Five-Year Anniversary,

Five Reasons To Focus On Multi Asset Risk Targeted

A five-year anniversary presents an ideal opportunity to take a step back and perform a thorough and objective analysis of the Multi Asset Risk Targeted strategy (the Strategy) to understand how performance was achieved and how it compares to the competition.

The past five years have been eventful, characterised by supportive financial conditions, heavy market stresses, recessionary fears, shifting central bank policy, geopolitical turmoil and swinging valuations. This ever-changing environment is the reality of managing portfolios, requiring adaptability, strong processes and diversified return streams. This is exactly what the Strategy is made of, which is why we are confident that its behaviour will be repeatable in the future, no matter what awaits investors in the years to come.

2020 will be a challenging year for flexible asset allocation and investors will need to contend with an upcoming US election, an anticipated global slowdown and high valuations. Now is a crucial time to highlight the benefits of a macro risk-based solution that aims to deliver smooth returns in different market conditions.

There are five points to take away from this paper:

- The Strategy delivered attractive risk-adjusted performance over the past five years

- It achieved positive asymmetry in different market conditions

- Its enhanced diversification and dynamic allocation worked as expected

- The process delivered on its promise of reducing risk while enhancing returns

- The Strategy has everything it takes to navigate the challenges and opportunities ahead in 2020

A Quick Look at 2019 Performance

2019 was an exceptional year for multi asset strategies, thanks mainly to the “beta party” triggered by central bank easing. In contrast to 2018, when returns on all risk premia disappointed, last year saw a broad-based reversal with most asset classes and cross-asset strategies posting strong returns. If last year had a song, it would be called “Thanks for the Dance, Central Bankers!” and the chorus would be: “The higher the beta to equity, the better the yearly performance”.

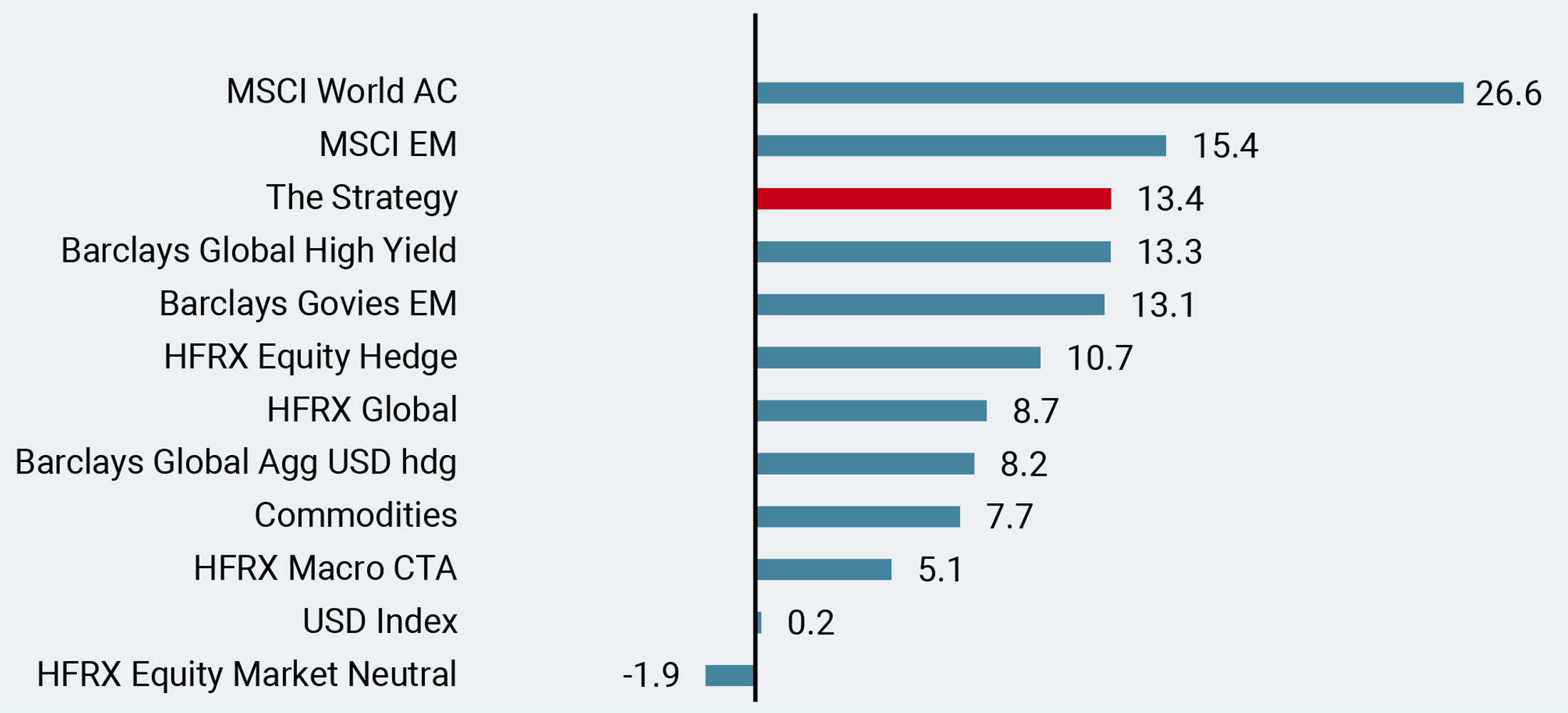

In that context, the Strategy delivered double-digit returns, outperforming hedging risk premia such as duration, and beating most of the key hedge fund indices (HFRX). (Figure 1)

Figure 1: 2019 Performance vs. Key Assets and Hedge Funds Indices

1) Attractive Risk-adjusted Performance over the Last Five Years

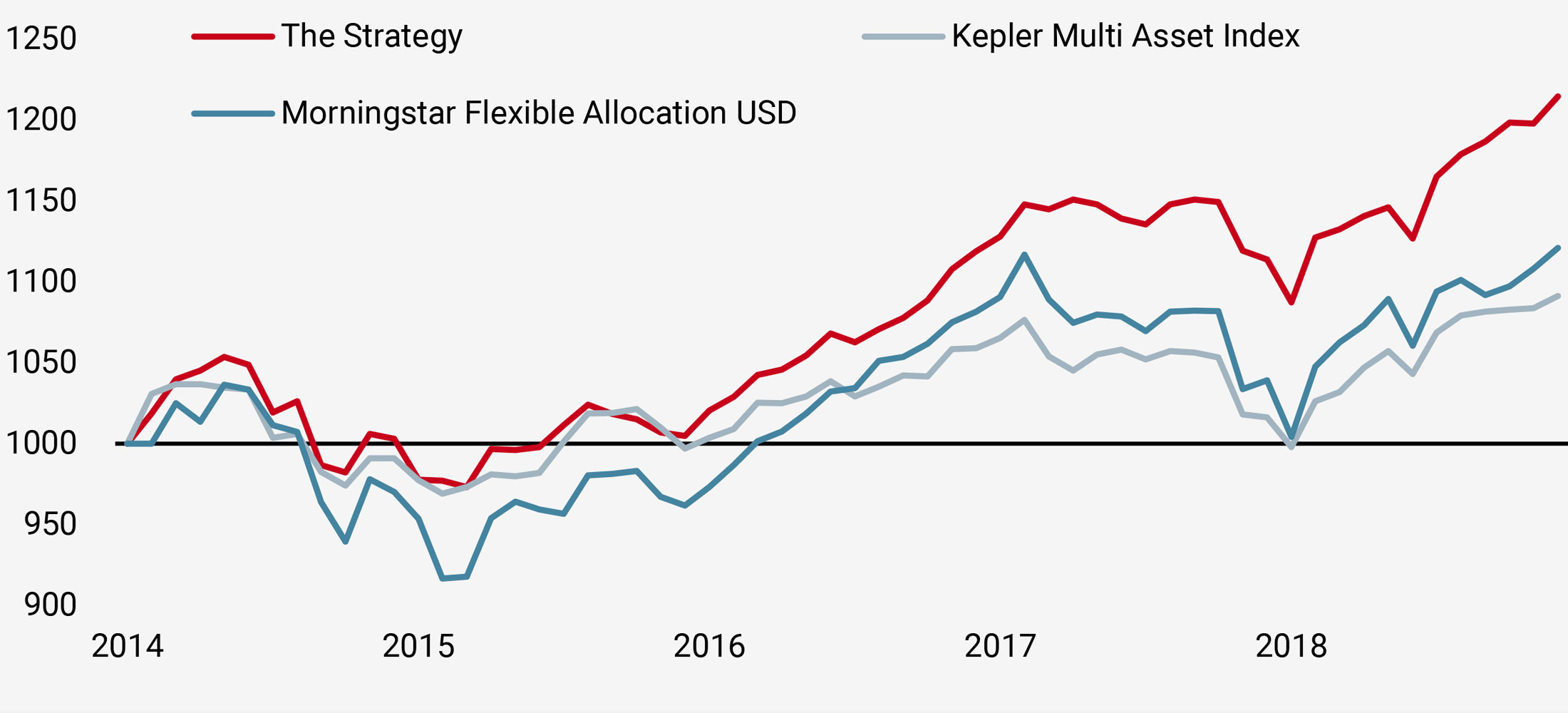

Over the last five years, the global economy has grown around potential levels with minimal inflation, allowing most assets to post strong performances. Moreover, accommodative biases from central banks have compressed the risk premia of most risky assets and pushed realised volatility lower. This stable macro scenario has been favourable for balanced portfolios, as shown in Figure 2. In that environment, the Strategy has outperformed both key multi asset indices, delivering 23% since December 2014 (net of fees) versus 14% for the Morningstar Flexible Allocation USD and 10% for the Kepler Multi Asset Index.

Figure 2: Performance since Inception

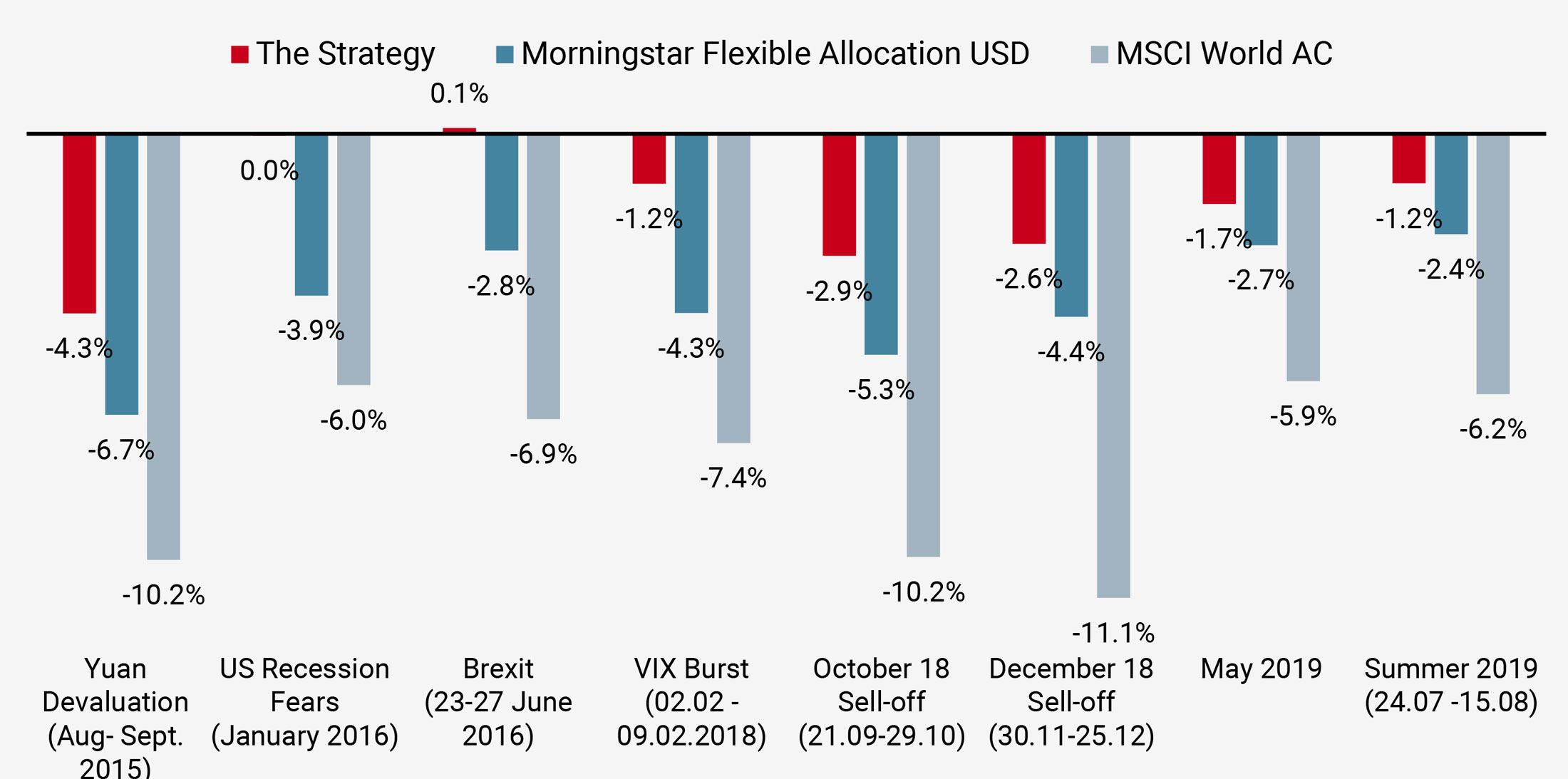

However, headline five-year performance only gives a partial view of the story. Beneath the surface of strong performance for most assets, returns have been far from linear. There have been many events that have triggered large drawdowns in risky assets, including a yuan devaluation in August 2015, the Brexit surprise in June 2016, a VIX spike in February 2018, quantitative tightening in Q4 2018 and US recession fears last year. In our view, the real risk for investors is capital loss, not volatility, so it is crucial to build a portfolio that can limit the negative impact of an equity market sell-off. As illustrated in Figure 3, the two pillars of the Strategy, 1) a diversified investment universe and 2) dynamic asset allocation, have both added value in these negative periods for equity markets. The Strategy has outperformed the Morningstar index 100% of the time and limited its beta-to-equity to 0.2% when equities fell by more than 5% (Figure 3).

Figure 3: Performance During Equity Market Sell-Offs

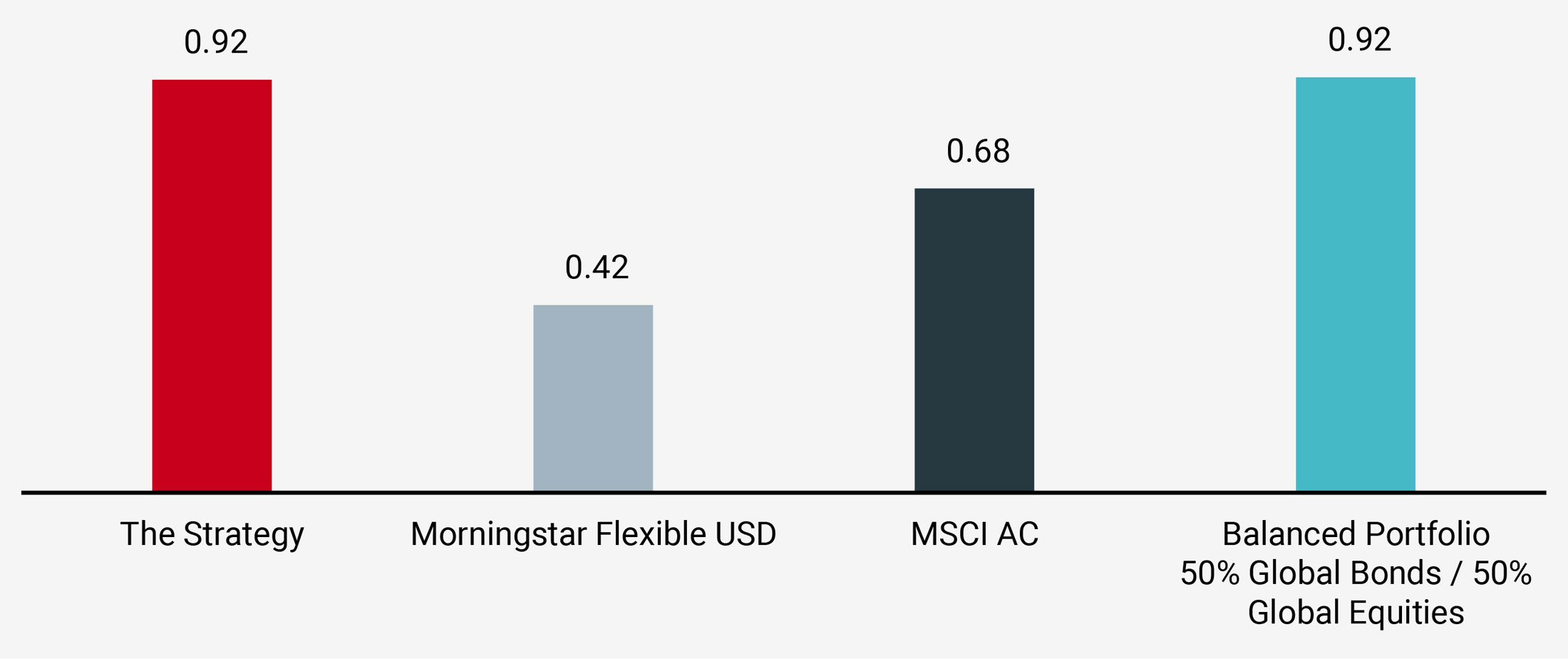

Consequently, the risk-adjusted performance of the Strategy has been high and in line with global equity and balanced passive portfolios (Figure 4).

Figure 4: Risk-adjusted Performance since Inception

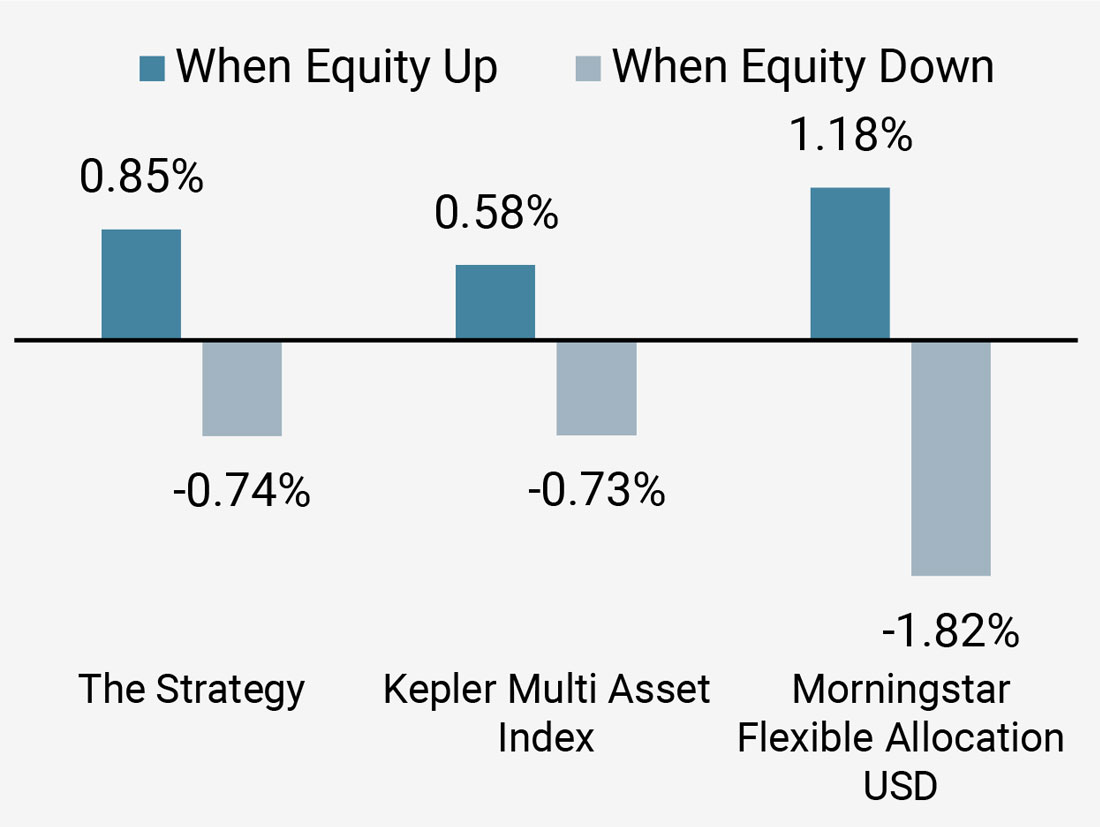

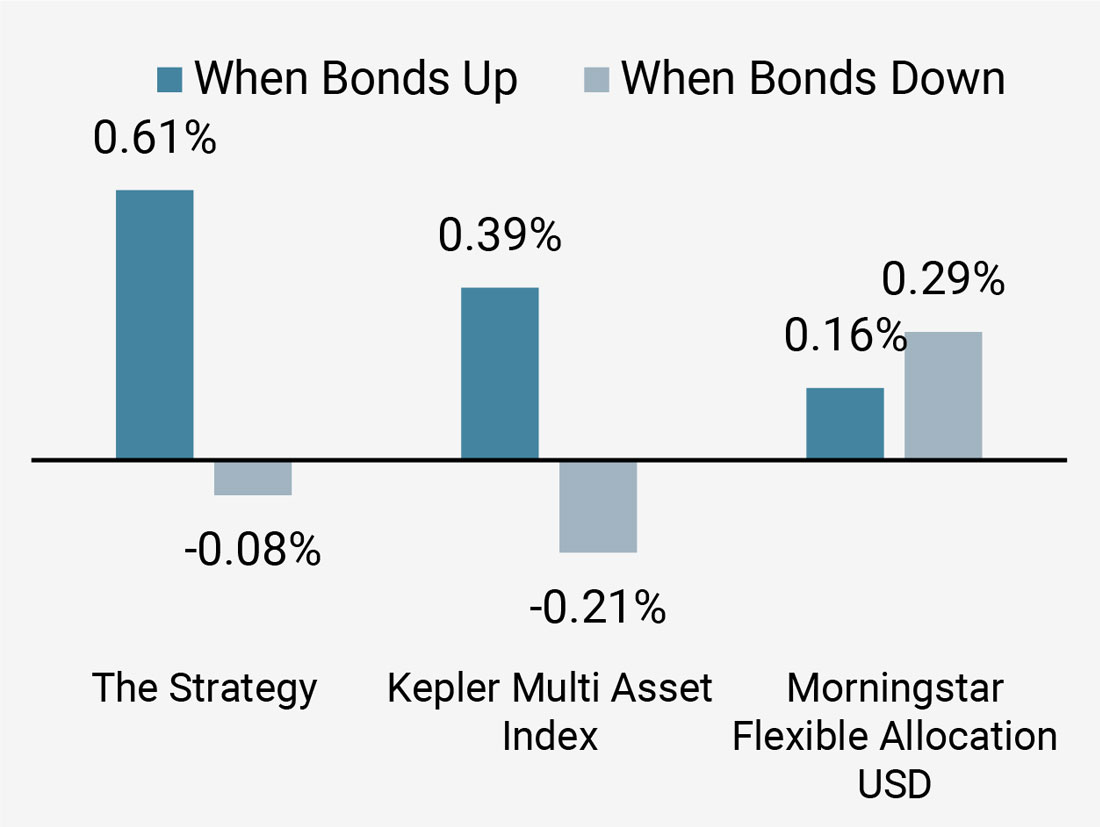

2) Delivered Positive Asymmetry in Different Market Conditions

The Strategy aims to deliver smooth and positive returns in different economic contexts and provide positive return asymmetry, ie higher upside than downside participation. As illustrated in Figures 5a and 5b, the Strategy has achieved, on average, higher bull market performance capture in bonds and equities than in bear contexts.

Figure 5a: Performance in Rising and Falling Equity Markets

This information is based on the most representative account of the Multi Asset Risk Targeted strategy. It is presented as supplemental information only and complements the GIPS compliant presentation (s) provided at the end of this presentation. Past performance is not indicative of future performance.

Figure 5b: Performance in Rising and Falling Bond Markets

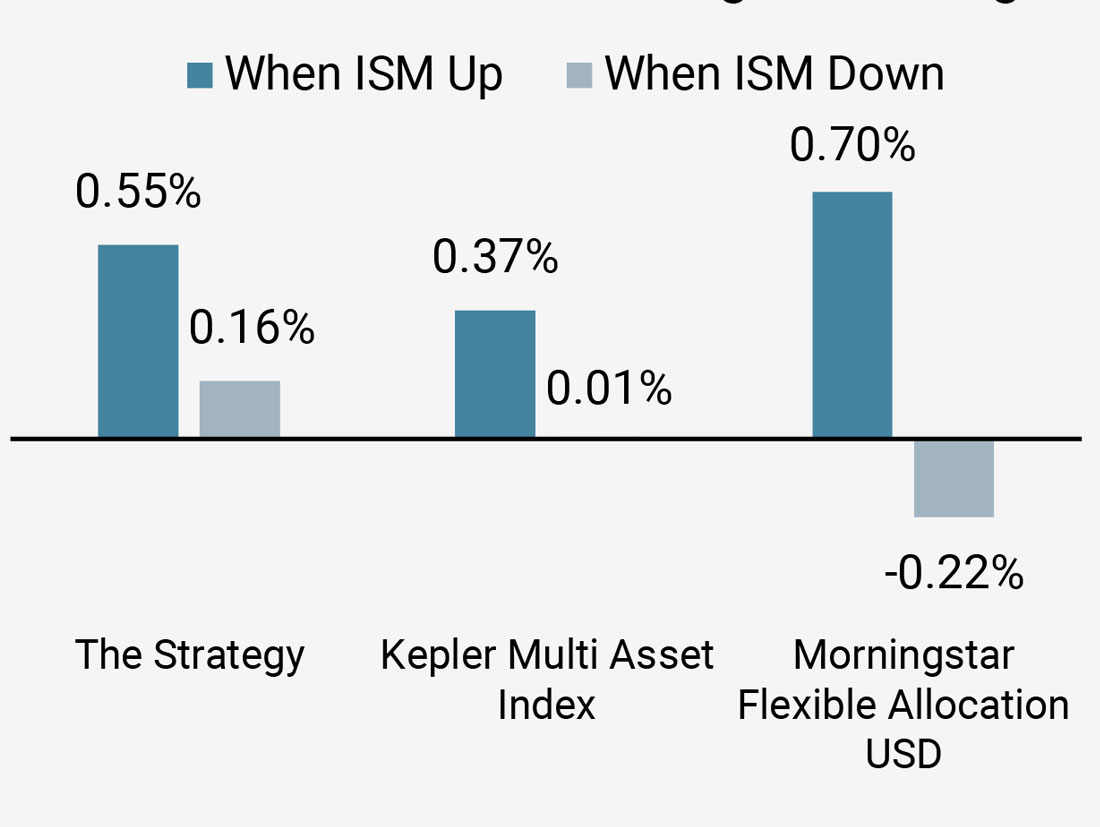

Moreover, thanks to its macro risk-based construction that aims to diversify risk across key macro regimes (recession, inflation surprise, market stress and steady growth), the Strategy has performed well across different economic conditions. As shown in Figure 5c, the Strategy has posted positive returns on average during both monthly declines and increases in the US ISM Manufacturing index.

Figure 5c: Performance when ISM is Rising and Falling

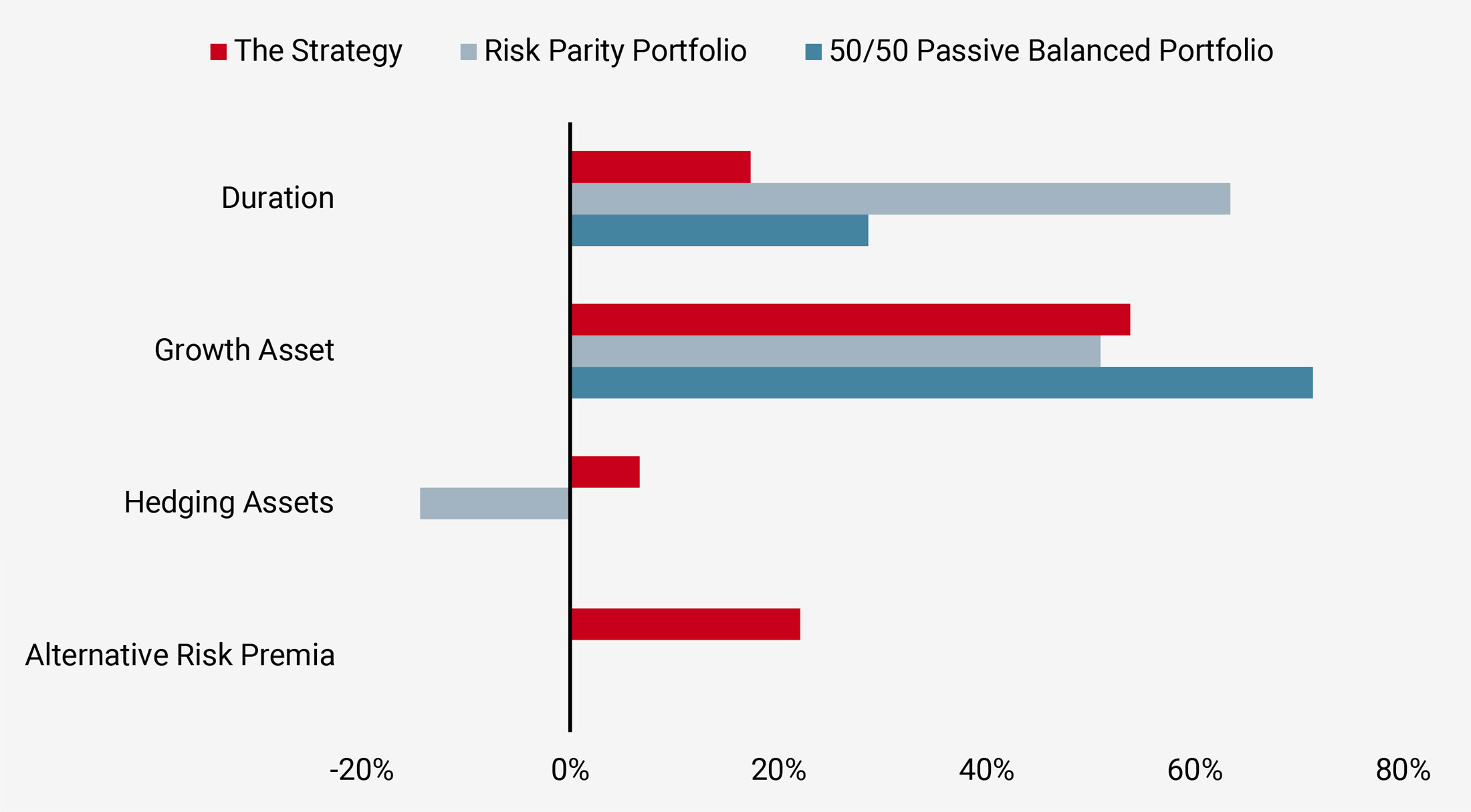

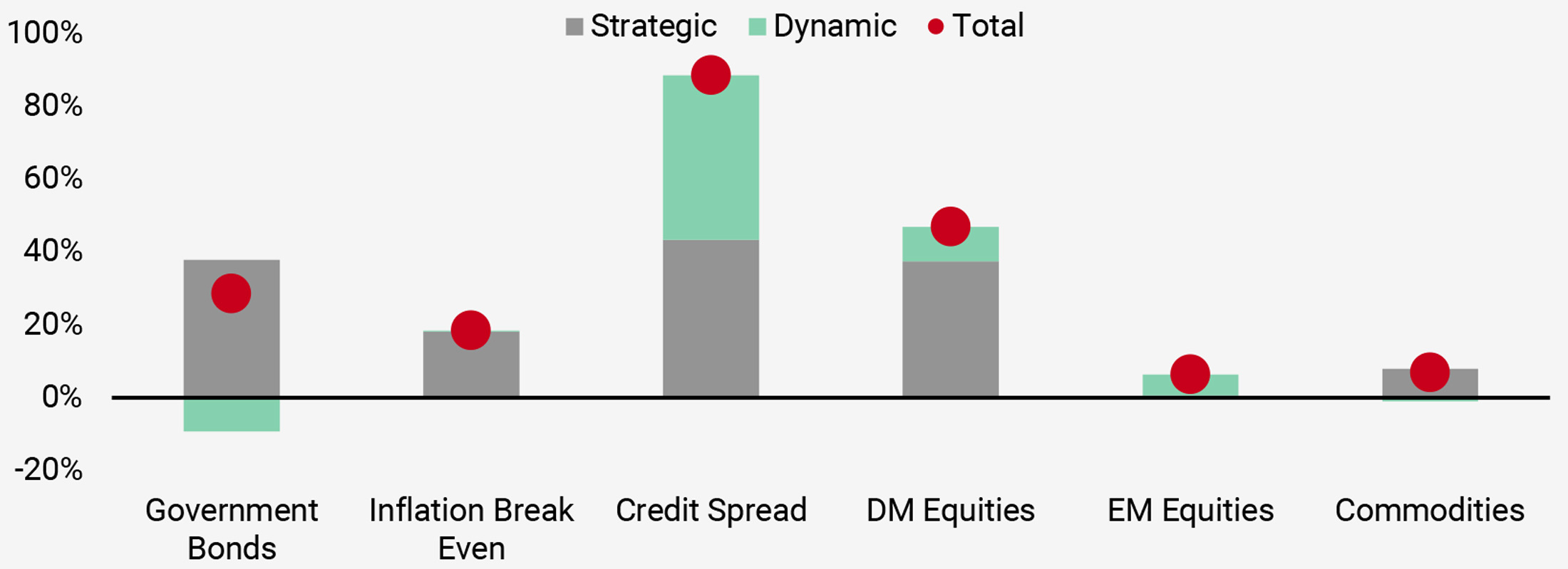

3) Diversified Source of Return

In our view, effective diversification expands the sources of return that drives portfolio performance. A very concentrated portfolio will be driven by only one contributor (e.g. equity) that tends to perform in one specific economic context (growth) or market condition (bull market). In the wake of global quantitative easing, Risk Parity strategies are often cited as a solution to diversify equity risk. This type of multi asset solution has become popular over the past ten years and has delivered attractive returns in many cases. However, traditional balanced portfolio returns have not been as diversified as expected. In 50% / 50% portfolios, equity returns represent on average more than 70% of total performance over the last five years, while duration contribution has been large for Risk Parity strategies, as shown in Figure 6.

Over the period, our expanded investment universe that mixes traditional and liquid alternative risk premia provided a more balanced performance contribution. For example, the contribution from growth assets represents less than 50% of the total performance, and duration less than 25%. The contribution from liquid alternative risk premia accounts for more than 25%, illustrating the benefits of an expanded investment universe that includes both traditional and alternative risk premia.

Figure 6: Performance Contribution by Assets

In our view, this highly differentiated return set bodes well for future performance at a time when equities and duration valuations are high and expected returns are low.

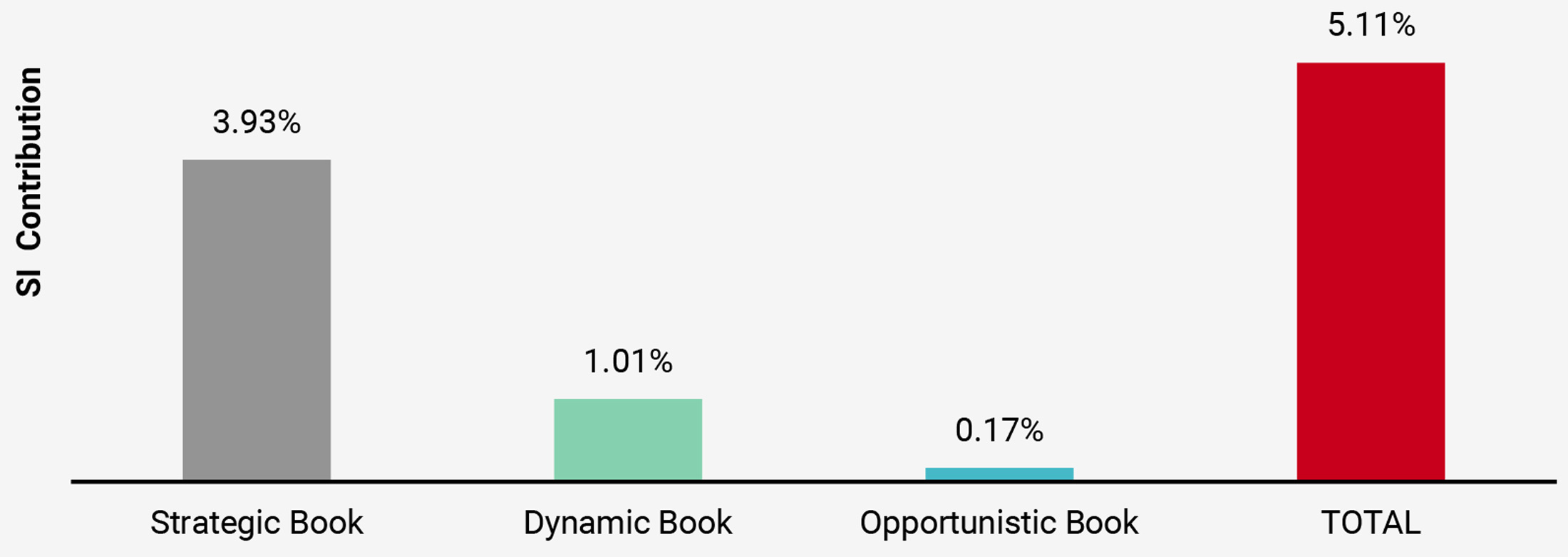

4) Robustness in the Investment Process

Our investment process consists of three main building blocks. The strategic book aims to harvest returns from a broad, diversified universe of traditional and liquid alternative risk premia using a risk-controlled framework to provide consistent returns on average across economic regimes. The dynamic book adapts the strategic portfolio to the current economic environment, both in terms of asset allocation within and across risk premia, and in terms of risk targeting. Finally, the opportunistic book takes short-term tactical positions to exploit specific opportunities via relative value trades with an expected low correlation to key risk premia.

This kind of portfolio construction provides full diversification: firstly across time horizons (long-term vs medium and short-term); secondly, across investment styles that mix systematic and discretionary elements; and finally, across risk dimensions with a close monitoring of macro risks, market sentiment and valuation, the three main drivers of asset returns over the long term.

As can be seen below (Figure 7), each component contributed positively to performance since inception on an annualised basis, consistent with their respective risk targets.

Figure 7: Contribution by Books in the Strategy

- Since inception, the Strategy has returned 5.1% p.a. (gross of fees), and 4.5% p.a. (net of fees)

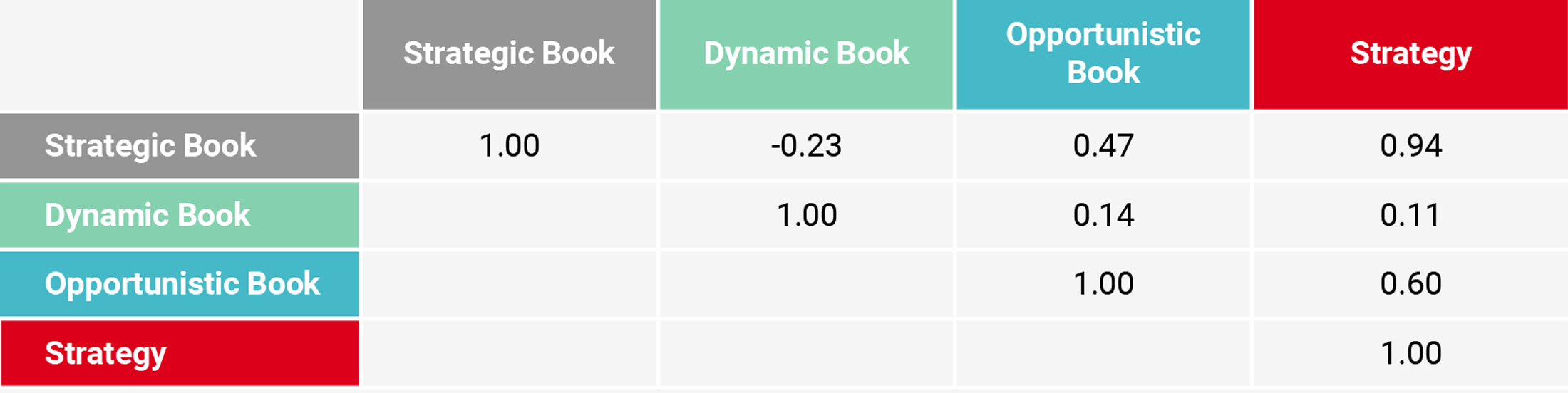

More importantly, the correlation between different elements was low and helped to smooth the return, meaning that dynamic risk management added return without increasing risk, which is the aim of a robust portfolio (Figure 8).

Figure 8: Correlation between Books in the Strategy

- Since inception, the Strategy has returned 5.1% p.a. (gross of fees), and 4.5% p.a. (net of fees)

Over the past five years, we have also developed a dedicated approach to integrating ESG factors into our investment process. Unigestion has been managing ESG/SRI solutions since 2004, including bespoke mandates tailored to reflect clients’ specific ESG criteria. In the Strategy, our ESG policy is applied across all the physical assets we invest in (equities, government bonds and commodities), representing 99% of the NAV (excluding cash). Thanks to our dedicated filters, we have improved the ESG scores and the carbon footprint for both equity and bond allocations in the Strategy, which are managed against key benchmarks, including the MSCI World and Barclays Global Treasury indices. The Strategy continues to be a pioneer in ESG investing within the multi asset space.

5) Well Equipped to Navigate Whatever 2020 Holds in Store

The global economy has been slowing since mid-2018. US monetary tightening implemented last year, the decline in global trade growth observed since 2016 and weak activity in Europe have been the main triggers, driving the deceleration over the last 15 months. In addition to weaker activity, rising tensions between the US and China have increased uncertainty, negatively impacting investment perspectives and production expectations.

Despite this broad economic slowdown, 2019 was a great year for global stocks, with the MSCI World index delivering its tenth best annual return since 1970. Historically, such returns for equities were driven by macroeconomic acceleration, an increase in corporate profitability or a positive shock such as globalisation or technological innovation. However, this time the backdrop has been one of slower global growth, unchanged earnings per share and a rise in geopolitical uncertainties and polarisation.

The key difference in 2019 was a globally coordinated central bank shift to a more stimulative stance that served to push growth assets higher. We believe that central bank policy is likely to remain supportive in light of muted inflation pressures that show no signs of increasing. However, the sustained rally has pushed valuations up to levels that we believe are concerning in some areas and 2020’s global political calendar will likely weigh heavily on investor sentiment.

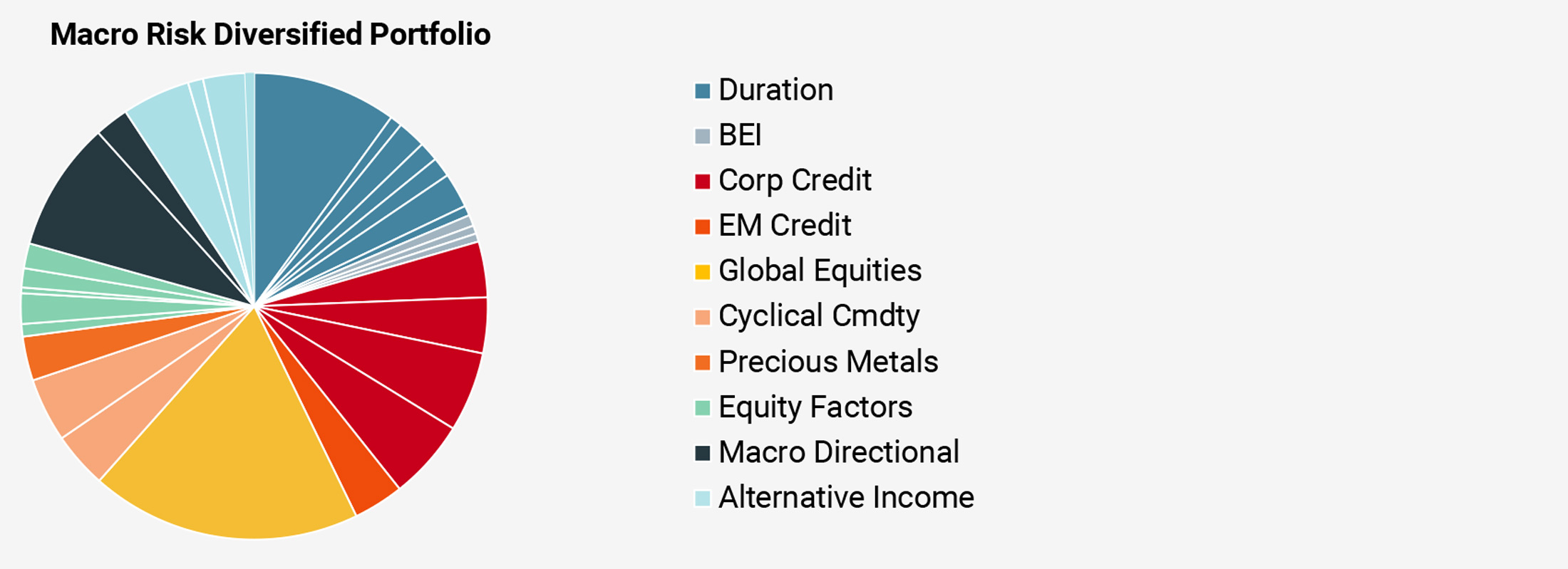

Figure 9a: Growth Tilts for Starting 2020 (capital allocation as of 31.12.2019)

Figure 9b: A Fully Diversified Portfolio (capital allocation by risk premia)

Against this backdrop, our main investment themes for 2020 are as follows:

- Although the global economy has been slowing for 15 months, we do not believe a recession is on the cards.

- With inflation nowhere to be found, we expect central banks to remain dovish, offering continued support to financial markets.

- While the outlook for growth-oriented assets remains positive, valuations are one area of concern.

- Within our multi asset portfolios, our preference is for equities and credit, but with greater discrimination than in the past.

We continue to believe that our macro risk-based Strategy with its two core pillars – enhanced diversification and dynamic risk management – is well equipped to deliver positive and stable returns in the coming years.

Important Information

Past performance is no guide to the future, the value of investments, and the income from them change frequently, may fall as well as rise, there is no guarantee that your initial investment will be returned. This document has been prepared for your information only and must not be distributed, published, reproduced or disclosed (in whole or in part) by recipients to any other person without the prior written consent of Unigestion. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation.

This is a promotional statement of our investment philosophy and services only in relation to the subject matter of this presentation. It constitutes neither investment advice nor recommendation. This document represents no offer, solicitation or suggestion of suitability to subscribe in either the investment vehicles to which it refers or to any securities or financial instruments described herein. Any such offer to sell or solicitation of an offer to purchase shall be made only by formal offering documents, which include, among others, a confidential offering memorandum, limited partnership agreement (if applicable), investment management agreement (if applicable), operating agreement (if applicable), and related subscription documents (if applicable). Such documentation contains additional information material to any decision to invest. Please contact your professional adviser/consultant before making an investment decision.

Where possible we aim to disclose the material risks pertinent to this document. The views expressed in this document do not purport to be a complete description of the securities, markets and developments referred to in it. Reference to specific securities should not be considered a recommendation to buy or sell. Unigestion maintains the right to delete or modify information without prior notice.

Investors shall conduct their own analysis of the risks (including any legal, regulatory, tax or other consequences) associated with an investment and should seek independent professional advice. Some of the investment strategies or financial instruments described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment. These are not suitable for all types of investors. Unigestion has the ability in its sole discretion to change the strategies described herein.

To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks. Actual results could differ materially from those in the forward-looking statements. As such, forward looking statements should not be relied upon for future returns. Targeted returns reflect subjective determinations by Unigestion based on a variety of factors, including, among others, internal modeling, investment strategy, prior performance of similar products (if any), volatility measures, risk tolerance and market conditions. Targeted returns are not intended to be actual performance and should not be relied upon as an indication of actual or future performance.

No separate verification has been made as to the accuracy or completeness of the information herein. Data and graphical information herein are for information only and may have been derived from third party sources. Unigestion takes reasonable steps to verify, but does not guarantee, the accuracy and completeness of information from third party sources. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. All information provided here is subject to change without notice. It should only be considered current as of the date of publication without regard to the date on which you may access the information. Rates of exchange may cause the value of investments to go up or down. An investment with Unigestion, like all investments, contains risks, including total loss for the investor.

Additional Information for U.S. Investors

The performance figures are based on estimated fees and expenses as well as on the underlying strategy’s estimated performances given by fund managers, administrators, custodians and third party sources at a given date. Where performance is reflected gross of fees, potential investors should be aware that the inclusion of fees, costs and charges will reduce the overall value of performance. Unless otherwise stated, the performance data source are Unigestion, Bloomberg and Compustat.

This information is provided to you solely to give you background information relating to Unigestion, certain strategies it implements and currently offers. Before making an investment decision with respect to the strategy discussed herein, potential investors are advised to consult with their tax, legal, ERISA and financial advisors. Note that not all strategies may be available or suitable for investment by U.S. investors.

This document may contain forward-looking statements, including observations about markets and industry and regulatory trends as of the original date of this document. Forward-looking statements may be identified by, among other things, the use of words such as “expects,” “anticipates,” “believes,” or “estimates,” or the negatives of these terms, and similar expressions. Forward-looking statements reflect Unigestion’s views as of such date with respect to possible future events. Actual results could differ materially from those in the forward-looking statements as a result of factors beyond a strategy’s or Unigestion’s control. Readers are cautioned not to place undue reliance on such statements. No party has an obligation to update any of the forward-looking statements in this document

Return targets or objectives, if any, are used for measurement or comparison purposes and only as a guideline for prospective investors to evaluate a particular investment program’s investment strategies and accompanying information. Performance may fluctuate, especially over short periods. Targeted returns should be evaluated over the time period indicated and not over shorter periods.

The past performance of Unigestion, its principals, shareholders, or employees is not indicative of future returns.

Except where otherwise specifically noted, the information contained herein, including performance data and assets under management, relates to the entire affiliated group of Unigestion entities over time including that of Unigestion UK. Such information is intended to provide the reader with background regarding the services, investment strategies and personnel of the Unigestion entities. No guarantee is made that all or any of the individuals involved in generating the performance on behalf the other Unigestion entities will be involved in managing any client account on behalf of Unigestion U.K. More specific information regarding Unigestion UK is set forth herein where indicated and is available on request.

There is no guarantee that Unigestion will be successful in achieving any investment objectives. An investment strategy contains risks, including the risk of complete loss.

The risk management practices and methods described herein are for illustrative purposes only and are subject to modification.

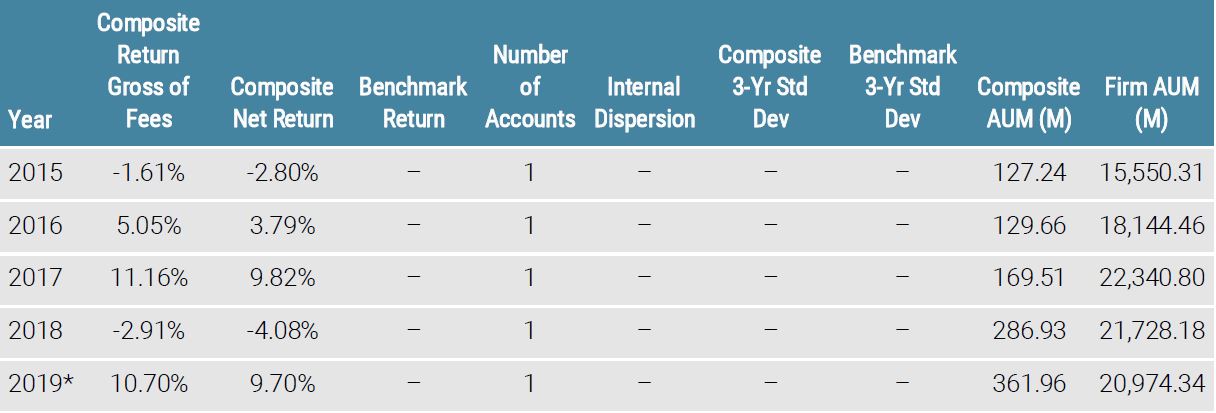

Unigestion

Multi Asset Risk Targeted (Medium) (USD)

31 Dec 2014 to 30 September 2019

*YTD 30 Septeber 2019.

Special Disclosure: For presentations prior to 31 March 2018 the strategy was measured against the LIBOR 3M USD + 4%. Beginning April 2018 the firm determined that the benchmark did not accurately reflect the strategy mandate and the benchmark was removed.

Definition of the Firm: For the purposes of applying the GIPS Standards, the firm is defined as Unigestion. Unigestion stands for the Unigestion Group and includes all Unigestion subsidiaries (Unigestion Asset Management (France) SA, Unigestion SA, Unigestion (UK) Ltd, Unigestion (US) Ltd, Unigestion Asset Management (Canada) Inc, Unigestion Asia Pte Ltd). Individual subsidiaries of the Unigestion Group do not claim GIPS compliance on a stand-alone basis. Unigestion is responsible for managing assets on the behalf of institutional investors. Unigestion invests in several strategies for institutional clients: Equities, Hedge Funds, Private Assets and the solutions designed for the clients of our Cross Asset Solution department. The GIPS firm definition excludes the Fixed Income Strategy Funds, which started in January 2001 and closed in April 2008, and the accounts managed for private clients. Unigestion defines the private clients as High Net Worth Families and Individual investors.

Policies: Unigestion policies for valuing portfolios, calculating performance, and preparing compliant presentations are available upon request.

Composite Description: The Multi Risk Targeted (Medium) composite was defined on 15 December 2014. It consists of accounts which aim to deliver consistent smooth returns of cash + 5% gross of fees across all market conditions over a 3-year rolling period. It seeks to achieve this by capturing the upside during bullmarkets while protecting capital during market downturns.

Benchmark: Because the composites strategy is absolute return and investments are permitted in all asset classes, no benchmark can reflect this strategy accurately.

Fees: Returns are presented gross of management fees, administrative fees but net of all trading costs and withholding taxes. The maximum management fee schedule is 1.2% per annum. Net returns are net of model fees and are derived by deducting the highest applicable fee rate in effect for the respective time period from the gross returns each month.

List of Composites: A list of all composite descriptions is available upon request.

Minimum Account Size: The minimum account size for this composite is 5’000’000.- USD.

Valuations: Valuations are computed in US dollars (USD). Performance results are reported in US dollars (USD).

Internal Dispersion & 3 YR Standard Deviation: The annual composite dispersion presented is an asset-weighted standard deviation calculated for the accounts in the composite the entire year. When internal dispersion is not presented it is as a result of an insufficient number of portfolios in the composite for the entire year. When the 3 Year Standard Deviation is not presented it is as a result of an insufficient period of time.

Compliance Statement: Unigestion claims compliance with the Global Investment Performance Standards (GIPS®) and has prepared and presented this report in compliance with the GIPS standards. Unigestion has been independently verified for the periods 1 January 2003 to 31 December 2016. The verification report(s) is/are available upon request. Verification assesses whether (1) the firm has complied with all the composite construction requirements of the GIPS standards on a firm-wide basis and (2) the firms policies and procedures are designed to calculate and present performance in compliance with the GIPS standards. Verification does not ensure the accuracy of any specific composite presentation.

Legal Entities Disseminating this Document

UNITED KINGDOM

This material is disseminated in the United Kingdom by Unigestion (UK) Ltd., which is authorized and regulated by the Financial Conduct Authority (“FCA”).

This information is intended only for professional clients and eligible counterparties, as defined in MiFID directive and has therefore not been adapted to retail clients.

UNITED STATES

This material is disseminated in the U.S. by Unigestion (UK) Ltd., which is registered as an investment adviser with the U.S. Securities and Exchange Commission (“SEC”). This information is intended only for institutional clients and qualified purchasers as defined by the SEC and has therefore not been adapted to retail clients.

EUROPEAN UNION

This material is disseminated in the European Union by Unigestion Asset Management (France) SA which is authorized and regulated by the French “Autorité des Marchés Financiers” (“AMF”).

This information is intended only for professional clients and eligible counterparties, as defined in the MiFID directive and has therefore not been adapted to retail clients.

CANADA

This material is disseminated in Canada by Unigestion Asset Management (Canada) Inc. which is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario and Quebec. Its principal regulator is the Ontario Securities Commission (“OSC”).

This material may also be distributed by Unigestion SA which has an international advisor exemption in Quebec, Saskatchewan and Ontario. Unigestion SA’s assets are situated outside of Canada and, as such, there may be difficulty enforcing legal rights against it.

SWITZERLAND

This material is disseminated in Switzerland by Unigestion SA which is authorized and regulated by the Swiss Financial Market Supervisory Authority (“FINMA”).

SINGAPORE

This material is disseminated in Singapore by Unigestion Asia Pte Ltd. which is regulated by the Monetary Authority of Singapore (“MAS”).