Rising Risks for European Equities

Political uncertainty, trade war, economic slowdown, declining earnings expectations, unattractive valuations – Stéphane Dutu, Fundamental Analyst, takes stock of the current headwinds faced by European equities.

Political risks are the first that come to mind when we think about risks for European equity investors. How would you describe the current situation?

We believe that European political risks are rising again due to worrying developments in the UK and Italy:

- In the UK, the odds of a hard exit from the EU have surged in the wake of the resignation of Prime Minister Theresa May due to her failure to strike a Brexit deal with the House of Commons. Brexit hardliner Boris Johnson is the bookmakers’ frontrunner to win the Tory leadership and replace Mrs May as Prime Minster by the end of July. In our opinion, this would be a negative outcome. The former Foreign Secretary is ready to accept a no-deal exit – if, among other things, the Irish backstop is not dropped by Brussels – and does not want to postpone Brexit beyond the end of October, which does not bode well for future negotiations with the EU. Following the surging popularity of the new Brexit party led by Nigel Farage, the British arch-enemy of the EU, many Tory leaders are now convinced that they must swiftly deliver on Brexit or face extinction as a political force.

- In Italy, tensions between 5 Star and Lega have soared so much that an end of their fragile government coalition followed by a snap election is now a likely scenario. Polls are suggesting that such an election will not produce a workable coalition majority for either right-wing or left-wing parties, leading to political paralysis and instability. Italy may be a small equity market, but it is the Eurozone’s third-largest economy and its sovereign bond market is the largest in the region. Such an unfavourable sequence of events would therefore weigh on all European equity markets.

Are there any positive factors underpinning European equities?

Yes, the increasingly dovish tone of systematically relevant central banks is a positive factor for equity markets. Both the US Federal Reserve and the European Central Bank have increasingly signalled their intention to ease monetary policy should the global economic slowdown intensify.

As you say, the global economy is slowing – is this not a big risk?

Yes, the global GDP slowdown continues and it has to be said that the loss of economic momentum is most striking in Europe, especially in Germany. The country has been negatively impacted by a confidence crisis in its key automotive sector, as well as by its above-average exposure to decelerating international trade. And Germany, as the economic engine of Europe, is contaminating its neighbours.

Elsewhere, in China, the slackening pace of economic growth is not only the result of trade tensions with the US. There are also structural drivers that the communist leadership can only partially offset if it does not want to boost the already-high financial leverage of China to a too dangerous level.

However, on a more positive note, the US has so far remained largely unscathed by the global economic slowdown. But, having said that, we are likely to see less robust US GDP growth over the next 12 months for the following reasons:

- The positive impact from the latest tax cuts will lapse this year.

- The lagged effect of past monetary tightening is starting to be felt in segments of the economy that are sensitive to interest rates, such as car sales and housing starts.

- The radicalisation of both the Democrats and the Republicans could dash hopes of a bi-partisan agreement on the necessary increase in public infrastructure spending. Should the Democrats seize Congress and the Presidency in 2020, they could even increase taxes – as an example to fund their ambitious energy transition programme, which would undermine the confidence of economic agents.

The basic trade war issues between the US and China remain unsolved.

The US and China trade war continues to make headlines. What can we expect going forward?

The basic issues that have led to the trade conflict between the US and China have not been solved. The US administration expects a firm commitment from the Chinese authorities to deal with the following issues that they say hurt corporate America and US workers:

- Lack of intellectual property protection

- Forced technology transfer

- State subsidies to corporate China

- The ever-rising trade deficit of the US with China

In addition, the US is also insisting on strict enforceability of any agreed trade deal, and on maintaining the increased tariffs on Chinese imports until sufficient evidence has been gathered that the Chinese are keeping their word. We doubt the latter will easily accept these stringent requirements, so these trade war risks are likely to persist in the months ahead.

We expect equity valuations cannot be sustained given the deteriorating macro and earnings backdrop.

What’s the outlook for corporate profits?

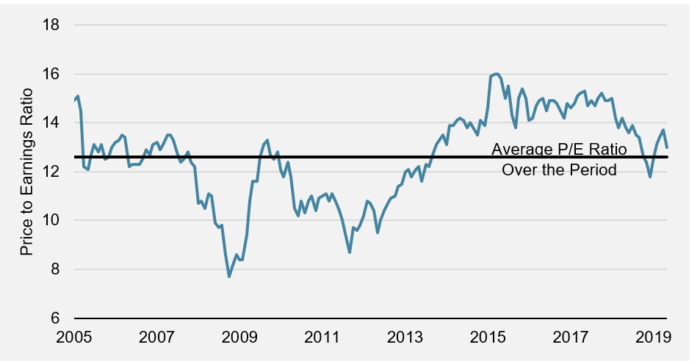

As a result of the reduced pace of global growth, earnings expectations have been falling, which is a burden for equities. And with equity valuations already materially above their historical average, we expect that the current levels will not be sustainable in the face of declining profit forecasts.

Figure 1: MSCI Europe – Price to Earnings Ratio 2005 to 2019

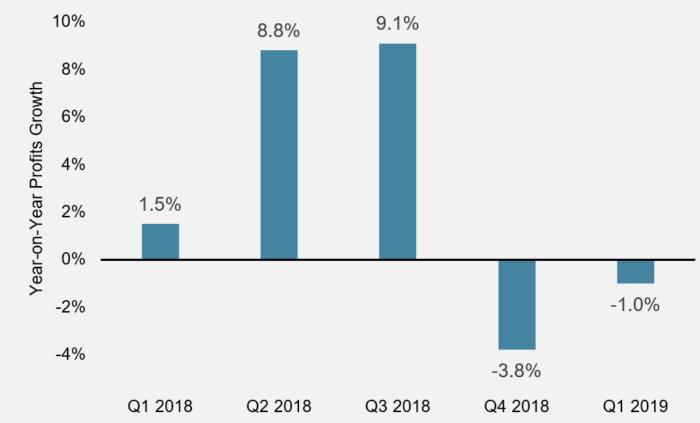

If we look at the numbers, earnings forecasts for the next 12 months are down 4% compared to their peak in September 2018. With a year-on-year earnings contraction of -1%, Q1 2019 was not an encouraging earnings season.

Figure 2: Year-on-Year Profit Growth for European Equities

Despite central bank support, the case for equities remains challenging.

Given the current backdrop, are you bullish or bearish?

So to sum things up, while key central banks may have become more supportive, there are powerful negative forces that continue to weaken the case for equities. These are increasing political risks, the unabated global economic slowdown, the unresolved trade conflict between China and the US, falling earnings estimates and too rich equity valuations.

Bearing this in mind, we think that the defensive positioning that we adopted in our European equity portfolios in the middle of 2018 is still justified.

Important Information

This document is provided to you on a confidential basis and must not be distributed, published, reproduced or disclosed, in whole or part, to any other person.

The information and data presented in this document may discuss general market activity or industry trends but is not intended to be relied upon as a forecast, research or investment advice. It is not a financial promotion and represents no offer, solicitation or recommendation of any kind, to invest in the strategies or in the investment vehicles it refers to. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment.

The investment views, economic and market opinions or analysis expressed in this document present Unigestion’s judgement as at the date of publication without regard to the date on which you may access the information. There is no guarantee that these views and opinions expressed will be correct nor do they purport to be a complete description of the securities, markets and developments referred to in it. All information provided here is subject to change without notice. To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks.

Data and graphical information herein are for information only and may have been derived from third party sources. Although we believe that the information obtained from public and third party sources to be reliable, we have not independently verified it and we therefore cannot guarantee its accuracy or completeness. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. Unless otherwise stated, source is Unigestion.

Past performance is not a guide to future performance. All investments contain risks, including total loss for the investor.

Unigestion SA is regulated by the Swiss Financial Market Supervisory Authority (FINMA). Unigestion (UK) Ltd is authorised and regulated by the Financial Conduct Authority (FCA) and SEC registered. Unigestion Asset Management (France) SA is regulated by the “Autorité des Marchés Financiers” (AMF). Unigestion (Luxembourg) SA is an Alternative Investment Fund Manager authorised by the Commission de Surveillance du Secteur Financier (CSSF) under the Luxembourg law of 12 July 2013 on AIFM. Unigestion Asset Management (Canada) Inc., with offices in Toronto and Montreal, is regulated in Canada by the securities regulatory authorities in Ontario, Quebec; Alberta, Manitoba, Saskatchewan, Nova Scotia, New Brunswick and British Columbia. Its principal regulator is the Ontario Securities Commission. Unigestion Asia Pte Ltd is regulated in Singapore by the MAS, as Capital Market Services (CMS) license holder and Exempt Financial Adviser under the Securities and Futures Act and Financial Advisers Act.

Document issued June 2019.