Central banks have returned to centre stage over the past few weeks as inflation expectations have continued to rise sharply and investors have started pricing in swifter adjustments to monetary policies. Central bank rhetoric of a “transitory inflationary environment” and their patient stance regarding future monetary action is being challenged by market participants, given the observable data. Why are policymakers sticking to their surprisingly dovish convictions given the macroeconomic context, and what can we expect over the medium term from major central banks?

Surprise, Surprise

What Happened?

Macro trends remain unchanged

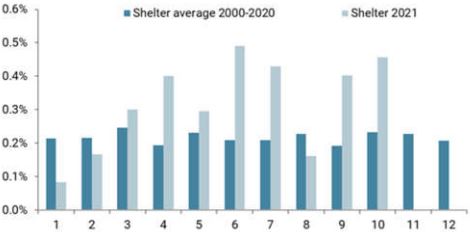

One thing that has not changed recently is the dynamics of macro fundamentals: inflation keeps on pushing higher and growth continues to stabilise above trend levels in developed economies. In the US, recent CPI numbers released for October came out stronger than expected (yet again): headline inflation jumped 6.2% year-over-year, the highest rate since December 1990, while core CPI surged 4.6%, more than twice the Fed’s long-term target of 2%. The latter is particularly alarming as the forces at play in this core measure are less volatile, stickier, and will consequently take longer to resorb than the headline measure, driven by cyclical elements such as energy prices. Shelter, the biggest component of core inflation measures – and the largest expenditure for most average citizens – once again posted an above average rise in October, highlighting that the trend remains strong and durable.

Figure 1: Shelter Inflation Is Alive and Well

Source: Bloomberg, Unigestion, as of 11 November 2021

Our proprietary Inflation Nowcaster, which measures the risk of inflation surprise over the medium term, correctly spotted an increasing likelihood for rising prices to become both a surprise and an issue early in 2021. The fact that the indicator has not yet come down from extreme levels and continues to push higher makes us believe that investors (and central bankers) could be surprised by the length of the current inflationary environment.

Central banks are surprisingly dovish

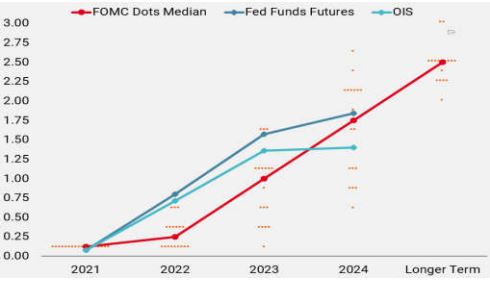

The outcomes of the most recent monetary policy meetings held by the Fed, the BOE and other central banks were a surprise to investors. Indeed, investors had started exhibiting high expectations of increasingly hawkish forward guidance. However, the Fed, despite delivering the much anticipated tapering of asset purchases, maintained its soft stance on inflation while the BOE did not hike interest rates even though it was supposed to be a done deal. Markets had already priced in future rate hikes and yield curves had adjusted accordingly, creating a window of opportunity to take a step further toward a less accommodative stance without shaking investor sentiment – a missed opportunity.

Yet investors remain defiant and in the case of the US, are still pricing the first rate hike to happen as soon as tapering is over, i.e. mid-2022.

Figure 2: Market Pricing for Rate Hikes Remains Elevated

Source: Bloomberg, Unigestion, as of 11 November 2021

If one considers that credibility is the most important asset for central banks, they have definitely incurred losses on this front.

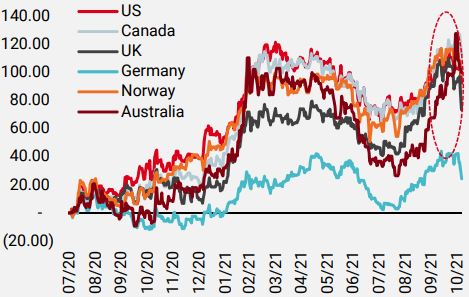

Figure 3: Yield Curve Reactions to Central Banks

Source: Bloomberg, Unigestion, as of 11 November 2021

The market is becoming ever more sceptical about the transitory nature of the current inflation shock, and the longer policymakers take to acknowledge the genie is already out of the bottle, the longer price pressures will stay with us without efficient counter measures. Even though the initial market reaction has been positive, as pushing forward the moment to tighten monetary conditions is good news for the investment community, their perceived complacency on inflation is negative over a slightly longer time horizon.

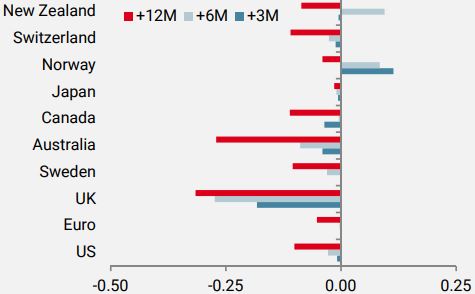

Figure 4: Changes in Hike Expectations Week-on-week

Source: Bloomberg, Unigestion, as of 11 November 2021

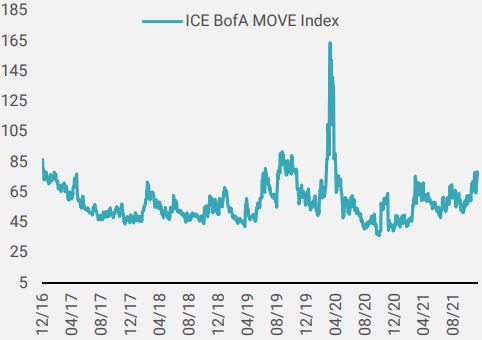

Medium-term consequences could be difficult to manage

The increasing divergence between economic reality and central bank patience could have negative consequences for both Main Street and Wall Street. Investor sensitivity to inflation numbers has sharply risen over the past couple of months and so has market volatility, especially in the bonds space. The MOVE index, which measures the implied volatility of 1-month options on a variety of tenors, is at its highest level since March 2020, buoyed by the rising risk of a monetary policy mistake. Fundamentally, the current levels of growth and inflation combined should (historically, in a pre-QE world) grant a sharp rise in interest rates, which in turn could be detrimental to risky assets. For now, only the inflation element has been priced: breakeven curves are now at multiyear highs while real rates remain at multi-year lows, deep in negative territories.

Once rates stop being maintained at artificially low levels by central bank asset purchase schemes, a recovery in real rates would be a good omen for risky assets, suggesting an improvement in growth and/or a decrease in inflation. On the contrary, risk assets would be negatively affected by a surge in yields, driven only by the inflation premium.

Figure 5: US Bonds Volatility: MOVE Index

Source: Bloomberg, Unigestion, as of 11 November 2021

Indeed, a purely systematic assessment of the macro forces at play should prompt a defensive stance on government bonds as the probability of seeing yields normalise is elevated due to the inflationary pressures. This would likely be accompanied by a cautious yet positive tilt to growth-related assets thanks to the benign growth environment.

We can interpret the surprisingly dovish central bank stance as testament to the seemingly imponderable equation they need to resolve: contending with inflation without derailing the post-pandemic recovery. This is the reason they have all been putting forward to justify their wait-and-see approach. They are taking the risk of spiralling inflation to make sure growth has become self-sustaining and achieve full employment, hoping that the supply disruptions driving surging prices will naturally reach an equilibrium point soon before fading away.

Positive as long as it lasts

Right or wrong, the surprisingly soft stance of central banks has given legs to the rally. Considering that monetary accommodation remains the key factor driving asset returns, above even the sacred fundamental factors, we believe it is still time to take advantage of the situation and remain exposed to both risk and real assets. History has demonstrated that trying to anticipate the actual change in financial conditions from an accommodative to a tightening situation usually yields disappointing results. We continue to scrutinize the specific factors that could indicate a rising risk of central banks adjusting faster than anticipated, which will be the time to turn more defensive.

Unigestion Nowcasting

World Growth Nowcaster

World Inflation Nowcaster

Market Stress Nowcaster

Weekly Change

- Last week, our World Growth Nowcaster ticked down slightly due to a lower European growth impulse.

- Our World Inflation Nowcaster moved slightly higher driven largely by higher readings out of the US and China.

- Our Market Stress Nowcaster moved modestly higher as volatilities rose and spreads widened.

Sources: Unigestion, Bloomberg, as of 12 November 2021.

Important Information

This document is provided to you on a confidential basis and must not be distributed, published, reproduced or disclosed, in whole or part, to any other person.

The information and data presented in this document may discuss general market activity or industry trends but is not intended to be relied upon as a forecast, research or investment advice. It is not a financial promotion and represents no offer, solicitation or recommendation of any kind, to invest in the strategies or in the investment vehicles it refers to. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment.

The investment views, economic and market opinions or analysis expressed in this document present Unigestion’s judgement as at the date of publication without regard to the date on which you may access the information. There is no guarantee that these views and opinions expressed will be correct nor do they purport to be a complete description of the securities, markets and developments referred to in it. All information provided here is subject to change without notice. To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks.

Data and graphical information herein are for information only and may have been derived from third party sources. Although we believe that the information obtained from public and third party sources to be reliable, we have not independently verified it and we therefore cannot guarantee its accuracy or completeness. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. Unless otherwise stated, source is Unigestion. Past performance is not a guide to future performance. All investments contain risks, including total loss for the investor.

Unigestion SA is authorised and regulated by the Swiss Financial Market Supervisory Authority (FINMA). Unigestion (UK) Ltd. is authorised and regulated by the UK Financial Conduct Authority (FCA) and is registered with the Securities and Exchange Commission (SEC). Unigestion Asset Management (France) S.A. is authorised and regulated by the French “Autorité des Marchés Financiers” (AMF). Unigestion Asset Management (Canada) Inc., with offices in Toronto and Montreal, is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario and Quebec. Its principal regulator is the Ontario Securities Commission (OSC). Unigestion Asset Management (Copenhagen) is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Danish Financial Supervisory Authority” (DFSA). Unigestion Asset Management (Düsseldorf) SA is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Bundesanstalt für Finanzdienstleistungsaufsicht” (BAFIN).