Q2 2021 earnings season will kick into full swing this week, with the majority of US and European firms reporting. Expectations for earnings growth may seem elevated in year-over-year terms, but Q2 2020 was the trough for earnings and different perspectives reveal that estimates are not particularly stretched. In addition to the top-line and bottom-line numbers, we will also be paying close attention to how firms are using their significant capital reserves, as their decisions have important consequences on the sustainability of the economic recovery, inflation, and financial markets.

Work It

What’s Next?

Strong results met with underwhelming market reaction

This week will see the bulk of firms in the US and Europe report their Q2 2021 results: nearly 200 firms in each of the S&P 500 and Stoxx 600, representing almost 50% of their respective index’s market cap. On a year-over-year basis, earnings-per-share (EPS) are expected to grow 67% for US firms and 75% for European ones, reflecting the nadir in earnings delivery last year on the back of the lockdowns seen in Q2 2020. However, on a quarter-over-quarter basis, expectations are more muted: 5% higher for the S&P 500 compared to Q1 2021 and 10% lower for the Stoxx 600. Moreover, compared to Q2 2019 – before the world had ever heard of COVID-19 – EPS is expected to grow by a measly 14% and 3% for the S&P 500 and Stoxx 600, respectively.

It is not surprising, therefore, that results so far are strongly beating estimates: of the already-reported firms in the S&P 500, 85% have beat on earnings and 80% have beat on sales. For the Stoxx 600, these numbers are 61% and 69%, respectively. Importantly, however, investors seem to be more positive than analysts heading into the season: those firms missing their expectations have been punished much more than firms who beat on theirs. For example, S&P 500 firms who missed their EPS and sales estimates underperformed the broader index by -3.3% after announcing their results on average, while those firms beating on these numbers outperformed the index by just 0.5%.

What will firms do with their large cash holdings?

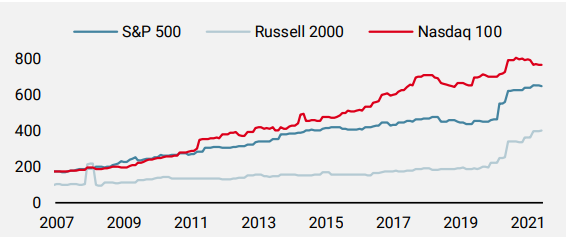

Beyond sales activity and profitability, corporate guidance on future plans to put their earnings to use has direct implications for the macroeconomic context and financial markets. As we have pointed out previously, firms have built up a significant amount of cash (and cash-like instruments) on their balance sheets following the coronavirus crisis. As Figure 1 shows, while the large-cap firms in the Nasdaq 100 are outpacing others, the phenomenon holds true even when we look at the small-to-mid-cap Russell 2000.

Figure 1: Cash and Cash Equivalents per Share

Source: Unigestion, Bloomberg, as of 23 July 2021.

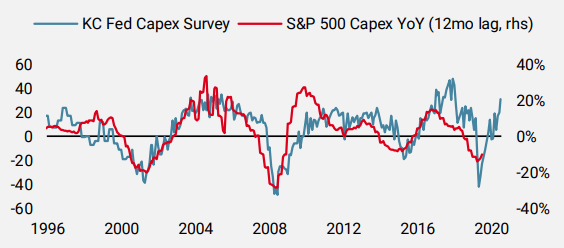

One key use of these reserves would be capital expenditure, which had been decelerating for some time before the pandemic and shifted into outright contraction last year. Capex surveys, for example the one administered by the Kansas City (KC) Fed, indicate that corporate investment activity should pick up meaningfully in the months ahead. Figure 2 demonstrates the reasonably tight link between this survey and actual capex growth for the S&P 500 (lagged by 12 months). If the historical relationship holds, a capex recovery would support near-term growth and put it on a more sustainable path. At the same time, given supply chain issues, inflation pressures would likely accelerate in the short-term, even if they fall over the long-term due to improved capacity.

Figure 2: Capex Expectations and Reality

Source: Unigestion, Bloomberg, as of 23 July 2021.

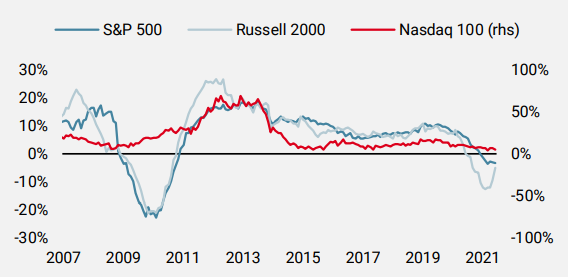

While firms have spent the last few years engaging in less capex, they have been more active in returning capital to shareholders. Figure 3 shows the growth in dividends per share (cumulated over 12 months) for the S&P 500, Russell 2000, and Nasdaq 100 (which is charted on the right axis to aid clarity). Both the S&P 500 and Russell 2000 saw dividends grow from about 5% year-over-year in 2016 to 10% in 2019. The Nasdaq 100 saw its dividend growth rate go from 5% in 2015 to 16% in 2019. Following the pandemic, dividends have struggled to grow, in line with earnings, but have recently started to show stability or even recovery.

Figure 3: Year-over-year Change in Trailing 12m Dividends per Share

Source: Unigestion, Bloomberg, as of 23 July 2021.

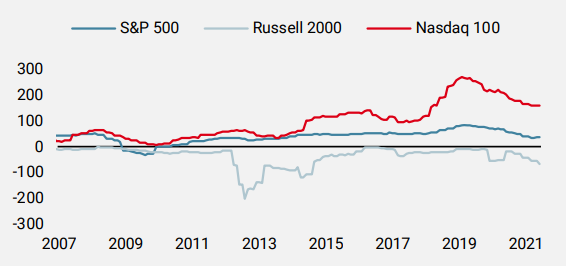

Another key channel for returning capital to shareholders is buybacks. Following banner years for corporate buybacks in 2018 and 2019, buybacks cooled in 2020 even though they remain elevated relative to their long-term history. Figure 4 charts net buybacks (buybacks less issuance) per share, showing how most of this activity was concentrated in the mega-cap tech names found in the Nasdaq 100. After the cool down in 2020, 2021 has seen a stabilisation and looking at announced buybacks from S&P 500 firms, the pace is consistent with that seen in 2019. If firms follow through on their plans, this reduction in equity supply would be a significant tailwind for markets over the rest of the year. On the other hand, it is interesting to note that firms in the Russell 2000 have, on net, been increasing their equity supply over the last few years.

Figure 4: Net Buybacks per Share (USD m)

Source: Unigestion, Bloomberg, as of 23 July 2021.

We continue to expect a stronger recovery than market consensus

While we have recently seen and communicated on a slowing of the macro momentum, our medium-term view has not meaningfully changed: we believe the recovery will be longer, broader, and stronger than expected. From the corporate sector, we expect strong profitability to be used to add further support to the real economy as well as provide some tailwinds for markets. While expectations for this year are high, those for next year are, importantly, much more muted. For instance, S&P 500 2022 earnings are expected to grow by 11% over their 2021 estimates, half of the 23% pace they have averaged since 1990. This motivates our preference to remain positive on growth assets, specifically developed market equities, even as we have reduced our negative view on nominal bonds and remain long the US dollar.

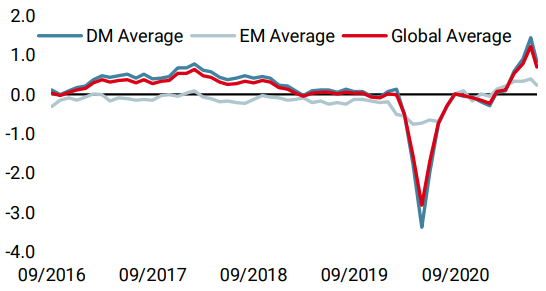

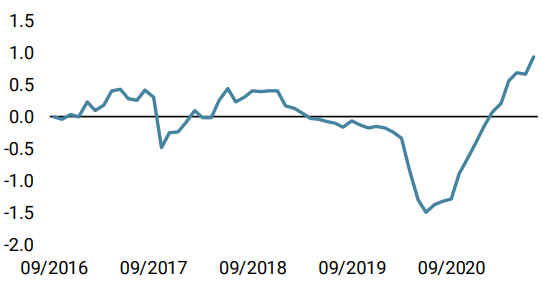

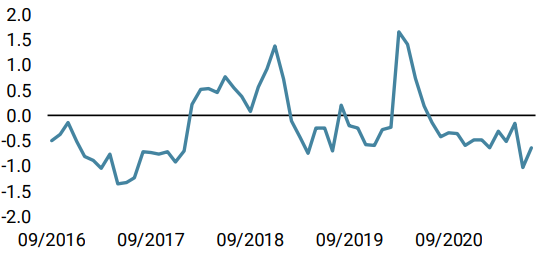

Unigestion Nowcasting

World Growth Nowcaster

World Inflation Nowcaster

Market Stress Nowcaster

Weekly Change

- Last week, our World Growth Nowcaster moved lower due to fading momentum in US and UK consumption.

- Our World Inflation Nowcaster remained steady at elevated levels with most countries seeing stable inflation pressures.

- Our Market Stress Nowcaster decreased modestly due to lower market volatilities.

Sources: Unigestion, Bloomberg, as of 23 July 2021.

Important Information

This document is provided to you on a confidential basis and must not be distributed, published, reproduced or disclosed, in whole or part, to any other person.

The information and data presented in this document may discuss general market activity or industry trends but is not intended to be relied upon as a forecast, research or investment advice. It is not a financial promotion and represents no offer, solicitation or recommendation of any kind, to invest in the strategies or in the investment vehicles it refers to. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment.

The investment views, economic and market opinions or analysis expressed in this document present Unigestion’s judgement as at the date of publication without regard to the date on which you may access the information. There is no guarantee that these views and opinions expressed will be correct nor do they purport to be a complete description of the securities, markets and developments referred to in it. All information provided here is subject to change without notice. To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks.

Data and graphical information herein are for information only and may have been derived from third party sources. Although we believe that the information obtained from public and third party sources to be reliable, we have not independently verified it and we therefore cannot guarantee its accuracy or completeness. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. Unless otherwise stated, source is Unigestion. Past performance is not a guide to future performance. All investments contain risks, including total loss for the investor.

Unigestion SA is authorised and regulated by the Swiss Financial Market Supervisory Authority (FINMA). Unigestion (UK) Ltd. is authorised and regulated by the UK Financial Conduct Authority (FCA) and is registered with the Securities and Exchange Commission (SEC). Unigestion Asset Management (France) S.A. is authorised and regulated by the French “Autorité des Marchés Financiers” (AMF). Unigestion Asset Management (Canada) Inc., with offices in Toronto and Montreal, is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario and Quebec. Its principal regulator is the Ontario Securities Commission (OSC). Unigestion Asset Management (Copenhagen) is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Danish Financial Supervisory Authority” (DFSA). Unigestion Asset Management (Düsseldorf) SA is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Bundesanstalt für Finanzdienstleistungsaufsicht” (BAFIN).