The month of May was marked by the publication of macroeconomic figures that combined surprise and contradiction. Surprise due to a US inflation figure well above expectations and a much weaker US employment figure. Contradictory because the former feeds the risk of a durable inflation shock, while the latter mitigates it significantly. In this context of renewed macroeconomic volatility, how can we navigate between the “Goldilocks” scenario, combining controlled inflation and stable growth, and what we call the “Regime Shift” scenario, characterised by strong economic expansion and potentially sustainable inflationary pressures? We believe that the consensus view underestimates the quality and sustainability of global growth and investors could be surprised by the second phase of economic reflation, which we foresee as “Harder, Better, Faster, Stronger”.

Harder, Better, Faster, Stronger

What’s Next?

Growth and inflation: stronger for longer

Regarding the global economic cycle, the consensus outlook is very clear: the growth peak should be reached in Q2 2021. The consensus then anticipates a gradual return to potential growth, which would be reached during the course of next year. In this context, the rise in inflation observed since the beginning of the year, which is the result of a combination of rising commodity prices and a lack of significant investment in many sectors, constraining supply and limiting the efficiency of the supply chain, would be temporary. This expectation for a sequence of bell-shaped quarterly growth, with a peak this year and a return to positive but decelerating growth thereafter, is also that of the major central banks.

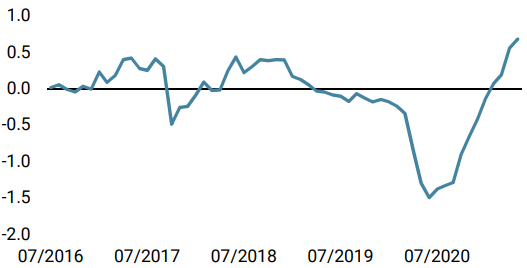

However, our proprietary Nowcaster and Newscaster indicators, which track the business cycle and inflation risk in real time via the aggregation of several hundred macroeconomic, financial and media data series, indicate a different perspective. Their analysis highlights the exceptional nature of the current situation via two key findings: 1) its level: at its highest since 1985, and 2) the very balanced distribution of contributors, both in terms of sectoral components and geographical areas (figure 1).

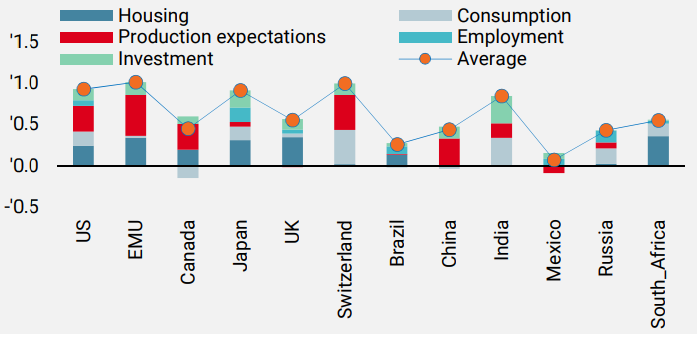

Figure 1: Growth Nowcasters (Breakdown by Components)

Source: Unigestion, Bloomberg, as of 25 May 2021

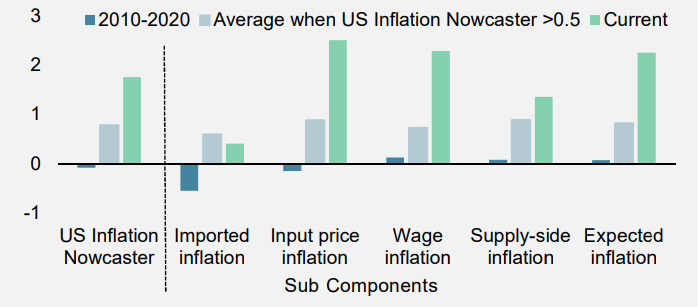

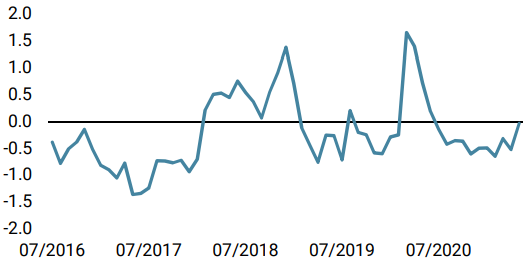

This last element underlines the global and sustainable nature of the world cycle. This situation is similar for our inflation tracking. Our Inflation Nowcaster is also up sharply, to a level not seen since 1985, and has the same characteristics in terms of homogeneity of contributors (figure 2).

Figure 2: US Inflation Nowcaster (Breakdown by Components)

Source: Unigestion, Bloomberg, as of 25 May 2021

Our historical analysis shows that this level of growth typically lasts longer than what current pricing indicates. We have studied the dynamics of Nowcasters, i.e. the average growth rate after reaching a high level, and its stability in terms of how long growth remains at this high rate. Our results for the US economy show that whenever the diffusion index (an index measuring the number of rising versus falling data series) was above 60%, reflecting accelerating growth, the Nowcaster continued to grow at an average level of 0.3 over the following six months (zero represents growth potential). Regarding the duration of the expansion regime, each time the Nowcaster has been above 0.5, i.e. growing well above its potential, it has stayed above that level on average for 10 months. This has happened four times since 1985: 1993-95, 1997-98, 2003-2005 and 2017-2018. On average, the S&P 500 index rose 4% over the six months following the Nowcaster reaching 0.5 while US 10-year yields remained stable on average over the same period.

Consumption and employment: better and faster

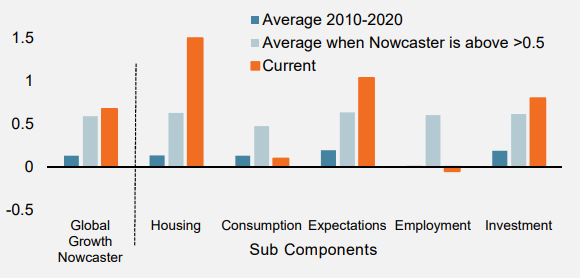

In our view, we have only seen one part of the economic rebound. This is the engine coming from the rebound in industrial and manufacturing activity enabled by the recovery in global trade. Because of the distancing measures, the “consumption” component, particularly that of services, has not yet regained its pre-crisis momentum or its contribution to growth. However, consumption of services is a major creator of jobs. In the coming months, we believe that demand for services will benefit from 1) reopening/vaccination, which will allow people to move freely, and 2) the exceptional level of savings, which will support a strong increase in consumption by households as well as by companies via investment. Our analysis of the components of the Growth Nowcaster (figure 3) perfectly highlights the scale of the potential from the demand side to support global growth in the coming quarters while “Employment” and “Consumption” remain below their average levels observed during the previous expansions.

Figure 3: Global Growth Nowcaster (Breakdown by Component)

Source: Unigestion, Bloomberg, as of 25 May 2021

Yield normalisation: harder

This expected boost from consumption will likely have two important impacts: a significant drop in unemployment rates and a longer period of inflation at high levels. Indeed, regarding inflation dynamics, we believe that the “supply shortage” effect, which drove output prices or the “prices paid” components of the surveys to record levels in the first quarter of 2021, will be joined by the “higher demand” effect. These two factors should challenge the very accommodative bias of monetary policy at the end of the summer, i.e. earlier than current pricing would suggest, anticipating a change in monetary policy at the beginning of next year at the earliest. Indeed, central bank guidelines or forecasts could be reached earlier than expected in terms of unemployment rate and inflation dynamics. It is interesting to note that during the four phases of strong growth mentioned above, the Fed normalised its monetary policy each time.

The second phase of rotation

What should we conclude in terms of asset allocation? The first quarter was marked by rotation between and within asset classes, with real assets outperforming so-called nominal assets. We expect this discrimination to continue as we forecast strong growth and persistently high inflation for the next six months. However, the discriminating factor could change. While interest rate sensitivity has been the determining factor in distinguishing the winners and losers of reflation in the first months of the year, the difference between “price maker” and “price taker “companies could become the new factor to monitor in this second phase of rotation. This period could also be a period of adjustment of expectations regarding growth and inflation prospects. This “repricing” could be a source of market stress and correlation shocks, as most transition phases from one growth regime to another have shown in the past.

In this context, we continue to favour assets that combine high cycle sensitivity and moderate valuation. Within equity indices, European, Japanese and emerging equities are favoured, as well as cyclical commodities and inflation breakevens, which historically provide a good hedge against persistently high inflation. Conversely, we maintain a negative view on sovereign bonds and defensive currencies such as CHF, EUR and SEK.

Unigestion Nowcasting

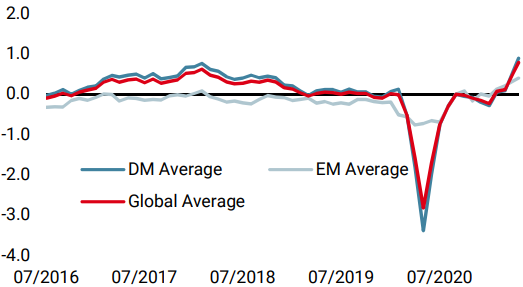

World Growth Nowcaster

World Inflation Nowcaster

Market Stress Nowcaster

Weekly Change

- Last week, our World Growth Nowcaster was steady at high levels with positive data from the UK offset by some modest deterioration in US investment perspectives.

- Our World Inflation Nowcaster also remained steady at its high level over the week with mixed data across countries.

- Our Market Stress Nowcaster decreased as volatility fell over the week.

Sources: Unigestion. Bloomberg, as of 28 May 2021

Important Information

This document is provided to you on a confidential basis and must not be distributed, published, reproduced or disclosed, in whole or part, to any other person.

The information and data presented in this document may discuss general market activity or industry trends but is not intended to be relied upon as a forecast, research or investment advice. It is not a financial promotion and represents no offer, solicitation or recommendation of any kind, to invest in the strategies or in the investment vehicles it refers to. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment.

The investment views, economic and market opinions or analysis expressed in this document present Unigestion’s judgement as at the date of publication without regard to the date on which you may access the information. There is no guarantee that these views and opinions expressed will be correct nor do they purport to be a complete description of the securities, markets and developments referred to in it. All information provided here is subject to change without notice. To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks.

Data and graphical information herein are for information only and may have been derived from third party sources. Although we believe that the information obtained from public and third party sources to be reliable, we have not independently verified it and we therefore cannot guarantee its accuracy or completeness. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. Unless otherwise stated, source is Unigestion. Past performance is not a guide to future performance. All investments contain risks, including total loss for the investor.

Unigestion SA is authorised and regulated by the Swiss Financial Market Supervisory Authority (FINMA). Unigestion (UK) Ltd. is authorised and regulated by the UK Financial Conduct Authority (FCA) and is registered with the Securities and Exchange Commission (SEC). Unigestion Asset Management (France) S.A. is authorised and regulated by the French “Autorité des Marchés Financiers” (AMF). Unigestion Asset Management (Canada) Inc., with offices in Toronto and Montreal, is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario and Quebec. Its principal regulator is the Ontario Securities Commission (OSC). Unigestion Asset Management (Copenhagen) is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Danish Financial Supervisory Authority” (DFSA). Unigestion Asset Management (Düsseldorf) SA is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Bundesanstalt für Finanzdienstleistungsaufsicht” (BAFIN).