- While investment activity rebounded to pre-COVID levels in H2, exit activity saw an overall steep decline in 2020, leading to large negative cash flows to investors.

- We predict that in 2021 the secondaries market will resume its strong pre-COVID growth on the back of a surge in GP-led opportunities, especially at the small end of the market, as well as larger LPs rebalancing their portfolios.

- Unigestion contributed EUR 673m to investments in 2020 while receiving EUR 425m in distributions.

Overview

As private equity investors continue to come to terms with the new normal imposed by the pandemic, we can reflect on a year of challenges and opportunities. Private equity investment and exit activity was understandably hit in the first half of 2020. However, while investment activity rebounded rapidly in the second half of the year, exit activity has yet to recover. Consequently, aggregate capital calls were considerably higher than distributions, leading to the largest negative cash flows to investors since 2008. Nevertheless, this did not entirely dampen investor enthusiasm as fundraising was only down by 20%1. Many private equity firms saw this as an opportunity to build up dry powder in anticipation of attractive opportunities coming from the current environment.

Exit activity falls off a cliff

The global aggregate value of private equity deals closed during 2020 was EUR 595bn, 23% down on the previous year. This was largely driven by a material decline in North America (-29%) with declines also in Europe (-18%) and APAC (-14%). While the first half of the year was hit by the onset of the pandemic, the second half of the year was much stronger with an almost 10% increase over H2 2019.

However, exit activity did not enjoy such a recovery. The global aggregate value of exits in 2020 was a meagre EUR 358bn, a 50% decline on the previous year. Both Europe (-54%) and APAC (-52%) were the drivers of this drop although North America (-40%) was also materially down.

Investors largely remained unperturbed by the market turbulence. Despite the constraints in place across most of the world, fundraising was remarkably robust. However, this was driven by several large cap funds closing well above USD 10bn, including CVC, EQT, Silver Lake and Platinum Equity. Anecdotally, investors found it easier to gain comfort to re-invest with the larger blue chip names than the smaller firms.

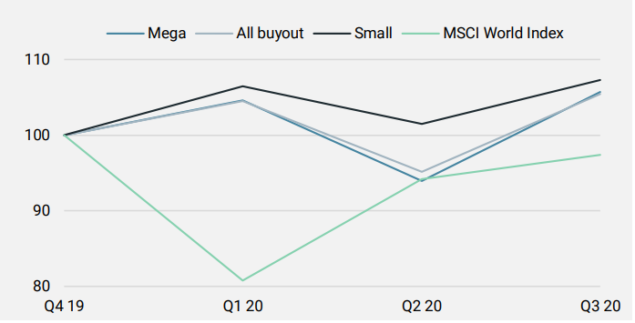

Figure 1: Quarterly performance

Source: Preqin (Private Capital Quarterly Index – PCQI) and MSCI as at January 2021. The PCQI captures average returns across funds (index at 31 December 2019 rebased to 100).

In addition, as shown in Figure 1, investors were rewarded with robust private equity performance during 2020. Driven by the initial uncertainty of how portfolio companies would perform during the pandemic as well as depressed public market comparable valuations, performance dipped in Q2. However, by 30 September, average performance was up by 5% for the year. For the same time period, the MSCI World Index was down by 3%.

Interestingly, the performance of small buyout funds did not go negative at all for the year up to 30 September, posting a 7% increase. This consistent performance was likely driven by the more limited use of leverage at this end of the market compared to the larger end of the market.

The performance of small buyout funds did not go negative at all for the year up to 30 September, posting a 7% increase. We have seen similarly robust performance in our own portfolios.

We have seen similarly robust performance in our own portfolios. For example, two of our maturing secondary strategies showed a 7.2% and 8.2% increase in TVPI respectively for the year to 30 September. This is a testament to our approach of building portfolios of high quality companies and playing investment themes which drive growth irrespective of macro conditions, rather than relying on financial engineering.

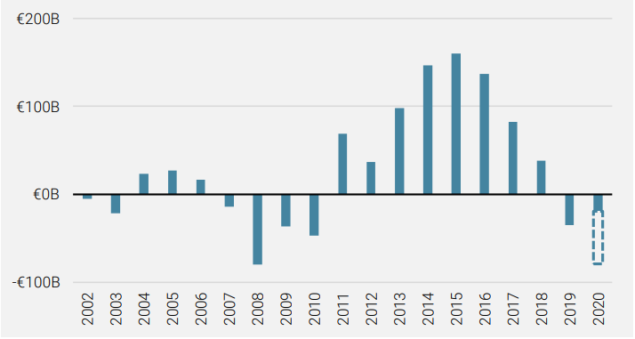

Probably the most critical issue for investors coming into 2021 has been cash flow management. With distributions drying up, some investors may find it difficult to continue funding capital calls without liquidating other parts of their portfolios.

Figure 2: Net cash flows to investors (EUR bn)

Source: Preqin; for 2020, solid bars indicate H1 2020, while dashed bars indicate estimates for H2 2020

As shown in Figure 2, aggregate net cash flows to investors were at their most negative since 2008. Under pressure to generate liquidity for their investors, many GPs have resorted to GP-led single or multi-asset restructurings. These have become a particularly attractive way of solving the tension between investors’ desire for liquidity and GPs’ desire not to sell assets at a sub-optimal time.

Since September, we have closed the first five deals of our latest secondaries strategy, and will imminently close several other deals. The common thread is that they are all GP-led deals, either generating liquidity for existing investors or providing capital to the best performing portfolio companies when existing investors are maxed out. For example, in December, we invested into the single-asset restructuring of Datamars, a leading global provider of livestock, pet and textile identification solutions. Having owned the asset for nine years, Columna Capital, the GP, wanted to give liquidity to its investors but still saw opportunities for the company to make further acquisitions, move into adjacent verticals and further grow market share.

Our PE outlook for 2021

Overall, 2020 turned out to be a very different year to what was initially expected. Nevertheless, we were either correct or very close in all five of our 2020 predictions. First, pricing for small and mid-market deals, and large and mega deals did not go in different directions as predicted. However, while falling in both cases, small and mid-market pricing fell further (from 10.4x to 8.8x EBITDA2) than large and mega pricing (13.4x to 12.1x). Second, while the secondary market contracted last year, the volume of GP-led deals increased as expected (from USD 26bn to USD 35bn3).

As larger LPs look to rebalance their portfolios and more GPs seek to tap into the secondary market for their own cash management needs, we think that secondaries are set for a big year.

Third, even though overall fundraising was down for the year, European venture capital had its best ever year in terms of total capital raised (USD 17.6bn vs USD 11.3bn raised in 20194). Admittedly, this was not a European-only phenomenon as a similar trend was seen in the US. Technology was clearly a key theme for investors in 2020.

Fourth, ESG has indeed increased in focus for investors and GPs. This is not only because the imminent SFDR regulations are requiring fund managers to focus much more on ESG risks but also because ESG is increasingly viewed as a key value creation tool.

Finally, although difficult to measure, we said that a wall of GP succession issues would lead to new opportunities. If we look at our own deals sourced and completed throughout 2020, a large number of them have come from new GPs. In 2020, specifically with emerging managers, we made four new commitments, seven GP-led transactions and three direct investments.

In the best of times, it is not easy to peek into the future and predict how a given year will turn out. Nonetheless, we hope that our 2021 outlook provides some interesting reading and insight into the market trends in both the short and long term.

The secondaries market will resume its strong pre-COVID growth. The market came back remarkably quickly following the first lockdown in Q1/Q2, especially at the nimbler, small end of the market. H2 2020 volume suggests that secondary transaction pace was already close to 2019 levels. As larger LPs look to rebalance their portfolios and more GPs seek to tap into the secondary market for their own cash management needs, we think that secondaries are set for a big year.

In the face of a subdued exit market, GPs will continue to seek alternative liquidity strategies. We think that GPs will be motivated to generate liquidity from their best companies in 2021 using whichever option optimises the outcome. However, trade sales will take time to recover while IPOs will remain an option only in a minority of cases. Secondary buyouts will gather steam as GPs look to deploy dry powder but GP-led transactions will reach a record high. As mentioned above, such transactions allow GPs to hold on to their best assets but still give some liquidity back to LPs. However, at the smaller end of the market, GPs are still less sophisticated and less familiar with this route – requiring the need for more hands-on and innovative secondary managers.

There will be record numbers of small and mid-market PE firms in the market for raising new funds. In 2020, LPs sought refuge and comfort in the large cap brand names, leading to robust fundraising at the large end of the market. There is now considerable pent up demand for small and mid-market exposure and investors will seek to rebalance their portfolios accordingly in 2021. However, there will be a clear “flight to quality” as certain GPs will raise easily (e.g. those who demonstrated good performance during the crisis) and others may eventually give up.

There will be a record number of managers raising a first time fund. The crisis has caused many PE professionals to reconsider their future careers at the large incumbent firms. Driven by the motivation to run their own firms, specialise in certain sectors and/or invest in the smaller, more entrepreneurial segments of the market, we expect many experienced PE professionals to spin-out and raise first-time funds. This presents an attractive opportunity for investors to back some of the future stars. However, the bar will remain very high and not all will be successful.

There will be a spike in the flow of co-investments and co-underwriting opportunities. Given the record number of small and mid-market and first time managers raising funds, we anticipate that many of them, even established ones, will fall short of their fundraising targets or not raise a fund at all. As a consequence, we anticipate a strong flow of co-investment and co-underwriting opportunities as fund managers require support from experienced co-investors to pursue their strategies.

We anticipate a strong flow of co-investment and co-underwriting opportunities as fund managers require support from experienced co-investors to pursue their strategies.

Despite the continued crisis, PE investment activity in 2021 will rebound to the heights last reached in 2019. In the second half of 2020, PE managers proved themselves adept at closing deals despite the various constraints in place. In 2021, we anticipate that there will be an increasing flow of opportunities coming from motivated sellers such as families looking to cash out, corporates wanting to offload non-core assets and companies needing capital for growth or to make acquisitions, especially at the small end of the PE market. However, there will be challenges. Firstly, valuations are high in certain COVID-resilient sectors such as healthcare and software. Secondly, it will not be easy for investors to diligence rigorously such opportunities. For example, 2021 will be the year of “COVID-adjusted EBITDA”, requiring a deep operational understanding of the industry and the company in order to assess performance clearly over the last 12 months.

Whatever happens, we see this as a useful exercise to study and question current trends in order to glean future opportunities.

Unigestion Private Equity Activity

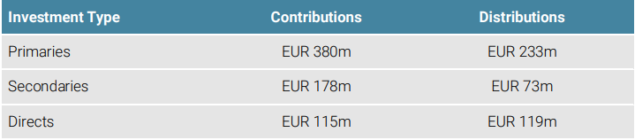

Despite the crisis, 2020 has been one of the busiest years ever for the Unigestion Private Equity team. Unigestion contributed EUR 673m to investments. We have closed commitments to ten new primary funds, covering North America and various regions in Europe. In addition, we completed 11 new direct deals and 12 secondary transactions. During a year when exit activity was down by 50%, Unigestion generated significant liquidity from its portfolio, receiving total distributions of EUR 425m.

Figure 3: Investment Activity in 2020

Source: Unigestion, January 2021.

In October, we completed a GP-led restructuring of four companies in the DACH (Germany, Austria & Switzerland) region. The main value driver of the portfolio, Empolis (www.empolis.com) provides decision support software as a service (SaaS), using semantic analysis, real-time data and machine learning, to government authorities and industrial companies. Both Afinum, the fund manager, and the management teams are investing significantly into the transaction, securing a strong alignment. Afinum, who has owned the portfolio companies for many years, is well positioned to manage the assets going forward and drive the future value generation.

In October, we committed to Verdane Edda II, a Nordic-based manager targeting lower mid-market growth companies in the Nordic countries and in Germany. Verdane Edda makes control investments in fast-growing tech-enabled businesses focusing mainly on the software and digital consumer segments. These businesses benefit from the fundamental shift to the new economy. Verdane is the Nordic leader in its segment with state-of-the-art deal sourcing capabilities and investment processes, which the team has developed over almost two decades.

In November, we invested in CEDES (www.cedes.com). CEDES, based in Switzerland, has been developing sensor and automation solutions for elevators, escalators and automatic doors since 1986. Beginning life as a two-person start-up in a kitchen, CEDES now employs around 400 people worldwide as a global reference in optical sensors utilizing active infrared technology and image processing. Seen as an innovation leader by its blue-chip client base, the company benefits from rising global safety standards, as well as growing urbanisation in the emerging markets.

In the same month, we invested in Wytech (www.wytech.com), a US precision manufacturer of specialty components for medical devices. These devices are used in minimally invasive procedures serving resilient medical end markets, including neurovascular, cardiovascular and orthopaedic. Founded in 1975, Wytech has demonstrated the ability to adapt and innovate and be recognized as a top tier partner to leading medical device OEMs worldwide. Having been a family-owned business with limited capital for growth, our investment will now give it the opportunity to expand into adjacent end-markets such as endoscopy and gastroenterology both organically and through selective acquisitions.

In December, we invested in FORM.com (www.form.com), a mobile data collection platform. FORM.com supports its blue chip customers (Coca Cola, Walmart, Fannie Mae) to digitise manual data entry processes (e.g. inspections of work place safety requirements; and audit of documents in a bank branch). Our investment will finance the acquisition of GoSpotCheck helping the company to expand into the food & beverages and consumer goods markets. FORM.com’s mobile data collection and workflows combined with GoSpotCheck’s mobile task management and image recognition capabilities will help customers collect data in real time, and make better decisions faster.

In December, we invested in ACADEMIA (www.academia-analytics.com), a network of specialty laboratories managed by physicians in Germany. Our investment will finance the acquisitions of other specialty laboratories across pathology, hematology and human genetics. Value will be created by acquiring at low multiples, scaling up the platform and improving medical decision making through digitisation and data sharing across the group.

In December, we invested in EXCEL Scientific (www.excelscientific.com), a leading US supplier of sealing films and foils to life science research, university and testing laboratories, as well as pharmaceutical companies and diagnostic providers. Boosted by COVID-related demand, the company should grow revenue by 90% in 2020, thanks to increasing market share by winning new key long-term customers.

In December, we also completed the GP-led single asset restructuring of Adform (www.adform.com), a leading independent fully integrated software provider to advertisers, agencies and publishers enabling them to control and target digital advertising spend. Adform operates in the high-growth digital ad segment which is also the least cyclical part of the advertisement business. The company offers one of the few end-to-end product suites addressing key parts in the complex digital advertisement value chain. The transaction was sourced directly through our privileged relationship with VIA Equity, the GP.

1,2Pitchbook

3Lazard

4Preqin

Important Information

Past performance is no guide to the future, the value of investments, and the income from them change frequently, may fall as well as rise, there is no guarantee that your initial investment will be returned. This document has been prepared for your information only and must not be distributed, published, reproduced or disclosed (in whole or in part) by recipients to any other person without the prior written consent of Unigestion. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation.

This is a promotional statement of our investment philosophy and services only in relation to the subject matter of this presentation. It constitutes neither investment advice nor recommendation. This document represents no offer, solicitation or suggestion of suitability to subscribe in either the investment vehicles to which it refers or to any securities or financial instruments described herein. Any such offer to sell or solicitation of an offer to purchase shall be made only by formal offering documents, which include, among others, a confidential offering memorandum, limited partnership agreement (if applicable), investment management agreement (if applicable), operating agreement (if applicable), and related subscription documents (if applicable). Such documentation contains additional information material to any decision to invest. Please contact your professional adviser/consultant before making an investment decision.

Where possible we aim to disclose the material risks pertinent to this document. The views expressed in this document do not purport to be a complete description of the securities, markets and developments referred to in it. Reference to specific securities should not be considered a recommendation to buy or sell. Unigestion maintains the right to delete or modify information without prior notice.

Investors shall conduct their own analysis of the risks (including any legal, regulatory, tax or other consequences) associated with an investment and should seek independent professional advice. Some of the investment strategies or financial instruments described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment. These are not suitable for all types of investors. Unigestion has the ability in its sole discretion to change the strategies described herein.

To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks. Actual results could differ materially from those in the forward-looking statements. As such, forward looking statements should not be relied upon for future returns. Targeted returns reflect subjective determinations by Unigestion based on a variety of factors, including, among others, internal modeling, investment strategy, prior performance of similar products (if any), volatility measures, risk tolerance and market conditions. Targeted returns are not intended to be actual performance and should not be relied upon as an indication of actual or future performance.

No separate verification has been made as to the accuracy or completeness of the information herein. Data and graphical information herein are for information only and may have been derived from third party sources. Unigestion takes reasonable steps to verify, but does not guarantee, the accuracy and completeness of information from third party sources. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. All information provided here is subject to change without notice. It should only be considered current as of the date of publication without regard to the date on which you may access the information. Rates of exchange may cause the value of investments to go up or down. An investment with Unigestion, like all investments, contains risks, including total loss for the investor.

Additional Information for US Investors

The performance figures are based on estimated fees and expenses as well as on the underlying strategy’s estimated performances given by fund managers, administrators, custodians and third party sources at a given date. Where performance is reflected gross of fees, potential investors should be aware that the inclusion of fees, costs and charges will reduce the overall value of performance. Unless otherwise stated, the performance data source are Unigestion, Bloomberg and Compustat.

This information is provided to you solely to give you background information relating to Unigestion, certain strategies it implements and currently offers. Before making an investment decision with respect to the strategy discussed herein, potential investors are advised to consult with their tax, legal, ERISA and financial advisors. Note that not all strategies may be available or suitable for investment by U.S. investors.

This document may contain forward-looking statements, including observations about markets and industry and regulatory trends as of the original date of this document. Forward-looking statements may be identified by, among other things, the use of words such as “expects,” “anticipates,” “believes,” or “estimates,” or the negatives of these terms, and similar expressions. Forward-looking statements reflect Unigestion’s views as of such date with respect to possible future events. Actual results could differ materially from those in the forward-looking statements as a result of factors beyond a strategy’s or Unigestion’s control. Readers are cautioned not to place undue reliance on such statements. No party has an obligation to update any of the forward-looking statements in this document

Return targets or objectives, if any, are used for measurement or comparison purposes and only as a guideline for prospective investors to evaluate a particular investment program’s investment strategies and accompanying information. Performance may fluctuate, especially over short periods. Targeted returns should be evaluated over the time period indicated and not over shorter periods.

The past performance of Unigestion, its principals, shareholders, or employees is not indicative of future returns.

Except where otherwise specifically noted, the information contained herein, including performance data and assets under management, relates to the entire affiliated group of Unigestion entities over time including that of Unigestion UK. Such information is intended to provide the reader with background regarding the services, investment strategies and personnel of the Unigestion entities. No guarantee is made that all or any of the individuals involved in generating the performance on behalf the other Unigestion entities will be involved in managing any client account on behalf of Unigestion U.K. More specific information regarding Unigestion UK is set forth herein where indicated and is available on request.

There is no guarantee that Unigestion will be successful in achieving any investment objectives. An investment strategy contains risks, including the risk of complete loss.

The risk management practices and methods described herein are for illustrative purposes only and are subject to modification.

Legal Entities Disseminating This Document

UNITED KINGDOM

This material is disseminated in the United Kingdom by Unigestion (UK) Ltd., which is authorized and regulated by the Financial Conduct Authority (“FCA”).

This information is intended only for professional clients and eligible counterparties, as defined in MiFID directive and has therefore not been adapted to retail clients.

UNITED STATES

This material is disseminated in the U.S. by Unigestion (UK) Ltd., which is registered as an investment adviser with the U.S. Securities and Exchange Commission (“SEC”). This information is intended only for institutional clients and qualified purchasers as defined by the SEC and has therefore not been adapted to retail clients.

EUROPEAN UNION

This material is disseminated in the European Union by Unigestion Asset Management (France) SA which is authorized and regulated by the French “Autorité des Marchés Financiers” (“AMF”).

This information is intended only for professional clients and eligible counterparties, as defined in the MiFID directive and has therefore not been adapted to retail clients.

CANADA

This material is disseminated in Canada by Unigestion Asset Management (Canada) Inc. which is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario, Quebec and Newfoundland & Labrador. Its principal regulator is the Ontario Securities Commission (“OSC”).

This material may also be distributed by Unigestion SA which has an international advisor exemption in Quebec, Saskatchewan and Ontario. Unigestion SA’s assets are situated outside of Canada and, as such, there may be difficulty enforcing legal rights against it.

SWITZERLAND

This material is disseminated in Switzerland by Unigestion SA which is authorized and regulated by the Swiss Financial Market Supervisory Authority (“FINMA”).

Document issued February 2021.