Overview

Private equity Emerging Managers is a hot topic these days. It is not a new concept as some of the largest public pension funds in the world have been pursuing the strategy successfully for almost two decades. However, over the past few years it has attracted broader interest, becoming a dedicated investment strategy for many LPs. The space has also been gaining momentum thanks to the proliferation of new funds, a strong macro tailwind, and the desire of many investors to diversify their exposures to the larger funds currently forming the core of their private equity exposure.

Below, we argue that, in the current environment, a diversified portfolio of allocations to Emerging Managers has the potential to deliver strong and differentiated returns. However, it can also deliver a number of other compelling investment benefits to experienced investors with sufficient resources to find the best opportunities and manage the risks particular to first-time managers.

What is an Emerging Manager?

For Unigestion, an Emerging Manager is a GP raising Fund I or II, focusing on primary deals in small and mid-market companies, with typical fund sizes of under USD 500m, though the majority of funds we see are rather in the USD 150-250m range. While in the past these first funds were typically launched by former investment bankers or the like, today it is more often spin-out teams of larger and well-established players, or family offices with proven track records and significant experience. These teams have a strong entrepreneurial drive and desire for greater control of the investment strategy, but also see an opportunity to focus on more specialist strategies and exploit new market niches. Allocating to Emerging Managers is also an opportunity to support more minority- and women-led firms, as they represent a larger proportion of the Emerging Manager universe compared to the established names. We have seen a significant increase in deal flow in the past years and expect the trend to continue.

The Investment Opportunity

The aim of Emerging Manager programmes is to build a diversified portfolio of highly specialised managers with above-average return potential in a segment that is difficult to access. The opportunity presents four key attractions:

- Specialist Strategies: Emerging Managers typically launch funds with specialist strategies consistent with their track record. They may be sector specialists with specific themes (e.g. Healthtech, Foodtech, Enterprise Software, etc.) or strategy specialists (e.g. Buy & Build, Growth, Complex Buyouts, etc). This focus on specialist strategies with highly experienced teams can drive outstanding returns with downside protection1.

- Ability to Minimise the Total Expense Ratio (TER): Committing to first time funds, in particular for investors with the ability to underwrite an offering early on and support GPs with best practice coaching, allows LPs to negotiate various special terms. These may include staggered carry schemes, short duration funds, cornerstone/first closer discounts, or fee-free co-investment rights. On a total cost basis, the final fee load can be significantly reduced relative to standard market terms.

- Attractive Co-investment to Primary Capital Ratio: Perceived risks and fee loads can be further minimised by combining a commitment in a GP’s Fund II with a staple into Fund I, or by stapling a Fund I commitment to the first portfolio deal. There may also be an agreement on a target ratio of fund commitments to co-investments or simply a right of first refusal for any co-investment opportunities that may arise. Adding co-investments can further reduce the TER thanks to no fee/no carry arrangements, reduce the blind pool risk by allowing investors to diligence a deal, and ensures faster deployment of capital.

- Access to Successor Funds: Committing to promising Emerging Managers early on is the best way to ensure future allocations. The combination of strong returns and moderate fund sizes means that access to these rising stars will be severely restricted for LPs wanting to jump onto the bandwagon at a later stage.

On a total cost basis, the final fee load can be significantly reduced relative to standard market terms.

Taken together, Emerging Manager GPs have the potential to not only be significant performance contributors up front, but to grow over time into core partners for institutional private equity portfolios.

Sourcing Emerging Manager Opportunities

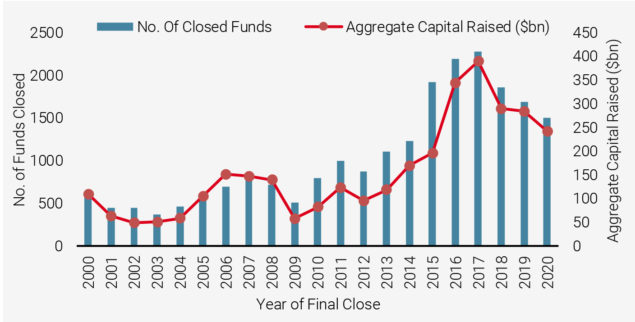

There has been tremendous growth in the Emerging Manager space, with thousands of new entrants over recent years driven by expanding private equity allocations and the ever-increasing need to find new sources of alpha and avoid segments with large amounts of dry powder. In fact, Emerging Managers typically represent well over half of the total universe of funds closed per year, making them a segment difficult to ignore.

Figure 1: Emerging Manager Fundraising: Funds Closed 2000-2020

Source: Unigestion as of 30.04.2021 and Preqin as of 31.12.2020, global data across all private equity strategies and geographies. Emerging Managers include first and second generation funds.

While this provides a large pool of potential investee funds, it also presents challenges due to the sheer number of funds to analyse, compounded by their emerging nature with little reputation to go on and limited quantitative data. Avenues for sourcing follow three main paths. The first option is desktop research, including tracking M&A deal-making per country via data providers, as well as subscribing to relevant fund databases and newsletters, trying to identify potential spin-out teams early on and adopting a proactive approach. It is worth noting that only a fraction of new funds will be found on the most popular private equity databases, so relying on this source alone is not advisable. Another important avenue is through networks. Fund lawyers, intermediaries, and like-minded LPs that focus on Emerging Managers are often the first to learn of new fund launches. Finally, LPs with a strong reputation for committing to Emerging Managers and offering best practice coaching are often contacted directly, providing an opportunity to get in early with the GPs deemed to be of the highest quality.

We supported them from the beginning, helping with everything from fund documentation, to setting terms and conditions, to their fundraising plans.

What Are Emerging Managers Looking for in a Partner?

Case Study:

SF Equity Partners (US)

Unigestion first met the founders of San Francisco-based SF Equity Partners in 2015 while they were trying to raise their first fund. Despite their lack of a fund track record, they had an interesting and highly specialised investment strategy in the high growth consumer-branded companies space and a proven ability to find smaller off-market opportunities at the right price, which we found compelling. They ultimately failed to raise that fund, but Unigestion went on to support them on a few individual deals and developed a strong rapport. When in 2018 they decided to try again (target fund size USD 100m) – this time with a ‘proof of concept’ deal-by-deal track record – we supported them from the beginning, helping with everything from fund documentation, to setting terms

and conditions, to their fundraising plans. The result was a highly attractive investment opportunity in a short-duration fund, good pipeline visibility and fast deployment pace, cornerstone terms, an Advisory Board seat, and a ‘first look’ right for Fund II. Today, SF Equity Partners has been steadily exiting companies at attractive multiples and returning capital at an impressive pace.

Case Study:

Greenpeak Partners (Germany)

Greenpeak Partners, based in Munich, started investing as a team in 2015 at ROBUR Industry Services, a buy-and-build platform, aimed at consolidating the high-end industrial services markets in the DACH region. Unigestion was a co-investor in ROBUR and the firm has become one of the top 10 players in Germany with 20 add-ons and turnover of over EUR 200m across five market segments. With over 10 years of deal-by-deal experience, but limited experience as an institutional fund, the team launched Greenpeak II in 2020 (target fund size EUR 135m) to pursue four new buy-and-build platforms, focusing on long-term ecological and social impact, backed by three megatrends: environment, health, and digitalisation. Three of the four platforms had already been identified and one was in the process of closing at the time of our commitment, providing high visibility. As a result of our strong relationship, Unigestion was approached as a cornerstone investor in the fund with preferential terms. Additional benefits were direct allocations to deals via a parallel co-investment vehicle, a short duration fund, and a concentrated portfolio.

Mitigating Potential Pitfalls

The attraction of Emerging Managers notwithstanding, there are also various challenges to be considered. The main areas of focus can be grouped into four categories:

Emerging Managers can exhibit a wider dispersion of returns than more established GPs.

- Dispersion of Performance: Despite the higher expected returns for Emerging Managers, they may exhibit a wider dispersion of returns than more established GPs. Mitigants are well-diversified programmes (10-12 fund commitments), a strong focus on specialist strategies, and a careful use of leverage.

- Fundraising Risks: The benefits of being an early supporter of Emerging Managers and having preferential terms come with a higher fundraising risk and potentially concentrated portfolios. Mitigants here include knowing the GP very well, having visibility over the fundraising pipeline, strict single-asset thresholds, and close interaction with other LPs in the due diligence process. Cornerstone LPs may further facilitate the fundraising by providing access to their own network and making introductions to like-minded investors.

- Operational Risks: First-time managers will need to navigate not just the investment challenges, but also operational complexities that may be new to them. Examples include managing strong personalities that are used to working independently, team-building, and simply learning the ropes of running a company. However, investors may be partially protected by more LP-friendly LPAs compared to the market standard while best practice coaching provided by experienced LPs is invaluable.

- Track Record: Most Emerging Managers lack a clear-cut track record. Mitigants include careful examination of the deal-by-deal track record and a focus on funds providing good visibility on the initial portfolio. A strongly collaborative relationship between GP and LP is also helpful.

The best-positioned investors will be those with a long experience of PE investing, ideally at the small end of the market, with large networks and a strong reputation of supporting Emerging Managers.

Is the Performance Really Worth the Extra Effort?

There has been much research into the performance of Emerging Managers, most of which clearly confirms their outperformance potential. When comparing median IRRs globally by vintage year across the entire private equity spectrum for the past 20 years, there is strong evidence that the first-time fund segment has performed strongly across market cycles (see Figure 2 below). At the same time, we also know that the dispersion of these returns may be higher, meaning that good selection is key and that LPs with strong sourcing networks, excellent selection strategies, and many years of experience will likely be at an advantage.

There is strong evidence that the first-time fund segment has performed strongly across market cycles.

Figure 2: Global Private Equity Median IRRs by Vintage: Emerging Managers vs. Established Managers

Source: Unigestion as of 30.04.2021 and Preqin as of 31.12.2020, global data across all private equity strategies and geographies. Emerging Managers include first and second generation funds, Established Managers are third generation funds onwards.

Dispersion of returns may be higher, meaning that good selection is key.

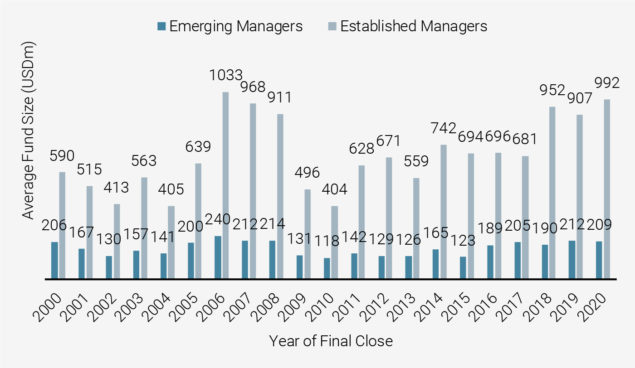

Another noticeable trend is that while the established GP funds seem to get larger over time – with size strongly correlated to the prevailing economic environment – the average fund size of Emerging Managers has been quite stable, typically between USD 150-250m. The result is more reasonable fund sizes that match the market opportunity, leading to less dry powder and more limited competition for deals.

Figure 3: Average Fund Sizes: Emerging Managers vs. Established Managers

Source: Unigestion as of 30.04.2021 and Preqin as of 31.12.2020, global data across all private equity strategies and geographies. Emerging Managers include first and second generation funds, Established Managers are third generation funds onwards.

The combination of more new funds being launched and fund sizes remaining stable leads to intense competition among Emerging Manager GPs for capital, but is also an opportunity for LPs with strong conviction and the willingness to work with Emerging Managers to structure attractive cornerstone agreements with preferential terms.

Uncertain Markets: Is This Really the Right Time to Allocate to Emerging Managers?

The past year with its pandemic-related challenges has made investing in private markets more difficult. Preqin data reports that private market fundraising reached USD 790bn in 2020 – a decline of 9% from 2019. Preqin further estimates that while an average of 26% of capital raised since 2000 has gone to first-time fund managers, in 2019 the figure fell to 19% and remained stable in 2020. Covid-19 weighed heavily on allocations as LPs focused on re-ups with existing and established managers, partly driven by the inability to conduct full onsite diligence due to travel restrictions. In conjunction with the LP trend towards more concentrated GP relationships, fundraising for first-time funds has become more challenging than usual.

Emerging Managers present a unique investment opportunity and can provide strong downside protection.

Nevertheless, Emerging Managers present a unique investment opportunity and, equally importantly, can provide strong downside protection due to the ‘triple alpha’ of (i) outperformance of small and mid-market managers, (ii) a focus on specialist strategies, and (iii) lower TER achieved through special terms.

For experienced LPs, this environment provides an opportunity to partner with highly attractive investment teams. In fact, some of the attributes of Emerging Managers may actually make them more compelling than usual. GPs just starting out have sufficient, but not excessive, dry powder available, making them highly selective in the deals they pursue. The overall alignment with LPs is very high, as they generally have a significant amount of their personal wealth invested and are highly aware that their future depends on the success of each deal. Furthermore, due to the smaller fund sizes, Emerging Managers know that their economic success is largely dependent on carry and not management fees. A final advantage is that new market entrants can devote their full time and energy to working with portfolio companies given the lack of large legacy portfolios – especially relevant during times of market turmoil.

Why Unigestion for Emerging Managers?

At Unigestion, we have been investing in the Emerging Manager space for well over 20 years. In the 1990s, we were early investors in Cinven, Permira, Carlyle Europe, and EQT. In the 2000s, we committed to the early funds of Waterland, Bowmark, and BlackFin, and in the 2010s, to HgCapital Mercury, Tenzing, Atlas, and Rubicon. These groups have now grown into blue-chip large-cap managers or hard-to-access small and mid-market managers. Since 1996, we have committed to over 100 Emerging Managers globally representing about one third of all commitments made and a core focus of our large and diverse primary investment activity. Over 70% of these funds achieved top or second quartile performance for their respective vintages as at December 2020, and our track record exhibits a very low loss ratio2.

Notwithstanding the attractive return potential, good selection is crucial to mitigate performance dispersion risk. While it is possible to select single Emerging Managers, a portfolio approach reduces the exposure to one specific GP and increases the chances of having one of the ‘future stars’ in your portfolio with whom you can build a long-term relationship. Our current active pipeline of Emerging Manager opportunities consists of over 200 funds globally and continues to grow.

A portfolio approach reduces the exposure to one specific GP and increases the chances of having one of the ‘future stars’ in your portfolio.

We have seen the Emerging Manager segment mature over the past two decades and through various market cycles, gaining invaluable insights along the way. Today we see a market with more new and unique funds being launched than ever before and an opportunity to get access to a highly complementary strategy at competitive terms. For LPs looking for specialist strategies in less crowded markets that carry a number of investment benefits in addition to strong return potential, the Emerging Manager segment is an option worth considering.

1Returns cannot be guaranteed

2Source: Unigestion data, includes all relevant Fund I and II commitments made from 1996-2018.

Important Information

Past performance is no guide to the future, the value of investments, and the income from them change frequently, may fall as well as rise, there is no guarantee that your initial investment will be returned. This document has been prepared for your information only and must not be distributed, published, reproduced or disclosed by recipients to any other person. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation.

This is a promotional statement of our investment philosophy and services only in relation to the subject matter of this presentation. It constitutes neither investment advice nor recommendation. This document represents no offer, solicitation or suggestion of suitability to subscribe in the investment vehicles to which it refers. Any such offer to sell or solicitation of an offer to purchase shall be made only by formal offering documents, which include, among others, a confidential offering memorandum, limited partnership agreement (if applicable), investment management agreement (if applicable), operating agreement (if applicable), and related subscription documents (if applicable). Please contact your professional adviser/consultant before making an investment decision.

Where possible we aim to disclose the material risks pertinent to this document, and as such these should be noted on the individual document pages. The views expressed in this document do not purport to be a complete description of the securities, markets and developments referred to in it. Reference to specific securities should not be considered a recommendation to buy or sell. Unigestion maintains the right to delete or modify information without prior notice. Unigestion has the ability in its sole discretion to change the strategies described herein.

Investors shall conduct their own analysis of the risks (including any legal, regulatory, tax or other consequences) associated with an investment and should seek independent professional advice. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment. These are not suitable for all types of investors.

To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks. Actual results could differ materially from those in the forward-looking statements. As such, forward looking statements should not be relied upon for future returns. Targeted returns reflect subjective determinations by Unigestion based on a variety of factors, including, among others, internal modeling, investment strategy, prior performance of similar products (if any), volatility measures, risk tolerance and market conditions. Targeted returns are not intended to be actual performance and should not be relied upon as an indication of actual or future performance.

No separate verification has been made as to the accuracy or completeness of the information herein. Data and graphical information herein are for information only and may have been derived from third party sources. Unigestion takes reasonable steps to verify, but does not guarantee, the accuracy and completeness of information from third party sources. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. All information provided here is subject to change without notice. It should only be considered current as of the date of publication without regard to the date on which you may access the information. Rates of exchange may cause the value of investments to go up or down. An investment with Unigestion, like all investments, contains risks, including total loss for the investor.

Legal Entities Disseminating This Document

UNITED KINGDOM

This material is disseminated in the United Kingdom by Unigestion (UK) Ltd., which is authorized and regulated by the Financial Conduct Authority (« FCA »). This information is intended only for professional clients and eligible counterparties, as defined in MiFID directive and has therefore not been adapted to retail clients.

UNITED STATES

This material is disseminated in the U.S. by Unigestion (UK) Ltd., which is registered as an investment adviser with the U.S. Securities and Exchange Commission (“SEC”). This information is intended only for institutional clients and qualified purchasers as defined by the SEC and has therefore not been adapted to retail clients.

EUROPEAN UNION

This material is disseminated in the European Union by Unigestion Asset Management (France) SA which is authorized and regulated by the French “Autorité des Marchés Financiers” (« AMF »).

This information is intended only for professional clients and eligible counterparties, as defined in the MiFID directive and has therefore not been adapted to retail clients.

CANADA

This material is disseminated in Canada by Unigestion Asset Management (Canada) Inc. which is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario, Quebec and Newfoundland & Labrador. Its principal regulator is the Ontario Securities Commission (« OSC »). This material may also be distributed by Unigestion SA which has an international advisor exemption in Quebec, Saskatchewan and Ontario. Unigestion SA’s assets are situated outside of Canada and, as such, there may be difficulty enforcing legal rights against it.

SWITZERLAND

This material is disseminated in Switzerland by Unigestion SA which is authorized and regulated by the Swiss Financial Market Supervisory Authority (« FINMA »).

Document issued May 2021.