Enter the vortex – How asset managers can transcend digital disruption

Enter the vortex – How asset managers can transcend digital disruption

Innovation in financial technology has unleashed a digital vortex that promises to transform the asset management value chain, from asset gathering through to investment and operations. We believe this digital vortex offers numerous potential opportunities for asset managers, but it also carries risks. If financial assets are managed by machines which interpret signals in the same way and recommend the same passive investments, how can we avoid crowded trades and the risk of a market stampede? This is where talented humans with forward-looking views will differentiate themselves.

We believe financial technology is best seen as a tool to empower asset managers and benefit clients. Just as athletes use game tapes and data analytics to fine-tune their performance, we envisage a future where new technology allows market participants to undertake accurate and structured analysis to deliver a better outcome to clients. Nevertheless, we are convinced that technology cannot be deterministic. Humans will still be the ones to give it purpose and take the key decisions.

In this short paper we share our thoughts on the direction the industry should take to transcend disruption, and give some examples of how Unigestion is using digital innovation to evolve the way we invest, to the benefit of our clients.

By Fiona Frick, Unigestion CEO

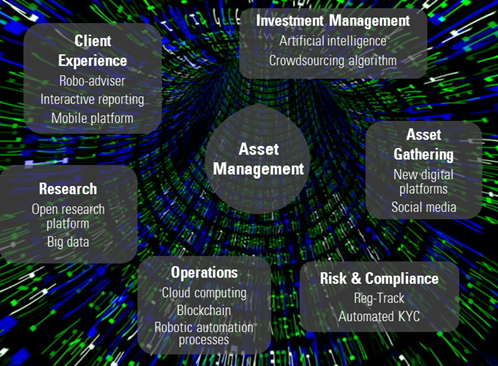

The digital vortex: six areas where asset management is being transformed

Example 1: Artificial intelligence and investment management

The pace of technological evolution is picking up. Last year, one of the world’s best Go players was beaten by AlphaGo, a narrow artificial intelligence computer programme developed by Google’s DeepMind. In March a further breakthrough was made when a programme trounced four professional poker players over the course of a 20-day tournament. Are asset managers next on the list to be beaten? We do not believe so. Artificial intelligence has a key role to play in improving process efficiency and the quality of decision making, but investors should be aware of some current pitfalls.

One issue that limits artificial intelligence at this stage of its evolution is the lack of transparency. It’s perfectly possible to programme a computer to find patterns in financial markets and assess which data most accurately predicts future market movements. The problem is that the investment process remains a “black box”, with clarity around the end decision but little around the reasoning that went into the decision.

Asset managers also need to be sure to check any patterns which have been identified and be careful not to deduce causality from correlation. As an example, the production of butter in Bangladesh was strongly correlated with the S&P 500 Index between 1981 and 1993. A computer could identify and act on this signal, but with no fundamental reason behind this correlation, it could unwind at any time. For this reason, we believe investment managers must give meaning to machine learning algorithms.

Another issue is the complexity of financial markets, where decisions can be interdependent and security movements are strongly influenced by players’ emotions. Unlike physics, biology or medicine, analysing financial markets is not an exact science but influenced by human behaviour, and this limits the value of pattern recognition. As John Maynard Keynes is quoted as saying, “Markets can remain irrational longer than you can remain solvent.” Artificial intelligence struggles to deal with the ambiguity or the evolving patterns resulting from behavioural bias.

How Unigestion intends to use these new technologies

We intend to take advantage of the processing power offered by artificial intelligence to provide portfolio managers with the tools to complement and support their decision making. The challenge for portfolio managers will be to increase their skills in this area to harness the latest technologies and take full advantage of them.

As a tool, artificial intelligence needs a large dataset to be predictive. It works well at recognising cats and dogs by drawing on near-unlimited amounts of data with fixed characteristics from social media, but financial market pattern recognition is more challenging because the data are more limited in volume and constantly evolving.

For this reason, most asset managers use artificial intelligence to extract short-term alpha signals from liquid and easily tradeable instruments such as currencies, commodities and market indices, where speed of processing and the ability to find patterns not easily detectable by traditional analysis can lend an advantage. It dominates the world of high-frequency trading, with algorithms written to look for patterns in volatility, newsflow or volume and then implement positions.

At Unigestion, we have chosen a different route. We use artificial intelligence to enhance the risk management part of our investment processes. We believe that risk management is an enduring driver of long-term investment performance, and apply artificial intelligence to strengthen and deepen our ability to identify and manage risks in investment strategies.

We consider artificial intelligence to be the next generation of quantitative management. We can imagine a world where investment managers will not be teaching a computer how to do things but will instead be showing it where the problem lies, watch it come up with a solution and then assess the results.

We have already diversified away from traditional quantitative models where investment managers ask models to find predefined factors. We have been using predictive algorithms such as Principal Component Analysis (PCA) since the beginning of our research into the minimum variance anomaly in 1995 to understand the evolving aspects of risk. We will continue to implement machine-learning techniques into the engineering of our investment processes, and are currently studying whether new sophisticated algorithms such as “auto deep encoding” could, in turn, replace PCA.

Yet, we are firm believers that the more we use artificial intelligence, the more important it is to have a strong investment philosophy to avoid the risk of “overfitting” data to an elusive and weak signal.

Example 2: Robo-advisers and client experience

The emergence of robo-advisers, providing automated investing services, brings a fresh approach to financial advice. After answering some simple questions, the customer is shown a range of potential investment outcomes and guided to an investment strategy without necessarily speaking to a financial adviser.

One could argue that a robo-adviser is nothing new and nothing more than algorithmic asset allocation applied to passive investment. Modern portfolio theory and exchange-traded funds were both developed in the last century.

We believe this assessment misses the point, which is the enhanced client experience this new technology enables. As with Uber and Airbnb, the innovation is around convenience and ease of use for users. These providers have managed to keep the complexities of their investment processes in-house, and provide simple outcome-oriented solutions to their users.

More than this, robo-advisers act to level the playing field for certain investment services which were previously available only to a select audience of institutional or very wealthy investors. These applications allow investors with capital in the thousands rather than the millions of dollars to access asset allocation and portfolio construction services.

As with artificial intelligence and investment management, we believe the ideal combination is to harness man and machine together. Even the pioneers who promised to rely on computers alone to manage money in this field now offer customers access to human financial advisers. Having an experienced investor able to give meaning to the results from the algorithm and make sure the suggested portfolio lines up with the current state of the market will result in a better outcome for the client, in our opinion. That’s particularly the case when the investment manager is able to support the client through periods of market volatility and act as an emotional circuit-breaker to potentially irrational behaviour.

What we have learned about the client experience at Unigestion

The asset managers who are moving into the robo-adviser area tend to be retail-oriented managers with strong client networks. As a “business to business” asset manager, Unigestion is not going to follow suit at this stage. However, we believe the ease of use of these services has lessons for all asset managers which apply across institutional as much as retail – definitions that are increasingly blurred as individuals take responsibility for their own pension plans.

Asset managers have historically invested in “back-end” technology aimed at delivering a better investment management to their clients. Now they need to be matched with technological investment in simple and personalised front-end tools that can provide a pleasant interactive experience that meets the needs of existing and prospective clients.

In a world where growth is fragile and interest rates are likely to remain low, risk management has taken centre stage in the effort to build a portfolio that can generate sustainable returns. This is why we have decided to build a premium portal providing clients access to our research and investment tools around asset allocation and risk management. This portal is like a cockpit where our clients will be able to see the output provided by the same quantitative tools we use when building portfolios, such as asset allocation models, macro-economic forecasters or risk factor analysis tools.

At Unigestion, we believe innovation and technology must serve a purpose. This portal is intended to generate discussion around the interests and requirements of our clients so that we can co-create with them the solutions that meet their needs.

Example 3: Big data and the new gold rush for investment research

Big data offers a promising way to transform investment research into new sources of return for our clients. If alpha is generated by skilfully exploiting information, the enormous rise in the volume of data available presents both opportunities and challenges for asset managers.

Some 90% of available data has been created in the past three years, coming from myriad sources such as weather sensors, social networks, satellite images, online transactions and GPS signals. With the “internet of things” forecast to grow from 8.4 to some 20.4 billion devices by 2020, the number of data points will grow exponentially.

This, in turn, allows the development of far more advanced indicators than in the past. Satellite images allow for a better understanding of a region’s property market, for example, while posts on social networks provide insight into investors’ appetite for risk and can be early indicators of market stress.

Equally, however, expertise is needed to sort through the data. The emergence of new and complex datasets has led to a new role in asset management companies with data scientists hired to filter out noise and “fake news”.

Furthermore, some new “fintech” companies have emerged with specific expertise in this area. Rezatec and Orbital Insight are specialists in the analysis of satellite data. AlphaSense uses linguistic algorithms to search for information across millions of documents while Quandl assesses the financial health of companies by analysing financial transactions. Most of these companies offer some processing capabilities on top of the raw data, to get closer to an investment signal.

Harnessing the power of new data at Unigestion

Asset managers must consider how to integrate this new data and the signals it provides into their investment processes. There is general agreement that there is limited value in using these new data-driven signals as a standalone investment strategy because of the high risk of being arbitraged away. Most asset managers use these signals as a complement to their in-house alpha engines.

Unigestion is evaluating what part of our investment process can profit from new data sources. We have partnered with a financial technology company called RavenPack, which filters news and other meaningful datasets and applies a weighted score. Our analysts combine the output from RavenPack with other investment models to anticipate changes in trading volumes and potential price anomalies in some securities.

Example 4: Blockchain and the promise of more efficient operational processes

Although technology has made huge progress, the operational aspects of managing assets remain cumbersome. Market participants follow heavily sequential processes that add cost and delay to the delivery of information to the end investor.

A recent study by McKinsey on the power of machine automation showed that although the world of finance relies on highly professional expertise, about 50% of finance workers’ time is spent collecting and processing data. It is a pity that so much talent is wasted doing tasks that could be automated.

The financial industry is heavily intermediated and siloed, with different entities being responsible for different parts of the value chain of asset management and its related services. Communication and exchange of information between asset managers, traders, custodians, administrators and regulators remains sub-optimal, with tasks strictly sequential rather than able to be processed in parallel.

Blockchain has the potential to transform the financial services industry by improving transparency, efficiency and security around the processes that link the different actors in the ecosystem. Blockchain represents the electronic ledger originally built to underpin new cryptocurrencies such as Bitcoin. Although the future of cryptocurrency is still being debated, the technology behind it is powerful as it permits distributed registration instead of relying on a central authority.

Unigestion’s first venture in blockchain

We recently had our first experience of this new technology when we introduced a blockchain platform for our private equity funds through cloud technology. While private equity is in demand from investors searching for return, the infrastructure has seen little innovation in recent years. We worked with our custodians to create an innovative ecosystem providing real-time insight to all parties. It also enables the transfer of fund ownership in a much more streamlined process.

Blockchain has a wide range of potential applications in asset management, but is still in its infancy in terms of practical implementation. It should enable asset managers to rethink post-trade, reporting and middle-office processes. With blockchain, for example, trade settlement will be able to be processed in a few minutes. On the client side, all the anti-money laundering and know-your-client requirements should be simplified and investors should be able to access their positions with a few clicks.

Our objective in the coming years will be to expand our first experience with blockchain to other aspects of our operations. For us, this new technology should help us meet three objectives. The first is to streamline our processes to make our operations more cost-efficient for our clients, our investment partners and for us. The second objective is to create a more secure environment to exchange information between stakeholders. Our third and final objective is to free up time for our professionals and permit them to work on new, value-added tasks, rather than the manual inputting and exchange of data.

Reworking investment managers’ relationship with machines

New technology can be seen as a replacement for human thought and action, or as a tool to empower humans. In a choice between switching human decision making to artificial intelligence or augmenting human intelligence through computer power, Unigestion has chosen the latter.

Even so, the way we collaborate with machines will change. A McKinsey study from 2016 showed that while technology will rarely eliminate jobs entirely over the next decade, it will affect all jobs to some degree. Machines will not replace workers so much as unbundle jobs into tasks that can be performed by an algorithm and those only humans can do.

Machines should therefore be used to free people from repetitive, low-value tasks, so that they can focus on work that requires creativity and consciousness. Computers excel in clearly-defined activities or when they have to respond to well-formulated questions with clear objectives. Human beings remain key in formulating the right questions, defining the end goal and in interpreting the results.

Artificial intelligence will get better year after year, while the human brain will not evolve at the same pace. Investment managers will therefore need to evolve their know-how, remain agile and develop their creativity. With the democratisation of education around the development of massive open online courses, investment professionals will constantly need to educate themselves and reinvent their skills to keep up with machine evolution.

Finally, new technology is creating a new collaborative ecosystem. It makes it possible to exchange know-how and collaborate with a wide group, beyond our company, our country or our client network. Open research exchange platforms permit investment specialists to share research between themselves, exchange ideas with the academic world and devise co-created investment solutions.

It may be that machines will do the work that makes life possible and that human beings will do all the other things that make life pleasant and worthwhile

Technology will change the way we do things but it will not alter the essence of finance, which is to provide consistent investment returns to our clients. Finance is an adaptive industry and has historically always adjusted to change. Technology cannot be deterministic; humans must give it meaning. As Isaac Asimov said, “It may be that machines will do the work that makes life possible and that human beings will do all the other things that make life pleasant and worthwhile”.

Important Information

The information and data presented in this page may discuss general market activity or industry trends but is not intended to be relied upon as a forecast, research or investment advice. It is not a financial promotion and represents no offer, solicitation or recommendation of any kind, to invest in the strategies or in the investment vehicles it refers to. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment.

The investment views, economic and market opinions or analysis expressed in this page present Unigestion’s judgement as at the date of publication without regard to the date on which you may access the information. There is no guarantee that these views and opinions expressed will be correct nor do they purport to be a complete description of the securities, markets and developments referred to in it. All information provided here is subject to change without notice. To the extent that this page contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks.

Data and graphical information herein are for information only and may have been derived from third party sources. Although we believe that the information obtained from public and third party sources to be reliable, we have not independently verified it and we therefore cannot guarantee its accuracy or completeness. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. Unless otherwise stated, source is Unigestion.

Past performance is not a guide to future performance. All investments contain risks, including total loss for the investor.