November saw an astonishing rise in risk appetite, buoyed by the election of Joe Biden in the US and the arrival of an effective vaccine that could end the Covid-19 pandemic sooner than expected. Equity markets thrived, posting one of the best monthly returns on record, and the long-awaited rotation finally began with former laggards outperforming strongly. Although questions remain around the distribution of the vaccine and the final impact of the health crisis on economic growth, euphoria could well turn into a prolonged bull market under the combined effects of reduced volatility, ample liquidity conditions and monetary support, and a sustained macro recovery. Within this framework, the case for emerging markets (EM) has improved over the medium term.

Travellin’ South

What’s Next?

Economic growth is vivid

The macro recovery observed in EM since H1 has been anything but tepid, with China leading the pack. Our proprietary Growth Nowcaster has been indicating above potential levels of economic activity since July and has currently stabilised at levels unseen since 2011. While China was initially the main engine to this very sharp recovery, thanks largely to its very stringent yet efficient pandemic management, other countries have recently shown signs of reacceleration, such as Mexico, Russia, India and Brazil to a lesser extent. The rate of improvement in economic data in most of these countries has been solidly anchored in the 60-70% range, and macro sentiment (measured by our high frequency Newscasters) has also been thriving since mid-October.

The path of the recovery in emerging economies is likely to be highly related to the access and distribution of the Covid-19 vaccine. However, tailwinds coming from the resurgence in commodities, effective fiscal and monetary support, and the rotation toward cyclical assets have set the stage for a supportive framework in the months to come.

One risk to this scenario is the potential normalisation in US rates, which would weigh on EM assets due to higher funding costs and the reduced carry that investors would receive on their local currency exposures. However, not all rising rate environments are equal, depending on the phase of the economic cycle and the drivers leading to policy tightening, or normalisation. EM have historically thrived during rising rate environments when the inflation premium is the driver, less so when growth (real yields) is being repriced.

Inflation expectations going into 2021 are building but monetary action is poised to limit the absolute rise in yields at sustainable levels. Real yields are therefore expected to remain low, which is historically supportive to higher yielding and EM assets in particular. In addition, phases of economic recovery are also very favourable for EM assets, especially in the currency space.

Sentiment has been following through

Investors have naturally welcomed the improvement in economic momentum, pushing risk assets materially higher. However, not all assets have reacted the same. While some stock markets have rebounded, recouping most, if not all losses incurred earlier in the year, others have lagged materially so far, notably in the EM FX space.

Following J. Biden’s election in the US and the perspective of a much quieter foreign and trade policy, flows into EM assets have been particularly strong, especially in equity funds. While there could be many arguments supporting prudence toward EM assets, especially the debt overhang weighing on EM countries’ fundamentals and growth prospects, tailwinds going into 2021 seem prominent with improving demand from the DM world, sensitivity to commodities, higher beta to risk appetite and economic strength in China.

Furthermore, liquidity remains plentiful and the tap from major central banks is not expected to be turned off in the year to come. US dollar money market funds have grown a staggering USD 700bn in 2020. Reduced uncertainty on the geopolitical and health fronts will help unleash this pent-up demand in the months to come, in what could become a new Goldilocks environment if no tail risks materialise. This could particularly benefit the laggards of the EM complex – EM local debt – despite reduced expected returns and currencies. Inflows into the asset class in the latter part of the year have not yet compensated outflows incurred during the Covid crisis, unlike hard currency flows that are now net positive in 2020.

Long EM assets, selectively

There is a need to distinguish between global demand for EM assets and idiosyncratic stories affecting specific countries/regions, and diversification remains key when looking at the asset class.

A combination of exposures to cyclical upside and carry through foreign exchange positions offer the best risk reward, with limited downside risk. Expectations for a “lower for longer” rates environment in the US and the introduction of average inflation targeting makes upward pressure on the US dollar less likely, and will keep higher yielding assets in demand in the fixed income and FX spaces.

A lower volatility context will favour currencies and attractive carry trades before exceptional liquidity starts to shrink. A basket of the four of the highest yielding crosses (BRL, MXN, ZAR, INR) is still down 14% year-to-date, while the MSCI EM equity index is now up 12%. This comes as a result of many different factors including EM healthcare infrastructure, the bloc’s capacity to deal with the health situation during winter in the southern hemisphere and, most importantly, central banks’ action on interest rates, cut significantly this time around relative to other historical crises. On average, short term rates have been lowered by 260bps in Brazil, Mexico, South Africa and India in 2020 whereas the Fed only cut rates by 150bps and the ECB preferred unconventional action leaving repo rates unchanged.

Looking forward, the combination of improving macro conditions, global risk appetite, lower uncertainties surrounding global trade and attractive carry constitute a strong investment case for the asset class over the medium term. Therefore, our strategies are now dynamically overweighted to EM assets broadly, with a preference within it for EM credit and selected high carry FX crosses.

Unigestion Nowcasting

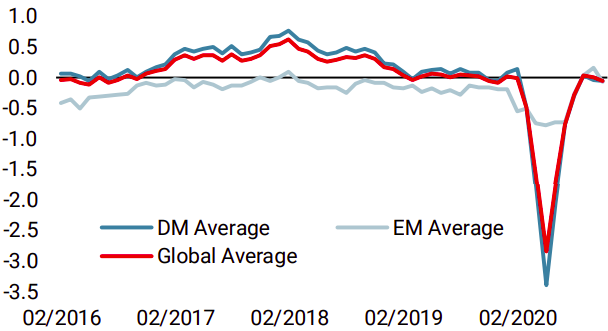

World Growth Nowcaster

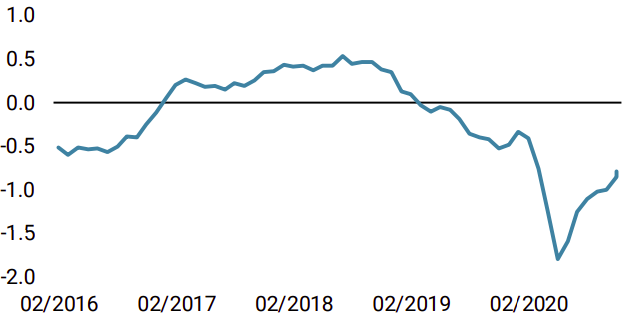

World Inflation Nowcaster

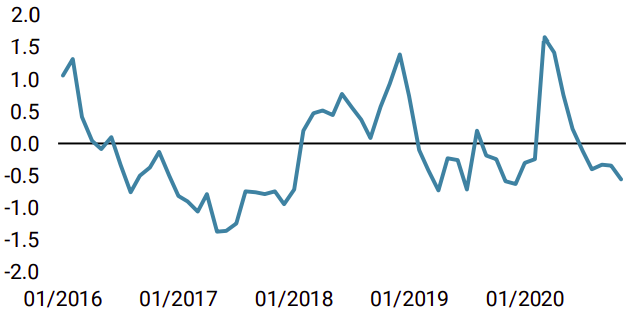

Market Stress Nowcaster

Weekly Change

- Our World Growth Nowcaster decreased last week as US data further improved but Chinese data showed a significant deterioration. Overall, the Growth Nowcaster remains high despite a week of decline.

- Our World Inflation Nowcaster increased slightly last week. Overall, inflation surprise risk is neutral.

- Last week, our Market Stress Nowcaster declined marginally as option-implied volatilities approached lower territory.

Sources: Unigestion. Bloomberg, as of 30 November 2020.

Important Information

This document is provided to you on a confidential basis and must not be distributed, published, reproduced or disclosed, in whole or part, to any other person.

The information and data presented in this document may discuss general market activity or industry trends but is not intended to be relied upon as a forecast, research or investment advice. It is not a financial promotion and represents no offer, solicitation or recommendation of any kind, to invest in the strategies or in the investment vehicles it refers to. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment.

The investment views, economic and market opinions or analysis expressed in this document present Unigestion’s judgement as at the date of publication without regard to the date on which you may access the information. There is no guarantee that these views and opinions expressed will be correct nor do they purport to be a complete description of the securities, markets and developments referred to in it. All information provided here is subject to change without notice. To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks.

Data and graphical information herein are for information only and may have been derived from third party sources. Although we believe that the information obtained from public and third party sources to be reliable, we have not independently verified it and we therefore cannot guarantee its accuracy or completeness. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. Unless otherwise stated, source is Unigestion. Past performance is not a guide to future performance. All investments contain risks, including total loss for the investor.

Unigestion SA is authorised and regulated by the Swiss Financial Market Supervisory Authority (FINMA). Unigestion (UK) Ltd. is authorised and regulated by the UK Financial Conduct Authority (FCA) and is registered with the Securities and Exchange Commission (SEC). Unigestion Asset Management (France) S.A. is authorised and regulated by the French “Autorité des Marchés Financiers” (AMF). Unigestion Asset Management (Canada) Inc., with offices in Toronto and Montreal, is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario and Quebec. Its principal regulator is the Ontario Securities Commission (OSC). Unigestion Asia Pte Limited is authorised and regulated by the Monetary Authority of Singapore (MAS). Unigestion Asset Management (Copenhagen) is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Danish Financial Supervisory Authority” (DFSA). Unigestion Asset Management (Düsseldorf) SA is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Bundesanstalt für Finanzdienstleistungsaufsicht” (BAFIN).