Continued Headwinds Undermine Global Growth

Over the last month, growth conditions have deteriorated, and the global economy now looks to be expanding near its potential rate. The slowdown has primarily been driven by the US, where a combination of constrained household spending and worsening business sentiment has slowed the world’s largest economy. While the current level of growth is not worrisome on its own, the forward picture raises concerns: real wage growth in the US is negative at the same time that savings have been drawn down. Business sentiment remains on a downward trend, and the Fed is likely to begin its tightening cycle this week. If that was not enough, the continuation of the Russia/Ukraine conflict creates, in addition to the humanitarian cost, further macro uncertainty: disrupted trade, higher commodity prices, and isolation of the world’s eleventh largest economy.

Can’t Buy Me Love

What’s Next?

The global economy looks to be growing at potential

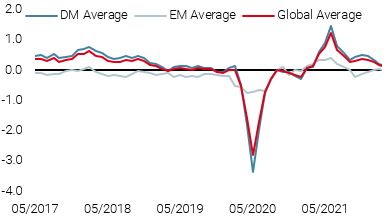

Global growth had been steady at an above-potential rate for most of Q4 2021 and the start of this year, thanks to a strong US expansion and a turn-around in the Chinese economy. However, over the last few weeks, the US economy looks to have lost some of its footing, weighing down on global growth. Figure 1 shows our Global Growth Nowcaster, as well as the Nowcaster for the world’s three key economies, highlighting the recent descent of the global indicator. Importantly, Eurozone growth has thus far remained robust, as all of its underlying components are at or above their long-term levels. Supportive monetary policy from the PBOC has also helped to boost demand from China, which now looks to be growing at an above-potential rate.

Figure 1: Growth Nowcasters

Source: Bloomberg, Unigestion. As of 09.03.2022.

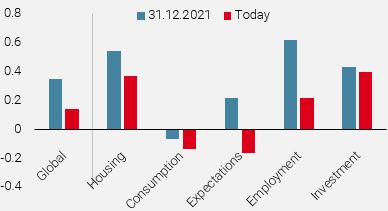

The impact of the deceleration in the US economy is also apparent when examining the underlying components of the Growth Nowcaster. As Figure 2 shows, the decline from the start of the year is largely driven by household consumption, which has been subdued for some time, business production expectations, and employment, as the jobs market normalises. Moreover, tighter monetary policy does not bode well for the housing sector, which is one of the largest contributors for now.

Figure 2: Global Growth Nowcaster and its Components

Source: Bloomberg, Unigestion. As of 09.03.2022

Importantly, the diffusion index of the Growth Nowcaster – the share of underlying data improving – has been 50% or lower since July of last year. Put another way, the majority of growth data has been deteriorating for seven months, suggesting the overall indicator is likely to continue falling.

US households: wage growth lagging inflation, putting further downward pressure on growth

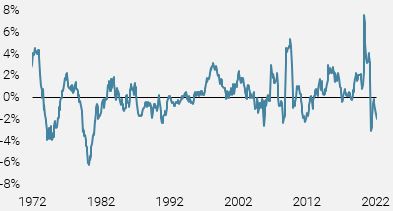

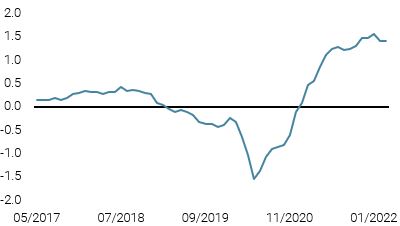

While the job market in the US has tightened significantly, with the unemployment rate down to 3.8% (versus a pre-Covid low of 3.5%), wage growth has not kept up with the massive pickup in inflation. Thus, households have seen their wages pay for less and less goods, creating a significant headwind for consumption to support the economy. Figure 3 puts real wage growth today in a longer-run perspective. While the picture is less dramatic than the 1970s, the inability of household incomes to keep up with inflation creates downward pressure on growth (via lower consumption and amplifying the risk of stagflation) or corporate margins (via higher labour costs). Neither alternative is a positive one for growth-oriented assets such as equities.

Figure 3: YoY Growth in Average Real Hourly Earnings for Private Nonfarm Payrolls

Source: Bloomberg, Unigestion. As of 10.03.2022

Of course, households could draw down on savings or use credit to finance spending. However, personal savings are back to their pre-Covid levels while tighter monetary policy will likely constrain credit growth.

Production expectations declining in US, stable in Eurozone

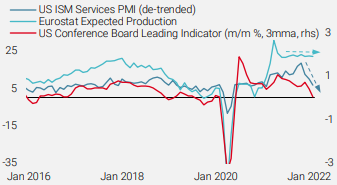

The other key element constraining growth has been the business environment, especially in the US, where the combination of the omicron surge at the end of last year, expectations of tighter monetary policy, and fading fiscal impulse have driven sentiment lower. Figure 4 shows the decline in two key macro data series: the ISM Services PMI and the month-over-month change in the US Conference Board’s Leading Indicator. While business investment remains supportive (see Figure 2), a continuation of this trend would likely lead to lower investments, as businesses scale back investment activity in the face of potentially lower demand.

Figure 4: US and European Production Expectations Surveys

Source: Bloomberg, Unigestion. As of 10.03.2022

In contrast, production expectations among European businesses has remained firmer, helping to support the growth dynamic in the Eurozone.

Russia/Ukraine conflict adds further uncertainty

The slowing growth dynamic is even more worrisome as the Russian/Ukraine conflict continues to unfold. In addition to the direct impact on each country’s economy, Russia’s role as key exporter of commodities, from energy to base metals to agriculture, has a significant impact on global growth. These commodities have surged since the Russian invasion, with their respective Bloomberg indices up 40%, 33%, and 23% year-to-date. As discussed last week, this run-up in commodity prices often precedes a recession, as households reduce real spending and corporate profitability declines, dis-incentivising investments, and leading to demand destruction.

While the risk of recession in the near-term remains low, it has risen significantly and will likely continue to do so, given the broader monetary and geopolitical context. Indeed, our Global Growth Newscaster, a fast-moving indicator based on news sentiment that tends to lead our Nowcaster especially around turning points, has shifted into high recession risk territory. By construction, this signal is volatile, but if present conditions persist, we would expect our Growth Nowcaster to also shift into the same direction, leading our dynamic allocation to become more defensive as a result. In the meantime, we maintain a cautious allocation, with lower deployed risk that is selective in its modest growth exposure.

Unigestion Nowcasting

World Growth Nowcaster

World Inflation Nowcaster

Market Stress Nowcaster

Weekly Change

- Last week, our World Growth Nowcaster ticked slightly lower on data from the US and China.

- Our World Inflation Nowcaster moved slightly lower, as many economies saw reduced, but still high, inflationary pressures.

- Our Market Stress Nowcaster moved up slightly, as volatilities grinded higher.

Sources: Unigestion, Bloomberg, as of 11 March 2022

Important Information

This document is provided to you on a confidential basis and must not be distributed, published, reproduced or disclosed, in whole or part, to any other person.

The information and data presented in this document may discuss general market activity or industry trends but is not intended to be relied upon as a forecast, research or investment advice. It is not a financial promotion and represents no offer, solicitation or recommendation of any kind, to invest in the strategies or in the investment vehicles it refers to. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment.

The investment views, economic and market opinions or analysis expressed in this document present Unigestion’s judgement as at the date of publication without regard to the date on which you may access the information. There is no guarantee that these views and opinions expressed will be correct nor do they purport to be a complete description of the securities, markets and developments referred to in it. All information provided here is subject to change without notice. To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks.

Data and graphical information herein are for information only and may have been derived from third party sources. Although we believe that the information obtained from public and third party sources to be reliable, we have not independently verified it and we therefore cannot guarantee its accuracy or completeness. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. Unless otherwise stated, source is Unigestion. Past performance is not a guide to future performance. All investments contain risks, including total loss for the investor.

Unigestion SA is authorised and regulated by the Swiss Financial Market Supervisory Authority (FINMA). Unigestion (UK) Ltd. is authorised and regulated by the UK Financial Conduct Authority (FCA) and is registered with the Securities and Exchange Commission (SEC). Unigestion Asset Management (France) S.A. is authorised and regulated by the French “Autorité des Marchés Financiers” (AMF). Unigestion Asset Management (Canada) Inc., with offices in Toronto and Montreal, is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario and Quebec. Its principal regulator is the Ontario Securities Commission (OSC). Unigestion Asset Management (Copenhagen) is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Danish Financial Supervisory Authority” (DFSA). Unigestion Asset Management (Düsseldorf) SA is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Bundesanstalt für Finanzdienstleistungsaufsicht” (BAFIN).