Are Higher Energy Prices a Game Changer For Growth?

Head of Macro and Dynamic Allocation, Cross Asset Solutions

Oil is once again in the spotlight, reaching levels not seen since 2014. After having witnessed the seemingly impossible event of negative prices when the pandemic took the world by surprise in 2020, we are now facing a 50% increase in Brent and WTI crude oil since January. This upside trend, which has extended to most of the commodities markets, places the Fed and the major central banks between a rock and a hard place: whereas the inflation shock intensifies in the short-term, the risk of recession is growing in the medium-term.

Smoke on the Water

What’s Next?

February 2022 is a new chapter for the history books

February was another epic month for the global economy and the financial markets, starting with hawkish messages from major central bankers and ending with the Russian invasion of Ukraine. Over the month, global equities declined by -2.6% while the US 10-year bond yield finished up slightly at 1.8%. Although the monthly changes may appear moderate given the geopolitical context, they hide a sharp increase in both dispersion across and within assets as well as huge intraday moves. In the equity markets, European stocks suffered the most, falling -5.9% in February versus -0.5% for Topix and -3% for the S&P 500. Energy and defensive sectors such as Healthcare and Utilities outperformed IT and Financials, while Quality and Momentum styles underperformed Value. Dispersion was also unusually high for individual stocks such as Facebook or Netflix, which declined 30% over the month. Finally, the US yield curve shifted dramatically, with a massive repricing of the Fed hiking cycle: a 26bps jump in 2-year bond yields vs 4bps for the 10-year. In that context, the VIX jumped from 24 to 31, its curve inverted, credit spreads widened and gold rallied. Commodities rose, with energy and base metals indices up 4.5% and 6.4% respectively, raising fears of stagflation.

While we don’t know when the geopolitical crisis will end and how it will transform the world order, we can acknowledge that the cost of war may be high for the global economy in the short-term.

The Cost of War 1: Higher risk premia for longer

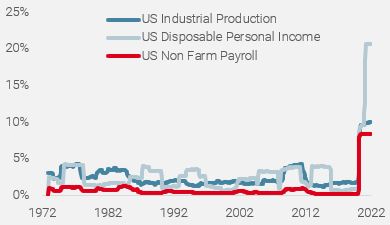

Asset returns depend on multidimensional risk factors that evolve over time, primarily fundamentals such as activity or inflation, monetary policy, market sentiment, regulation and geopolitics. Recent events in Ukraine dramatically exposed the risks of war. In a situation where anything is possible, uncertainty tends to increase, injecting volatility into the financial markets. Consequently, the risk premium embedded in any asset class rises via either the incorporation of a new type of risk (war), or a change in its potential impact and odds of occurrence. Stock and Watson1 soundly documented the relationship between realised volatility of macro-economic data and the one embedded in various assets. In a nutshell, the higher the speed of a car, the higher the risk of an accident. Today, regardless of the data we use, whether employment change, inflation rate or household disposable income (Figure 1), the amplitude of change has massively expanded over the last few years.

Figure 1: US Macro Volatility (realised volatility 3-year rolling)

Sources: Unigestion, Fed, BLS.

As a result, the number of sigma events or VAR shocks have increased significantly, implied volatility has jumped across the board, and correlation pairs tend to be less and less stable. Conversely, liquidity for major instruments such as US and German treasuries (Figure 2), the S&P 500 and most other “liquid” derivatives has significantly dried up, increasing the risk of huge overshoots and massive intraday moves. This in turn prompts longer-term investors to reduce their exposure and amplifies the liquidity reduction in a classic feedback loop.

Figure 2: German bond futures liquidity (Hui-Huebel liquidity ratio)

Source: Bloomberg, Unigestion. As of 05.03.2022

In that framework of higher and more durable volatility, the best dynamic risk management is to scale down the size of tactical bets to incorporate the higher risk premia.

The Cost of War 2: From “supply shock” to “demand destruction”

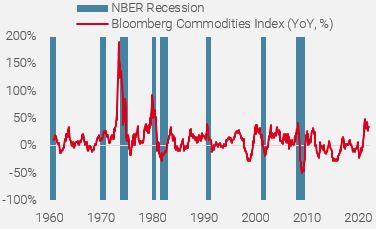

A continuation of the “out of control” trend observed in the energy markets would raise the odds of a global recession. As illustrated in Figure 3, most of the past US recessions dated by the NBER came after a jump of more than 50% in global commodities prices.

Figure 3: NBER and commodities prices

Source: Bloomberg, NBER, Unigestion. As of 28.02.2022

The underlying mechanism linking commodities prices and the global economy is very simple: when price increases are as extreme as they are today, higher cyclical commodities prices such as industrial metals or energy act as a tax for corporates and household, because they don’t have the time to adjust their processes or consumption habits to new higher prices. As a result, profitability and real disposable income decline quickly and sharply, triggering a demand reduction and then a risk of excess inventory shock. We see depressed consumer sentiment, high prices, and negative real wage growth threatening consumption in the first half of this year, as reflected by the decline in both consumption components of our US Growth Nowcaster and the Conference Board confidence data.

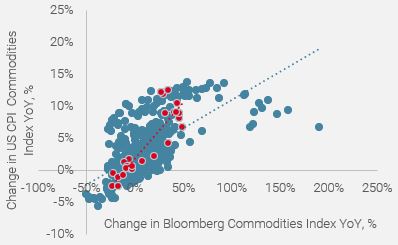

The risk of demand destruction is accentuated by the higher correlation between global commodities and its impact on US consumer inflation. Historically, the correlation between the Bloomberg Commodities index and the US CPI Commodities component, which represents 49% of the US CPI, is strong (Figure 4). Our historical analysis shows that a jump of 10% in the year-on-year change in the commodities index translates with an increase 0.8% in the US CPI Commodities component. Nevertheless, as shown in Figure 4, the impact on the US CPI from higher commodities has been larger in 2021/2022. Our data analysis shows that the pass through has been quicker and larger in 2021 and 2022 than in the past, both on the downside and upside.

Figure 4: US CPI Commodities component vs Bloomberg Commodities index

Source: Bloomberg, BLS, Unigestion. As of 28.02.2022

Focusing too much on the current level of inflation could be futile at best, since it tells a narrative of the past, and at worst, it can increase the risk of a policy mistake. In our view, markets should focus on the growth outlook and the rhythm of its deceleration rather than on inflation risk, which is already priced into the bond and commodities markets. Geopolitics can influence the timing of the peak and the path of deceleration by temporarily increasing inflations pressures through higher commodities prices. Nevertheless, even in the current context, demand destruction led by a jump in prices would weigh more on global growth and the policy mix than an incremental increase in headline inflation.

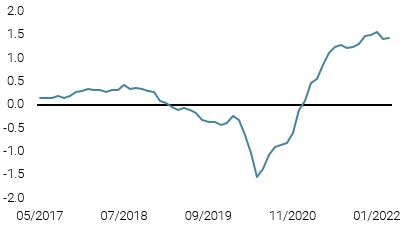

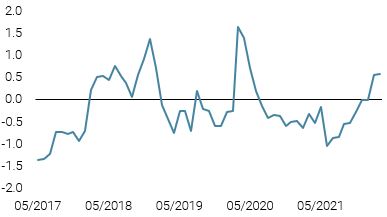

Unigestion Nowcasting

World Growth Nowcaster

World Inflation Nowcaster

Market Stress Nowcaster

Weekly Change

- Last week, our World Growth Nowcaster moved down slightly, driven by further slowing in the US and Eurozone.

- Our World Inflation Nowcaster ticked up slightly due to increasing inflation pressures among EM economies.

- Our Market Stress Nowcaster fell modestly, as liquidity conditions improved while spreads continued to widen.

Sources: Unigestion, Bloomberg, as of 04 March 2022

1,Stock, James; Mark Watson (2002). “Has the business cycle changed and why?“

Important Information

This document is provided to you on a confidential basis and must not be distributed, published, reproduced or disclosed, in whole or part, to any other person.

The information and data presented in this document may discuss general market activity or industry trends but is not intended to be relied upon as a forecast, research or investment advice. It is not a financial promotion and represents no offer, solicitation or recommendation of any kind, to invest in the strategies or in the investment vehicles it refers to. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment.

The investment views, economic and market opinions or analysis expressed in this document present Unigestion’s judgement as at the date of publication without regard to the date on which you may access the information. There is no guarantee that these views and opinions expressed will be correct nor do they purport to be a complete description of the securities, markets and developments referred to in it. All information provided here is subject to change without notice. To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks.

Data and graphical information herein are for information only and may have been derived from third party sources. Although we believe that the information obtained from public and third party sources to be reliable, we have not independently verified it and we therefore cannot guarantee its accuracy or completeness. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. Unless otherwise stated, source is Unigestion. Past performance is not a guide to future performance. All investments contain risks, including total loss for the investor.

Unigestion SA is authorised and regulated by the Swiss Financial Market Supervisory Authority (FINMA). Unigestion (UK) Ltd. is authorised and regulated by the UK Financial Conduct Authority (FCA) and is registered with the Securities and Exchange Commission (SEC). Unigestion Asset Management (France) S.A. is authorised and regulated by the French “Autorité des Marchés Financiers” (AMF). Unigestion Asset Management (Canada) Inc., with offices in Toronto and Montreal, is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario and Quebec. Its principal regulator is the Ontario Securities Commission (OSC). Unigestion Asset Management (Copenhagen) is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Danish Financial Supervisory Authority” (DFSA). Unigestion Asset Management (Düsseldorf) SA is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Bundesanstalt für Finanzdienstleistungsaufsicht” (BAFIN).