-

Private equity markets have been hit hard by the COVID-19 crisis, with North America experiencing the worst of the falls in investment and exit activity.

-

We are already seeing a number of investment opportunities emerge, from the current crisis, particularly among small and mid-market companies and secondaries.

-

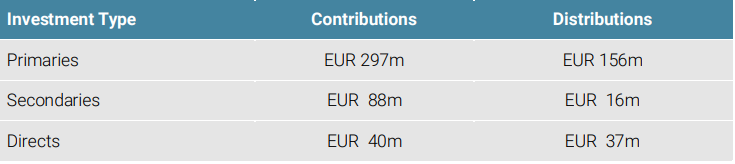

In H1 2020, Unigestion contributed EUR 425 million to investments and received distributions from investments of EUR 209 million.

Overview

The impact of the COVID-19 pandemic on private equity investment and exit activity in the second quarter has been severe. However, the fall in activity has not been uniform across the market. North America posted particularly large declines in both investment and exit activity, while Europe and the APAC region were less impacted. In addition, small and mid-market investment activity has shown more resilience than at the larger end of the market. Meanwhile, investors have in general not been put off by the crisis with fundraising activity remaining buoyant. Indeed, total fundraising in the first half of 2020 fell by only 4% compared to the same period in 2019.

Small Deal Activity Holds Up

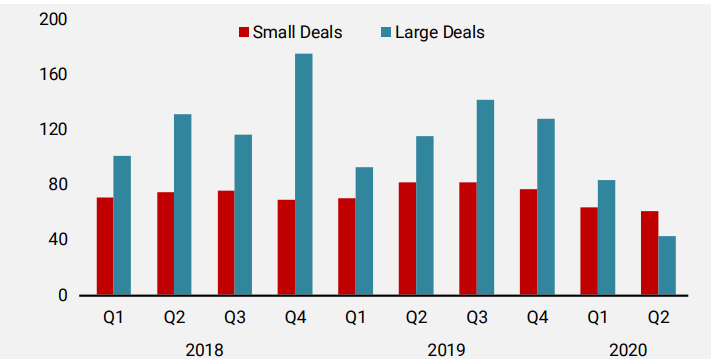

The global aggregate value of private equity deals closed during Q2 2020 was EUR 103bn, 48% down on the same quarter last year1. Likely driven by the more protracted pandemic in the US, North America saw the largest decline with a 55% decrease. Europe showed a 40% drop while APAC fared better with only a 26% drop.

Investment activity in small and mid-market companies (defined as deals less than EUR 500m in enterprise value) showed more resilience than large cap deals (deals greater than EUR 500m). The aggregate value of small and mid-market deals completed declined by 26% in the quarter, compared to 63% for large cap deals. This means that, for the first quarter in more than five years, more capital has flowed to deals at the small end than the large end of the market.

Figure 1: Investment Activity by Deal Size (EUR bn)

This was likely driven by a significant drop in availability of debt for larger deals, as well as the volatility of the public markets limiting the number of public to privates and large corporate carve-outs.

On the other hand, small and mid-market deals have fewer obstacles. Firstly, the use of debt is more limited and can be sourced from specialist debt funds or other institutional providers, rather than banks who have concerns over their existing loan books. Secondly, small and mid-market companies are known to show more resilience during recessions2. Indeed, such companies tend to operate in niche sectors or in those that are less sensitive to economic ups and downs. Furthermore, they are usually more nimble. In times of trouble it is easier for them to react quickly – for example to immediately cut costs or reduce capex.

This is demonstrated by the latest investment for Unigestion Direct II. In June 2020, Unigestion closed its investment in Aquam Water Services (AWS), the UK’s leading provider of outsourced tech-enabled standpipe management services to water utilities. AWS is exposed to stable end markets such as street cleaning services. Indeed, volumes of hired standpipes managed by the company continued to grow even through the worst of the UK’s COVID-19 lockdown.

Global exit activity continued a downward trajectory that began before the COVID-19 pandemic. The global aggregate value of exits in Q2 2020 was EUR 76bn, 56% down on the same quarter last year. Again, North America posted the largest decline (-60%), with Europe (-52%) and APAC (-34%) showing lower but still material declines.

Despite the economic crisis caused by COVID-19 and the consequent slowdown in private equity deal activity, investors have not reduced their demand for private equity exposure.

As we saw in Q1, despite the economic crisis caused by COVID-19 and the consequent slowdown in private equity deal activity, investors in general have not reduced their demand for private equity exposure. So far in 2020, EUR 220bn has been raised which is only 4% down on the same period last year3. However, given that the number of funds closed is more than 30% down, it seems that investors are preferring to invest in larger funds.

Average pricing for private equity deals reached record levels of over 11x EBITDA towards the end of 2019. Many investors are hoping to see prices fall on the back of the current slowdown. While it is too early to see any trend in the data, it is clear that competition for deals will not easily go away as private equity managers continue to collect fresh capital.

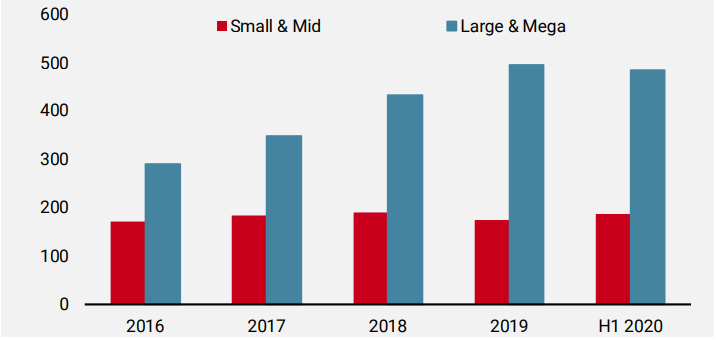

However, we believe that the ratio of dry powder to investment activity at the small end of the market is much more favourable than at the large end of the market. Figure 2 below shows how dry powder for funds with size of EUR 1.5bn or greater has risen by 67% in the last 5 years. For funds below EUR 1.5bn, dry powder has remained flat. This suggests that the upward pressure on pricing at the large end will be much greater than at the small end of the market, especially given that larger deals have recently become scarcer.

Figure 2: Dry Powder by Fund Size (EUR bn)

Secondary Opportunities Are Appearing

In April 2020, we wrote a paper outlining why we thought that the economic crisis caused by the COVID-19 pandemic will likely present some excellent secondary opportunities, particularly at the smaller end of the market. However, we expected that most potential sellers would wait until at least the publication of Q2 valuations before tapping into the secondary market. Nonetheless, we are already seeing a whole range of highly interesting opportunities.

According to intermediaries, this is a phenomenon only being seen at the lower end of the market. Currently, we are seeing a range of secondary types, from singe LP stakes to sidecar funds, and from different types of sellers, from banks to family offices.

In Italy, we are in the final stages of purchasing a large stake from a family office in a 2012 vintage fund consisting mainly of two food-related companies. Although the companies have been performing particularly well, we were able to negotiate a material discount.

In Denmark, we have just completed a transaction with a GP whereby we are the sole investor in a sidecar fund set up to provide growth capital to the two most promising companies in their portfolio. The largest investment in the portfolio is in a wearable tech company for women which will grow at over 100% this year. Nevertheless, we were able to negotiate a sizeable discount to the valuation set prior to the COVID-19 pandemic, combining a secondary purchase with a convertible instrument.

In the US, we are working on a single asset restructuring of the last remaining portfolio company of a 2000 vintage fund. Even though this company has performed extremely well in recent months, we have the opportunity to come in at a 50% discount to the latest valuation.

The similarities across these opportunities are that (i) they are all small secondary transactions, (ii) they are deals consisting of one or two “COVID winners” – companies which have performed well during the lockdown, and (iii) we are able to negotiate sizeable discounts. While larger sellers are waiting longer before beginning formal sale processes, small sellers tend to be more opportunistic and prefer selling through quick discrete bilateral processes.

We will continue to search for the best secondary opportunities that are currently emerging from the crisis.

Unigestion Private Equity Investment Activity

The first half of this year was very busy for the private equity team at Unigestion, despite the slowdown in the market caused by the pandemic. Between January and June 2020, Unigestion contributed EUR 425 million to new investments and received distributions of EUR 209 million.

In H1 2020, we contributed EUR 425 million to new investments.

Figure 3: Investment Activity in H1 2020

Some highlights of the new commitments and investments we made are as follows:

In April, we committed to Polaris V, a small to mid-market buyout fund with a focus on the Nordics. Founded in 1998, Polaris is one of the longest established firms in Denmark. The firm typically makes majority buyout investments in succession situations or carve-outs of niche businesses from large corporates. The firm has an agnostic approach towards sectors but has invested mainly in businesses operating in the services, industrials and consumer sectors. Over the years, Polaris has developed a robust and structured value creation approach, combining hands-on operational impact, buy-and-build execution and organisational development.

In the same month, we also committed to Rubicon Technology Partners Fund III, a small to mid-market buyout fund in the US. Founded in 2012, Rubicon Technology Partners is an operationally focused buyout firm investing in North American enterprise software companies. Targeted companies enjoy recurring software revenues, are profitable or near profitability and are typically founder-led businesses. Rubicon seeks to partner with management teams who are strongly aligned with go-forward plans particularly in areas of investment, operational improvements and long-term strategy.

In June, we committed to Bencis Buyout Fund VI, a small to mid-market buyout fund with a focus on the Benelux region. Established in 1999, Bencis concentrates on business and consumer services, industry and manufacturing, and food and beverage, aiming to identify stable companies in overlooked market niches but with strong market positions and the potential for organic growth. Bencis favours fragmented sectors in which it can consolidate through the acquisition of smaller players. The lower entry prices for these add-ons also typically leads to multiple expansion at exit, when Bencis can sell a larger company with a strong market share.

Also in June, Unigestion Direct II, together with our investment partner Cadence Equity Partners, invested in Aquam Water Services (AWS) and Orbis. AWS is based in Manchester and is the UK’s number one provider of outsourced standpipe management services to water utilities. The company enables end water users (e.g. local authorities who need water from street level access points for road cleaning, etc.) to rent standpipes and legally extract water from utility networks.

In addition to AWS, the transaction included Orbis, which has been the “outsourced R&D arm” of AWS. Based in San Diego, Orbis manufactures GPS-backed intelligent modules that can provide customers with valuable data on water usage, location, leakage detection, etc. These modules can be attached to AWS’ standpipes, creating intelligent standpipes that are rented at higher price points. There is also scope for Orbis’ intelligent modules to be applied to various other adjacent items, including hydrants and pipes, thereby substantially expanding the customer base and addressable market of the combined group.

We also invested in Evondos alongside Verdane Capital. Founded in 2009, Evondos is a Finnish company that develops and assembles automated medical dispensing solutions and rents them to its customers over contracts of 1 to 4-years. Its main product is a dispensing robot targeted at elderly patients with reduced cognitive abilities, which automatically dispenses the right medicine at the right time in the right quantity and enables caretakers to easily and accurately track a patient’s medication intake.

The products are used mainly by elderly home care patients and sold to municipalities or home care agencies. Evondos is a market leader and its USP compared to existing and emerging competitors is higher reliability and the ability to read all multi-dose sachets in the Nordics market, as well as a broader set of features which makes the service more suitable for various patients.

1Pitchbook, July 2020.

2See “Small and Mid-Market Private Equity: The Calm During the Storm” published by Unigestion in May 2020.

3Preqin, April 2020.

4See “Private Equity Secondaries: the Opportunity of the Decade?” published by Unigestion in April 2020.

Important Information

Past performance is no guide to the future, the value of investments, and the income from them change frequently, may fall as well as rise, there is no guarantee that your initial investment will be returned. This document has been prepared for your information only and must not be distributed, published, reproduced or disclosed (in whole or in part) by recipients to any other person without the prior written consent of Unigestion. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation.

This is a promotional statement of our investment philosophy and services only in relation to the subject matter of this presentation. It constitutes neither investment advice nor recommendation. This document represents no offer, solicitation or suggestion of suitability to subscribe in either the investment vehicles to which it refers or to any securities or financial instruments described herein. Any such offer to sell or solicitation of an offer to purchase shall be made only by formal offering documents, which include, among others, a confidential offering memorandum, limited partnership agreement (if applicable), investment management agreement (if applicable), operating agreement (if applicable), and related subscription documents (if applicable). Such documentation contains additional information material to any decision to invest. Please contact your professional adviser/consultant before making an investment decision.

Where possible we aim to disclose the material risks pertinent to this document. The views expressed in this document do not purport to be a complete description of the securities, markets and developments referred to in it. Reference to specific securities should not be considered a recommendation to buy or sell. Unigestion maintains the right to delete or modify information without prior notice.

Investors shall conduct their own analysis of the risks (including any legal, regulatory, tax or other consequences) associated with an investment and should seek independent professional advice. Some of the investment strategies or financial instruments described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment. These are not suitable for all types of investors. Unigestion has the ability in its sole discretion to change the strategies described herein.

To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks. Actual results could differ materially from those in the forward-looking statements. As such, forward looking statements should not be relied upon for future returns. Targeted returns reflect subjective determinations by Unigestion based on a variety of factors, including, among others, internal modeling, investment strategy, prior performance of similar products (if any), volatility measures, risk tolerance and market conditions. Targeted returns are not intended to be actual performance and should not be relied upon as an indication of actual or future performance.

No separate verification has been made as to the accuracy or completeness of the information herein. Data and graphical information herein are for information only and may have been derived from third party sources. Unigestion takes reasonable steps to verify, but does not guarantee, the accuracy and completeness of information from third party sources. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. All information provided here is subject to change without notice. It should only be considered current as of the date of publication without regard to the date on which you may access the information. Rates of exchange may cause the value of investments to go up or down. An investment with Unigestion, like all investments, contains risks, including total loss for the investor.

Unigestion Direct II (UDII) has been created as a SCS-SICAV-RAIF in Luxembourg and qualifies as an Alternative Investment Fund (AIF) within the meaning of the law dated 12 July 2013 on Alternative Investment Fund Managers implementing the Directive 2011/61/EU (AIFMD). As a result, units of this vehicle may be offered only to professional investors and may not be distributed on a public basis in or from any country where such distribution would be prohibited by law. This document contains a preliminary summary of the purpose and principal business terms of an investment in UDII. This summary does not purport to be complete and is qualified in its entirety by reference to the more detailed discussion to take place with the AIF. UDII has the ability in its sole discretion to change the strategies described herein. Before making a decision to invest in UDII, you are advised to consult with your tax, legal and financial advisors.

Additional Information for US Investors

Unigestion Direct II SCS-SICAV-RAIF (UDII): An investment in the Unigestion Direct II SCS-SICAV-RAIF (the “Fund”) involves a high degree of risk and is not suitable for all types of investors. Prior to making an investment, prospective investors should carefully consider all the information set out in the Private Placement Memorandum and, in particular, should evaluate the applicable risk factors which, individually or in aggregate, could have a material adverse effect on the Fund and its investments.

For US investors, Unigestion is relying on SEC Rule 15a-6 under the Securities Exchange Act of 1934 regarding exemptions from broker-dealer registration for foreign broker dealers. Foreside Global Services, LLC is acting as the chaperoning broker dealer for Unigestion for the purposes of soliciting and effecting transactions with of for US institutional investors or major US institutional investors.

The performance figures are based on estimated fees and expenses as well as on the underlying strategy’s estimated performances given by fund managers, administrators, custodians and third party sources at a given date. Where performance is reflected gross of fees, potential investors should be aware that the inclusion of fees, costs and charges will reduce the overall value of performance. Unless otherwise stated, the performance data source are Unigestion, Bloomberg and Compustat.

This information is provided to you solely to give you background information relating to Unigestion, certain strategies it implements and currently offers. Before making an investment decision with respect to the strategy discussed herein, potential investors are advised to consult with their tax, legal, ERISA and financial advisors. Note that not all strategies may be available or suitable for investment by U.S. investors.

This document may contain forward-looking statements, including observations about markets and industry and regulatory trends as of the original date of this document. Forward-looking statements may be identified by, among other things, the use of words such as “expects,” “anticipates,” “believes,” or “estimates,” or the negatives of these terms, and similar expressions. Forward-looking statements reflect Unigestion’s views as of such date with respect to possible future events. Actual results could differ materially from those in the forward-looking statements as a result of factors beyond a strategy’s or Unigestion’s control. Readers are cautioned not to place undue reliance on such statements. No party has an obligation to update any of the forward-looking statements in this document

Return targets or objectives, if any, are used for measurement or comparison purposes and only as a guideline for prospective investors to evaluate a particular investment program’s investment strategies and accompanying information. Performance may fluctuate, especially over short periods. Targeted returns should be evaluated over the time period indicated and not over shorter periods.

The past performance of Unigestion, its principals, shareholders, or employees is not indicative of future returns.

Except where otherwise specifically noted, the information contained herein, including performance data and assets under management, relates to the entire affiliated group of Unigestion entities over time including that of Unigestion UK. Such information is intended to provide the reader with background regarding the services, investment strategies and personnel of the Unigestion entities. No guarantee is made that all or any of the individuals involved in generating the performance on behalf the other Unigestion entities will be involved in managing any client account on behalf of Unigestion UK. More specific information regarding Unigestion UK is set forth herein where indicated and is available on request.

There is no guarantee that Unigestion will be successful in achieving any investment objectives. An investment strategy contains risks, including the risk of complete loss.

The risk management practices and methods described herein are for illustrative purposes only and are subject to modification.

Legal Entities Disseminating This Document

UNITED KINGDOM

This material is disseminated in the United Kingdom by Unigestion (UK) Ltd., which is authorized and regulated by the Financial Conduct Authority (« FCA »). This information is intended only for professional clients and eligible counterparties, as defined in MiFID directive and has therefore not been adapted to retail clients.

UNITED STATES

This material is disseminated in the U.S. by Unigestion (UK) Ltd., which is registered as an investment adviser with the U.S. Securities and Exchange Commission (“SEC”). This information is intended only for institutional clients and qualified purchasers as defined by the SEC and has therefore not been adapted to retail clients.

EUROPEAN UNION

This material is disseminated in the European Union by Unigestion Asset Management (France) SA which is authorized and regulated by the French “Autorité des Marchés Financiers” (« AMF »).

This information is intended only for professional clients and eligible counterparties, as defined in the MiFID directive and has therefore not been adapted to retail clients.

CANADA

This material is disseminated in Canada by Unigestion Asset Management (Canada) Inc. which is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario, Quebec and Newfoundland & Labrador. Its principal regulator is the Ontario Securities Commission (« OSC »). This material may also be distributed by Unigestion SA which has an international advisor exemption in Quebec, Saskatchewan and Ontario. Unigestion SA’s assets are situated outside of Canada and, as such, there may be difficulty enforcing legal rights against it.

SWITZERLAND

This material is disseminated in Switzerland by Unigestion SA which is authorized and regulated by the Swiss Financial Market Supervisory Authority (« FINMA »).

SINGAPORE

This material is disseminated in Singapore by Unigestion Asia Pte Ltd. which is regulated by the Monetary Authority of Singapore (« MAS »).

Document issued September 2020.