While the global recovery is accelerating and broadening across the economic components we track, divergences are building. Foremost among these is the gap between developed and emerging economies: a supportive policy mix, vaccine rollouts and gradual reopenings have helped push the developed world past the emerging one. The difference in growth dynamics has naturally led to differences in inflationary pressures between the two regions, suggesting that policy responses will continue to diverge. This context provides important opportunities and risks, pushing us to favour EM equities at the expense of EM credit.

Separate Ways (Worlds Apart)

What’s Next?

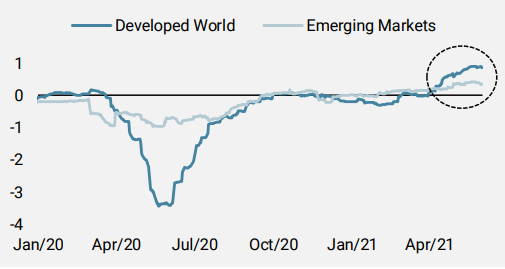

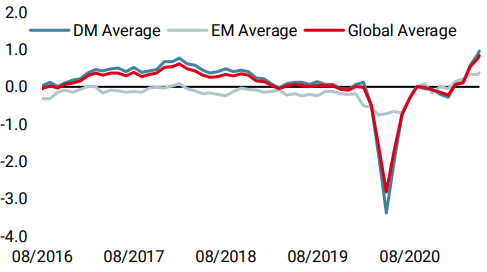

DM and EM growth have been diverging

In our view, consensus estimates, market pricing, and many central bankers are underestimating the strength and sustainability of the recovery, focusing primarily on the direct impacts of economic reopening. However, the knock-on impacts of higher employment and a return of still-lagging consumption will help support the expansion for some time. This is why we believe that, despite our Global Growth Nowcaster hitting historically high levels, it will remain elevated for some time, well beyond this quarter. Consequently, we believe we will see a sustained period of inflationary pressures, not just a transitory regime that can simply be disregarded. In short, the risks are tilted to the upside.

Looking below the surface reveals important details. First, as we discussed last week, the recovery is broad-based across many components and countries. However, it is also clear that the emerging world is growing closer to its potential levels than the developed world. As Figure 1 shows, the coronavirus crisis hit developed countries much harder than those in the emerging world. From the nadir of the crisis, there was a largely synchronised recovery until two months ago when the developed world shifted into much higher levels of activity.

Figure 1: Growth Nowcasters by Region

Source: Unigestion, Bloomberg, as of 02 June 2021

Two worlds, two policy responses

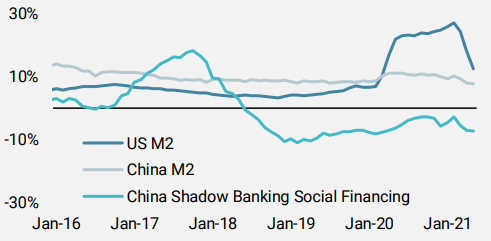

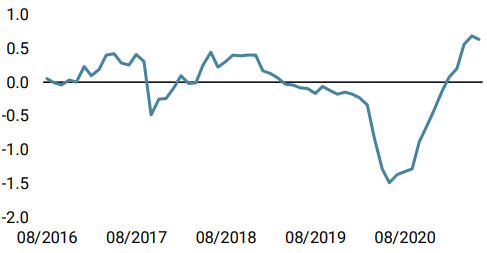

One of the key drivers of this divergence is the disparity in monetary policy: in the developed world, central bankers, led by the Fed and ECB, have opened up the taps and pumped an extraordinary amount of money into the real and financial economy. The PBOC, on the other hand, has focused more on China’s debt problems and provided limited stimulus. As Figure 2 shows, there is a massive difference in the rate of money growth between the US and China. The figure also shows that shadow banking, which has helped support Chinese growth in the past, continues to shrink as policymakers reign in credit creation.

Figure 2: Money Supply Growth (year-over-year percent change)

Source: Unigestion, Bloomberg, as of 02 June 2021

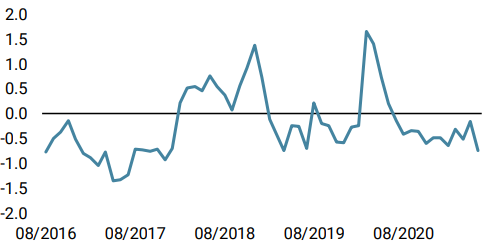

High EM inflation still well below DM inflation

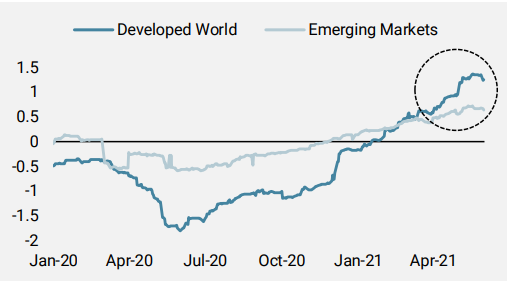

The consequences of these disparate growth stories can be seen in the difference in inflation pressures facing the two regions. While the developed world is seeing all components of inflation above their long-term levels, reflected by our Developed World Inflation Nowcaster hitting historical highs, inflation in the emerging world has yet to climb as high (Figure 3). Looking at the components, the main lagging factor is clearly underlying demand in the emerging world. Importantly, the recovery in commodity prices has meant that food inflation is very high, which will add further downside pressure on demand.

Figure 3: Inflation Nowcaster by Region

Source: Unigestion, Bloomberg, as of 02 June 2021

EM equities more attractive than EM credit

It is worth noting that we are still at the early stages of this divergence, and that economic conditions in the emerging world are quite healthy, if not as healthy as in the developed world. Nevertheless, these ongoing dynamics have important asset allocation consequences. For instance, we believe that EM equities provide an attractive risk/reward opportunity as they had been flat year-to-date up until a couple of weeks ago and stand to benefit from improved global demand and a fall in risk aversion. If the growth gap between the regions is closed by a pickup in emerging world growth, EM equities will be the greatest beneficiary. On the other hand, slowing emerging world growth could be offset by Chinese policymakers, who possess a large set of tools to respond if needed.

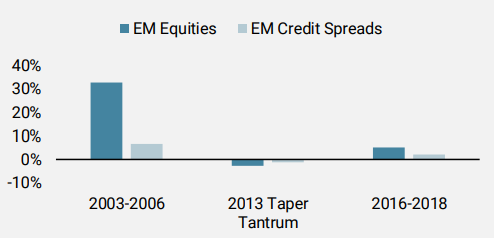

Conversely, EM credit spreads are at risk in our view: with five-year spreads near their three-year lows, there is little room for prices to rise and the carry offered is minor. Indeed, our cross-asset valuation metric ranks EM credit spreads as the most expensive asset in our investment universe. At the same time, with inflationary pressures building in the US and the broader developed world, DM sovereign bond yields will likely rise, adding currency pressures to hard currency EM debt. In Figure 4, we compare the returns on the MSCI EM index to those of a long exposure to five-year EM CDX over the last three periods of rising US 10-year yields. As the chart shows, EM equities tend to perform better in such an environment as they can benefit from the repricing of the growth premium embedded in bond yields.

Figure 4: Annualised Excess Returns During Periods of Rising US 10-Year Yields

Source: Unigestion, Bloomberg, as of 02 June 2021

Unigestion Nowcasting

World Growth Nowcaster

World Inflation Nowcaster

Market Stress Nowcaster

Weekly Change

- Last week, our World Growth Nowcaster ticked up modestly, largely due to improving data from Europe.

- Our World Inflation Nowcaster also rose slightly due to continued broad-base inflationary pressures.

- Our Market Stress Nowcaster decreased markedly due largely to improving liquidity conditions.

Sources: Unigestion. Bloomberg, as of 04 June 2021

Important Information

This document is provided to you on a confidential basis and must not be distributed, published, reproduced or disclosed, in whole or part, to any other person.

The information and data presented in this document may discuss general market activity or industry trends but is not intended to be relied upon as a forecast, research or investment advice. It is not a financial promotion and represents no offer, solicitation or recommendation of any kind, to invest in the strategies or in the investment vehicles it refers to. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment.

The investment views, economic and market opinions or analysis expressed in this document present Unigestion’s judgement as at the date of publication without regard to the date on which you may access the information. There is no guarantee that these views and opinions expressed will be correct nor do they purport to be a complete description of the securities, markets and developments referred to in it. All information provided here is subject to change without notice. To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks.

Data and graphical information herein are for information only and may have been derived from third party sources. Although we believe that the information obtained from public and third party sources to be reliable, we have not independently verified it and we therefore cannot guarantee its accuracy or completeness. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. Unless otherwise stated, source is Unigestion. Past performance is not a guide to future performance. All investments contain risks, including total loss for the investor.

Unigestion SA is authorised and regulated by the Swiss Financial Market Supervisory Authority (FINMA). Unigestion (UK) Ltd. is authorised and regulated by the UK Financial Conduct Authority (FCA) and is registered with the Securities and Exchange Commission (SEC). Unigestion Asset Management (France) S.A. is authorised and regulated by the French “Autorité des Marchés Financiers” (AMF). Unigestion Asset Management (Canada) Inc., with offices in Toronto and Montreal, is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario and Quebec. Its principal regulator is the Ontario Securities Commission (OSC). Unigestion Asset Management (Copenhagen) is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Danish Financial Supervisory Authority” (DFSA). Unigestion Asset Management (Düsseldorf) SA is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Bundesanstalt für Finanzdienstleistungsaufsicht” (BAFIN).