“Defying Gravity” – Wicked, 2003

A great disconnect is currently playing out in markets: economic data is deteriorating, as widely acknowledged by central banks around the world, while equity markets are rising, defying gravity. Over past experiences, such as in 2011 or 2015, gravity eventually got the upper hand. In our opinion, today is no different and the next earnings season is likely to reveal a worse-than-expected corporate profits picture. Most of the signs are there and the attraction force of bad news will strike back. We remain firmly grounded in the cautious camp.

What’s Next?

Complacency all over the place

In our view, there are three reasons that could explain why markets disagree with the clues that the economic situation could be more severe than expected.

First of all, there is actually a limited consensus around the fact that a world recession is currently brewing. US growth in 2019 is still expected to be at 2.4%, while the Eurozone’s is expected to reach 1.2%. Weaker activity is only expected for Q1: the Atlanta Fed’s GDPnow is putting Q1 growth in the US at 0.4% (annualised), while the New York Fed Nowcaster expects it to be 1.4%. Our own US Growth Nowcaster sees growth of 1.5%. A recession is not yet on the cards for the majority of economists – or even in the data for now. But we think that the direction of data is currently more important than their absolute levels.

Second, there are mild signs of a recovery from this long stream of decelerating data. In the US, the National Association of Home Builders’ surveys published last week are pointing to a stable to better situation. Oil prices have recovered significantly, increasing by 35% since their lows of December 2018, which rarely happens over a period of recession. The Philadelphia Fed Business Outlook survey also corrected from its drop from last month, surprising economists on the upside, while capacity utilisation rates remain in elevated territory, showing very limited signs of a deteriorating situation. Without denying this more positive news, we think the US is not the heart of the problem: Europe is.

Third, markets have also acquired the impression that central banks and fiscal spending will always be able to protect the world economy from the worst scenario possible. Unfortunately, all central banks and governments are not on an even keel. If the Fed has some room to lower rates, the ECB seems to be much more cornered. If the German government have room to support German demand, the same cannot be said about Italy or France. More importantly, even the Fed’s situation today is a far cry from conditions in 2008: it is unlikely that with a balance sheet of this size that Fed can be in a position to surprise markets the way it did in 2008.

The big picture

So why do we disagree with markets? A cornerstone of business cycle analysis relies on a “consistency” analysis. Most of the work initiated by Burns and Mitchel in the 1940s, and pursued later by the real business cycle school in the 1970s, led to one essential conclusion: if every recession comes for various reasons, their impact on the economy is usually very comparable. It shows across (1) many economic sectors, such as consumption, investment or the employment market, across (2) a significant number of countries, as most economies relate to the world business cycle, and (3) it exerts a negative influence on the level of prices, as slower economic activity prevents prices from rising too fast. We believe this textbook analysis framework fits the current situation particularly well.

Our proprietary Nowcasting indicators are pointing to such consistent signs of deceleration. Our Growth Nowcaster recently breached the zero line, indicating that the world should now be growing below its potential. The Eurozone is the region with the most alarming signs. On average, since March 2018, we have seen a consistent 67% of deteriorating data and the most recent reading of the Eurozone PMI breached the psychological level of 50, usually a forward indication that the region is likely to experience dire economic conditions. The US, China and several other countries, such as Canada, Norway and Sweden, are also experiencing slowdowns of various magnitude. These slowdowns have an impact on a majority of the sectors upon which our Nowcasters are based: consumption, employment, production expectations and investment have all been slowing down in a synchronised way since March last year. Only housing markets are still in green territory, with the notable exception of the US, which is unsurprising given the level of interest rates. On the back of this growth deceleration, inflationary pressures are also slowing down. US inflation (ex food and energy) dropped from 2.35% to 2.1%, which cannot be simply explained by the drop in oil prices. In the Eurozone, inflation remains around 1% and there are very limited chances of it hitting 2%, at least from the perspective of our Inflation Nowcasters, whose latest readings indicate that inflation will not be an issue. Across these three elements, we see a line of consistency and ask the question Burns and Mitchel would surely have asked. How can the S&P 500 index be trading above 2,800?

We think the current disconnect stands very little chance of remaining with us in the near future. With the earnings season starting, investors are likely to discover that revenue growth has been lower-than-expected and cards are likely to be reshuffled between bulls and bears. In our opinion, valuations are now even more vulnerable to bad news given the recent rally. Defying gravity rarely ends well.

Defying Gravity

STRATEGY BEHAVIOUR

Our medium-term views remain cautious, so we are complementing a more positive pro-growth stance with options to protect the portfolio in the case of equity drawdowns.

PERFORMANCE REVIEW

Year to date, the Multi Asset Risk Targeted Strategy has returned 4.7% versus 11.5% for the MSCI AC World index, while the Barclays Global Aggregate (USD hedged) index is up 2.8%.

* The Multi Asset Risk Targeted Strategy performance is shown in USD net of fees for the representative account of the Multi Asset Risk Targeted (Medium) USD Composite and reflects the deduction of advisory fees and brokerage commission and the reinvestment of all dividends and earnings. Past performance is not indicative of future performance. This information is presented as supplemental information only and complements the GIPS compliant presentation provided on the following page.

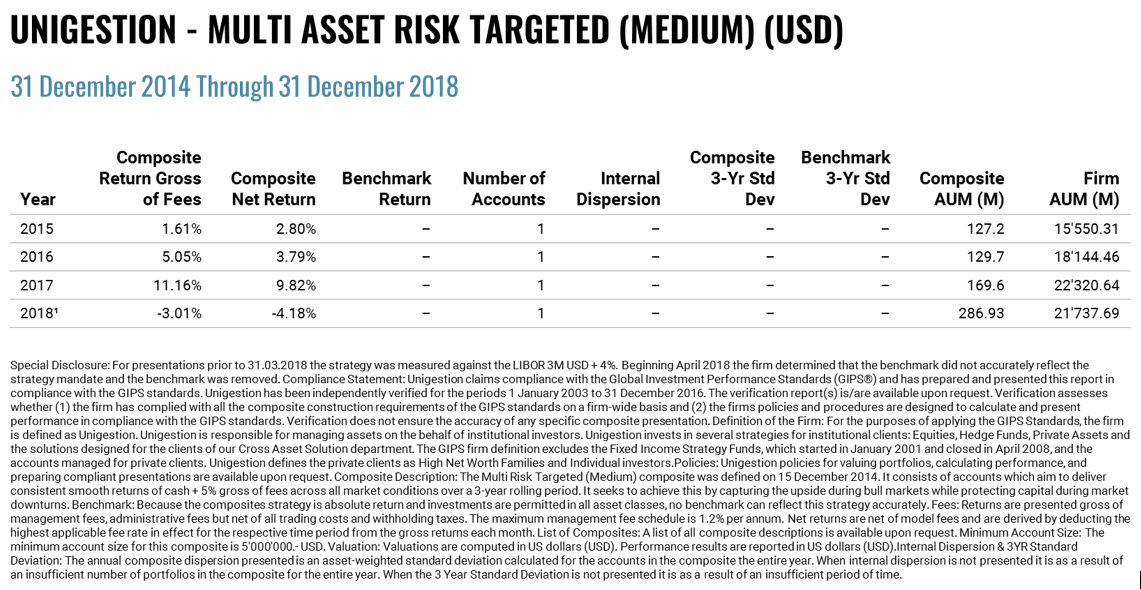

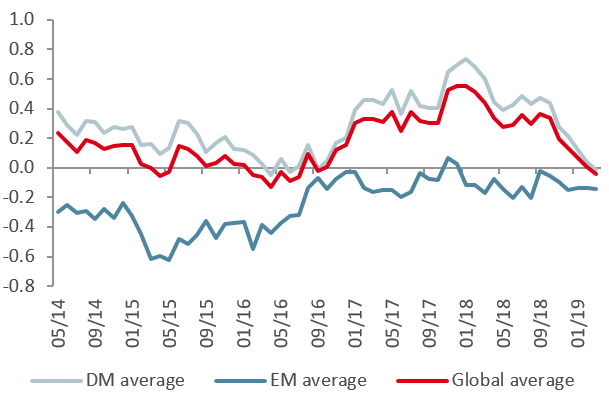

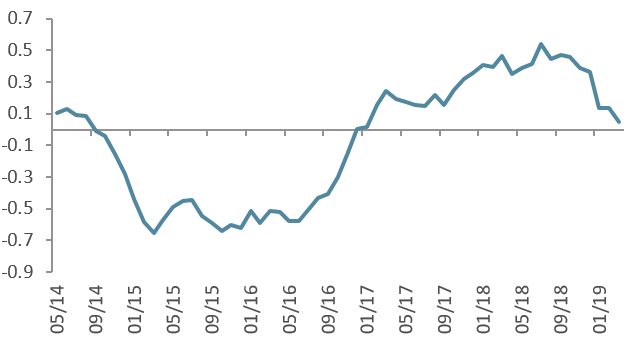

UNIGESTION NOWCASTING

World Growth Nowcaster

World Inflation Nowcaster

Market Stress Nowcaster

Weekly Change

- Our World Growth Nowcaster is now below zero, following a limited decline over the past week.

- Inflationary pressures receded across the board last week.

- Market stress increased at the end of last week, with volatility and spreads reaching higher grounds.

Sources: Bloomberg, Unigestion as at 25 March 2019.

Important Information

Past performance is no guide to the future, the value of investments can fall as well as rise, there is no guarantee that your initial investment will be returned. This document has been prepared for your information only and must not be distributed, published, reproduced or disclosed by recipients to any other person. This is a promotional statement of our investment philosophy and services only in relation to the subject matter of this presentation. It constitutes neither investment advice nor recommendation. This document represents no offer, solicitation or suggestion of suitability to subscribe in the investment vehicles it refers to.

Please contact your professional adviser/consultant before making an investment decision. Where possible we aim to disclose the material risks pertinent to this document, and as such these should be noted on the individual document pages. Please contact Unigestion for a complete list of all the applicable risks. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment.

These are not suitable for all types of investors. To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks. As such, forward looking statements should not be relied upon for future returns. Data and graphical information herein are for information only and may have been derived from third party sources. Unigestion takes reasonable steps to verify, but does not guarantee, the accuracy and completeness of this information. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. All information provided here is subject to change without notice.

It should only be considered current as of the date of publication without regard to the date on which you may access the information. Rates of exchange may cause the value of investments to go up or down. An investment with Unigestion, like all investments, contains risks, including total loss for the investor.

Depending on your country of residence, this document is distributed by Unigestion UK Limited, Unigestion SA, Unigestion Asset Management (France) S.A., Unigestion Asia Pte Limited or Unigestion Asset Management (Canada) Inc. Unigestion UK Limited is authorised and regulated by the UK Financial Conduct Authority (“FCA”). Unigestion UK Limited is also registered as an investment adviser with the U.S. Securities and Exchange Commission (“SEC”). Unigestion SA is authorised and regulated by the Swiss FINMA. Unigestion Asset Management (France) S.A. is authorised and regulated by the French Autorité des Marchés Financiers. Unigestion Asia Pte Limited is authorised and regulated by the Monetary Authority of Singapore. Unigestion Asset Management (Canada) Inc. is authorised and regulated by the Ontario Securities Commission.