Volatility Creates Opportunity: Managing Risk and Pursuing Rewards in Emerging Market Equities

- We believe the current divergence between emerging and developed markets is a temporary situation.

- Although recent reforms may keep volatility elevated in the short term, we believe it will lead to a healthier and more balanced Chinese economy.

- We have developed macro-based dynamic signal arbitraging between absolute and active risk management which helps to systematically adapt our portfolio to different market regimes and cycles.

- Combining human judgment with machine learning has allowed us to anticipate negative market moves and prevent sizeable losses.

When things start to decline – there are bad headlines in the papers and on television – will you have the stomach for the market volatility and the broad-based pessimism that tends to come with it?

Executive Summary

Despite recent market turbulence, the longer-term outlook for emerging markets looks optimistic, underpinned by rising dispersion, attractive valuations and improving fundamentals. The low-risk style is well-positioned in the current environment.

However, as the sources of risk become ever more diverse, managing risk has become increasingly challenging and complicated. Therefore, to effectively manage long-term risk in conjunction with short-term noise, active investors need to take calculated risks and fortify low-risk portfolios with a holistic approach that encompasses fundamental quality control, better ESG and carbon characteristics, diversified style exposures and the avoidance of valuation extremes. Alternative and big data sets can help investors identify and address hidden (non-linear and clustered) risks as well as navigating different macro regimes.

Emerging Markets: Not All Doom and Gloom

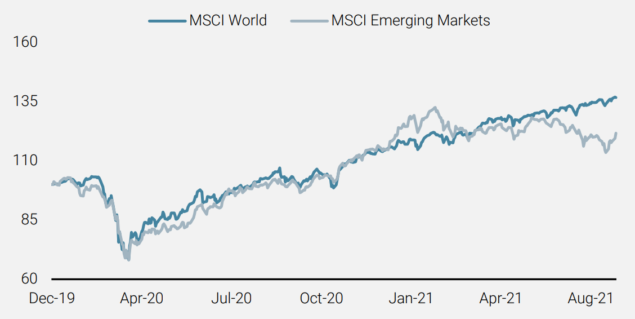

Stocks in Hong Kong and on mainland China have been among the world’s worst performing major equity gauges this year, at a time when the US equity markets have been setting record highs. In particular, regulatory reforms continue to depress Chinese stocks. In July, shares in China were down by more than 13%, which contributed to an 8.5% difference in returns between developed markets (DM) and emerging markets (EM)1. Year-to-date, EM equities have returned 2.8% versus 18.0% for their DM counterparts, with volatilities of 16.0% and 10.7% respectively2. This performance differential is illustrated in Figure 1. However, we believe the current storm is temporary and the situation is far from all doom and gloom.

Figure 1: Diverging Performance Between Emerging and Developed Markets in 2021

Source: Unigestion. As at 31 August 2021.

We experienced this type of turbulence back in 2011, 2015, and 2018. During these periods, the turbulence was unrelated to the economic cycle and markets were unsettled, instead, by China’s regulatory reforms and geopolitical risks, such as the restriction on margin financing from the Chinese Securities Regulatory Commission (CSRC) in both 2011 and 2015, and the trade war between Beijing and Washington in 2018.

Previous reforms have all led to market anxiety, but also a subsequent recovery.

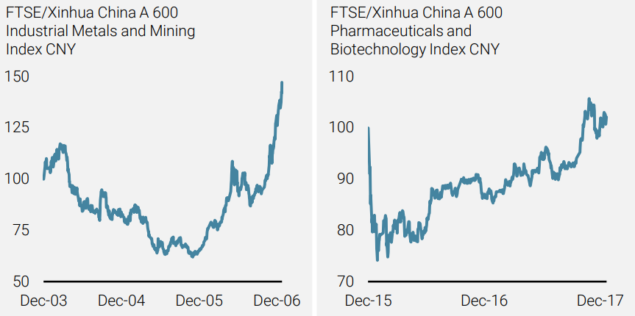

While the historical record does not ease the pain of the current sell-off, we believe it provides insightful context on recent volatility. For example, like the current crackdown in specific industries such as education and gaming, the reform of the steel industry led by the National Development and Reform Commission in 2004/053 and that of the pharmaceutical industry by China’s national food and drug regulator in 20164, all caused market anxiety, but also a subsequent recovery. This is demonstrated in Figure 2. In addition, MSCI Inc.’s Chairman and CEO Henry Fernandez summed this up well in a recent interview with Bloomberg: “Every three, four, five years and obviously the markets have sold-off at the time. But very quickly afterwards, the markets have recovered and gone through to new heights”5.

Figure 2: Rebounding Fast: Melting Steel and Tumbling Pharmaceuticals

Source: Unigestion. As at 31 August 2021.

In our view, there will be more regulatory action and further clarity on the various guidelines coming out in the months ahead – similar to our aniticpation about the introduction of the National Press and Publication Administration’s (NPPA) new online gaming rules from the end of August. Having knowledge of these regulatory guidelines helps investors assess the impact on a particular sector’s companies. While some industries and companies face heightened uncertainty, other business areas, which are more aligned with the government’s policy priorities, could offer additional investment opportunities.

The current reforms may keep volatility elevated in the short term, but we believe it will lead to a healthier and more balanced Chinese economy.

The current reforms may keep volatility elevated in the short term, but we believe it will lead to a healthier and more balanced Chinese economy, which translates into attractive medium- to long-term growth prospects for the Chinese equity market. Looking at emerging markets more broadly, we think they are likely to remain resilient in the face of current challenges, be they China’s regulatory crackdown or the sporadic Covid-19 resurgence.

At Unigestion, the current market conditions in EM are guiding us to exploit volatility and provide investors with a potentially attractive entry point to harvest the low-risk premium with intelligent risk-taking. In the following sections, we explore the new dawn in EM, and how the risk-managed approach can navigate the current and future storms, delivering positive outcomes for investors who have a long-term investment horizon and can stomach the volatility (intelligently).

Increasing Alpha Opportunities in Emerging Markets – A Compelling Prospect

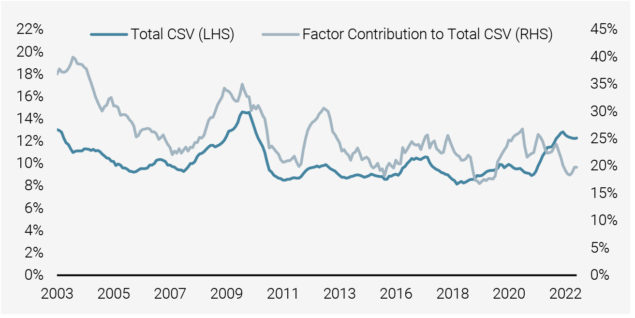

Since the pandemic, the dispersion in EM, measured as cross-sectional volatility (CSV), has picked up significantly, indicating a higher degree of individual stock variation. The result is an increasing breadth and number of opportunities within the EM universe, as illustrated in Figure 3.

Since the pandemic, the dispersion in emerging markets has picked up significantly (the highest level for a decade), indicating a higher degree of individual stock variation. The result is an increasing breadth and number of opportunities, paving the way for alpha opportunities.

Furthermore, investors can decompose the CSV into the common factor contributions (such as country, industry and style) and stock-specific components. In general, when CSV is high, it would receive more contributions from the factor risk group, and less stock-specific contributions as stock correlations are on the rise. However, the current period is unique due to the rising CSV being associated with decreasing contributions from common factors, which implies a lower level of stock correlations, and higher stock-specific contributions. Ultimately, this results in fertile ground for an active manager to capture more alpha opportunities with a focus on managing the full spectrum of risks including country, sector, style, stock-specific, macro, geopolitical and ESG, among others.

Figure 3: High Dispersion is Paving the Way for Alpha Opportunities

Source: MSCI. As at 31 August 2021.

Valuations Appear Attractive, So Follow the Flows

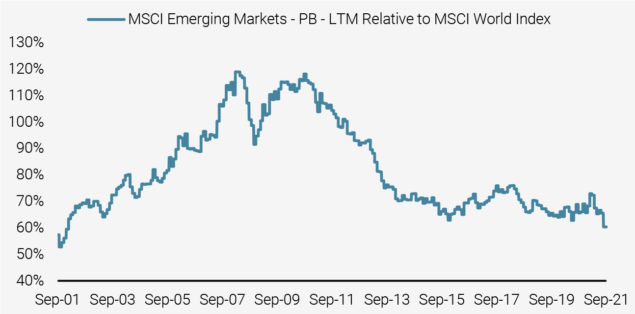

EM continue to provide investors with an appealing entry point with their relatively attractive valuations on a sector-adjusted basis. As shown in Figures 4a and 4b, the price-to-book value of EM stocks sits at the historical average level of 1.6x – a 40% discount to DM. In addition, EM are currently trading at approximately 13 times forward earnings, as shown in Figure 4c. This compares to a level of 18 a year ago, according to Bloomberg. This is almost double the advance seen for DM, which have a valuation multiple of about 206.

Most valuation metrics suggest attractive entry points for emerging market equities.

Figure 4A: Current Valuations Provide Attractive Entry Points

Source: Unigestion. As at 31 August 2021.

Figure 4B: Relative Valuations Also Look Compelling

Source: MSCI, Bloomberg, Factset and Unigestion. As at 31 August 2021.

Figure 4C: Relative Valuation on Forward P/E

Source: MSCI, Bloomberg, Factset and Unigestion. As at 31 August 2021.

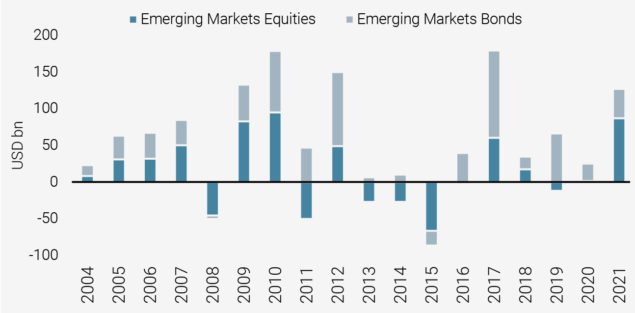

For those investors who are still not convinced, fund flows data (Figure 5) is showing that EM equity funds have already taken in USD 81bn year-to-date, according to flow data provider EPFR7. This has been driven by fast movers who continue to close their underweight positions in the asset class.

Figure 5: Trend in Fund Flows

Source: EPFR, JPMorgan and LAM. As at June 2021.

The Low Risk Factor is Roaring Back to Life

Over the past 12 to 18 months, we have experienced the unprecedented pandemic shock, the post-pandemic cyclical recovery, the tailwinds from extraordinary central bank support and possibly the headwinds from fiscal retrenchment. All of these factors have ensured the continuation of EM volatility. The latest swings have been evident not only at the broad market performance level but also in terms of styles within EM.

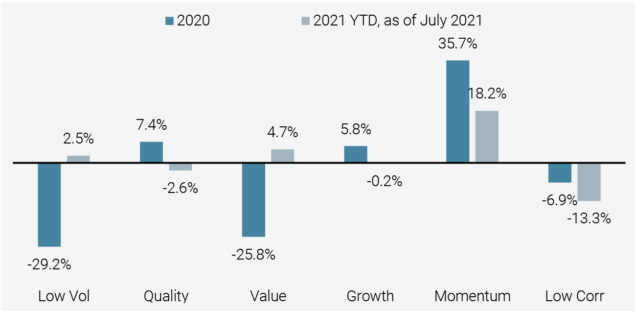

The pandemic, subsequent recovery, central bank support and fiscal retrenchment have created a volatile environment for emerging market equities over the last 18 months. Low Volatility and Value have staged a comeback.

In the first half of 2021, volatile inflationary expectations, on the back of economic recovery and further fiscal stimulus, drove a massive rotation in factors, significantly reflating both Low Volatility and Value, while all other factors displayed only weak improvements or declining returns. After an overwhelming rotation into stocks with higher value and lower growth characteristics, the Momentum factor continued its positive performance in chasing the recent winners, as shown in Figure 6.

Figure 6: Factor Rotation YTD and in 2020

Source: MSCI, Bloomberg and Unigestion. As at 31 July 2021.

Besides these traditional risk premia factors, it is crucial to highlight the importance of the Growth factor, which is a key influencer in EM. There are periods (subject to over/underweight exposures to it) that it drives the out/underperformance of EM managers when the Growth style is in favour, such as in 2019 and 2020. In our low-risk investment process, our systematic combination of top-down style constraints and bottom-up stock selection with multiple style considerations allows us to seek return consistency regardless of broad market leadership. Moreover, from an active risk perspective, our process helps investors avoid a significant part of the systematic active risk being attributed to a specific factor, such as Growth, while still maintaining a positive exposure to Low Volatility and Quality.

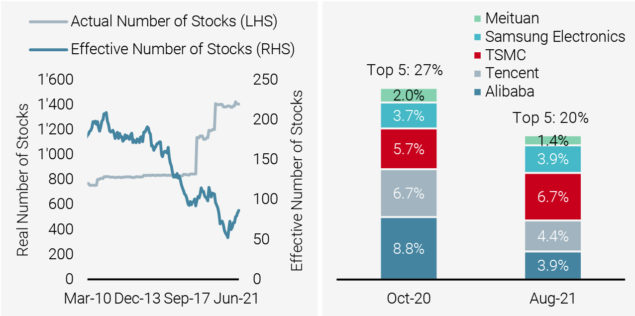

Market Concentration Remains a Challenge

Despite the fact that the recent market sell-off slightly eased the market concentration in EM, as shown in Figure 7, the narrowness of these markets remains a challenge. If the exposure and active risk from these concentrated positions is not managed carefully, it could prove very painful given their dominance in driving index performance.

If the active risk from concentrated positions is not managed carefully, it could prove very painful.

Figure 7: Market Concentration in Emerging Markets

Source: MSCI, Bloomberg and Unigestion. As at 31 August 2021.

According to our research last year8, we have seen that concentration risks in global equity portfolios have increased. This is evident both at the country and individual stock level – the former due to the dominant position of the US within DM equities and China within EM equities, and the latter due to the rise of Asia’s tech giants (Alibaba, Tencent, Samsung, and Taiwan Semiconductor). The high market concentration led to a high concentration of active risk within portfolios.

In particular, we evaluated the concentration of our specific tracking error. Here, we saw that the five largest stocks in the benchmark represented the majority of our active bets, given our very strong underweight in these names previously. Mitigating the risk of concentration (i.e. managing the weight of the respective stock exposures in our portfolio) is important so that the portfolio’s relative performance will be less dependent on just a handful of stocks. We have therefore recently enhanced our portfolio construction process to tighten our maximum active country exposure and impose top-down constraints to avoid a significant part of the systematic active risk being attributed to a specific factor, such as Growth, while leaving our positive exposure to Quality and Low Volatility unchanged. To address stock-specific concentration, we are also systematically managing the active idiosyncratic risk. The ultimate goal of these enhancements is to improve the breadth of upside potential for investors, while also continuing to provide downside protection.

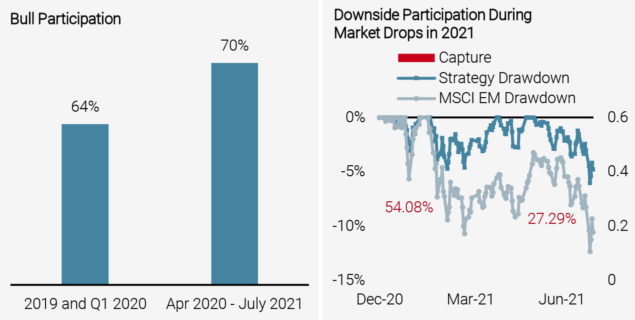

Our emerging market risk-managed strategy has shown robust performance in 2021 with positive excess performance versus both the market cap and min volatility indices.

With these timely enhancements, we are pleased to see our EM risk-managed strategy has shown robust performance in 2021 with positive excess performance versus both the market cap and min volatility indices. Moreover, the recent enhancements have achieved more positive outcomes – increased participation in up and reduced participation in down markets – as shown in Figure 8.

Figure 8: Responding to Market Concentration to Enhance Upside Capture

Source: MSCI, Bloomberg and Unigestion. As at 31 July 2021.

Integrating Macro-Based Dynamic Signals

Inflation has been in the headlines for many EM investors lately. The rise in inflation observed since the beginning of the year has resulted from a combination of rising commodity prices and a lack of significant investment in many sectors constraining supply and limiting the efficiency of the supply chain. Putting the debate about whether current inflation is transitory or persistent to one side, EM equities may be a beneficiary of rising inflation given their positive relationship with commodities. Moreover, if the inflation is accompanied by a strong and healthy economic growth cycle, it could provide a further tailwind to EM equities.

Macro regimes and market cycles are also important in the context that they are significantly correlated to the excess performance of a low-risk strategy, among other equity risk premiums. Hence, together with our Cross Asset Solutions colleagues, we have utilised macro indicators, which track the business cycle and inflation risk in real-time via the aggregation of several hundred macroeconomic, financial and media data series, to develop macro-based dynamic signal arbitraging between absolute risk management and active risk management within our portfolio construction process. This helps us to systematically adapt to different market regimes and cycles.

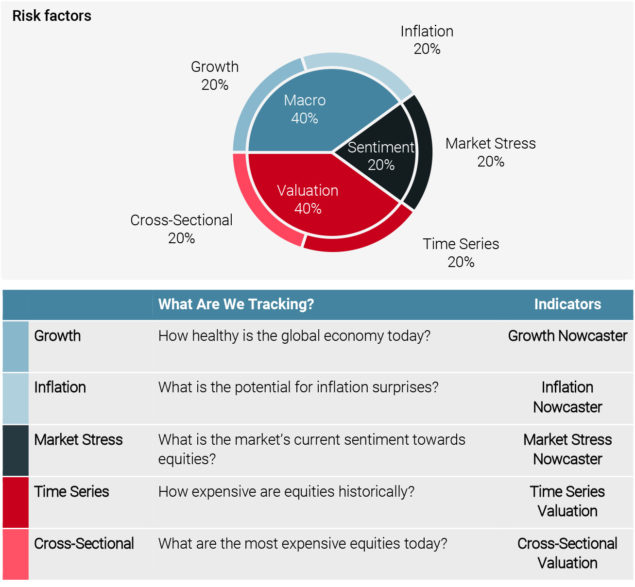

To mitigate the cyclicality and incorporate macroeconomic regimes, we broaden the sources of volatility mitigation by introducing an explicit balance between total risk reduction and active risk control based on macroeconomic and valuation conditions. Using the latest nowcasting techniques and models, we build robust indicators (“Nowcasters”) to evaluate where we currently stand in terms of Growth, Inflation and Market Stress, as shown in Figure 9. Based on the level of these proprietary Nowcasters, their rate of change and the market valuation metrics, we can further determine whether we are at high or low risk of experiencing a recession, an inflation shock, an episode of market stress, or whether there is a “steady growth” environment that prevails.

Figure 9: Improved Returns with Stable Risk Reduction

Source: Unigestion. As at August 2021.

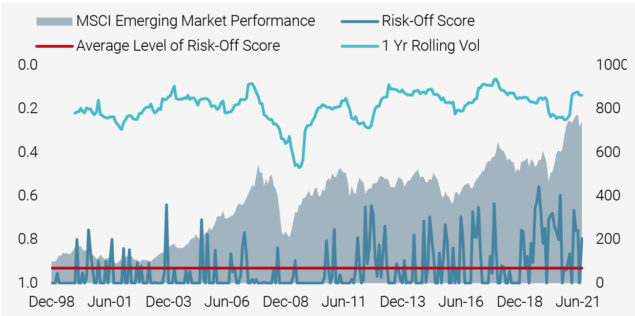

Furthermore, we also integrate these macroeconomic signals into our systematic investment process to dynamically balance the absolute risk management objective of the strategy with the need to control active risk. In other words, dynamically tilting the portfolio between full defensiveness (risk-off) and adaptive (risk-on), as shown in Figure 10.

Figure 10: Risk Positioning of Our Emerging Markets Strategy

Source: MSCI and Unigestion. As at 31 August 2021.

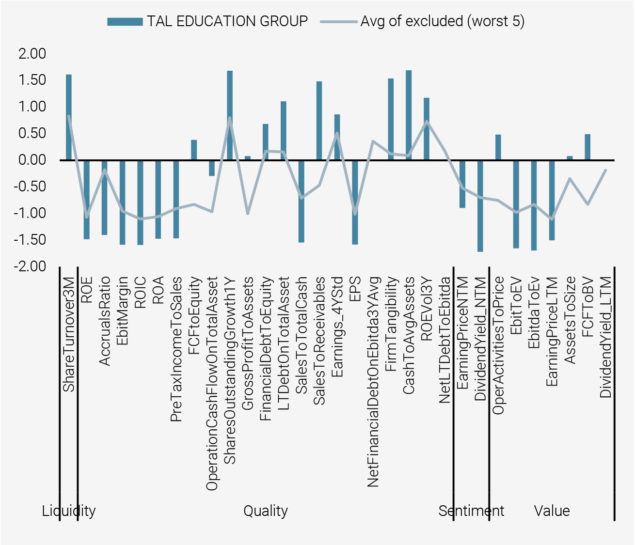

Combining Human Judgement with Machine Learning

American Depositary Receipts (ADRs), historically a favoured route to access the Chinese equity market, are under threat due to the geopolitical tensions between the US and China. Our fundamental research analysts and EM working group therefore have to assess the risk associated with each ADR position and invest on a case-by-case basis. Subsequently, we have formulated a risk mitigation plan that only considers Chinese ADRs with a dual listing (in the US and Hong Kong) and that synchronises the “homecoming” trend – i.e. Chinese ADR stocks that are rushing back to Hong Kong for IPOs.

Combining human judgment with machine learning has allowed us to anticipate negative market moves and prevent sizeable losses.

While carrying out the fundamental analysis on ADRs, it is intriguing to see that the use of machine learning filters actually helped us to better exclude stocks with large tail risks in the portfolio construction process well before the market sell-off, such as TAL Education Group. As shown in Figure 11, the company failed on several key machine learning filters. As a result, our systems suggested liquidating the position well before the turmoil of education stocks came into play and ultimately prevented sizeable losses for the strategy.

Figure 11: Most Important Features of Machine Learning Forecasts: Z-scores, June 2021

Source: MSCI and Unigestion. As at June 2021.

No Greenwashing but Build on the Paris Climate Accord

As climate risks increase worldwide, we are seeing governments responding in the form of regulation (e.g. the recent guidance on EU climate transition benchmarks and EU Paris-aligned benchmarks), carbon taxes and public investment, as well as shifts in consumer sentiment and business models. The transition away from fossil fuels (stranded assets) toward more sustainable and clean energy could transform the global economy and create significant investment opportunities.

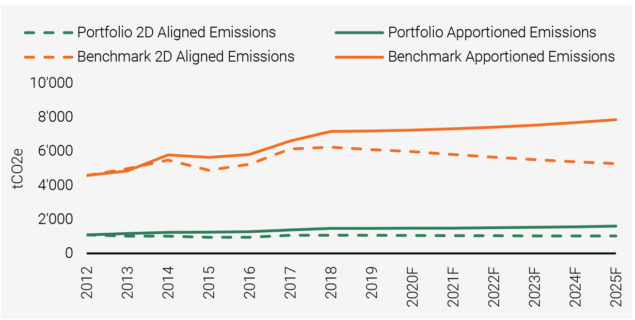

Decarbonisation is only the start of the journey. Integrating carbon constraints allows us to significantly reduce carbon risk exposure as measured by carbon intensity. However, this straightforward approach to transition risk makes a number of implicit assumptions, such as all companies effectively pay the same carbon price. This has led us to evaluate our EM strategy’s (and that of our other risk-managed strategies) levels of alignment with global climate goals based on a transition pathway approach in which the rate of decarbonisation of each holding is assessed against rates required to achieve 2°C or below 2°C of warming.

As Figure 12 shows, the apportioned greenhouse gas emissions (the green line) of our low risk emerging market strategy is approximately only 4,984 tCO2e9 over the 2°C carbon balance (the green dotted line) over the 2012-2025 period. This is lower than the corresponding benchmark’s emissions trajectory (the orange line), where apportioned emissions are 15,380 tCO2e higher than the carbon budget associated with a 2°C level of warming (the orange dotted line). In other words, our low volatility strategies would have a smooth and fair transition. At Unigestion, we are committed to achieving Paris alignment and are actively enhancing our processes to control the temperature of low risk portfolios and align them relative to the 2°C trajectory.

Figure 12: Portfolio Transition Pathway – Apportioned GHG Emissions

Source: MSCI and Unigestion. As at March 2021.

Given the climate risk dimension also directly aligns with global climate-focused initiatives like the UN’s Sustainable Development Goals (SDGs), we could also potentially target transition opportunities by focusing (tilting) on specific areas such as green technologies or renewable energies. As such, the strategies would make significant contributions towards SDG 7 (affordable and clean energy).

By combining climate risk analysis with asset specific modelling, we can help investors manage risk from multiple dimensions.

By combining climate risk analysis with asset specific modelling, we could help investors manage risk from multiple dimensions and adjust asset allocation accordingly, ultimately fulfilling multiple goals during their investment horizons.

Looking Ahead

China’s regulatory reforms could be disruptive in the short term, but as long-term investors, we should focus on enduring positives. Recent crackdowns in the country’s education, gaming and real estate sectors have driven up risk premia in other sectors such as pharmaceuticals, health care and its supply chains, clean energy and utilities. This has provided compelling entry points for resilient, good quality and fair-valued companies that are in line with the government’s long-term development plans and can contribute to economic growth in China. It is our belief that once markets overcome the initial shock of the regulation crackdown, they will eventually accept the new rules when viewed from a different perspective – from the lens of sensible policies that lead to long-term sustainable growth and social welfare. This has been the case with similar policy reforms in the past.

To effectively manage long-term risk, active investors need to take calculated risks and fortify low volatility portfolios with a holistic approach to risk.

Looking ahead, country, industry/sector and stock selection will remain critical from an active EM investing perspective. For investors allocating and expanding their EM allocations, low volatility style allocations can help capture the growth potential of EM while smoothing the returns pattern, particularly during periods of uncertainty. It is also vital to make sure that a resilient portfolio is constructed in such a way as to cushion an allocation from the unique challenges we are facing in 2021 and beyond. As sources of risk continue to grow and become increasingly diverse, managing them has become more challenging. Therefore, to effectively manage long-term risk, active investors need to take calculated risks and fortify low volatility portfolios with a holistic approach to risk, encompassing fundamental quality control, better ESG characteristics, diversified style exposures and the avoidance of valuation extremes. Alternative and big data sets can help investors identify and address hidden (non-linear and clustered) risks as well as assist in navigating different macro regimes.

1Source: Bloomberg, MSCI and Unigestion.

2Source: Bloomberg, MSCI and Unigestion.

3https://www.ndrc.gov.cn/xxgk/zcfb/fzggwl/200507/t20050719_960668_ext.html

4http://www.gov.cn/xinwen/2016-03/20/content_5055575.htm

5https://www.bloomberg.com/news/articles/2021-08-24/china-stocks-can-shrug-off-crackdown-to-reclaim-highs-msci-says

6https://www.bloomberg.com/news/articles/2021-06-04/emerging-market-stocks-in-pole-position-to-gain-as-world-reopens

7https://www.ft.com/content/4546f956-c48e-4530-9eaa-e567fa2856e1

8Unigestion Emerging Markets Equity Strategy: Responding to Universe Concentration to Enhance Upside Capture

9tCO2e stands for tonnes (t) of carbon dioxide (CO2) equivalent (e)

Important Information

Past performance is no guide to the future, the value of investments, and the income from them change frequently, may fall as well as rise, there is no guarantee that your initial investment will be returned. This document has been prepared for your information only and must not be distributed, published, reproduced or disclosed by recipients to any other person. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation.

This is a promotional statement of our investment philosophy and services only in relation to the subject matter of this presentation. It constitutes neither investment advice nor recommendation. This document represents no offer, solicitation or suggestion of suitability to subscribe in the investment vehicles to which it refers. Any such offer to sell or solicitation of an offer to purchase shall be made only by formal offering documents, which include, among others, a confidential offering memorandum, limited partnership agreement (if applicable), investment management agreement (if applicable), operating agreement (if applicable), and related subscription documents (if applicable). Please contact your professional adviser/consultant before making an investment decision.

Where possible we aim to disclose the material risks pertinent to this document, and as such these should be noted on the individual document pages. The views expressed in this document do not purport to be a complete description of the securities, markets and developments referred to in it. Reference to specific securities should not be considered a recommendation to buy or sell. Unigestion maintains the right to delete or modify information without prior notice. Unigestion has the ability in its sole discretion to change the strategies described herein.

Investors shall conduct their own analysis of the risks (including any legal, regulatory, tax or other consequences) associated with an investment and should seek independent professional advice. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment. These are not suitable for all types of investors.

To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks. Actual results could differ materially from those in the forward-looking statements. As such, forward looking statements should not be relied upon for future returns. Targeted returns reflect subjective determinations by Unigestion based on a variety of factors, including, among others, internal modeling, investment strategy, prior performance of similar products (if any), volatility measures, risk tolerance and market conditions. Targeted returns are not intended to be actual performance and should not be relied upon as an indication of actual or future performance.

No separate verification has been made as to the accuracy or completeness of the information herein. Data and graphical information herein are for information only and may have been derived from third party sources. Unigestion takes reasonable steps to verify, but does not guarantee, the accuracy and completeness of information from third party sources. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. All information provided here is subject to change without notice. It should only be considered current as of the date of publication without regard to the date on which you may access the information. Rates of exchange may cause the value of investments to go up or down. An investment with Unigestion, like all investments, contains risks, including total loss for the investor.

Legal Entities Disseminating This Document

UNITED KINGDOM

This material is disseminated in the United Kingdom by Unigestion (UK) Ltd., which is authorized and regulated by the Financial Conduct Authority (« FCA »). This information is intended only for professional clients and eligible counterparties, as defined in MiFID directive and has therefore not been adapted to retail clients.

UNITED STATES

This material is disseminated in the U.S. by Unigestion (UK) Ltd., which is registered as an investment adviser with the U.S. Securities and Exchange Commission (“SEC”). This information is intended only for institutional clients and qualified purchasers as defined by the SEC and has therefore not been adapted to retail clients.

EUROPEAN UNION

This material is disseminated in the European Union by Unigestion Asset Management (France) SA which is authorized and regulated by the French “Autorité des Marchés Financiers” (« AMF »).

This information is intended only for professional clients and eligible counterparties, as defined in the MiFID directive and has therefore not been adapted to retail clients.

CANADA

This material is disseminated in Canada by Unigestion Asset Management (Canada) Inc. which is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario, Quebec and Newfoundland & Labrador. Its principal regulator is the Ontario Securities Commission (« OSC »). This material may also be distributed by Unigestion SA which has an international advisor exemption in Quebec, Saskatchewan and Ontario. Unigestion SA’s assets are situated outside of Canada and, as such, there may be difficulty enforcing legal rights against it.

SWITZERLAND

This material is disseminated in Switzerland by Unigestion SA which is authorized and regulated by the Swiss Financial Market Supervisory Authority (« FINMA »).

Document issued September 2021.