Commodity markets have been largely uneventful in recent years, with the Bloomberg Commodity index trading in a relatively narrow range since 2015. However, last year’s pandemic crisis was a game changer with commodity markets enjoying a phenomenal run, capturing investors’ attention and making headlines. This move is being fuelled by what one could describe as a perfect storm of a supply and demand imbalances combined with ample liquidity thanks to extraordinary fiscal and monetary stimulus. As long as our macro / inflation scenario continues to play out, we think that commodity markets will continue to thrive over the next few years.

Forgotten Years

What’s Next?

The perfect alignment of supply and demand

Following the slump in commodity markets in 2015, global corporate spending across the commodity sectors, from energy to mining and agriculture, fell dramatically. This was a reaction to the oversupply and weakening demand following growth concerns around China, the world’s largest consumer. Similarly, the Covid crisis of 2020 led to a huge demand shock but, unlike many other asset classes, commodity markets also suffered further supply side constraints. For example, during the lockdowns, many mines were left temporarily closed or operating well below capacity. However, as a result of the extraordinary monetary and fiscal stimulus and the easing of post-vaccine lockdown measures, global growth, as indicated by our proprietary Nowcasters, experienced a sharp V-shape recovery leading to a sharp rise in demand for many commodities and some resulting shortages. Both our Growth Nowcasters and Newscasters continue to point towards an acceleration of global growth, which should continue to drive demand higher for commodities.

Aside from the strong growth momentum we are seeing, many governments have pledged huge infrastructure spending, which should further boost demand for commodities that underpin these projects. US President Biden has proposed a USD 2.3tn infrastructure plan, the EU has put together its EUR 750bn “NextGenerationEU” plan to make Europe greener, more digital and more resilient while Asian economies have also committed to similar infrastructure plans. The commodity story is therefore no longer purely reliant on Chinese growth. It is becoming a global phenomenon with all the stars aligning.

Commodities and inflation

Many end users are already facing significant price increases and shortages in their production chain. Input price inflation, one of the components of our proprietary Inflation Nowcaster indicator, has been one of the largest contributors to the indicator’s rising levels in countries such as Canada, Japan and the UK. We believe that producers will be left with little choice but to continue passing on those cost increases to consumers. Lumber, also known as timber, a type of hard or softwood used for structural purposes ranging from construction to furniture to planks, saw its price increase by a mind-blowing +900% year on year. The National Association of Home Builders (NAHB) in the US have already reported that the price surge in lumber has resulted in an increase of USD 36,000 for the average single-family home. Copper prices have more than doubled since their lows seen at the peak of the Covid crisis last year. Copper inventories on the London Metal Exchange are down close to 90% since 2011 and are now back to their 2020 lows at 268 metric tonnes.

The sharp rise in commodity prices further reinforces our view of a high probability of inflation surprise risk over the course of the year. Many central bankers around the world and some investors expect inflationary forces to be a temporary phenomenon, but we disagree. Just as the Covid crisis will have a long-term and lasting impact on the price and availability of certain commodities, we believe inflationary pressures will persist. Sovereign bond pricing therefore seems to show a misalignment with the underlying fundamental picture, unlike commodities, which seem to reflect the fundamental supply and demand imbalance. Commodity exposure also offers an excellent hedge against inflation surprise risk.

What about the oil market?

Oil experienced unprecedented price action during the Covid crisis as the sharp demand shock resulting from the global lockdowns sent its price into negative territory for the first time in history. Just like the rest of the commodity complex, oil has since made a strong comeback as demand returned along with the strong macro recovery and reopening of economies around the globe. Oil is an important component as it has a direct impact on most goods and services, and feeds directly into inflation via pass-through effects. The IMF estimates that a 10% increase in global oil inflation increases domestic inflation by an average of 0.4% on average, but adds that the effects can be asymmetric in nature given variations across countries, notably in CPI basket components, which can vary from country to country. Looking at the supply side, total US Shale oil production is still very far away from pre-Covid production levels and the picture is even more striking for Baker Hughes US Rig counts, which currently stand at 352, down from close to 700 in early 2020. US total crude oil inventories have also been moving south with stocks (excluding strategic petroleum reserve) reaching their pre-pandemic levels earlier in February this year despite having recently picked up over the last two months. We can expect more production down the line with OPEC likely to further raise production to meet increasing demand. In addition, US oil wells have also made a very strong comeback and production is now above their pre pandemic highs. Uncertainty remains around OPEC cuts: Iran could return to the market if sanctions are lifted while risks of further lockdowns remain due notably to the Indian Covid variant. As the world reopens and air travels resume we can expect demand for oil to remain firm particularly this summer, and for stocks to continue to fall, which should support the market.

Valuations

With many growth-oriented assets showing signs of exuberance and stretched valuations such as developed market equities, commodities are among the few market segments where valuations remain attractive. Many commodity markets remain in steep backwardation, such as Oil and Copper, which means that the forward price is discounted versus the current price level. Such backwardations provide a positive roll yield, making long commodity exposure particularly attractive from a valuation perspective.

Over the last year, commodity markets have experienced their strongest rally since the 1970’s. Despite these impressive moves, most commodity markets remain well below their highs of the last decade. In the short term, the relentless strength of some commodity markets and stretched positioning could leave the sector exposed to a potential pullback due to some deleveraging. However we believe that such pullback will provide a good buying opportunity as the commodity story remains very compelling over the medium to long term, both from fundamental and valuation perspectives as long as our macro scenario continues to unfold. Commodity markets will also continue to gain traction as investors look to increase inflationary hedges. As ever, there are risks that could challenge our view, notably around potential Covid variants, which could prove more resilient to vaccines and lead to further lockdowns. However, such a scenario remains a tail risk at this stage.

Despite the strong macro momentum, certain market segments are showing some stretched positioning and exuberance. A selective approach to asset allocation is therefore essential, which is why we favour cyclical trades in line with our high inflation surprise risk scenario. We therefore hold an overweight in cyclical commodities expressed via a long Energy and Industrial metals allocation. We also remain long cyclical global equities via an overweight to the Japanese Topix and the US Russell 2000 indices while keeping an underweight in Sovereign bonds as we believe a catch up will eventually take place despite a challenging few weeks of consolidation / retracements in yields. It is also worth highlighting that the initial phase of inflation we experienced was characterised by real assets outperforming assets with nominal cash flows. In the second phase of inflation we will likely see more discrimination between countries and sectors.

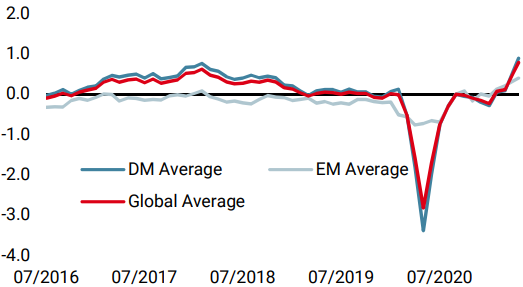

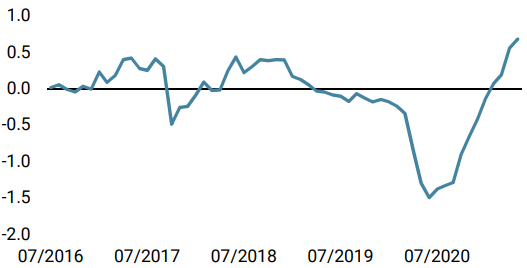

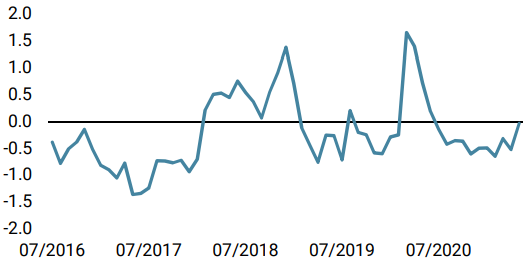

Unigestion Nowcasting

World Growth Nowcaster

World Inflation Nowcaster

Market Stress Nowcaster

Weekly Change

- Last week, our World Growth Nowcaster increased further with a broad improvement across countries, both developed and emerging.

- Our World Inflation Nowcaster is largely unchanged from its high level last week, as data gave a mixed picture over the week.

- Our Market Stress Nowcaster is unchanged from last week and remains at a neutral level.

Sources: Unigestion. Bloomberg, as of 21 May 2021

Important Information

This document is provided to you on a confidential basis and must not be distributed, published, reproduced or disclosed, in whole or part, to any other person.

The information and data presented in this document may discuss general market activity or industry trends but is not intended to be relied upon as a forecast, research or investment advice. It is not a financial promotion and represents no offer, solicitation or recommendation of any kind, to invest in the strategies or in the investment vehicles it refers to. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment.

The investment views, economic and market opinions or analysis expressed in this document present Unigestion’s judgement as at the date of publication without regard to the date on which you may access the information. There is no guarantee that these views and opinions expressed will be correct nor do they purport to be a complete description of the securities, markets and developments referred to in it. All information provided here is subject to change without notice. To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks.

Data and graphical information herein are for information only and may have been derived from third party sources. Although we believe that the information obtained from public and third party sources to be reliable, we have not independently verified it and we therefore cannot guarantee its accuracy or completeness. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. Unless otherwise stated, source is Unigestion. Past performance is not a guide to future performance. All investments contain risks, including total loss for the investor.

Unigestion SA is authorised and regulated by the Swiss Financial Market Supervisory Authority (FINMA). Unigestion (UK) Ltd. is authorised and regulated by the UK Financial Conduct Authority (FCA) and is registered with the Securities and Exchange Commission (SEC). Unigestion Asset Management (France) S.A. is authorised and regulated by the French “Autorité des Marchés Financiers” (AMF). Unigestion Asset Management (Canada) Inc., with offices in Toronto and Montreal, is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario and Quebec. Its principal regulator is the Ontario Securities Commission (OSC). Unigestion Asset Management (Copenhagen) is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Danish Financial Supervisory Authority” (DFSA). Unigestion Asset Management (Düsseldorf) SA is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Bundesanstalt für Finanzdienstleistungsaufsicht” (BAFIN).