Over the year so far, 16 central banks have eased for a total of 23 moves and a cumulative 1,060 basis points. Understandably, macro data, except inflation, did not get a lot of attention as most investors are convinced that central banks will successfully re-stimulate the economy as they did during the late ‘90s pre-emptive easing cycles. The market’s preoccupation with interest rates has been notable for some time, leading investors to read bad news as good news and vice versa. Interest rates have been the main driver of almost all asset classes and the steady “everything rally” forced even highly risk-averse investors up the risk ladder into more crowded positions. The trade talks between China and the US ended on a “constructive” note and the next round of talks were scheduled for September. The Fed meeting passed and implied volatilities were pricing a quiet summer. Sentiment was upbeat, valuations were mostly irrelevant… until the daydreamers were woken up by a tweet. Market expectations were high going into the long-awaited Fed July meeting, so it proved tough to deliver a dovish surprise. Donald Trump made no secret of the fact that he was not happy with Jerome Powell’s decision, and shortly thereafter, he increased the pressure on China by taxing essentially all Chinese imports. Is the US president convinced that he has discovered a free lunch? The Fed has remained politically independent so far, but Trump seems very confident that central bankers will react to changing economic and financial conditions. In his view, he will be able to bash the Fed and China, which appears to be popular with voters, without paying the price for it. However, the White House’s high-stake game of chicken with China and the Fed could have serious consequences. Trump will probably succeed in pressuring the Fed, as the risk of recession would be too high to face if it backfired. However, comments like “we will be taxing the hell out of China” will not work, as the Politburo is fully aware that a trade war-induced recession would greatly reduce the probability of Trump’s re-election. By contrast, the Chinese president, Xi Jinping, does not have to think in election cycles and therefore time seems to be ticking in his favour. Our US proprietary macro Nowcasters show a similar picture as during the 1995-1998 period: decent levels of growth with falling inflation. However, the backdrop is more challenging this time. During the late nineties, emerging markets were suffering from a currency crisis, but developed countries were in a much better situation than they are currently. Over the past months, the global business cycle has decelerated noticeably and global trade has been hit hard by the trade war. Open, export-oriented countries like Germany are caught in the crossfire. German industrial production in June saw its largest fall in almost a decade and business expectations have fallen below the levels seen during the last European recession.“Daydreamer” – David Cassidy, 1973

What’s Next?

Game of chicken

Is the US consumer immune to tariffs?

The latest threat to raise tariffs on the remaining USD 300 bn of Chinese exports to the US will put even more pressure on the fragile manufacturing sector. This will be a real game-changer for the US consumer, who was largely immune until now as consumer products were excluded in the earlier rounds of tariffs. This comes at a time when upbeat consumers (US consumer confidence is at an eighth-month high) are the only major growth driver.

The key question will be how much more desperately needed stimulus will come from the consumer given that unemployment is already at a five-decade low and sustained wage gains and more affordable mortgages are already priced in? Private and corporate debt will no longer fuel the economy as consumers (beyond mortgages) and corporates have aggressively levered up during this extended business cycle.

The market was very nervous going into the Fed meeting as most of the systematic strategies had increased exposure to risky assets and even the most defensive discretionary investors were forced up the risk ladder due to the steady “everything rally”. There was some kind of a relief, despite a disappointing cut, after the Fed meeting had passed. The S&P 500 index was about to retest its highs and complacent investors were about to fall back into daydreaming. But then President Trump’s tweet hit the market. Over the next three days, the major US indices dropped over 8% on an intraday basis and the VIX spiked to 24.8, driven by the threat of tariff increases. However, the market shock seemed to be short lived and complacency and confidence were back almost as fast as they had disappeared. If a tweet can provoke such an overshoot in the most liquid instruments, it will be interesting to see how illiquid, crowded passive instruments will absorb a market shock that lasts longer than three days. The dovish Fed pivot has clearly driven the equity market rally in 2019. More than 90% of the gains in the S&P 500 index have been driven by valuation expansions, as earnings growth expectations weakened but the market priced in central bank cuts. The market consensus is that the move lower in rates is supportive for equities, justifying above-average valuations going forward. But shouldn’t lower yields also be a reflection of weaker growth? Even if sales can grow moderately during low growth, profit margins are likely to remain under pressure from wage growth, supply chain disruption, rising input costs and slowing capex due to the trade war. The earnings cycle remains crucial for equity markets, and while central banks are starting to loosen their monetary policy to reflate the economy, we doubt this will be enough to save current expectations of double-digit EPS growth for 2020 and 2021.Liquidity is a coward; it disappears at the first sign of trouble

Valuations do not matter until they do

We see a low recession risk probability, coupled with increased odds of negative inflation surprises. Therefore, central banks will have enough flexibility to pump even more liquidity into the system, which favours carry strategies. Markets are clearly on-edge regarding trade, but equally willing to “buy the dip”. Accordingly, sentiment and valuation have made a comeback, leading to a reduction of our overall market exposure. We keep on protecting tail risk via convex option strategies.Cross asset allocation: cautious and dynamic

Daydreamer

Our medium-term views remain cautious, and we prefer to get exposure to growth via high yield corporate credit. We are also complementing our modest equity exposure with options to protect the portfolio in the case of equity drawdowns. Over the month of August thus far, the Uni-Global – Cross Asset Navigator fund is down 0.6% versus a 2.7% fall for the MSCI AC World Index, while the Barclays Global Aggregate (USD hedged) is up 1.0%. Year-to-date, the Uni-Global – Cross Asset Navigator has returned 7.7% versus 13.5% for the MSCI AC World index and 8.0% for the Barclays Global Aggregate (USD hedged) index.Strategy Behaviour

Performance Review

Unigestion Nowcasting

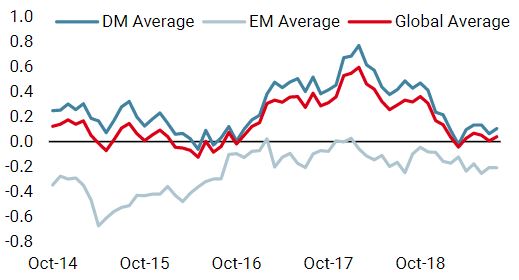

World Growth Nowcaster

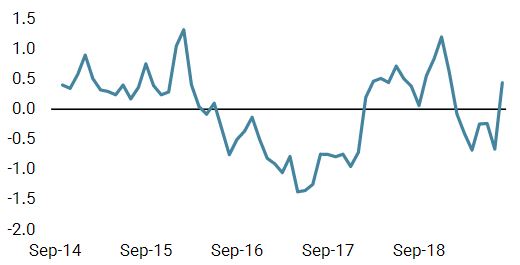

World Inflation Nowcaster

Market Stress Nowcaster

Weekly Change

- Our world Growth Nowcaster improved this week, largely driven by an improvement in US consumption.

- Our world Inflation Nowcaster declined further this week, with both the US and Switzerland seeing weaker supply-side inflation.

- Market stress picked up this week, as the trade war uncertainty continues, lifting volatility and widening spreads.

Sources: Unigestion, Bloomberg, as of 12 August 2019.

Past performance is no guide to the future, the value of investments can fall as well as rise, there is no guarantee that your initial investment will be returned. Important Information Past performance is no guide to the future, the value of investments, and the income from them change frequently, may fall as well as rise, there is no guarantee that your initial investment will be returned. This document has been prepared for your information only and must not be distributed, published, reproduced or disclosed by recipients to any other person. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. This is a promotional statement of our investment philosophy and services only in relation to the subject matter of this presentation. It constitutes neither investment advice nor recommendation. This document represents no offer, solicitation or suggestion of suitability to subscribe in the investment vehicles to which it refers. Any such offer to sell or solicitation of an offer to purchase shall be made only by formal offering documents, which include, among others, a confidential offering memorandum, limited partnership agreement (if applicable), investment management agreement (if applicable), operating agreement (if applicable), and related subscription documents (if applicable). Please contact your professional adviser/consultant before making an investment decision. Where possible we aim to disclose the material risks pertinent to this document, and as such these should be noted on the individual document pages. The views expressed in this document do not purport to be a complete description of the securities, markets and developments referred to in it. Reference to specific securities should not be considered a recommendation to buy or sell. Investors shall conduct their own analysis of the risks (including any legal, regulatory, tax or other consequences) associated with an investment and should seek independent professional advice. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment. These are not suitable for all types of investors. To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks. Actual results could differ materially from those in the forward-looking statements. As such, forward looking statements should not be relied upon for future returns. Targeted returns reflect subjective determinations by Unigestion based on a variety of factors, including, among others, internal modeling, investment strategy, prior performance of similar products (if any), volatility measures, risk tolerance and market conditions. Targeted returns are not intended to be actual performance and should not be relied upon as an indication of actual or future performance. Data and graphical information herein are for information only and may have been derived from third party sources. Unigestion takes reasonable steps to verify, but does not guarantee, the accuracy and completeness of this information. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. All information provided here is subject to change without notice. It should only be considered current as of the date of publication without regard to the date on which you may access the information. Rates of exchange may cause the value of investments to go up or down. An investment with Unigestion, like all investments, contains risks, including total loss for the investor. Uni-Global – Cross Asset Navigator is a compartment of the Luxembourg Uni-Global SICAV Part I, UCITS IV compliant. This compartment is currently authorised for distribution in Austria, Belgium, Denmark, Finland, France, Germany, Ireland, Italy, Luxembourg, Netherlands, Norway, Spain, UK, Sweden, and Switzerland. In Italy, this compartment can be offered only to qualified investors within the meaning of art.100 D. Leg. 58/1998. Its shares may not be offered or distributed in any country where such offer or distribution would be prohibited by law. No prospectus has been filed with a Canadian securities regulatory authority to qualify the distribution of units of these funds and no such authority has expressed an opinion about these securities. Accordingly, their units may not be offered or distributed in Canada except to permitted clients who benefit from an exemption from the requirement to deliver a prospectus under securities legislation and where such offer or distribution would be prohibited by law. All investors must obtain and carefully read the applicable offering memorandum which contains additional information needed to evaluate the potential investment and provides important disclosures regarding risks, fees and expenses. All investors must obtain and carefully read the prospectus which contains additional information needed to evaluate the potential investment and provides important disclosures regarding risks, fees and expenses. Unless otherwise stated performance is shown net of fees in USD and does not include the commission and fees charged at the time of subscribing for or redeeming shares. Unigestion UK, which is authorised and regulated by the UK Financial Conduct Authority, has issued this document. Unigestion SA authorised and regulated by the Swiss FINMA. Unigestion Asset Management (France) S.A. authorised and regulated by the French Autorité des Marchés Financiers. Unigestion Asia Pte Limited authorised and regulated by the Monetary Authority of Singapore. Performance source: Unigestion, Bloomberg, Morningstar. Performance is shown on an annualised basis unless otherwise stated and is based on Uni Global – Cross Asset Navigator RA-USD net of fees with data from 15 December 2014 to 12 August 2019.Navigator Fund Performance

Performance, net of fees

2018

2017

2016

2015

Navigator (inception 15 December 2014)

-3.6%

10.6%

4.4%

-2.2%