Analyst Expections Too Rosy Ahead Of Earnings Season

Q2 2022 corporate earnings season has begun, and the next few weeks will see a majority of firms reporting on their ability to generate revenues and support margins in an environment fraught with economic slowdown and surging inflation. The last few reporting seasons have been characterised by firms handily beating muted earnings estimates, but with policy shifting from supportive to restrictive, this leitmotif may be challenged. Indeed, as the medium-term prospect of recession grows, analyst estimates may be too optimistic. If earnings are heavily revised down, which has yet to happen for developed equities, they would provide a major headwind for equity markets amidst the tumultuous waters they already find themselves in.

Optimistic

What’s Next

Economic and earnings recessions go hand-in-hand

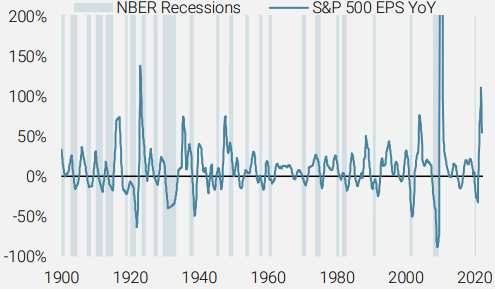

Market participants have shifted from a focus on inflation shock risk to recession risk over the last few weeks: energy commodities have suffered, inflation breakevens have declined, and bond yields have fallen, while equity markets remain volatile. Corporate earnings season has started, with many financials reporting this week, providing a micro-perspective on the balance between growth and inflation in the real economy. Whereas firms can mitigate higher input costs by passing them through to their output prices, thereby supporting their margins, slowing demand is much more challenging for firms to mollify. Figure 1 provides a long-term perspective on earnings-per-share (EPS) growth for the S&P 500, highlighting the unsurprising feature that an economic recession typically leads to an earnings recession.

Figure 1: Trailing S&P 500 Earnings Growth

Source: Bloomberg, Robert Shiller, Unigestion, as of 06 July 2022.

On average since 1900, the S&P 500 has seen earnings fall -5% year-over-year on a monthly basis during a recession, compared to a gain of 16% outside of recessions. Looking at the more recent and relevant past paints a starker picture: since 1970, year-over-year earnings growth has averaged -13% on a monthly basis during recessions compared to 22% outside of recessions.

Where are we today?

The spectre of recession is upon us, whether the Fed would risk it or not. Our Growth Nowcaster shows economic activity significantly below potential and nearing recessionary levels. Over 60% of the underlying data series are deteriorating, suggesting the trend will likely continue. While household consumption has been resilient thanks to significant savings, monetary policy will remain restrictive in the near-term, which will weigh on the labour market and credit conditions. On the positive side, our Global Inflation Nowcaster has ebbed modestly thanks to a retracement in commodity prices, and 65% of its underlying data series have moved lower. While calling the peak in inflation this year has been a challenge, there is strong evidence that inflation may be at a turning point.

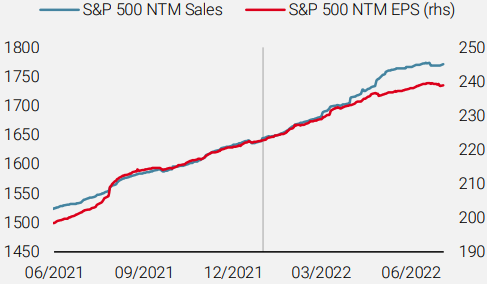

When examining analyst expectations for corporate profitability, the economic slowdown does not seem to be well-reflected. Figure 2 shows analysts’ estimates for aggregate revenue and earnings for the S&P 500 over a rolling 12-month forward window, split by the vertical bar at the start of 2022. As this chart reveals, revenue and earnings have been expected to rise steadily together for the last year with robust margins. More recently, analysts are seeing a retracement in margins, as sales growth expectations rise faster than earnings expectations. Nowhere in these expectations is there much concern about an earnings growth slowdown, never mind an earnings recession.

Figure 2: Next Twelve Months (NTM) Sales and EPS Estimates for the S&P 500

Sources: Bloomberg, Unigestion. Data as at 07 July 2022.

These overly optimistic (in our view) expectations have been a driver of the recent improvement in forward-looking equity valuations, which naively appear to offer attractive entry points. However, once they are revised lower in the face of the current economic slowdown, they will provide additional headwinds for equity markets.

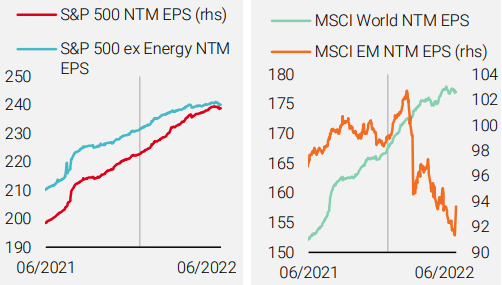

It is important to note that this dynamic is not driven by the energy sector, despite those companies enjoying the largest sales and earnings growth estimates. Indeed, if we consider the S&P 500 Ex Energy index, we get a similar, if less extreme, picture (Figure 3, left chart). Optimistic earnings growth estimates are not only limited to the US: many developed equity markets are displaying a similar phenomenon. As the right chart in Figure 3 shows, the MSCI World index as a whole has seen earnings expectations continue to rise despite hawkish central banks and economic slowdown. While the index is heavily weighted toward the US, which comprises nearly 70% of the index, the same features hold true when looking at individual country indices.

Figure 3: NTM EPS Growth for Various Equity Indices

Sources: Bloomberg, Unigestion. Data as at 06 July 2022.

The right chart in Figure 3 also reveals where earnings estimates have fallen significantly and are looking to bottom out: emerging markets, and China in particular. Analysts have heavily revised earnings estimates there, which are down nearly 10% from their February peak. Combined with slowly improving growth conditions in China, stimulative policy, and depressed price levels, the nascent earnings recovery should provide a tailwind to Chinese and, by extension, emerging market equities.

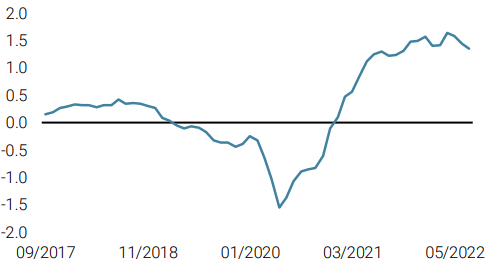

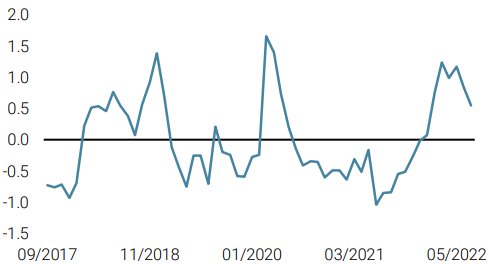

Unigestion Nowcasting

World Growth Nowcaster

World Inflation Nowcaster

Market Stress Nowcaster

Weekly Change

- Last week, our World Growth Nowcaster continued lower amidst slowing growth in the US and Europe.

- Our World Inflation Nowcaster moved down slightly with further easing in inflationary pressures in the US and Eurozone.

- Our Market Stress Nowcaster moved lower last week, as volatility dropped and liquidity improved.

Sources: Unigestion, Bloomberg, as of 11 July 2022.

Important Information

This document is provided to you on a confidential basis and must not be distributed, published, reproduced or disclosed, in whole or part, to any other person.

The information and data presented in this document may discuss general market activity or industry trends but is not intended to be relied upon as a forecast, research or investment advice. It is not a financial promotion and represents no offer, solicitation or recommendation of any kind, to invest in the strategies or in the investment vehicles it refers to. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment.

The investment views, economic and market opinions or analysis expressed in this document present Unigestion’s judgement as at the date of publication without regard to the date on which you may access the information. There is no guarantee that these views and opinions expressed will be correct nor do they purport to be a complete description of the securities, markets and developments referred to in it. All information provided here is subject to change without notice. To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks.

Data and graphical information herein are for information only and may have been derived from third party sources. Although we believe that the information obtained from public and third party sources to be reliable, we have not independently verified it and we therefore cannot guarantee its accuracy or completeness. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. Unless otherwise stated, source is Unigestion. Past performance is not a guide to future performance. All investments contain risks, including total loss for the investor.

Unigestion SA is authorised and regulated by the Swiss Financial Market Supervisory Authority (FINMA). Unigestion (UK) Ltd. is authorised and regulated by the UK Financial Conduct Authority (FCA) and is registered with the Securities and Exchange Commission (SEC). Unigestion Asset Management (France) S.A. is authorised and regulated by the French “Autorité des Marchés Financiers” (AMF). Unigestion Asset Management (Canada) Inc., with offices in Toronto and Montreal, is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario and Quebec. Its principal regulator is the Ontario Securities Commission (OSC). Unigestion Asset Management (Copenhagen) is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Danish Financial Supervisory Authority” (DFSA). Unigestion Asset Management (Düsseldorf) SA is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Bundesanstalt für Finanzdienstleistungsaufsicht” (BAFIN).