disseminated in Switzerland by Unigestion SA which is authorized and regulated by the Swiss Financial Market Supervisory Authority („FINMA“).

Document issued June 2022.