After a four-month rally, global equities paused for breath in January. Historically, this is no cause for alarm: January returns on the MSCI World index have been -0.3% on average since 1997. Moreover, valuations are high on risky assets after the strong returns achieved in 2019. However, this week’s song might well have been “Don’t Look Down”. The dispersion across and within assets, countries and sectors observed during the month was unusually large and flashes as a first red flag for our positive outlook for growth-oriented assets. This situation is typically a source of rising volatility across markets. Contradictory signals generally lead to lower conviction, which motivates greater caution in our positioning.Don’t fight the central banks

This Fear Of Emptiness

What’s Next?

No one sang the same song in January

On the surface, everything seemed quiet in early January. Phase one of the trade war deal had been signed, soft Brexit had been voted for and tensions in the Middle East failed to escalate. Even the Coronavirus seemed manageable and unlikely to weigh too much on the global economy in the medium term. The main tail risks that clouded the horizon last year had been removed and we could have reasonably expected positive performance across the board for risky assets. However, beneath the surface, things were more complex and divergent.

First, positive returns were the exception, not the norm. As an illustration, the MSCI US and Switzerland indices were up slightly while the MSCI Europe and Japan indices were down more than 1%. The MSCI Emerging Markets index tumbled by 4.7% following the outbreak of the Coronavirus. Performance disparity was larger across sectors. Utilities and Technology outperformed strongly while Energy and Auto underperformed sharply. That led to a strong performance of Quality, Low Volatility and Momentum styles and a new decline in the Value factor over the month. Second, we saw contradictory messages within growth-oriented assets that usually perform in the same way. In contrast to US equities that posted a slightly positive return, US high yield spreads widened markedly, delivering negative returns. We also saw a sharp fall in cyclical commodities such as oil (-15% over the month) and copper (-10%).

Third, despite the improvement in macro momentum and support from key central banks that met in January and delivered a dovish message, risky assets failed to price in the positive macro narrative. Fourth, and more importantly, safe assets delivered “recession-like” returns and outperformed growth-oriented assets. As an example, US bond yields declined by 40bps, back to August 2019 levels (1.51%) driven by a fall in both main risk premia: growth and inflation. We saw a similar trend for German, Australian, Canadian and British curves but to a lesser extent than for the US curve. Gold was up 4% as well in January while the VIX index jumped by 30% over the month back to 18. Finally, the USD strengthened across the board, gaining more than 4% versus cyclical developed market currencies such as the AUD, CAD, NZD or NOK and emerging currencies like the BRL, ZAR and CLP. Even versus safe currencies like the JPY or CHF, the greenback was up in January.

The momentum of momentum

To summarise the start of the year, despite hopes of a global rotation across and within assets, the momentum of momentum continued unabated: expensive, quality and big names won while cheap, emerging and small ones lagged. Being diversified was costly while being concentrated was rewarded. For example, in January, the best five performers in the S&P 500 index were Google, Apple, Amazon, Visa and Salesforce.com. In a similar way, the MSCI World returned -0.6% in January versus -2% for the MSCI World equal weighted. Did someone say “crowded positioning”?

This trend comes from two main factors: 1) the increasing weight of passive investment that tends to increase the momentum effect as well as stock concentration and the cost of being contrarian; and 2) the rising weight of services in the global economy. Global corporates are much better equipped than small ones to leverage the low yield environment (financial engineering for buybacks) and global digitalisation. We believe that the two trends are structural and should continue to weigh on asset allocation decisions.

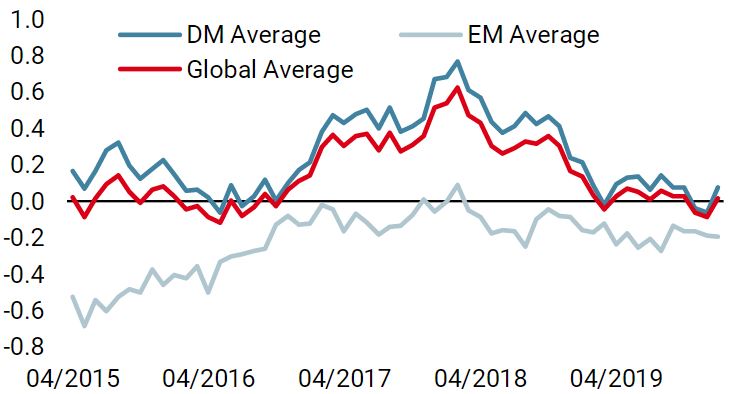

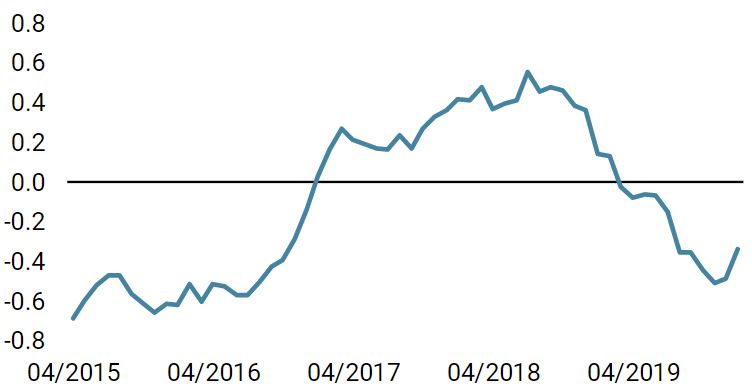

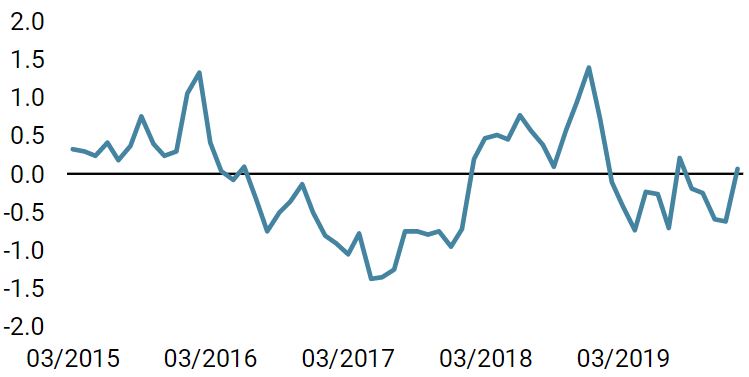

To monitor the song being sung by investors, we have built four simple macro baskets of assets: 1) a growth basket comprising global equity and high yield credit spread, 2) a recession basket driven by global sovereign bonds, 3) an inflation basket that mixes break-even inflation and commodities, and finally 4) the market stress basket that combines VIX futures, Ted spread and AUD/JPY. Unsurprisingly, the best performers in January were the recession and market stress baskets that delivered positive returns while inflation and growth baskets delivered sharply negative returns. These results confirm that the dance has changed in January versus last quarter. After euphoria, market sentiment is shifting toward prudence. This shift is confirmed by our PCA analysis applied to key assets that shows a net decline in the growth premium in January. As valuations tend to be expensive for most assets, a cursory assessment might lead us to revise down expected returns for global equities and de-risk our multi assets portfolios. However, doing this would overlook a key element of long-term asset returns: the global policy mix and, more specifically, the prevailing monetary policy bias. Accommodative monetary policy has two main positive impacts on risky assets. One is straightforward; it supports consumption and investment by easing financial conditions. The second effect is less direct and has been amplified by unconventional monetary policy and negative bond yields: a significant reduction in the negative impact and length of macroeconomic tail risks. This does not mean that the frequency of these events has declined or will decline, it implies that the risk premium associated with any asset will likely be lower when QE is global and sustained. In a sense, we could say that the “search for yield” that has driven asset allocation and led to amazing returns for most risky assets and incredible Sharpe and Calmar ratios over the last decade, has been driven by TINA (There Is No Alternative) as much as DIRP (Decline In Risk Premium ). While TINA could be challenged by higher valuations, DIRP will remain as long as monetary policy stays accommodative – and we think it will. In our view, the macro picture could improve in the coming months thanks to greater visibility in global trade, a recovery in manufacturing and supportive financial conditions. As an illustration, our Growth Nowcaster continues to point to a low risk of recession. Recently, “Housing”, “Durable goods consumption”, “Employment” and “Investment perspective” have all improved. Moreover, as long as inflation risk stays moderate, as measured by our Inflation Nowcaster, central banks should remain accommodative, limiting realised volatility. Despite volatile market sentiment that can quickly change the dance in the short term, central bankers will continue to be the market’s DJ. The longer-term musical horizon will likely remain unchanged and, thanks to the DIRP effect, that would be supportive for global equity and carry strategies. World Growth Nowcaster World Inflation Nowcaster Market Stress Nowcaster Weekly Change Sources: Unigestion. Bloomberg, as of 03 February 2020. Important Information This document is provided to you on a confidential basis and must not be distributed, published, reproduced or disclosed, in whole or part, to any other person. The information and data presented in this document may discuss general market activity or industry trends but is not intended to be relied upon as a forecast, research or investment advice. It is not a financial promotion and represents no offer, solicitation or recommendation of any kind, to invest in the strategies or in the investment vehicles it refers to. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment. The investment views, economic and market opinions or analysis expressed in this document present Unigestion’s judgement as at the date of publication without regard to the date on which you may access the information. There is no guarantee that these views and opinions expressed will be correct nor do they purport to be a complete description of the securities, markets and developments referred to in it. All information provided here is subject to change without notice. To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks. Data and graphical information herein are for information only and may have been derived from third party sources. Although we believe that the information obtained from public and third party sources to be reliable, we have not independently verified it and we therefore cannot guarantee its accuracy or completeness. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. Unless otherwise stated, source is Unigestion. Past performance is not a guide to future performance. All investments contain risks, including total loss for the investor. Unigestion SA is authorised and regulated by the Swiss Financial Market Supervisory Authority (FINMA). Unigestion (UK) Ltd. is authorised and regulated by the UK Financial Conduct Authority (FCA) and is registered with the Securities and Exchange Commission (SEC). Unigestion Asset Management (France) S.A. is authorised and regulated by the French “Autorité des Marchés Financiers” (AMF). Unigestion Asset Management (Canada) Inc., with offices in Toronto and Montreal, is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario and Quebec. Its principal regulator is the Ontario Securities Commission (OSC). Unigestion Asia Pte Limited is authorised and regulated by the Monetary Authority of Singapore (MAS). Unigestion Asset Management (Copenhagen) is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Danish Financial Supervisory Authority” (DFSA). Unigestion Asset Management (Düsseldorf) SA is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Bundesanstalt für Finanzdienstleistungsaufsicht” (BAFIN).The “safe assets” narrative could be wrong

Unigestion Nowcasting