- While financial markets appear to have forgotten about Covid, some, such as the UK, have not fully recovered.

- Even accounting for structural differences, most UK sectors have de-rated relative to their European counterparts.

- Short-term growth has been stronger in the UK, suggesting an element of ‘catch up’.

- While we are currently comfortable with our underweight UK position, we expect investors will start re-rating UK companies and we will monitor our position accordingly.

The Post-Covid Recovery Differences

For most of us, the Covid pandemic is probably the most unprecedented and disruptive crisis that we will have experienced. However, thanks to rapid mass vaccinations, there is a sense that things are finally under control across Europe, though we are far from a complete normalisation of the situation.

From a financial perspective, and judging by the performance of, and valuations in, equity markets, the crisis has long been forgotten. Indeed, supported by decisive monetary and fiscal policies, European economies went through the crisis without suffering any major or lasting damage. The consequences of the health measures were a series of confinements and restrictions to economic activity, but contrary to other crises, there was significantly less impact on the means of production. As a result, most companies came through this episode and are now back in business.

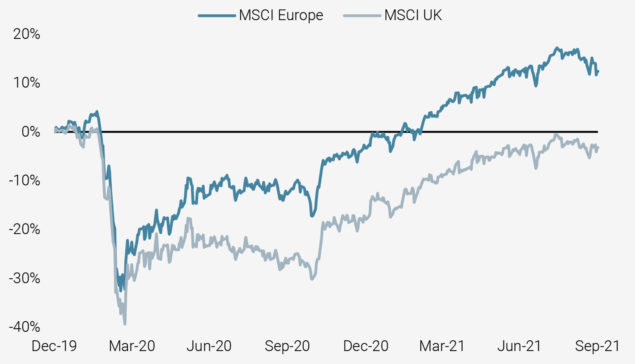

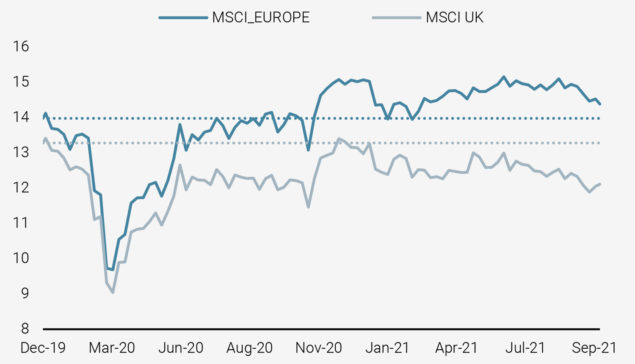

However, looking closer at individual European countries, we see that the picture is not as encouraging everywhere, and the UK is a case in point. As Figure 1 shows, the market performance here has not fully recovered, showing persistently weaker returns, while valuations remain de-rated, with the Price-Earnings ratio currently at 12.1 compared to 13.3 at the end of 2019 (Figure 2).

Figure 1: Performance of UK and European Equities (Net of Dividends, in EUR)

Source: MSCI, Unigestion. As at 30 September 2021.

Figure 2: Price to Earnings Ratio (FY3 Consensus Median)

Source: MSCI, CapitalIQ, Unigestion. As at 30 September 2021.

What’s Behind the UK’s Underperformance?

Since the Brexit referendum in 2016, the UK market has been approached with circumspection by investors given the significant political and economic uncertainty. As a result, the local market has underperformed the European one markedly. However, five years later, Brexit is no longer an investment question or source of uncertainty. The question now is more one of the economic consequences of reduced integration with continental Europe, and the increasing disruptions associated with this, as well as the second order impacts of the Covid crisis. The evolution of relative valuations is reflective of this situation.

At first glance, one could point to the structural differences between the UK and European indices. Traditionally cheaper sectors which may have profited less in the post-crisis rebound, such as Materials, Financials or Communication Services, are overweight in the UK. Conversely, the more expensive Information Technology sector has a relatively low weight in the index. However, even accounting for sectoral differences, most UK sectors have been de-rated compared to their European counterparts.

Figure 3: The Re-Rating of UK Sectors Relative to European Counterparts (Since 31.12.2019)

Source: MSCI, CapitalIQ, Unigestion. As at 30 September 2021.

This de-rating is better explained by lower earnings growth perspectives. It appears that analysts were initially expecting much firmer earnings growth for UK companies coming out of the crisis. By early 2021, though, these higher expectations morphed into much milder growth, to the tune of 4.8% in the UK, compared to a European average of 8.2%, as demonstrated in Figure 4.

Figure 4: Expected Earnings Growth (FY3 vs FY2)

Source: MSCI, CapitalIQ, Unigestion. As at 30 September 2021.

Current Positioning Justified, But Things Will Improve

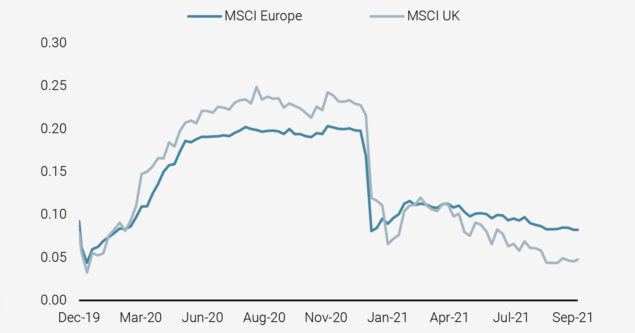

We see no short-term catalyst for a reversal of fortunes for UK companies, and even less so if we account for the current disruptions which have surfaced in the UK economy through the fuel crisis-related logistical issues. We are therefore comfortable limiting our exposure to the UK in our European portfolios, acknowledging in addition the somewhat riskier nature of UK stocks compared to European ones.

Figure 5: Current Average Volatilities By Country

Source: MSCI, Unigestion. As at 30 September 2021.

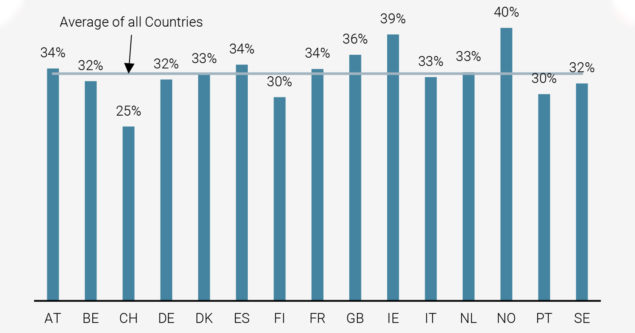

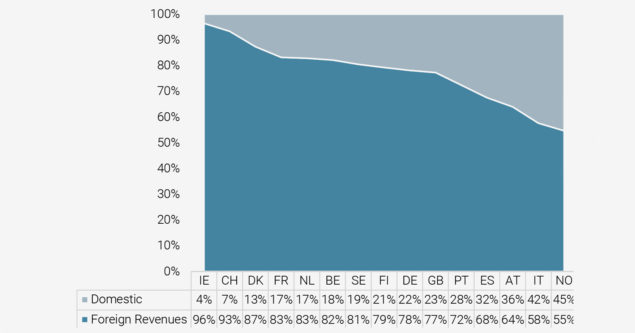

However, looking ahead, the situation will certainly improve for a number of reasons. Firstly, we see no fundamental disconnect between the UK and European economies in terms of long-term GDP growth prospects. Indeed, European economies remain largely interconnected. Secondly, shorter-term GDP growth is higher in the UK, suggesting that there is an element of ‘catch up’ already taking place. According to the most recent data, Q2 GDP growth was 5.5% in the UK, compared to 1.9% for the EU as a whole and 1.8% in Switzerland. Thirdly, the companies we are considering, essentially large caps, are predominantly international companies with global revenue sources.

Figure 6: Average Proportion of Foreign Revenues by Country

Source: MSCI, Factset, Unigestion. As at June 2021.

As Figure 6 highlights, the UK is pretty average from this perspective, with members of the local MSCI index deriving, on average, 77% of their revenues from abroad. The impact of UK economic growth on UK stocks is therefore significantly smaller than one would intuitively expect. There is therefore no reason for British companies not to profit from global opportunities as much as their continental counterparts.

While the current picture may be dark and grey, at some point (and we believe this will be sooner rather than later) the skies will clear and the sun will shine again on corporate UK, leading investors to re-rate UK companies and close the valuation gap on their European competitors.

Important information

Past performance is no guide to the future, the value of investments, and the income from them change frequently, may fall as well as rise, there is no guarantee that your initial investment will be returned. This document has been prepared for your information only and must not be distributed, published, reproduced or disclosed by recipients to any other person. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation.

This is a promotional statement of our investment philosophy and services only in relation to the subject matter of this presentation. It constitutes neither investment advice nor recommendation. This document represents no offer, solicitation or suggestion of suitability to subscribe in the investment vehicles to which it refers. Any such offer to sell or solicitation of an offer to purchase shall be made only by formal offering documents, which include, among others, a confidential offering memorandum, limited partnership agreement (if applicable), investment management agreement (if applicable), operating agreement (if applicable), and related subscription documents (if applicable). Please contact your professional adviser/consultant before making an investment decision.

Where possible we aim to disclose the material risks pertinent to this document, and as such these should be noted on the individual document pages. The views expressed in this document do not purport to be a complete description of the securities, markets and developments referred to in it. Reference to specific securities should not be considered a recommendation to buy or sell. Unigestion maintains the right to delete or modify information without prior notice. Unigestion has the ability in its sole discretion to change the strategies described herein.

Investors shall conduct their own analysis of the risks (including any legal, regulatory, tax or other consequences) associated with an investment and should seek independent professional advice. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment. These are not suitable for all types of investors.

To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks. Actual results could differ materially from those in the forward-looking statements. As such, forward looking statements should not be relied upon for future returns. Targeted returns reflect subjective determinations by Unigestion based on a variety of factors, including, among others, internal modeling, investment strategy, prior performance of similar products (if any), volatility measures, risk tolerance and market conditions. Targeted returns are not intended to be actual performance and should not be relied upon as an indication of actual or future performance.

No separate verification has been made as to the accuracy or completeness of the information herein. Data and graphical information herein are for information only and may have been derived from third party sources. Unigestion takes reasonable steps to verify, but does not guarantee, the accuracy and completeness of information from third party sources. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. All information provided here is subject to change without notice. It should only be considered current as of the date of publication without regard to the date on which you may access the information. Rates of exchange may cause the value of investments to go up or down. An investment with Unigestion, like all investments, contains risks, including total loss for the investor.

Legal Entities Disseminating This Document

UNITED KINGDOM

This material is disseminated in the United Kingdom by Unigestion (UK) Ltd., which is authorized and regulated by the Financial Conduct Authority (« FCA »). This information is intended only for professional clients and eligible counterparties, as defined in MiFID directive and has therefore not been adapted to retail clients.

UNITED STATES

This material is disseminated in the U.S. by Unigestion (UK) Ltd., which is registered as an investment adviser with the U.S. Securities and Exchange Commission (“SEC”). This information is intended only for institutional clients and qualified purchasers as defined by the SEC and has therefore not been adapted to retail clients.

EUROPEAN UNION

This material is disseminated in the European Union by Unigestion Asset Management (France) SA which is authorized and regulated by the French “Autorité des Marchés Financiers” (« AMF »).

This information is intended only for professional clients and eligible counterparties, as defined in the MiFID directive and has therefore not been adapted to retail clients.

CANADA

This material is disseminated in Canada by Unigestion Asset Management (Canada) Inc. which is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario, Quebec and Newfoundland & Labrador. Its principal regulator is the Ontario Securities Commission (« OSC »). This material may also be distributed by Unigestion SA which has an international advisor exemption in Quebec, Saskatchewan and Ontario. Unigestion SA’s assets are situated outside of Canada and, as such, there may be difficulty enforcing legal rights against it.

SWITZERLAND

This material is disseminated in Switzerland by Unigestion SA which is authorized and regulated by the Swiss Financial Market Supervisory Authority (« FINMA »).

Document issued October 2021.