- Newscasting is the use of macro news sentiment signals to augment and improve the existing dynamic systematic Nowcaster signals.

- News indicators were more timely in capturing the COVID-19 economic collapse, supporting their case as a complement to Nowcasters.

- Our studies show that the addition of Newscasters to a portfolio based on Nowcasters can improve performance, increase the hit ratio and lower drawdowns.

Overview

Unigestion has for many years used Nowcasters for the purpose of asset allocation across traditional and alternative risk premia. In this paper we introduce an evolution of this framework based on what we call Newscasting, which is the use of macro news sentiment signals to augment and improve the existing dynamic systematic Nowcaster signals. The Newscaster signals are carefully constructed from RavenPack macro news sentiment data.

We find that growth Nowcasters and Newscasters have low contemporaneous correlations. We also identify that Newscasters lead Nowcasters, typically at turning points. All in all, we present evidence that Newscasters helped improve the results of asset allocation methodologies over the last twenty years, both on a return and risk basis. More anecdotally, the COVID-19 crisis has illustrated the value of Newscasters given that they reacted ahead of the Nowcasters.

The structure of the paper is as follows: Section 1 provides a brief literature review. Section 2 explains the functioning of Newscasters and compares them to Nowcasters. It reports results on the contemporaneous and lead-lag correlations between Nowcasters and Newscasters. Section 3 then illustrates this behaviour in the form of a case study of the divergence between Newscasters and Nowcasters during the COVID-19 crisis. In section 4, we illustrate the implications for asset allocation and show that Newscasters provide complementary information to Nowcasters. It compares the performance of a cross-asset risk premia portfolio based on Nowcasters alone and contrasts this with that of a version that is augmented with Newscasters. Finally, section 5 concludes.

1: Literature Review

In this section we provide a brief literature review of Nowcasters and the use of news information for asset allocation purposes.

The concept of Nowcasters did not originate in the finance or economics profession but was coined by Keith Browning in 1981 during the first meteorological symposium on Nowcasters and refers to the description of the current state of weather forecasting which predicts it on an hourly time scale (WMO, 2018).

Banbura et al. (2010) survey the literature on Nowcasting in economics. Nowcasting has become a best practice in tracking the economic activity in real-time for leading institutions. For instance, the Fed of Atlanta and the Fed of New-York publish well-known Nowcast estimates for US GDP (see Bok et al., 2019). Since 2014, Unigestion has developed proprietary Nowcaster models (Ielpo, 2020) which track real-time growth and inflation dynamics across many developed and emerging countries, whereas most available solutions are restricted to specific zones and typically the US.

In recent years, academics and practitioners have started moving beyond Nowcasters, that are based on structured data (coming from statistical offices), into the use of unstructured text data associated to news (Getzkow et al., 2019). The use of news in financial analysis has a long-standing tradition but has undergone a renewed interest with the availability of a much larger set of news (Big Data) and the development of methodologies that allow better interpretation, such as Natural Language Processing algorithms.

It has been shown that financial news can help predict stock returns (e.g. Heston and Sinha, 2013). The application to macroeconomics is newer but opens up many interesting avenues from forecasting growth or inflation dynamics, through to estimating the effects of policy uncertainty. Scott and Varian (2013), for example, use data from Google searches to produce high-frequency estimates of macroeconomic variables such as unemployment claims, retail sales, and consumer sentiment that are otherwise available only at lower frequencies from survey data. Carriero et al. (2020) show that using weekly information and Bayesian regression models helps to improve tail nowcasts of economic activity.

Building on this nascent literature, we use macroeconomic news and the sentiment contained therein to create indicators that complement traditional Nowcasters. We label these indicators “Newscasters”.

2: Newscasters – How They Work and Relate to Nowcasters

Newscaster Construction

Inspired by the above literature on extracting news from unstructured text for forecasting purposes, our research on Newscasters is based on the hypothesis that writers (journalists, bloggers, etc.) are each reporting on world events and informing their readers about the economic impact. This economic interpretation of world events, which can be thought of as public news sentiment on the economy, may contain valuable information about the current and upcoming state of the economy. Indeed, we found this to be the case.

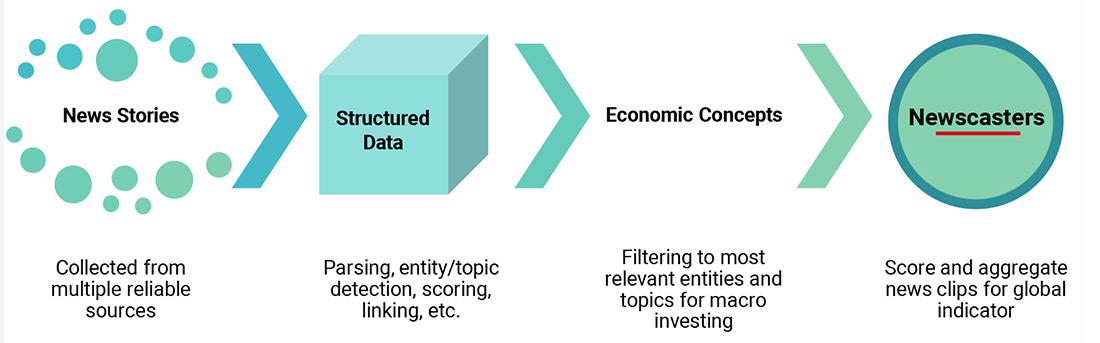

In our research we have used RavenPack news stories and sentiment scores to classify, score and aggregate news clips to create growth and inflation sentiment indicators that we label “Newscasters”. RavenPack reports that it has processed several petabytes of news data in its archives. Figure 1 illustrates our process to ingest and transform this data in a stylized way. While eliding the details of the Newscaster construction and the extensive research behind it, the figure shows how individual news stories are transformed into raw structured data (via RavenPack’s algorithms), from which we then extract the most relevant information for economic concepts and assemble this information into a global indicator.

Figure 1: Overview of the Unigestion Macro Newscasters Construction Process

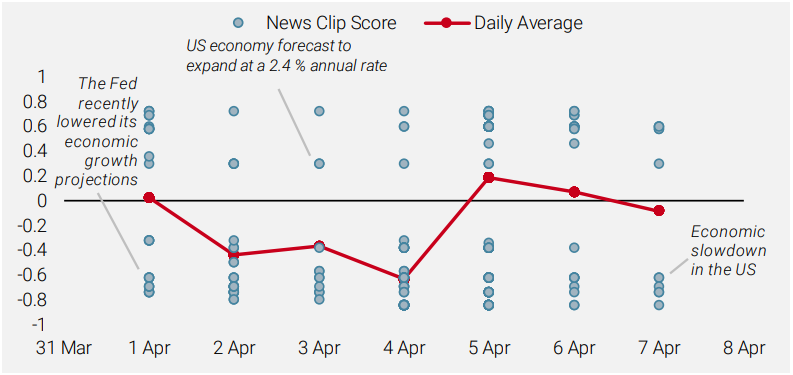

Figure 2 illustrates the concept in more detail using the US Growth Newscaster as an example. Simply put, the construction process underlying the Newscaster selects relevant news clips each day, assesses their view on growth, and averages them together.

Figure 2: Illustration of the US Growth Newscaster (1 to 7 April 2019)

Similar to the construction of the Unigestion Nowcaster, we also distinguish between the level (the indicator) of the Newscaster and its change (the “diffusion” index). Our multi-year experience with the use of Nowcasters for asset allocation purposes has taught us that the diffusion index is very often as valuable as the indicator itself. The diffusion index plays a critical role in capturing the market phenomenon of prices reacting to the second derivative of economic conditions, which is especially important around turning points. Market prices are driven by surprises and this can be, for example, explained in a so-called rational expectations framework (Muth, 1961), although there is debate about how rational investors are in forming their expectations (Bordalo et al., 2020). The indicator as an average of assessments of economic conditions is likely closely related to current expectations, while the diffusion index may reflect positive or negative surprises relative to existing indicators. The diffusion index is therefore likely to be closely related to future returns.

Our experience with the use of Nowcasters for asset allocation purposes has taught us that the diffusion index is very often as valuable as the indicator itself.

Relating Newscasters to Nowcasters

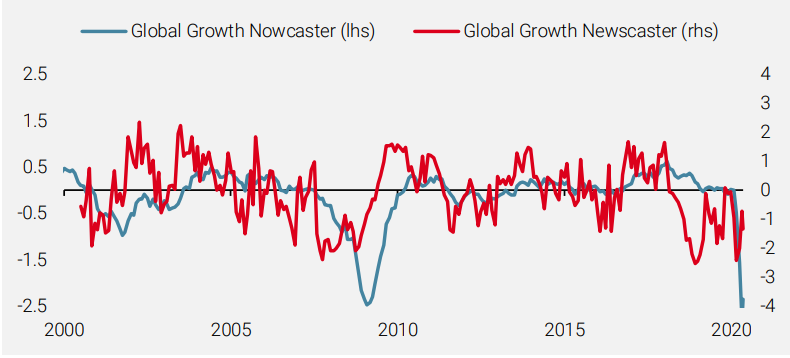

In this section, we briefly examine whether Newscasters contain different information from that found in Nowcasters. Figure 3 shows the time-series behaviour of the Global Growth Newscaster and Nowcaster (similar features hold for inflation). While the Nowcaster and Newscaster track each other over the long-term, over the short-term there is meaningful variation. The time series also suggests a lead/lag relationship between the indicators, with the Newscaster seeming to react faster to economic conditions, especially around turning points. Indeed, we can see in Figure 3 that during the GFC and the COVID-19 crisis, the Newscaster was quicker to reflect the downturn than the Nowcaster, and we discuss this further below. The trade-off for this faster reaction time is additional volatility, with the Newscaster exhibiting roughly twice the volatility of the Nowcaster.

Figure 3: The Growth Newscaster Leads the Growth Nowcaster, Especially Around Turning Points

The correlation between the Newscaster and the Nowcaster is relatively low, suggesting the two signals contain different information even if they are trying to capture a similar concept.

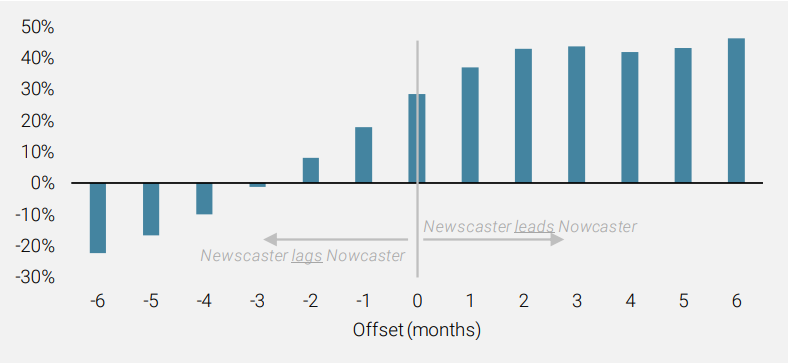

The contemporaneous correlation between the Newscaster and the Nowcaster is relatively low at about 25% (monthly frequency), suggesting the two signals contain meaningfully different information even if they are trying to capture a similar concept. As Figure 4 shows, the Newscaster seems to exhibit a lead of around two to three months over the Nowcaster. Beyond three months, the correlations stabilise at around 45%.

Figure 4: Lead/Lag Correlation of Global Growth Newscaster and Nowcaster

All in all, the Newscaster is faster moving but is also noisier than the Nowcaster.

In the next section we provide a case study of how the Newscaster reacted compared to the Nowcaster during an especially precarious time, the COVID-19 crisis. After discussing this case, we will turn to how we convert the Newscaster into an allocation using the same framework that we have developed to transform Nowcasters into an asset allocation.

3: Case Study

Divergence of Newscasters and Nowcasters During COVID-19

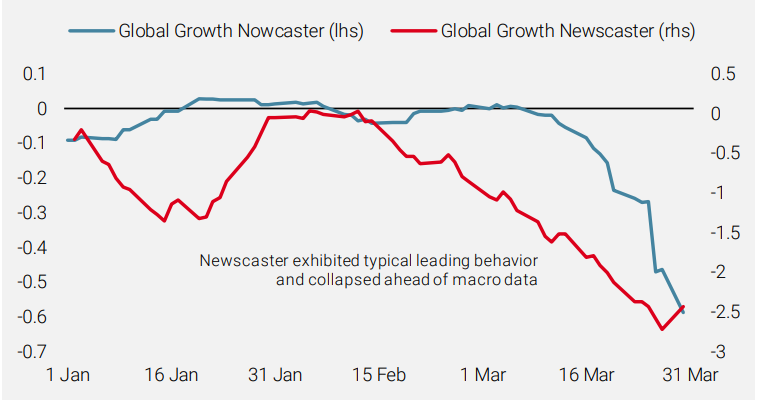

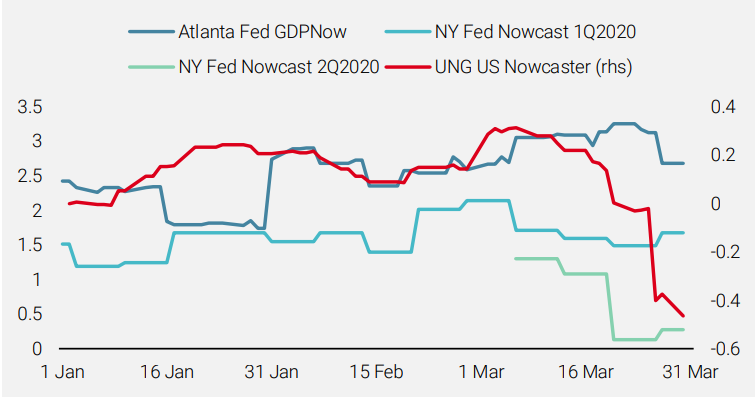

As we saw in the previous section, the Newscaster historically leads the Nowcaster on average. One case study of this relationship is the COVID-19 crisis, although it is important to note that our Newscasters are designed to find news related to economic growth and inflation, and they are not designed to find news on pandemics per se. Rather, they will incorporate events such as pandemics if and when such events start impacting economic news. Figure 5 shows that during this crisis, the Global Growth Newscaster exhibited the typical leading behaviour and collapsed in January and February ahead of the macro data as captured by the Global Growth Nowcaster. It also shows that the Unigestion Nowcaster performed favourably compared to the NY Fed and Atlanta Fed Nowcasters.

Figure 5: The Newscaster and Nowcaster During the COVID-19 Crisis (Q1 2020)

On 8 June 2020, the NBER officially labelled February 2020 as the peak in monthly US economic activity, marking the end of the expansion that began in June 2009 and the beginning of a recession. The reporting delay was to be expected given the process by which the NBER determines business cycle dates, and it should not surprise anyone that financial markets had adjusted well before the official dates were determined.

It is precisely due to reporting lags that Nowcasters were developed to monitor economic activity. However, given the extreme shock of COVID-19, they also exhibited some lag.

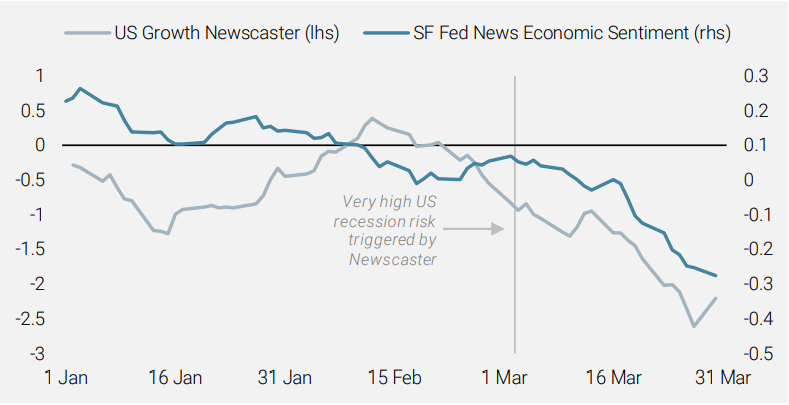

It is precisely due to reporting lags that Nowcasters were developed to monitor economic activity. However, given the extreme exogenous shock, they also exhibited some lag. For instance, our US Growth Nowcaster signalled a very high risk of recession at the end of March, after risky markets had already sold off. News indicators – ours and others – were more timely in capturing the economic collapse, further supporting their case as a complement to Nowcasters. Figure 6 shows the evolution of our US Growth Newscaster, along with the San Francisco Fed’s News Economic Sentiment index. We can see from the chart how the Fed’s News Index began collapsing in mid-March, ahead of some of their Nowcasters (see Figure 5). Our own US Newscaster turned in mid-February and by early March was signalling a very high risk of recession in the US, information that was clearly more useful then than in early June.

Figure 6: Comparison of Newscasters During the COVID-19 Crisis (Q1 2020)

4: Using the Newscaster for Macro Risk-Based Dynamic Allocation

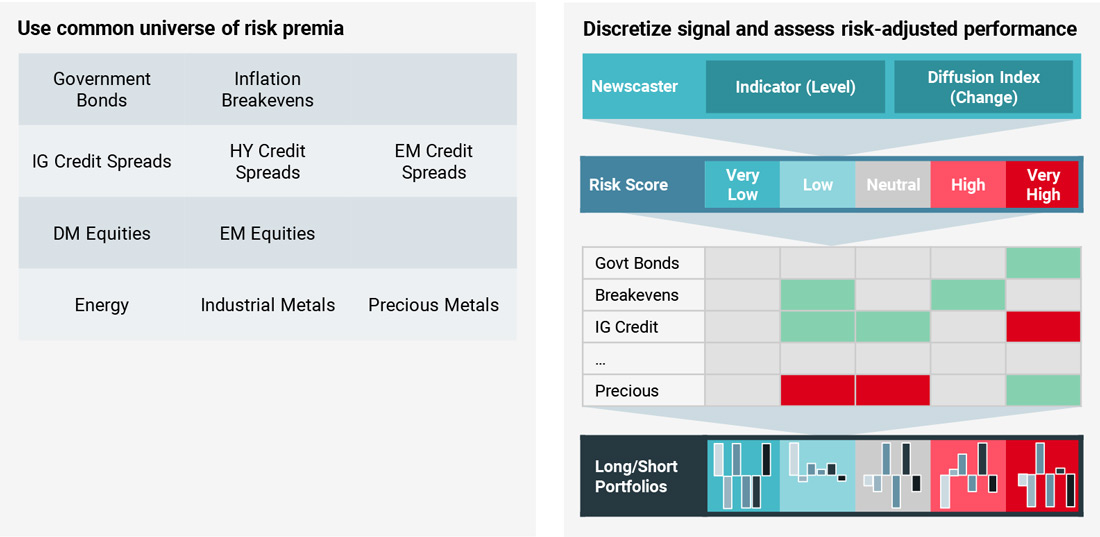

In order to construct a portfolio allocation using our macroeconomic signals (Nowcasters and Newscasters), we adopt a regime-based asset allocation framework. Our preferred framework allocates to ten global risk premia using five regimes corresponding to different levels of risk (from very low to very high). The regimes are determined using both the indicator (i.e., the level) and the diffusion index (i.e., the change). Regime-dependent portfolios are then constructed by going long/short those risk premia that exhibit strong and robust outperformance/underperformance in a given regime for each signal. Figure 7 provides a visual summary of the process (details are described in Blin et al., 2020).

In order to construct a portfolio allocation using our macroeconomic signals (Nowcasters and Newscasters), we adopt a regime-based asset allocation framework.

Figure 7: Macro Risk-Based Dynamic Asset Allocation Framework

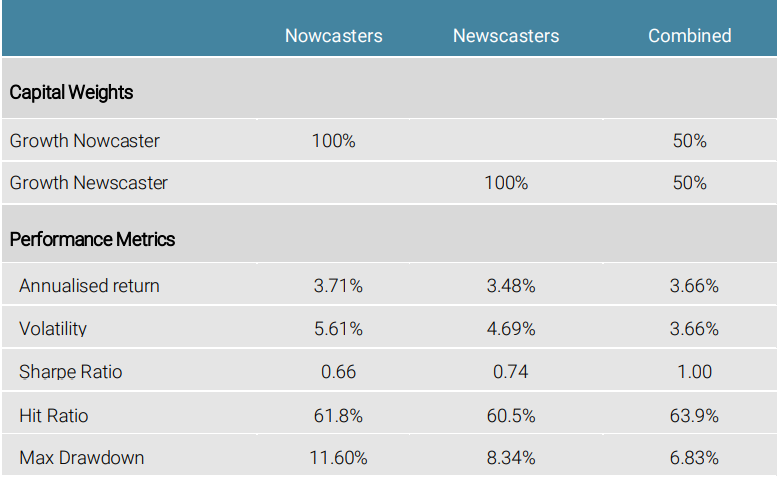

Given that the Newscaster signals seem to contain information that is different from that in Nowcasters, as discussed above, we examined whether this differentiated information could be used to improve the performance (raw and/or risk-adjusted) of a multi-asset portfolio. We constructed a portfolio that was equally-weighted (in capital) between the Growth Nowcaster and Growth Newscaster (labelled “Combined”). Figure 8 details the portfolio allocations and key performance metrics for the simulation period (June 2000 – May 2020, monthly frequency). As the table shows, we see that the Newscaster and Nowcaster have close results, with some better results for the Newscaster. But, even more spectacularly, the combination delivers much higher risk-adjusted returns. This comes mainly from the reduction in risk metrics (either volatility or drawdown) which is notably due to the almost zero correlation between both types of indicator.

Figure 8: Allocation and Performance of Nowcasters and Newscasters Portfolios

Source: Bloomberg, RavenPack, Unigestion.

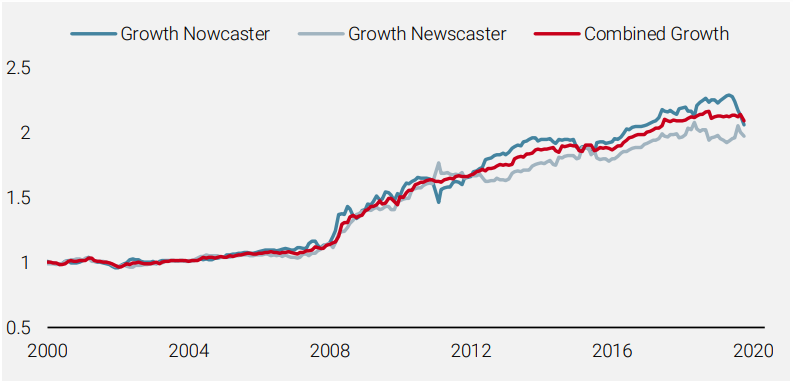

Finally, Figure 9 shows the performance of the Growth Nowcaster and Growth Newscaster through time, along with their equal-weighted combination (“Combined Growth”). An important feature that comes through is the diversifying nature of the return streams. Indeed, when the Growth Nowcaster underperforms (e.g., September 2011, late 2015 – early 2016), the Growth Newscaster tends to outperform. We can also see that during the COVID-19 crisis, the Growth Newscaster helped to offset losses coming from the Growth Nowcaster.

Figure 9: Cumulative Performance of Growth Nowcaster and Newscaster Portfolios

5: Conclusion

In this article we have introduced the concept of Newscasters and compared it to Nowcasters. We have shown that Newscasters, which are based on macroeconomic news sentiment from RavenPack, historically lead Nowcasters while offering a differentiated signal. This has also proven to be the case during the COVID-19 crisis. Finally, we have demonstrated how a multi-asset allocation can be constructed from these indicators and illustrated the benefit of complementing Nowcasters and Newscasters with each other to deliver better risk-adjusted performance.

References

Ang A., and G. Bekaert (2004), “How Regimes Affect Asset Allocation”, Financial Analysts Journal 60, 86-99.

Banbura M., Giannone D., and L. Reichlin (2010). « Nowcasting ». In Clements M., Hendry D. (eds.). Oxford Handbook on Economic Forecasting. Oxford University Press.

Beber A., Brandt M., and M. Luizi (2015), “Distilling the Macroeconomic News Flow”, Journal of Financial Economics 117, 489-507.

Blin O., Ielpo F., Lee J., and J. Teiletche (2020), “Factor Timing Revisited: Alternative Risk Premia Allocation Based on Nowcasting and Valuation Signals”, Available at SSRN: https://ssrn.com/abstract=3247010

Bok B., Caratelli D., Giannone D., Sbordone A., and A. Tambalotti (2017), “Macroeconomic Nowcasting and Forecasting with Big Data”, Federal Reserve Bank of New-York Staff Report No. 830.

Bordalo, Pedro, Nicola Gennaioli, Yueran Ma, and Andrei Shleifer. Forthcoming. “Overreaction in Macroeconomic Expectations .” American Economic Review.

Carriero A., T. Clark, and M. Marcellino (2020), “Nowcasting Tail Risks to Economic Activity with Many Indicators”, Federal Reserve Board of Cleveland Working Paper No. 20-13.

Gentzkow M., Kelly B., and M. Taddy (2019), “Text As Data”, Journal of Economic Literature 57(3), 535-574

Heston S., and N. Sinha (2016), “News versus Sentiment: Predicting Stock Returns from News Stories”, Board of Governors of the Federal Reserve System, Working Paper 2016-048.

Ielpo F. (2020), “Introduction to Unigestion Nowcasters”, Unigestion Research Paper.

Muth J. (1961), “Rational Expectations and the Theory of Price Movements”, Econometrica 29(3), 315-335.

Scott S., and H. Varian (2013), “Predicting the Present with Bayesian Structural Time Series”, Available at SSRN: https://ssrn.com/abstract=2304426.

WMO (2018), Guide to Nowcasting Techniques, WMO-No. 1198.

Important Information

Past performance is no guide to the future, the value of investments, and the income from them change frequently, may fall as well as rise, there is no guarantee that your initial investment will be returned. This document has been prepared for your information only and must not be distributed, published, reproduced or disclosed by recipients to any other person. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation.

This is a promotional statement of our investment philosophy and services only in relation to the subject matter of this presentation. It constitutes neither investment advice nor recommendation. This document represents no offer, solicitation or suggestion of suitability to subscribe in the investment vehicles to which it refers. Any such offer to sell or solicitation of an offer to purchase shall be made only by formal offering documents, which include, among others, a confidential offering memorandum, limited partnership agreement (if applicable), investment management agreement (if applicable), operating agreement (if applicable), and related subscription documents (if applicable). Please contact your professional adviser/consultant before making an investment decision.

Where possible we aim to disclose the material risks pertinent to this document, and as such these should be noted on the individual document pages. The views expressed in this document do not purport to be a complete description of the securities, markets and developments referred to in it. Reference to specific securities should not be considered a recommendation to buy or sell. Unigestion maintains the right to delete or modify information without prior notice. Unigestion has the ability in its sole discretion to change the strategies described herein.

Investors shall conduct their own analysis of the risks (including any legal, regulatory, tax or other consequences) associated with an investment and should seek independent professional advice. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment. These are not suitable for all types of investors.

To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks. Actual results could differ materially from those in the forward-looking statements. As such, forward looking statements should not be relied upon for future returns. Targeted returns reflect subjective determinations by Unigestion based on a variety of factors, including, among others, internal modeling, investment strategy, prior performance of similar products (if any), volatility measures, risk tolerance and market conditions. Targeted returns are not intended to be actual performance and should not be relied upon as an indication of actual or future performance.

No separate verification has been made as to the accuracy or completeness of the information herein. Data and graphical information herein are for information only and may have been derived from third party sources. Unigestion takes reasonable steps to verify, but does not guarantee, the accuracy and completeness of information from third party sources. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. All information provided here is subject to change without notice. It should only be considered current as of the date of publication without regard to the date on which you may access the information. Rates of exchange may cause the value of investments to go up or down. An investment with Unigestion, like all investments, contains risks, including total loss for the investor.

Legal Entities Disseminating This Document

UNITED KINGDOM

This material is disseminated in the United Kingdom by Unigestion (UK) Ltd., which is authorized and regulated by the Financial Conduct Authority (« FCA »). This information is intended only for professional clients and eligible counterparties, as defined in MiFID directive and has therefore not been adapted to retail clients.

UNITED STATES

This material is disseminated in the U.S. by Unigestion (UK) Ltd., which is registered as an investment adviser with the U.S. Securities and Exchange Commission (“SEC”). This information is intended only for institutional clients and qualified purchasers as defined by the SEC and has therefore not been adapted to retail clients.

EUROPEAN UNION

This material is disseminated in the European Union by Unigestion Asset Management (France) SA which is authorized and regulated by the French “Autorité des Marchés Financiers” (« AMF »).

This information is intended only for professional clients and eligible counterparties, as defined in the MiFID directive and has therefore not been adapted to retail clients.

CANADA

This material is disseminated in Canada by Unigestion Asset Management (Canada) Inc. which is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario, Quebec and Newfoundland & Labrador. Its principal regulator is the Ontario Securities Commission (« OSC »). This material may also be distributed by Unigestion SA which has an international advisor exemption in Quebec, Saskatchewan and Ontario. Unigestion SA’s assets are situated outside of Canada and, as such, there may be difficulty enforcing legal rights against it.

SWITZERLAND

This material is disseminated in Switzerland by Unigestion SA which is authorized and regulated by the Swiss Financial Market Supervisory Authority (« FINMA »).

SINGAPORE

This material is disseminated in Singapore by Unigestion Asia Pte Ltd. which is regulated by the Monetary Authority of Singapore (« MAS »).

Document issued September 2020.