Chinese Economy Nearing Inflection Point

The Chinese economy is a cautionary tale for policymakers: early and aggressive restrictions kept the virus contained and allowed the economy to recover strongly and ahead of most others. Outbreaks were contained from March 2020 until the beginning of this year, when the omicron variant sent confirmed cases soaring. Relatively low vaccination rates with a less potent vaccine placed the country’s zero-Covid policy as the key line of defence, causing the economy to stall again and Chinese financial markets to suffer. With the outbreak receding, restrictions starting to be lifted, and policy very supportive, Chinese equities are in deep discount and offer investors an attractive entry point, even if not all risks have faded.

Walking on the Chinese Wall

What’s Next

Chinese growth back to lows

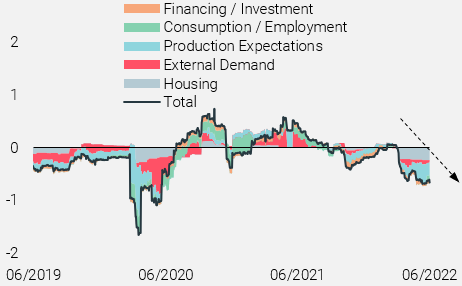

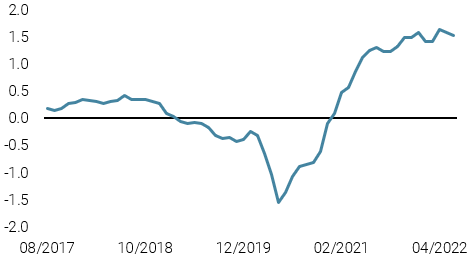

The Chinese economy was a bright star during the second half of 2020: while most economies, especially the US and Eurozone, were hobbled by continued Covid restrictions, China had largely re-opened and was booming. It also strongly benefited from cash-rich households in the developed world that could not spend on services and instead bought more goods, boosting Chinese exports. However, as external demand started to fade at the end of last year and policymakers re-oriented their focus back to containing credit and the housing market, growth faded to levels around its long-term potential. Figure 1, which shows our aggregate Chinese Growth Nowcaster as well as its underlying components, reveals how economic conditions have further deteriorated during the year so far. The current slowdown is primarily driven by a slower global growth impulse as well as a housing sector that remains under pressure and dour production expectations.

Figure 1: Chinese Growth Nowcaster and Components

Source: Bloomberg, Unigestion, as of 08 June 2022

Zero-Covid is a costly but largely necessary policy

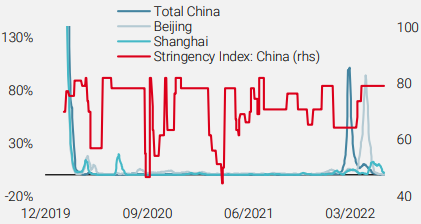

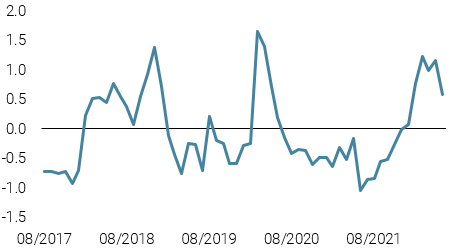

The stalling economy is to be expected, given China’s zero-Covid policy and the explosion of omicron cases it experienced earlier this year. As Figure 2 shows, new cases grew at a rate not seen since the start of the pandemic (when the number of cases were small, amplifying the percent change). Vaccination rates among the elderly, specifically those over 80 years, was low at the onset of the outbreak: just 51% of over 80-year-olds had received two doses by March 2022, and only 20% had received an additional booster. Moreover, many received the Sinovac or Sinopharm vaccines, which data suggests are less effective than the BioNTech or Moderna vaccines, especially in preventing death for the elderly. Given this context, it is not surprising that policymakers re-introduced lockdowns and other stringency measures in response (see Figure 2).

Figure 2: Week-over-Week Percent Change in Confirmed Covid Cases and Oxford Stringency Index

Source: Bloomberg, Unigestion, as of 08 June 2022

The situation, importantly, is improving significantly. As Figure 2 also shows, the rate of new cases has dropped off dramatically, and some lockdowns in turn have been lifted. Booster shots among older residents have also expanded significantly, bolstering the case of easing restrictions. Continued improvement will be necessary for the economy to open up further, and growth will remain constrained in the short-term, but China looks to be nearing a Covid inflection point, which has proven to be a critical period for financial markets.

Policy mix is about as favourable as it was in 2020

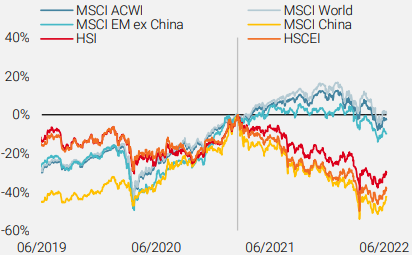

Chinese policymakers were among the largest contributors to the global stimulus experienced in 2020: lower reserve ratios, rate cuts, lending facilities, and over 5% of GDP in fiscal spending was key in supporting the global economy. As 2021 progressed, policymakers shifted their focus on their next Five-Year Plan: place social development and resilience on par with economic development. Regulatory, fiscal, and monetary policy shifted to a much less supportive stance, and investors took notice. Figure 3 charts the performance of equity indices from the February 2021 peak of the MSCI China index. Despite a favourable environment for global stocks, Chinese equities clearly decoupled from their peers. From the peak to the end of 2021, the MSCI China index underperformed the MSCI World index by over 50% and the MSCI EM ex China index by 37%. Only a fraction of this underperformance has reversed during the recent rally in Chinese stocks.

Figure 3: Performance since MSCI China Peak in February 2021

Source: Bloomberg, Unigestion, as of 08 June 2022

The scale of the economic slowdown and market turmoil has naturally led policymakers to pivot to stimulative policy, in stark contrast to many other economies. Nearly 3% of GDP in fiscal spending has been announced, interest rates have been reduced, and housing purchase restrictions have eased. Figure 4 shows the Required Reserve Ratio (RRR) for major Chinese banks, which was cut by 25bps in April and is now at its lowest level since 2007.

Figure 4: Required Reserved Ratio for Major Banks

Source: Bloomberg, Unigestion, as of 08 June 2022

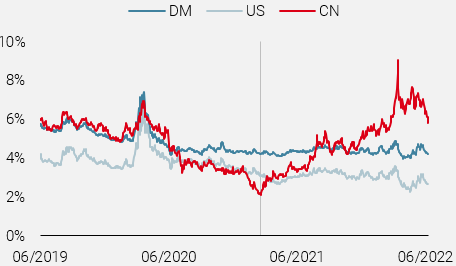

Indeed, from a cross-asset perspective, the spread between earnings and domestic sovereign bond yields offered by Chinese equities is at 6%, a much more attractive level than that offered by either US or developed market (DM) equities (see Figure 5).

Figure 5: Earnings Yields vs Domestic Bond Yields

Source: Bloomberg, Unigestion, as of 08 June 2022

The positive aspects for Chinese equities are balanced by some significant negative pressures. First, the prospective turnaround in economic conditions is dependent on avoiding another significant outbreak that would require strict adherence to the zero-Covid policy and necessitate lockdowns. Second, regulatory policy – especially for large firms and those in the tech industry – remains aggressive and challenging. While there have been some positive developments (more institutionalized framework instead of policy by edict, coordination with US bodies, etc.), there is a strong case for incorporating a significant regulatory risk premium in Chinese equities. Thus, while the equity risk premium for Chinese stocks should remain well above other developed world peers, current pricing suggests investors have yet to adjust their expectations for the improving Chinese domestic context.

Unigestion Nowcasting

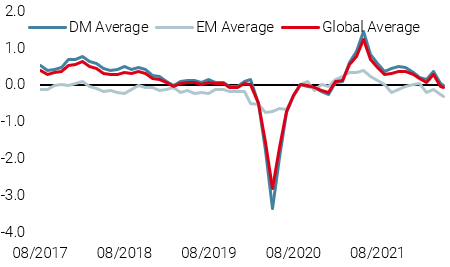

World Growth Nowcaster

World Inflation Nowcaster

Market Stress Nowcaster

Weekly Change

- Last week, our World Growth Nowcaster declined further as US employment and consumption data slowed.

- Our World Inflation Nowcaster ticked down slightly due largely to lower expected inflation in the UK.

- Our Market Stress Nowcaster moved slightly lower, primarily driven by an easing in liquidity conditions.

Sources: Unigestion, Bloomberg, as of 13 June 2022.

Important Information

This document is provided to you on a confidential basis and must not be distributed, published, reproduced or disclosed, in whole or part, to any other person.

The information and data presented in this document may discuss general market activity or industry trends but is not intended to be relied upon as a forecast, research or investment advice. It is not a financial promotion and represents no offer, solicitation or recommendation of any kind, to invest in the strategies or in the investment vehicles it refers to. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment.

The investment views, economic and market opinions or analysis expressed in this document present Unigestion’s judgement as at the date of publication without regard to the date on which you may access the information. There is no guarantee that these views and opinions expressed will be correct nor do they purport to be a complete description of the securities, markets and developments referred to in it. All information provided here is subject to change without notice. To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks.

Data and graphical information herein are for information only and may have been derived from third party sources. Although we believe that the information obtained from public and third party sources to be reliable, we have not independently verified it and we therefore cannot guarantee its accuracy or completeness. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. Unless otherwise stated, source is Unigestion. Past performance is not a guide to future performance. All investments contain risks, including total loss for the investor.

Unigestion SA is authorised and regulated by the Swiss Financial Market Supervisory Authority (FINMA). Unigestion (UK) Ltd. is authorised and regulated by the UK Financial Conduct Authority (FCA) and is registered with the Securities and Exchange Commission (SEC). Unigestion Asset Management (France) S.A. is authorised and regulated by the French “Autorité des Marchés Financiers” (AMF). Unigestion Asset Management (Canada) Inc., with offices in Toronto and Montreal, is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario and Quebec. Its principal regulator is the Ontario Securities Commission (OSC). Unigestion Asset Management (Copenhagen) is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Danish Financial Supervisory Authority” (DFSA). Unigestion Asset Management (Düsseldorf) SA is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Bundesanstalt für Finanzdienstleistungsaufsicht” (BAFIN).