September saw the five-month-long market recovery falter. With no significant upside triggers materialising, investors seem to have taken the opportunity to re-assess their exposures in light of the looming risks on the horizon. Just as important, the typical diversifiers or hedges in multi asset portfolios failed to deliver positive returns commensurate to the fall in growth-oriented assets. While we still believe that the current environment remains favourable for these assets, we also believe that the road ahead will be a bumpy one and care must be taken to find true diversifiers in these extraordinary times.

Sad Sad City

What’s Next?

The rally takes a break…

Global equities retraced some of their recent gains in September, with the MSCI World index finishing the month down -3.5%, although the MSCI Emerging Markets index fared a bit better at -1.6% on the month. The Nasdaq 100 bore the brunt of the sell-off and was down -10.5% on the month before recovering strongly and finishing at -5.7%. European equities were more resilient, with the Euro Stoxx 50 index down -2.5%, the SMI index flat, and the FTSE 100 index up 0.2% (though sterling weakness was a tailwind for the first half of the month given the index’s exposure to foreign revenue).

While equities were the initial focal point, the negative mood permeated other growth-oriented assets later in the month, leading the Barclays US High Yield index to fall -1.1% on the month. Global corporate bonds did a bit better, with the Barclays Global Aggregate Corporate index down -0.3% (USD hedged). Inflation expectations also fell, though modestly so, but cyclical commodities suffered more acutely: the Bloomberg Energy index fell -9.7% while the Industrial Metals index fell -3%. Despite such market moves, safe haven assets underperformed their typical behaviour: the Barclays Global Aggregate Treasuries index returned just 0.5% and the Bloomberg Precious Metals index fell -7.7%. While the VIX index did get up as high as 33.6 early on, it ended the month essentially flat at 26.4, making it difficult to profit from a long volatility position over the month.

…although it does not look at risk for a reversal

At this point, the market action does not seem to point toward a significant change in growth expectations or a major rotation within equities. Analyst expectations for corporate earnings growth have been largely steady, and our own market-implied earnings growth has not deteriorated significantly either. The market moves seem rather to have been driven by a combination of stretched positioning (especially in recent outperformers/US Tech), high valuations, mixed messages from the Fed, and market technicals (market short gamma, unwinding of unprecedented long calls on Tech, and CTAs cutting exposure after the initial market correction). In addition, while the recent outperformers corrected more over the month than recent underperformers, the difference was minimal: the MSCI World Momentum index was down -3.2% while the Quality index fell -2.6%. At the same time the MSCI World Value index returned -3.2%, the equal-weighted counterpart was down -2.4%, and the Minimum Volatility index fell -1.7%. The dispersion is not yet significant enough to suggest investors are fleeing growth/outperforming stocks for value/laggards.

“What we’ve got here is failure to…” diversify

From our perspective, one of the important lessons from the past month is that the typical cross-asset correlations that multi asset managers rely upon will be challenged for the foreseeable future. With governments engaged in significant spending and central banks deploying multiple measures to ensure this spending can be financed cheaply, we cannot expect government bonds to provide a diversifying source of returns to reduce equity risk in a multi asset portfolio. Until the pandemic is well behind us, we expect yields to move within a fairly tight range regardless of what equities may be doing, much as they did during World War II. While we were concerned that a day would come when low yields and anemic growth would push fiscal and monetary policy to coordinate and finance spending, we did not expect it to come as quickly as it did.

The elevated-but-stable level of the VIX will also pose a challenge in the near-term for investors looking to hedge their equity exposure by a long position in VIX futures. With October, November, and December contracts all around 32, investors are expecting daily equity moves of over 2% for the next few months. While such moves are not uncommon, there would need to be a sustained downturn to make the current level of pricing attractive.

In the land of the blind, the one-eyed man is king

In our view, currencies are a critical source of diversifying returns in this current environment of low yields and high volatility. From a strategic perspective, systematically harvesting the value premia embedded in currencies should provide an uncorrelated return stream. Indeed, the Barclays G10 FX Value index was up 1.1% in September and 8.2% on a year-to-date basis. From a tactical perspective, they can provide a useful source of alpha. As we discussed last week, the US dollar is in a particularly interesting spot where short-term factors are positive whereas the longer-term factors are negative. Indeed, it was supported by the market correction in September and rose against nearly all developed world peers (excluding the Japanese yen). However, against emerging market currencies, it could not hold its own: it fell -1.1% against the South African rand, -0.9% against the Chinese yuan, -1.3% against the Taiwanese dollar, and -1.5% against the Korean won. The case for Asian currencies against the US dollar is especially strong. The combination of negative real yields in the US, current account surpluses in some countries, and the direct and indirect impacts of the strong Chinese economic recovery on the rest of the region should support a broad basket of Asian currencies against the greenback.

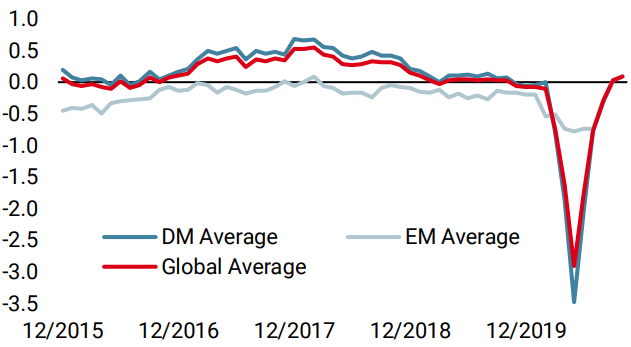

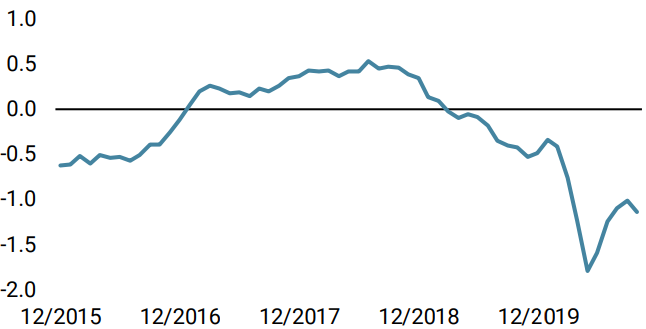

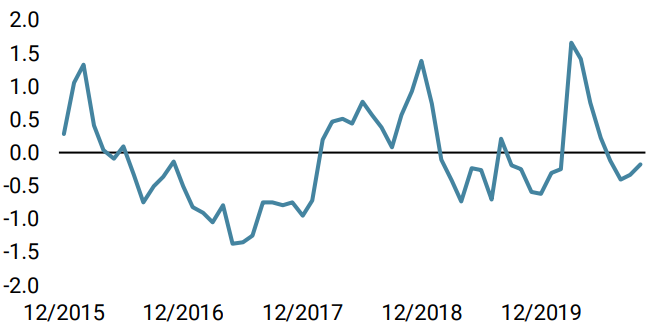

Unigestion Nowcasting

World Growth Nowcaster

World Inflation Nowcaster

Market Stress Nowcaster

Weekly Change

- Our World Growth Nowcaster increased last week: an excellent batch of Japanese data helped, while most countries are now showing strong signs of normalisation. Our World Growth Nowcaster is now in positive territory.

- Our World Inflation Nowcaster declined marginally last week, largely because US data has been down. Overall, inflation surprise risk is very low.

- Last week, our Market Stress Nowcaster remained stable in spite of a volatile period. Liquidity improved while volatility and spreads remained higher.

Sources: Unigestion. Bloomberg, as of 5 October 2020.

Important Information

This document is provided to you on a confidential basis and must not be distributed, published, reproduced or disclosed, in whole or part, to any other person.

The information and data presented in this document may discuss general market activity or industry trends but is not intended to be relied upon as a forecast, research or investment advice. It is not a financial promotion and represents no offer, solicitation or recommendation of any kind, to invest in the strategies or in the investment vehicles it refers to. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment.

The investment views, economic and market opinions or analysis expressed in this document present Unigestion’s judgement as at the date of publication without regard to the date on which you may access the information. There is no guarantee that these views and opinions expressed will be correct nor do they purport to be a complete description of the securities, markets and developments referred to in it. All information provided here is subject to change without notice. To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks.

Data and graphical information herein are for information only and may have been derived from third party sources. Although we believe that the information obtained from public and third party sources to be reliable, we have not independently verified it and we therefore cannot guarantee its accuracy or completeness. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. Unless otherwise stated, source is Unigestion. Past performance is not a guide to future performance. All investments contain risks, including total loss for the investor.

Unigestion SA is authorised and regulated by the Swiss Financial Market Supervisory Authority (FINMA). Unigestion (UK) Ltd. is authorised and regulated by the UK Financial Conduct Authority (FCA) and is registered with the Securities and Exchange Commission (SEC). Unigestion Asset Management (France) S.A. is authorised and regulated by the French “Autorité des Marchés Financiers” (AMF). Unigestion Asset Management (Canada) Inc., with offices in Toronto and Montreal, is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario and Quebec. Its principal regulator is the Ontario Securities Commission (OSC). Unigestion Asia Pte Limited is authorised and regulated by the Monetary Authority of Singapore (MAS). Unigestion Asset Management (Copenhagen) is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Danish Financial Supervisory Authority” (DFSA). Unigestion Asset Management (Düsseldorf) SA is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Bundesanstalt für Finanzdienstleistungsaufsicht” (BAFIN).