Big Things have Small Beginnings

- Small and Mid-market Private Equity – A Source of Hidden Gems.

- Small and mid-market companies represent a key part of the overall economy and are a hothouse for tomorrow’s leaders

- It is at the small end of the market, rather than among the biggest companies, that private equity deals with the highest return potential are to be found1

- Attractive valuations, low leverage and multiple ways to create value lead to compelling investment opportunities

- Given the breadth of the opportunity, and to avoid the common pitfalls, it is important to partner with local investment specialists who are best placed to source, analyse and invest in the most attractive deals

- A smart portfolio of direct investments should be diversified across regions and sectors and exposed to the most attractive long-term trends

Capturing the Growth Potential of the Small and Mid-market Private Equity Universe

Much of what we consume today, be it goods or services, is developed, produced and delivered by small and mid-market companies – those valued under USD 500 million. In fact, according to the Small Business Association, they account for almost 50% of output in the US. Furthermore, and contrary to the conventional wisdom that smaller companies are more vulnerable to downturns, two million jobs were actually added in the US small and mid-market segment during the last recession, while larger companies were reducing headcount2. In the EU, between 2002 and 2010, over 80% of net new jobs were created by small and mid-market companies3.

The small and mid-market is therefore a key contributor to the overall economy. Moreover, even the successful large-cap companies of today spent much of their existence as fast growing minnows. Consequently, most investors are keen to tap into the growth potential at the smaller end of the market.

Today’s successful large-cap companies spent most of their existence as fast growing minnows.

However, accessing these opportunities has historically been a challenge. Such companies are typically not listed on public stock exchanges and the information available on them is scarce. Therefore, investing with private equity specialists who focus on the small and mid-market can be an attractive way of gaining access to the high potential returns that the segment offers.

Accessing the small end of the market has historically been a challenge to investors.

The objective of a typical private equity investor who operates in the small and mid-market is to identify and invest in companies that have the highest potential to grow and become leading enterprises. This involves moving them up the ladder in terms of professionalisation, operational efficiency, breadth of their service/product offering, internationalisation and expansion into new markets. A few examples of companies that are household names today, but that have gone through significant size and operational transformations while under private equity ownership, include: Louis Poulsen (lighting products, Denmark); Oscar de la Renta and Moncler (luxury consumer goods, US and Italy respectively); Pandora (jewellery retail, global); Pret a Manger and Wagamama (fast casual restaurants, UK); and Cass (alcoholic beverages, South Korea). Having started as small companies in their respective markets, they have grown to become global brands and a part of people’s daily lives.

The Benefits of the Small and Mid-market

Breadth of Opportunity

The small and mid-market is vast, with a considerable range of investment opportunities. We estimate that there are around 500,000 investable companies globally in this segment, and this number gets larger every year.

In our view it is in the less well publicised small and mid-market that some of the best value is to be found.

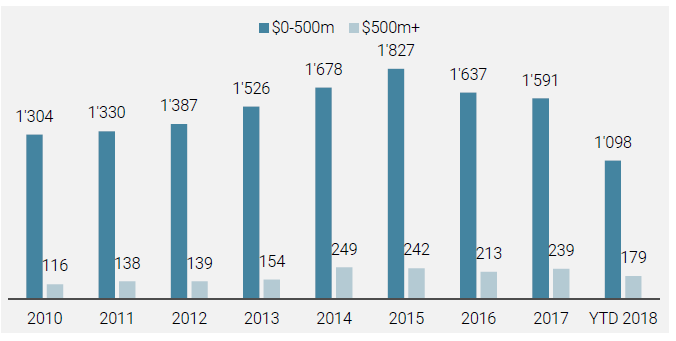

Indeed, the number of buyouts completed at less than USD 500 million in enterprise value is more than five times the number of deals above USD 500 million. When considering growth capital and turnaround deals in addition to buyout deals, this number increases to almost ten times. This has consistently been the case for the last ten years and it is unlikely to change in the future. Founders will continue to have succession challenges, companies will always have opportunities to expand into new markets/product lines, and conglomerates, by their nature, will continually provide spinout opportunities.

With such a broad and diverse universe, there are clearly a large number of companies with substantial growth potential, but which are currently not well known among investors – the difficulty, of course, is finding them.

There clearly exists a large number of companies with substantial growth potential – the challenge, of course, is finding them.

Figure 1: Number of Private Equity Deals by Transaction Size in USD

Less Dry Powder

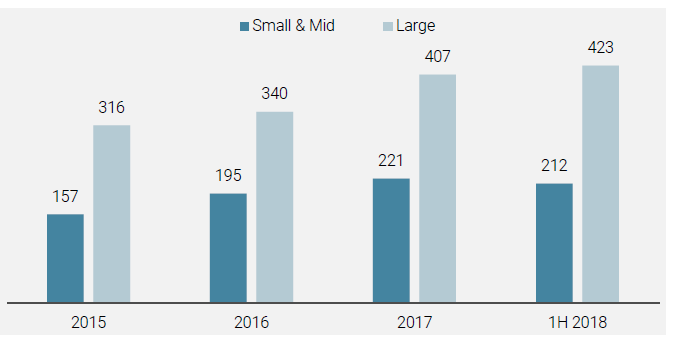

There are currently record amounts of committed but not yet invested capital (’dry powder’) in the overall private equity market, driven by record fundraising. However, conditions are not necessarily uniform across the market. Indeed, for small and mid-market funds4, dry powder has been growing at a slower pace than the rest of the market over the last three years (as of June 2018, 6% CAGR5 vs. 16% for large cap6).

With less dry powder, the demand-supply dynamics remain favourable at the lower end of the market; the vast number of small and mid-market opportunities should easily absorb the capital available.

Figure 2: Dry Powder, in USD Billion

Attractive Valuations

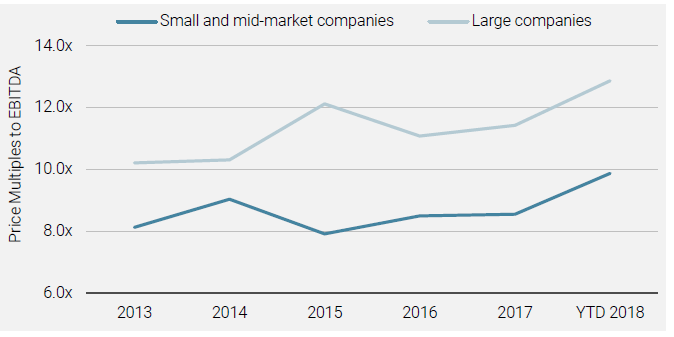

On a multiple of EBITDA7 basis, small and mid-market deals in North America and Europe can have valuations as much as 50% lower than those of large-cap deals. Furthermore, the gap between the valuations of large vs. small and mid-market transactions has widened over the last five years. Why does this price arbitrage exist?

Transaction prices in the small and mid-market are often more attractive.

With more dry powder burning holes in fund managers’ pockets, competition for deals at the large end of the market has become more intense. In addition, rather than through competitive auctions, deals are typically sourced through proprietary networks, where local knowledge and relationships are key. A company owner is often sensitive to the identity of the ultimate buyer, given that the business may have either been within the family for generations or is an important employer in the local community. As a result, the transaction price is often a secondary consideration.

There can of course be negative reasons for why small companies are cheaper than large companies – they may be less efficiently run, have a narrower product range or involve more risk than their larger counterparts operating in the same sector. However, therein lies the opportunity. A talented private equity manager with the appropriate skills would be able to help such companies solve these problems, leading to an increase in their value.

Figure 3: Small and Mid-market Companies Acquired at Lower Multiples

For example, in 2011, mydentist, the largest group of dental practices in the UK, was acquired by a large private equity firm for GBP 580 million, or 9.8x EBITDA. In the same year, Curaeos, a much smaller dental chain in the Netherlands, was acquired by a local private equity firm for EUR 134 million, or 6.7x EBITDA. Both firms have followed a buy-and-build strategy but this has led to quite different outcomes. Through acquisitions, the smaller firm multiplied its revenue ten-fold and was last year sold to a large pan-European private equity firm for EUR 560 million, or 15x EBITDA. Meanwhile, in seven years, the larger firm has only managed to double its revenue through acquisitions and has failed to increase EBITDA due to integration difficulties.

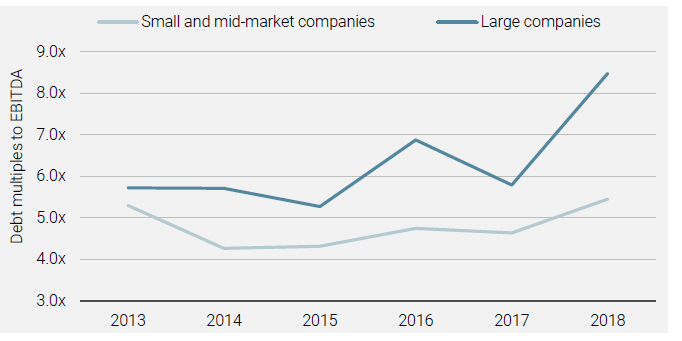

Small and mid-market companies have historically carried around 20% less leverage.

Lower Leverage

Small and mid-market companies have historically carried around 20% less leverage (on a multiple of EBITDA basis) than similar large-cap companies, as banks have generally been more reluctant to extend credit to smaller firms. The lower leverage multiples of smaller companies mean that, firstly, they have a sufficient buffer in case times are tough and, secondly, they are not constantly restricted by the need to service the debt in case they want to make internal investments or add-on acquisitions. In addition, from an investor’s point of view, lower leverage and simpler capital structures allow for the use of preferred equity instruments, thus providing more downside protection while preserving the upside potential of the investment.

Figure 4: Small and Mid-market Companies Use Less Leverage Than Larger Firms

Value Creation in Small and Mid-market Companies is Driven by Operational Improvement Rather than Leverage

Since private equity investors in small companies cannot rely on leverage to drive returns, investors are compelled to create value predominantly through ’true’ business growth and operational improvements. This is not necessarily straightforward, and requires a talented private equity manager at the helm.

Based on analysis of Unigestion’s historical investments, approximately 50% of value creation in small and mid-market companies was driven by EBITDA growth. A further 37% was driven by multiple arbitrage (selling at a higher multiple vs. the entry multiple), while only 13% came from the use of leverage. For large companies, almost 80% of value creation came from the use of leverage, while 10% came from EBITDA growth.

Investors in small and mid-market companies have several levers that they can pull. Indeed, the investor will already identify value creation opportunities during the ’getting to know the business’ and due diligence phases. They will therefore be able to assess which value creation strategies are viable and, if so, the steps necessary to implement them and mitigate any risks.

Investors in small and mid-market companies have several levers they can pull to create value.

Firstly, there is typically scope to professionalise a small company by upgrading its management team. This will help effect change in areas such as improving sales efficiency, finding new markets or launching new products, ultimately seeking to develop growth opportunities and improve overall efficiency for the company. In addition, strong private equity firms will have networks of professionals and operating partners they have worked with before, and who can be brought in to execute the agreed upon plans, such as cost rationalisation or process improvement.

Secondly, the ongoing consolidation process in a number of industries offers strong potential to add value by enabling companies to acquire growth and benefit from cost synergies. Small companies are also generally able to follow a buy-and-build strategy without encountering problems with competition authorities.

The cherry on the cake for an investor is that a well-run company will demand a premium from the next buyer. Thus, properly executed operational improvements should result in value creation through revenue growth, EBITDA growth and multiple arbitrage.

Outperformance of the Small and Mid-market

The proof is in the pudding, and the result of the above factors have historically led to better returns at the small end of the market relative to the large end. A research study conducted by Professor Oliver Gottschalg, from HEC Business School Paris, and Unigestion concluded that, historically, small and mid-market private equity funds have outperformed large-cap private equity funds8. Indeed, the median performance for portfolios of small and mid-market funds (covering vintages from 1998 to 2011) has been a TVPI9 of 1.78x. Meanwhile, the median performance for portfolios of large-cap funds has been a TVPI of 1.69x. Considering only top and second quartile funds, the outperformance is even clearer, with small and mid-market funds achieving a median TVPI of 2.24x, while large-cap funds achieved a median of TVPI of 2.04x.

How to Access and Exploit the Opportunity

Sourcing the Most Attractive Investment Opportunities

How can investors find the best small and mid-market companies amid this vast investment universe? Intuitively, private equity investors should cast their nets as far and wide as possible in order to maximise the number of investment opportunities seen. Practically, this requires both a large team and a deep network. The more opportunities an investor can source, the better the chance of finding hidden gems. It is no surprise that for a typical private equity investor, out of 100 deals sourced, only one to three will end up as completed investments.

How can investors find the best small and mid-market companies amid this vast investment universe?

Often small and mid-market companies are focused on very specific niche businesses or local markets. In order to source and execute the best deals globally, it is important to partner with specialist investment managers or entrepreneurs who understand and have a track record in exploiting value in niche sectors and local markets. In addition to gaining access to the best deals, the partners will aim to reduce overall deal execution risk and to bring important value to the company

post-investment.

The ability to source investment opportunities locally and analyse companies across the world has helped private equity firms find companies such as Jimmy Choo in the UK, Joe & the Juice in Denmark, Alibaba in China, Canada Goose in Canada, Bliss in the US and many others that are today household names globally.

In-depth Analysis to Identify the Best Opportunities

Once a potential investment opportunity has been identified, how can investors determine if it is worthy of investment? Each opportunity needs to be subjected to a rigorous selection approach using quantitative and qualitative filters to discern the health and viability of its business. Ideally, an initial screening of the opportunities will rapidly identify red flags, such as high leverage ratios, low growth sectors, low cash conversion or deteriorating margins. This will allow for quick rejects, freeing up time to be spent on the more attractive opportunities. A formal investment process should be in place to ensure that all the checks and balances are performed and that each investment is subject to the same scrutiny. It should not be underestimated how resource-intensive such a process is, especially if the intention is to build a diversified, global portfolio.

Each opportunity needs to be subjected to a rigorous selection approach using quantitative and qualitative filters.

Build a Smart Portfolio

We believe the above steps are the basis for identifying and investing in the most exciting companies on a standalone basis, but how does an investor ensure that a portfolio can withstand all environments? Firstly, companies of course need to be resilient in their own right. TowerBrook acquired luxury shoemaker, Jimmy Choo, for GBP 185 million in February 2007, on the eve of the global financial crisis. However, given the strength of the brand and the opportunity to enter underpenetrated markets, the company was able to continue its strong growth through internationalisation and expansion into adjacent product lines. In 2011, the company was sold to Labelux for GBP 500 million.

Secondly, a private equity investor needs to develop a macro and sector view. Which countries or regions offer higher growth potential? Which sectors are undervalued and are less correlated to overall GDP growth? While good investment decisions should be first made at the company level, it is critical to diversify across regions, sectors and underlying sources of risk in order to build a truly robust portfolio.

Conclusion

The world is full of exciting small and mid-market companies, most of which are hidden from view of the typical investor. By their nature, these companies will likely be only present in one country, may still be run inefficiently or have inexperienced and incomplete management teams. However, a select few of them, under the right ownership, will be destined for greatness. The trick is in finding them and herein lies the opportunity for investors who have the right resources, focus, persistence and expertise.

The world is full of exciting small and mid-market companies – the trick is in finding them.

Unigestion partners with local investment specialists and entrepreneurs to source and execute direct investment opportunities globally.

Long-term Growth Potential or Short-term Fad?

Successful private equity investors need to be close to the markets in order to differentiate long-term secular trends from short-term fads. For example, after the Fukushima nuclear disaster in 2011, the Japanese government ordered an immediate and permanent ban on the use of nuclear energy. Since Japan is devoid of fossil fuels, there was a dire need for locally generated power from renewable sources as an alternative to having to import the vast majority of its energy at a higher cost. This would therefore clearly lead to long-term opportunities for small companies involved in renewable energy. In 2012, a private equity firm in Asia invested in a small solar developer in the country and generated attractive returns for its investors.

By contrast, countries such as Spain have tried to meet renewable energy targets in the past, but there has been no overriding urgency as they could always fall back on traditional sources of energy. Renewable energy firms in such countries are thus highly susceptible to regulatory changes and, in our view, are unlikely to grow significantly over the long term.

This is the first thing private equity investors should be acutely aware of: they should target areas that promise long-term growth, as opposed to companies exposed to themes that are ’hot’ at the time of investment, but have no clear drivers in place to ensure that the growth is sustainable.

[1] Based on Preqin Performance Analyst database. Comparing performance of mid-cap to large-cap funds for

vintage years 2002-2012. Past performance is not a reliable indicator for future performance.

[2] Source: OECD.

[3] Source: European Commission, based on new jobs created less jobs lost.

[4] Source : Preqin (funds up to USD 1.5 billion in size).

[5] CAGR: Compound annual growth rate.

[6] Source: Preqin, as of June 2018.

[7] EBITDA: Earnings before interest, taxes, depreciation and amortisation.

[8] Source: “Size matters – small is beautiful 2.0”, study by Unigestion and Professor Oliver Gottschalg, HEC Business School Paris.

[9] TVPI: Total value to paid-in-capital.

Important Information

This document is provided to you on a confidential basis and must not be distributed, published, reproduced or disclosed, in whole or part, to any other person.

The information and data presented in this document may discuss general market activity or industry trends but is not intended to be relied upon as a forecast, research or investment advice. It is not a financial promotion and represents no offer, solicitation or recommendation of any kind, to invest in the strategies or in the investment vehicles it refers to. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment.

The investment views, economic and market opinions or analysis expressed in this document present Unigestion’s judgement as at the date of publication without regard to the date on which you may access the information. There is no guarantee that these views and opinions expressed will be correct nor do they purport to be a complete description of the securities, markets and developments referred to in it. All information provided here is subject to change without notice. To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks.

Data and graphical information herein are for information only and may have been derived from third party sources. Although we believe that the information obtained from public and third party sources to be reliable, we have not independently verified it and we therefore cannot guarantee its accuracy or completeness. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. Unless otherwise stated, source is Unigestion.

Past performance is not a guide to future performance. All investments contain risks, including total loss for the investor.

Unigestion SA is regulated by the Swiss Financial Market Supervisory Authority (FINMA). Unigestion (UK) Ltd is authorised and regulated by the Financial Conduct Authority (FCA) and SEC registered. Unigestion Asset Management (France) SA is regulated by the “Autorité des Marchés Financiers” (AMF). Unigestion (Luxembourg) SA is an Alternative Investment Fund Manager authorised by the Commission de Surveillance du Secteur Financier (CSSF) under the Luxembourg law of 12 July 2013 on AIFM. Unigestion Asset Management (Canada) Inc., with offices in Toronto and Montreal, is regulated in Canada by the securities regulatory authorities in Ontario, Quebec; Alberta, Manitoba, Saskatchewan, Nova Scotia, New Brunswick and British Columbia. Its principal regulator is the Ontario Securities Commission. Unigestion Asia Pte Ltd is regulated in Singapore by the MAS, as Capital Market Services (CMS) license holder and Exempt Financial Adviser under the Securities and Futures Act and Financial Advisers Act.