- Private equity investment activity rebounded in Q3 but remains materially down vs. the prior year, driven by a slump in large cap deals. However, small deal activity remains resilient.

- As demonstrated by our own investment activity, we believe that the small and mid-market is currently enjoying particularly attractive dealflow.

- In the last six months, Unigestion contributed EUR 454m to investments.

Overview

Private equity investment activity showed a small rebound in Q3 as investors continued to operate within the constraints posed by the COVID pandemic. However, it was still materially down versus the same quarter last year1, particularly as many large cap private equity managers struggled to execute deals in the current environment. Meanwhile, as in Q2, the small end of the market showed most activity. At the same time, private equity managers are clearly waiting for better conditions to exit portfolio companies given that exit activity this quarter was at its lowest level in years.

Small deal activity remains resilient

The global aggregate value of private equity deals closed during Q3 2020 was EUR 128bn, a 24% increase on Q2 but still 43% down on the same quarter last year . North America and Europe showed similar increases (15% and 20%, respectively) but, for both regions, this was around 50% down on Q3 2019. Meanwhile, APAC showed a very healthy 54% increase in activity versus Q2, representing an 11% increase on the same quarter a year ago.

Investment activity in small and mid-market companies (defined as deals less than EUR 500m in enterprise value) continues to show more resilience than large cap deals (deals greater than EUR 500m). Although the aggregate value of large cap deals completed in Q3 was 43% up on Q2, it was still 58% down on Q3 2019. Meanwhile, small and mid-cap deal activity was only 17% down on Q3 2019.

Figure 1: Small vs. large deal activity

Given the amount of dry powder available for large cap deals, it is almost a certainty that activity at the large end of the market will eventually catch up. Indeed, although fundraising overall is trending lower versus last year, the average fund size closed is noticeably up. For example, in Europe, the average size of funds closed in Q3 was a record USD 1.7bn2 . However, with more dry powder chasing fewer deals, it is likely that prices for large cap deals will remain high for the foreseeable future.

Meanwhile, at the small end of the market, we think that the current dynamics remain favourable for investors given that less capital is being raised and more deals are being done. Indeed, given the amount of dealflow, small and mid-market managers are able to keep the bar high and target companies which have performed well in the current environment. In fact, we are benefiting from this dynamic in our direct fund, Unigestion Direct II. Since the pandemic began, we have been able to close five deals. Three of these deals were closed in Q3 – Infobip, Evaluate and Avania – which are discussed later in this document. The common thread across these deals is that they are resilient small and mid-market companies playing long-term investment themes which have only been accelerated by the current crisis.

The common thread across these deals is that they are resilient small and mid-market companies playing long-term investment themes which have only been accelerated by the current crisis.

How can we close deals in this environment given the various constraints in place? In several cases (e.g. Avania and Evaluate), we already know the companies well as they are existing portfolio companies of our investment partners so we have been able to observe their development closely. In addition, our investment partners are based in the same countries as the companies, so they are able to do on-site due diligence where relevant. Finally, we are still able to do our usual in-depth due diligence virtually through video conferences, expert interviews and thorough desktop modelling and analysis.

Global exit activity continued to post declines. The global aggregate value of exits in Q3 2020 was EUR 48bn, 72% down on the same quarter last year. As exit processes can typically take several months, it is likely that the pandemic and the initial wide-scale lockdowns are still having a delayed effect on activity. Now that GPs are seeing that portfolio valuations have largely been holding up, we may now see exit activity begin to pick up again.

One exit option that has lately attracted a lot of attention has been the use of special purpose acquisition companies (SPACs). A SPAC is a “blank cheque” shell corporation designed to take companies public without going through the traditional IPO process. The pandemic has caused this exit method to become much more popular given the increased uncertainty of performing an IPO in this environment. In the first nine months of 2020, US SPACs raised USD 42bn — 44% of all public offerings in the US3. A merger between a company and a SPAC can take about four to six months to complete, compared to an IPO which can take 12 to 18 months or longer. Furthermore, the valuation of a merger with a SPAC is pre-negotiated whereas the pricing of an IPO is set on the day before the listing.

In September, we benefited from this exit method when our portfolio company, Chargepoint (a global leader in electric charging vehicle stations), agreed to be acquired by a listed SPAC. The transaction values the company at USD 2.4bn and our holding will be locked up until Q2 2021 (although we can exit through a secondary sale in the meantime). At the current share price, our investment in Chargepoint will deliver over a 5x cost to our investors. Chargepoint has particularly benefited from the transition from petrol/diesel to electric vehicles. This trend has been steady even during the current pandemic. For example, in the UK, while overall new car registrations in September 2020 declined by 4% versus the prior year, electric car registrations increased by 184%.

The calm in the storm

In early April, we reported to clients our first assessment of the expected impact of the COVID-19 crisis on our funds and mandates by assessing the situation of the portfolio companies representing over 80% of the NAV of each programme. For each company, we considered both the impact on value and the financial headroom. Based on this deep analysis, we prepared our clients for a potential down valuation of our investment programmes in the following quarters in the range of 10% to 25%. It turned out that we were on the conservative side as valuations have fallen in some cases by up to 13% but in most cases have stayed flat or even positive.

Throughout the crisis, we have continued to monitor our programmes closely and have been on top of the developments in portfolio companies by maintaining regular contact with investment partners. In September, we conducted the COVID-19 impact analysis once again and presented the outcome to clients. Overall, we saw an improvement in our portfolios with the percentage of companies in the “high” and “medium” impact categories reducing by 15%. Furthermore, the percentage of companies which were considered to have “tight financial headrooms” reduced from 10% to 7%. However, in the majority of these cases, there are robust plans in place to support the companies through the crisis, even if the current second wave worsens.

This is a strong validation of our theme-driven investment strategy and the resilience of the business models in which we invest. Bike24, the leading e-commerce bicycle retailer in Germany, experienced a tremendous increase in demand during the crisis, driven by cycling being more popular during lockdown as well as a convenient way to avoid public transportation. As a result, Bike24’s valuation increased from 1.0x in Q4 2019 to 1.7x in Q2 2020.

Another success story is Jane Iredale, a US premium make-up and skincare producer, which distributes its products mostly through professional channel accounts, such as salons/spas as well as dermatological and other medical facilities. Those channels faced a massive loss of sales when the facilities had to close down. Thanks to a pro-active management team, the online channel janeiredale.com was further expanded and the company restructured, keeping the company on budget for the year. The company was marked up to 1.1x in Q2 2020 from 1.0x.

We believe that these examples highlight the attraction of small- and mid-market companies. Such companies are resilient in their own right thanks to strong market positions, management and financials, and are able to implement their growth plans irrespective of market conditions.

Unigestion Private Equity Activity

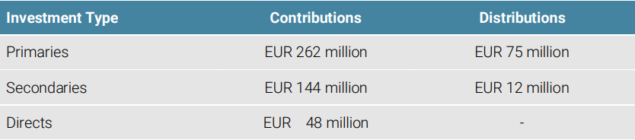

During the crisis, the private equity team of Unigestion has closed on some exceptional investment opportunities. From April 2020 to September 2020, Unigestion contributed EUR 454m to investments. We have closed commitments to three new primary funds, covering North America, Benelux and Scandinavia. In addition, we completed four new direct deals and four secondary transactions. In the same time period, Unigestion received distributions of investments of EUR 86m.

During the crisis, the private equity team of Unigestion has closed on some exceptional investment opportunities.

Figure 2: Investment Activity from April to September 2020

Source: Unigestion, October 2020.

In July, we closed a direct secondary transaction in two high-growth break-out portfolio companies. The first company is Blue Ocean Robotics, a developer of mobile professional

service robots. For example, these robots are used as cleaning robots to reduce the risk of virus transmission at London Heathrow Airport by using ultraviolet rays to kill viruses and bacteria. The other company is Bellabeat, a holistic women’s healthtech developer, which sells fashionable smart jewellery and associated apps. The company has around 1.6 million subscribers.

In August, we invested in Infobip, a communications platform service provider to major enterprises to help manage and execute customer communications across multiple channels (SMS, email, WhatsApp, etc.). For example, the company enables banks and

financial institutions to automatically send one-time passcodes by SMS to customers when logging into their online accounts.

The company, headquartered in the UK but with a global customer base, is the leader in its segment and is seeing revenue growth at over 30% per year.

In September, we committed to Vance Street III, a US, lower mid-market buyout fund. Vance Street Capital is based in Los Angeles and invests in

mid-sized companies in North America that provide high-tech, mission-critical products and services to blue-chip clients in the healthcare and industrial sectors. The firm typically makes investments of USD 25 to 50 million in family businesses or spin-offs that require professional management, operational improvements and strategic leadership.

In September, we invested in Avania, a full-service Clinical Research Organisation (“CRO”) which supports medical device companies in such areas as preclinical and clinical trials,

regulatory approval and commercialisation.This company is the only pure-play medical device CRO with a global offering. The medical device CRO market is growing at over 11% p.a. but is highly fragmented, thus offering the opportunity for the company to grow further through strategic add-on acquisitions.

In the same month, we invested in Evaluate, a provider of commercial market intelligence for the pharma industry. Evaluate has developed

a platform to streamline access to accurate, transparent commercial intelligence, supported by personalised, expert guidance and customised offerings. Over the past 20 years, it has become the go-to provider for market forecasting for new drugs. Indeed, its client base includes every single Top 25 pharma company and its revenues are 100% subscription-based with a net client retention rate of over 100%.

We also closed a secondary single asset restructuring in Ivanti, a global mid-market leader in IT enterprise software. The company provides

mission critical software that enables employee access to company applications and data, and to devices such as smart phones, tablets, desktops and laptops. Ivanti is the largest consolidator of mid and lower mid- market enterprise IT software companies, with a management team well versed in acquisition and integration. For that reason, the transaction includes an undrawn component to be used for acquisitions.

1Pitchbook, October 2020.

2Preqin, October 2020

3Financial Times

Important information

Past performance is no guide to the future, the value of investments, and the income from them change frequently, may fall as well as rise, there is no guarantee that your initial investment will be returned. This document has been prepared for your information only and must not be distributed, published, reproduced or disclosed (in whole or in part) by recipients to any other person without the prior written consent of Unigestion. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation.

This is a promotional statement of our investment philosophy and services only in relation to the subject matter of this presentation. It constitutes neither investment advice nor recommendation. This document represents no offer, solicitation or suggestion of suitability to subscribe in either the investment vehicles to which it refers or to any securities or financial instruments described herein. Any such offer to sell or solicitation of an offer to purchase shall be made only by formal offering documents, which include, among others, a confidential offering memorandum, limited partnership agreement (if applicable), investment management agreement (if applicable), operating agreement (if applicable), and related subscription documents (if applicable). Such documentation contains additional information material to any decision to invest. Please contact your professional adviser/consultant before making an investment decision.

Where possible we aim to disclose the material risks pertinent to this document. The views expressed in this document do not purport to be a complete description of the securities, markets and developments referred to in it. Reference to specific securities should not be considered a recommendation to buy or sell. Unigestion maintains the right to delete or modify information without prior notice.

Investors shall conduct their own analysis of the risks (including any legal, regulatory, tax or other consequences) associated with an investment and should seek independent professional advice. Some of the investment strategies or financial instruments described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment. These are not suitable for all types of investors. Unigestion has the ability in its sole discretion to change the strategies described herein.

To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks. Actual results could differ materially from those in the forward-looking statements. As such, forward looking statements should not be relied upon for future returns. Targeted returns reflect subjective determinations by Unigestion based on a variety of factors, including, among others, internal modeling, investment strategy, prior performance of similar products (if any), volatility measures, risk tolerance and market conditions. Targeted returns are not intended to be actual performance and should not be relied upon as an indication of actual or future performance.

No separate verification has been made as to the accuracy or completeness of the information herein. Data and graphical information herein are for information only and may have been derived from third party sources. Unigestion takes reasonable steps to verify, but does not guarantee, the accuracy and completeness of information from third party sources. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. All information provided here is subject to change without notice. It should only be considered current as of the date of publication without regard to the date on which you may access the information. Rates of exchange may cause the value of investments to go up or down. An investment with Unigestion, like all investments, contains risks, including total loss for the investor.

Unigestion Direct II (UDII) has been created as a SCS-SICAV-RAIF in Luxembourg and qualifies as an Alternative Investment Fund (AIF) within the meaning of the law dated 12 July 2013 on Alternative Investment Fund Managers implementing the Directive 2011/61/EU (AIFMD). As a result, units of this vehicle may be offered only to professional investors and may not be distributed on a public basis in or from any country where such distribution would be prohibited by law. This document contains a preliminary summary of the purpose and principal business terms of an investment in UDII. This summary does not purport to be complete and is qualified in its entirety by reference to the more detailed discussion to take place with the AIF. UDII has the ability in its sole discretion to change the strategies described herein. Before making a decision to invest in UDII, you are advised to consult with your tax, legal and financial advisors.

Additional Information for US Investors

The performance figures are based on estimated fees and expenses as well as on the underlying strategy’s estimated performances given by fund managers, administrators, custodians and third party sources at a given date. Where performance is reflected gross of fees, potential investors should be aware that the inclusion of fees, costs and charges will reduce the overall value of performance. Unless otherwise stated, the performance data source are Unigestion, Bloomberg and Compustat.

This information is provided to you solely to give you background information relating to Unigestion, certain strategies it implements and currently offers. Before making an investment decision with respect to the strategy discussed herein, potential investors are advised to consult with their tax, legal, ERISA and financial advisors. Note that not all strategies may be available or suitable for investment by U.S. investors.

This document may contain forward-looking statements, including observations about markets and industry and regulatory trends as of the original date of this document. Forward-looking statements may be identified by, among other things, the use of words such as “expects,” “anticipates,” “believes,” or “estimates,” or the negatives of these terms, and similar expressions. Forward-looking statements reflect Unigestion’s views as of such date with respect to possible future events. Actual results could differ materially from those in the forward-looking statements as a result of factors beyond a strategy’s or Unigestion’s control. Readers are cautioned not to place undue reliance on such statements. No party has an obligation to update any of the forward-looking statements in this document

Return targets or objectives, if any, are used for measurement or comparison purposes and only as a guideline for prospective investors to evaluate a particular investment program’s investment strategies and accompanying information. Performance may fluctuate, especially over short periods. Targeted returns should be evaluated over the time period indicated and not over shorter periods.

The past performance of Unigestion, its principals, shareholders, or employees is not indicative of future returns.

Except where otherwise specifically noted, the information contained herein, including performance data and assets under management, relates to the entire affiliated group of Unigestion entities over time including that of Unigestion UK. Such information is intended to provide the reader with background regarding the services, investment strategies and personnel of the Unigestion entities. No guarantee is made that all or any of the individuals involved in generating the performance on behalf the other Unigestion entities will be involved in managing any client account on behalf of Unigestion U.K. More specific information regarding Unigestion UK is set forth herein where indicated and is available on request.

There is no guarantee that Unigestion will be successful in achieving any investment objectives. An investment strategy contains risks, including the risk of complete loss.

The risk management practices and methods described herein are for illustrative purposes only and are subject to modification.

Legal Entities Disseminating This Document

UNITED KINGDOM

This material is disseminated in the United Kingdom by Unigestion (UK) Ltd., which is authorized and regulated by the Financial Conduct Authority (“FCA”). This information is intended only for professional clients and eligible counterparties, as defined in MiFID directive and has therefore not been adapted to retail clients.

UNITED STATES

This material is disseminated in the U.S. by Unigestion (UK) Ltd., which is registered as an investment adviser with the U.S. Securities and Exchange Commission (“SEC”). This information is intended only for institutional clients and qualified purchasers as defined by the SEC and has therefore not been adapted to retail clients.

EUROPEAN UNION

This material is disseminated in the European Union by Unigestion Asset Management (France) SA which is authorized and regulated by the French “Autorité des Marchés Financiers” (“AMF”).

This information is intended only for professional clients and eligible counterparties, as defined in the MiFID directive and has therefore not been adapted to retail clients.

CANADA

This material is disseminated in Canada by Unigestion Asset Management (Canada) Inc. which is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario, Quebec and Newfoundland & Labrador. Its principal regulator is the Ontario Securities Commission (“OSC”). This material may also be distributed by Unigestion SA which has an international advisor exemption in Quebec, Saskatchewan and Ontario. Unigestion SA’s assets are situated outside of Canada and, as such, there may be difficulty enforcing legal rights against it.

SWITZERLAND

This material is disseminated in Switzerland by Unigestion SA which is authorized and regulated by the Swiss Financial Market Supervisory Authority (“FINMA”).

Document issued November 2020.