Risk appetite has skyrocketed since the beginning of the year, as monetary and fiscal support remain in full swing and expectations of future growth and reflation have continued to improve. A traditional “risk-on” rally pushed equity indices to record highs, commodities boomed and bond yields surged as the reflation theme gained traction. However, credit returns have remained muted, raising questions: why has performance been so tepid in spite of rising risk appetite globally, and what can we expect from the asset class over the short to medium term?

Low Expectations

What’s Next?

Macro will remain supportive

In the fixed income space, and credit in particular, macro-driven fundamentals are a key driver, as investors seek to avoid corporate issuers that could potentially default. Even if the global risk environment does matter to credit pricing, the asset class remains primarily driven by economic factors rather than speculation or technical factors, as it is often the case in the equities world. It can explain why the asset class can be resilient in certain shocks, as it was in early 2018 during the implosion of the volatility complex, or why it underperformed stocks on a risk-adjusted basis during the Covid-19 crisis.

The economic situation today is less rosy than it was at the end of last year due to the impact of renewed lockdowns to contain the second wave of the pandemic. Our proprietary Growth Nowcasters peaked in terms of both level and diffusion indices between November and December 2020 and have fallen steadily since then in the case of developed economies. The proportion of improving macroeconomic data fell to 50% in Europe and 40% in North America and Japan, but has stabilised around these levels. Nevertheless, we believe this slowdown will only be temporary as the vaccination campaign is increasing the odds of reduced containment measures and increases our confidence in a complete macro recovery by year-end.

Expectations for 2021 remain strong enough to justify current spread levels across the credit spectrum. Economic activity should achieve above potential growth as countries emerge from the pandemic with massive fiscal and monetary support, propelling capex, consumption, and employment. Increasing demand in the sectors that have been most impacted by Covid-related measures will provide an extra boost to growth that should help to materially reduce credit default risk. In 2020, 8% of US High Yield (HY) issuers defaulted, of which two thirds were companies operating in Energy and consumer-related sectors. Given our positive expectations for global trade and the very high level of savings still to be injected in the economy, default rates should come down in 2021, as already implied by current market pricing.

Sentiment has become excessive

Sentiment and momentum in risk assets have continued to rise rapidly in 2021 but now seem extreme. Many indices have reached record highs, cash levels held by pension investors have shrunk to historical lows while riskier, more speculative segments of the market that were overlooked last year have been favoured this year. In HY, the difference between option-adjusted spreads in CCC and B-rated US names has tightened to historical lows: below 200bps. At the sector level, spreads in the Energy sector have strongly outperformed, tightening by 96bps since the end of 2020, compared to Cyclicals and Industrials, which are 30bps and 5bps tighter respectively. Positioning in synthetic indices, although not as extreme as it was a month ago, remains close to historical highs, both in investment grade (IG) and HY markets. Trend following strategies now also hold substantial longs in the asset class given the momentum observed since the beginning of the recovery in Q2 2020.

Volatility has also strongly receded in the asset class, diverging meaningfully with the trajectory in equity volatility that remains well above historical lows. This is yet another indication of rising complacency and a disconnection between typically very correlated risk premia. Beta to equities has decreased materially too, which also explains the divergence in volatility compression between the two asset classes. Stocks have room to expand multiples further, driven by flows and the lack of decent alternatives, while current pricing and positioning in credit leaves little room for further spread compression. On the downside, credit is vulnerable to macro shocks and global deleveraging, but lower liquidity in the asset class makes it more sticky and typically less impacted by technical sell-offs than in equities. During the last week of January, the MSCI World index dropped by 4% but major HY indices only lost 75bps, less than half the loss historical correlations would have implied.

Consequently, we believe that positioning and sentiment in credit has reached extremely high levels, leaving it vulnerable to the high macro volatility environment that we expect over the year ahead. Spreads have bottomed over the short term and we expect little spread compression, if not widening.

Valuations are rich, risk reward is unattractive

While macro expectations support the case for credit spreads to remain at historical lows for some time, current market pricing (valuations) indicates that positive news has already been discounted, depressing expected returns and leaving investors with low compensation for risks taken. If history is any guide, these spread levels have rarely led to incremental capital appreciation. Over the last 15 years, net positive performance from these levels over an ensuing three-month period only occurred 58% of the time with almost no occurrence of above-carry returns. This means that the base case over the next few months is for 15bps returns in IG and below 1% for HY. Given credit duration, only a slight widening in spreads over the period will eat up a full year of carry, creating a very unfavourable risk reward profile in the asset class over the short term.

Adjusted for inflation (real expected returns), the picture looks even darker. For the first time in history, 40% of issues in the IG space yield an inflation-adjusted yield below -0.5%. This very favourable spread environment for issuers should push corporates to increase supply, either to fund upcoming maturities or to finance share buybacks. Those changes in capital structures could prove beneficial for equity investors while creditors will face deteriorated balance sheets due to higher use of leverage and receive negative real returns in exchange. For the majority of investors holding physical corporate bonds, duration represents another valuation mispricing, which started to correct this year and will continue to do so. Therefore, the combination of higher duration, very low spreads and deteriorating capital structures currently puts the credit space at risk.

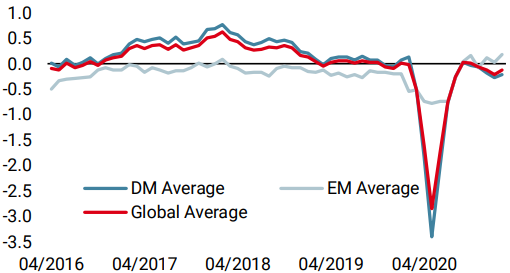

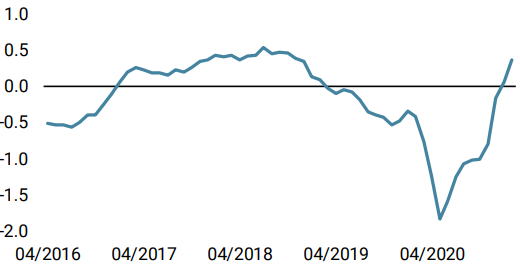

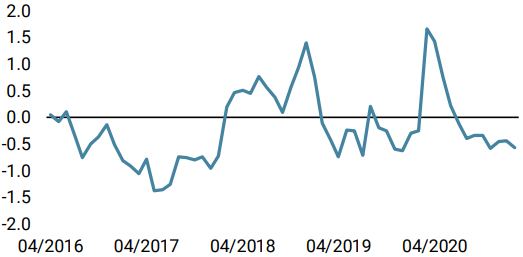

Unigestion Nowcasting

World Growth Nowcaster

World Inflation Nowcaster

Market Stress Nowcaster

Weekly Change

- Last week, our World Growth Nowcaster increased as US and Canadian data improved. Recession risk is low.

- Our World Inflation Nowcaster increased significantly, especially on the US front. Inflation risk is very high.

- Our Market Stress Nowcaster remained stable, showing signs of investor bullishness.

Sources: Unigestion. Bloomberg, as of 18 February 2021.

Important Information

This document is provided to you on a confidential basis and must not be distributed, published, reproduced or disclosed, in whole or part, to any other person.

The information and data presented in this document may discuss general market activity or industry trends but is not intended to be relied upon as a forecast, research or investment advice. It is not a financial promotion and represents no offer, solicitation or recommendation of any kind, to invest in the strategies or in the investment vehicles it refers to. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment.

The investment views, economic and market opinions or analysis expressed in this document present Unigestion’s judgement as at the date of publication without regard to the date on which you may access the information. There is no guarantee that these views and opinions expressed will be correct nor do they purport to be a complete description of the securities, markets and developments referred to in it. All information provided here is subject to change without notice. To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks.

Data and graphical information herein are for information only and may have been derived from third party sources. Although we believe that the information obtained from public and third party sources to be reliable, we have not independently verified it and we therefore cannot guarantee its accuracy or completeness. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. Unless otherwise stated, source is Unigestion. Past performance is not a guide to future performance. All investments contain risks, including total loss for the investor.

Unigestion SA is authorised and regulated by the Swiss Financial Market Supervisory Authority (FINMA). Unigestion (UK) Ltd. is authorised and regulated by the UK Financial Conduct Authority (FCA) and is registered with the Securities and Exchange Commission (SEC). Unigestion Asset Management (France) S.A. is authorised and regulated by the French “Autorité des Marchés Financiers” (AMF). Unigestion Asset Management (Canada) Inc., with offices in Toronto and Montreal, is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario and Quebec. Its principal regulator is the Ontario Securities Commission (OSC). Unigestion Asset Management (Copenhagen) is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Danish Financial Supervisory Authority” (DFSA). Unigestion Asset Management (Düsseldorf) SA is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Bundesanstalt für Finanzdienstleistungsaufsicht” (BAFIN).