Carbon has been one of the hottest topics of discussion this year. Climate action is a huge theme that affects both individuals and companies, and governments around the world have been actively addressing this essential topic, as witnessed at the recent COP26 Summit in Glasgow. Carbon also plays a critical role in the investment world. At Unigestion, we have been active proponents of responsible investing since 2004 and it is ingrained into everything we do. We believe it will become a growing focus for many other market players as well in the coming years.

Carbon credits or offsets are examples of mechanisms used to drive the necessary behavioural changes needed to limit climate change. A higher carbon price is required to incentivise change and is the foundation behind decarbonisation efforts to reduce carbon dioxide (CO2) output into the atmosphere. In this week’s Macro Views, we focus on how macro, government and regulatory policies will shape the price of carbon going forward.

Green Light

Where Do We Go From Here?

Market mechanics

The Paris Agreement, which came into force in 2016, is the first legally binding global climate change agreement. It aims to limit global warming to below 2°C. A global stocktake every five years was also agreed upon to assess progress and enhance policies. In late 2020, the world’s largest pension funds and insurers (representing USD 2.4 trillion in assets) committed to transitioning their portfolios to net-zero emissions (removing all manmade greenhouse gas (GHG) emissions) by 2050. G20 countries account for approximately 80% of the world’s GHG, making global cooperation essential in achieving net-zero emissions.

Market-based instruments are essential in determining a price for carbon emissions. The two mechanisms that exist today, Emission Trading Systems (ETS) and carbon taxes, have a common goal, but it is important to note the differentiation between them. ETS, also known as cap and trade systems, establish a market price for GHG emissions by effectively predetermining an allocated carbon budget / allowance. In many countries, these have been standardised into derivatives instruments. The most advanced market is currently in Europe with physically deliverable futures contracts of emission allowances. Each emission allowance being an entitlement to emit one tonne of CO2 equivalent gas. A carbon tax, on the other hand, is characterised by a predefined price set by governments that emitters must pay for each tonne of GHG emissions emitted.

It is also worth noting the difference between carbon credits and carbon offsets. The former represents the right to “pollute” and works like an allowance that parties will pay for, the latter takes the form of environmental projects (e.g., planting trees, clean energy projects, and mechanical carbon capture) that will “offset” a company’s or an individual’s carbon footprint. Both methods effectively have the same purpose – creating a financial incentive for polluters to reduce emissions.

Many countries have now adopted their own similar schemes. In the US, we have the California Carbon Allowance and the Regional Greenhouse Gas Initiative (RGGI) allowances, the UK and China launched their own ETS this year and, after a pilot study, Mexico will launch theirs next year. Many other countries have also initiated similar programmes. However, Europe’s remains the most established one.

One of the outcomes of the COP26 meeting was the agreement that the world needs a “global carbon market”. Questions around the impact of cross-border trading on climate change are complex and here, once again, the EU is a pioneer having opened the topic of a “carbon border adjustment tax”. This would take the form of a duty on imports based on the amount of carbon emissions resulting from the production of these goods and services. But critics argue that some countries will use such a tax as a form of “green protectionism”. Additionally, it is a complex process to accurately access / quantify emissions, especially on a cross-border basis.

The derivatives market

Carbon derivatives play a crucial role in achieving the net-zero emissions goal. They effectively provide a simple solution for companies to manage and comply with their emissions obligations in a transparent and cost-effective manner. Exchanges allow for an easy and regulated way for buyers and sellers to meet. Futures enable companies to hedge forward and manage transition risk / comply with their obligations. The supply and demand balance of carbon emissions therefore determines the cost of polluting.

However, derivatives also have their limitations, as many markets outside of the European one are still in their infancy and therefore face liquidity issues and complex market access (with a majority of the liquidity being Over-the-Counter (OTC)), although these subtleties should improve over time.

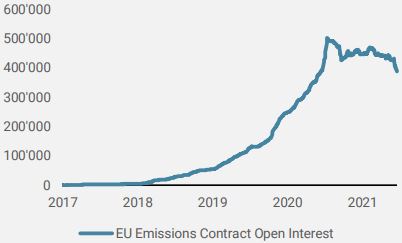

Figure 1: Growth of the Carbon Market

Source: Unigestion, Bloomberg as of the 17.11.2021.

Supply and demand drivers

On the demand side, the trend of market participants is currently exponential as emissions is no longer a subject that can be ignored. Some industries have a mandatory obligation to comply with emissions (e.g. power companies in the energy sector). Where such compliance is not mandatory (e.g., certain corporates, hedge funds, banks, commodity firms), these organisations have also been proactive in recent years to compensate for their carbon footprint by engaging in carbon trading schemes / offset projects. Carbon trading is also slowly but surely starting to form an integral part of investment strategies and, importantly, financial institutions have also become key liquidity providers for the industry.

The supply side is very much controlled by government and regulatory authorities as they decide how many allowances circulate in the market. Member states auction their allowances in accordance with the ETS Directive. In the EU, some manufacturing industries received up to 80% of their emissions allowances for free in 2013, limiting cost impacts relative to non-EU competitors. The aim was to give these industries time to adapt and switch to “greener” alternatives. These “free” emissions allowances will decrease gradually every year at an estimated annual rate of 2.2% between 2021 and 2030. Industries that do not use all of their carbon credits are free to sell them back to the market, giving them an additional incentive to reduce emissions in a timely manner.

Allocating to carbon in a macro risk-based framework

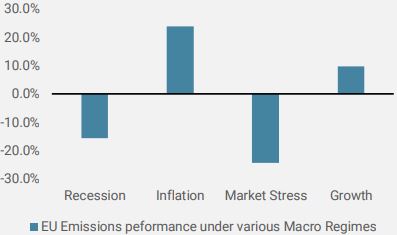

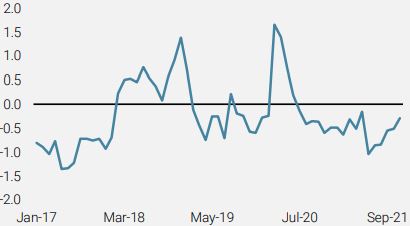

Macroeconomic conditions are one of the key drivers of the carbon market. We examined the average performance of carbon across four macro regimes: recession, inflation surprise, market stress and steady growth. As can be seen in Figure 2, carbon performs best during inflation and growth regimes. Indeed, strong economic growth dynamics imply a rise in demand for goods and services and the resulting manufacturing activity leads to higher emissions and thus a higher need for carbon offsets. The strong economic recovery post the Covid crisis is a significant factor behind the current rally in the price of carbon.

Figure 2: Performance of EU Emissions Futures under Different Macro Regimes

Source: Unigestion, Bloomberg as of the 17.11.2021.

The risk of inflation surprise is the most supportive regime for carbon and the strong inflationary pressures in commodity and energy prices over the last year have led to an increase in the use of coal, pushing the green energy transition further away. The notorious by-product of burning coal is CO2, making it one of the most polluting sources of energy. Increased coal burning therefore automatically increases the demand for carbon offsets. A potentially cold winter and the resulting demand for heating could act as a further catalyst for carbon. Our proprietary Inflation Nowcasters and Newscasters are both pointing towards an elevated inflation surprise risk and show no signs of abating.

A focus on greener energy sources means the energy sector has suffered from significant levels of underinvestment over the last decade and the supply constrains we are currently facing are unlikely to get resolved quickly. Price pressures in carbon are also inflationary in themselves. Until the various impacted industries find “greener” production alternatives, that extra cost burden of higher carbon prices could also be passed onto the consumer.

At Unigestion we believe that ETS present an efficient way to integrate ESG criteria into commodity investing. We have incorporated EU carbon allowances into some of our strategic allocations as part of our allocation to cyclical commodities. Please refer to our recent Perspectives paper for further details on this topic: Responsible Commodities Investing: Assessing the Options. It is also feasible that at some point in the future, the benchmark commodity indices will start to integrate carbon into their universes.

Concluding remarks

Although the carbon market is far from new, the focus and emphasis on it has grown exponentially over the last couple of years and it would not be surprising to see a trading boom in emissions credits over the coming years as more and more players enter the space. As the global carbon market continues to grow outside Europe, so too will liquidity. This will see users who currently utilise European emissions contracts switch to more local and relevant alternatives.

Although the carbon market is becoming more established, firms are left with a complex problem to solve in accessing and quantifying their carbon impact.

The dynamics of achieving the goals of the Paris Agreement also remain complex and many details still need to be addressed. Unlike in other parts of the financial markets, governments are in the driving seat, controlling the majority of the supply mechanism and regulatory aspects of these derivatives. However, the message from authorities is clear – a higher carbon price is needed to incentivise the switch towards net-zero.

We can therefore expect carbon prices to continue moving north over the next decade. With macro momentum having slowed and inflation surprise risk still very high, we remain overweight real assets via inflation breakevens and cyclical commodities. All in all, this environment should continue to remain supportive for carbon.

Unigestion Nowcasting

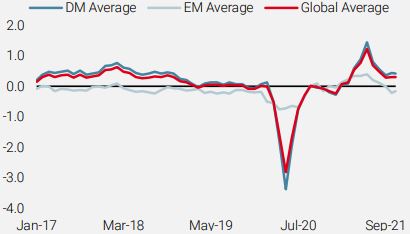

World Growth Nowcaster

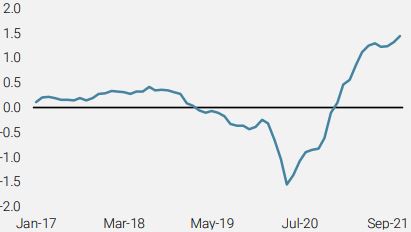

World Inflation Nowcaster

Market Stress Nowcaster

Weekly Change

- Last week, our World Growth Nowcaster moved slightly higher with improving data from the US and, to a lesser extent, China.

- Our World Inflation Nowcaster also rose modestly, as inflation pressures continue to persist or build further across the developed world.

- Our Market Stress Nowcaster continued its steady climb due to higher market volatilities.

Sources: Unigestion, Bloomberg, as of 19 November 2021.

Important Information

This document is provided to you on a confidential basis and must not be distributed, published, reproduced or disclosed, in whole or part, to any other person.

The information and data presented in this document may discuss general market activity or industry trends but is not intended to be relied upon as a forecast, research or investment advice. It is not a financial promotion and represents no offer, solicitation or recommendation of any kind, to invest in the strategies or in the investment vehicles it refers to. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment.

The investment views, economic and market opinions or analysis expressed in this document present Unigestion’s judgement as at the date of publication without regard to the date on which you may access the information. There is no guarantee that these views and opinions expressed will be correct nor do they purport to be a complete description of the securities, markets and developments referred to in it. All information provided here is subject to change without notice. To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks.

Data and graphical information herein are for information only and may have been derived from third party sources. Although we believe that the information obtained from public and third party sources to be reliable, we have not independently verified it and we therefore cannot guarantee its accuracy or completeness. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. Unless otherwise stated, source is Unigestion. Past performance is not a guide to future performance. All investments contain risks, including total loss for the investor.

Unigestion SA is authorised and regulated by the Swiss Financial Market Supervisory Authority (FINMA). Unigestion (UK) Ltd. is authorised and regulated by the UK Financial Conduct Authority (FCA) and is registered with the Securities and Exchange Commission (SEC). Unigestion Asset Management (France) S.A. is authorised and regulated by the French “Autorité des Marchés Financiers” (AMF). Unigestion Asset Management (Canada) Inc., with offices in Toronto and Montreal, is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario and Quebec. Its principal regulator is the Ontario Securities Commission (OSC). Unigestion Asset Management (Copenhagen) is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Danish Financial Supervisory Authority” (DFSA). Unigestion Asset Management (Düsseldorf) SA is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Bundesanstalt für Finanzdienstleistungsaufsicht” (BAFIN).