Distinguishing noise from fundamentals is critical for any investor, and today’s world of hyper-information makes this even more difficult. Sentiment, fuelled by headlines and tweets in real-time, can dominate the underlying macro fundamentals. While we do not intend to understate the impact of the COVID-19 virus on the global economy and on the lives of those affected, we do believe at this stage the virus will be short lived rather than a fundamental shift when looking beyond the next few weeks. In light of this, we see a sovereign bond market that has rallied on virus fears but now faces headwinds on the horizon.Fear premium leaves bond rally vulnerable

Time to Get Ill, The Beastie Boys, 1986

Time to Get Ill

What’s Next?

Virus concerns receding but not gone

Following news headlines alone to track the COVID-19 virus can easily whipsaw investors, as dramatic reports encourage more readers and revenue. Instead, we are tracking the spread of the virus using data from the Center for Systems Science and Engineering at Johns Hopkins University, paying particular attention to the daily growth rate of confirmed cases. While the data can be subject to revisions, it shows a clear slowing in the spread of the virus in China: the last seven days have seen confirmed cases grow by under 2%. The uptick in confirmed cases on February 13 (34% day-over-day) was just over two weeks after the previous significant increase in confirmed cases on January 27 (63% day-over-day), in line with the virus’s incubation period. It would not be surprising if there is another significant increase in about a week, and we will be watching closely to see if it is below the February 13 rate.

Outside China, the number of confirmed cases is growing, leading to a resumption of risk-off sentiment. But it is important to keep in mind that these numbers remain low at present, more is now known about the virus than when it first broke out in China, and the most concerning countries (Japan, South Korea, and Singapore) have well-developed healthcare systems. Nonetheless, we are following the spread of the virus outside China closely, especially in countries with a high population density and less developed healthcare systems.

As we communicated last week, measuring the impact of the virus on economic growth is difficult at this stage. The lack of alarming headlines about supply chain disruptions as Chinese factories partially reopen is certainly a positive, but the fall in US PMIs last Friday is concerning. Our own proprietary Growth Nowcaster does not yet show much of an impact from the virus on Chinese or global growth but should do so if the virus persists and begins to meaningfully drag on growth. However, the PBOC has, and will, continue to provide easy monetary policy to counter the demand contraction emanating from China. More broadly, global monetary policy is tilted towards easing, which will help support growth if the virus persists and transforms into a recession risk.

Equity and bond investors agree to disagree

Stock and bond investors seem to have very different assessments of the impact of the virus: despite a pickup in realised volatility, equity markets (especially in the developed world) have reached new highs over the last couple of weeks. The VIX index rose above 17 at the end of last week, but is well below the levels seen in August 2019 in the midst of the US-China trade war (24.6) or at the end of December 2018 when recession fears gripped markets (36). Implied earnings growth rates for equities remain solidly positive, even for the MSCI Emerging Markets index (about 5% over the next year). The view from the equity market seems clear: COVID-19 is a risk but should not derail the supportive context for corporate earnings and stock prices.

Over the period, bond yields have fallen, with the US 10-year yield down to 1.47% and the 30-year yield down to a historical low of 1.91%. The driver of the move has been real yields: the 10-year yield is down 40bps from before news broke about the virus, 25bps of which come from real yields that are now negative. The 5-year yield is down 34bps, with the corresponding 5-year real yield falling by 28bps to -0.3%. At the short end of the US interest rate curve, two cuts are now priced in for 2020. While the yield curve remains about 12bps from inverting (based on 10 vs 2-year yields), bond investors are giving a clear signal that the virus will have a meaningful, non-transient negative impact on growth.

From our perspective, bonds seem more at risk than equities at this point. The focus on the virus has turned attention away from the relatively positive growth data we have been seeing over the last few weeks. Assessing the economic impact of the virus has also focused largely on the demand shock and less on potential inflation pressures from low inventories and reduced capacity (though the drop in oil prices is a large offsetting factor for inflation). And while portfolio rebalancing post the 2019 rally in equities has been supportive for bond inflows this year, yields have moved tightly with virus headlines. Thus, we see the bond rally as driven more by fear than a change in underlying fundamentals and it is therefore prone to a sharp reversal if these fears dissipate.Bonds exposed to reversal of fear premium

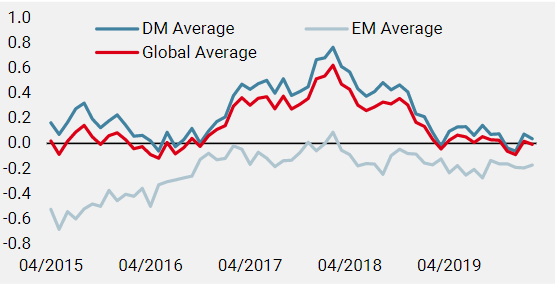

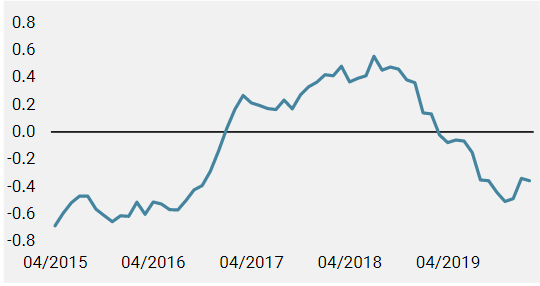

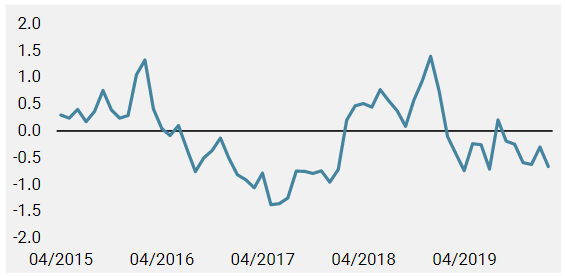

Unigestion Nowcasting

World Growth Nowcaster

World Inflation Nowcaster

Market Stress Nowcaster

Weekly Change

- Our world Growth Nowcaster increased over the course of the week, driven by an overall improvement in developed market countries.

- Our world Inflation Nowcaster remained steady, still pointing to neutral inflation risk.

- Our Market Stress Nowcaster increased marginally. Liquidity however gives clear signs of improvement.

Sources: Unigestion. Bloomberg, as of 24 February 2020.

Important Information

This document is provided to you on a confidential basis and must not be distributed, published, reproduced or disclosed, in whole or part, to any other person.

The information and data presented in this document may discuss general market activity or industry trends but is not intended to be relied upon as a forecast, research or investment advice. It is not a financial promotion and represents no offer, solicitation or recommendation of any kind, to invest in the strategies or in the investment vehicles it refers to. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment.

The investment views, economic and market opinions or analysis expressed in this document present Unigestion’s judgement as at the date of publication without regard to the date on which you may access the information. There is no guarantee that these views and opinions expressed will be correct nor do they purport to be a complete description of the securities, markets and developments referred to in it. All information provided here is subject to change without notice. To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks.

Data and graphical information herein are for information only and may have been derived from third party sources. Although we believe that the information obtained from public and third party sources to be reliable, we have not independently verified it and we therefore cannot guarantee its accuracy or completeness. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. Unless otherwise stated, source is Unigestion. Past performance is not a guide to future performance. All investments contain risks, including total loss for the investor.

Unigestion SA is authorised and regulated by the Swiss Financial Market Supervisory Authority (FINMA). Unigestion (UK) Ltd. is authorised and regulated by the UK Financial Conduct Authority (FCA) and is registered with the Securities and Exchange Commission (SEC). Unigestion Asset Management (France) S.A. is authorised and regulated by the French “Autorité des Marchés Financiers” (AMF). Unigestion Asset Management (Canada) Inc., with offices in Toronto and Montreal, is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario and Quebec. Its principal regulator is the Ontario Securities Commission (OSC). Unigestion Asia Pte Limited is authorised and regulated by the Monetary Authority of Singapore (MAS). Unigestion Asset Management (Copenhagen) is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Danish Financial Supervisory Authority” (DFSA). Unigestion Asset Management (Düsseldorf) SA is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Bundesanstalt für Finanzdienstleistungsaufsicht” (BAFIN).