After a very positive start to the month for risky assets, triggered by strong expectations on the fiscal front, the noise coming from various pockets of risk has taken its toll on investor optimism. Uncertainty about the outcome of the US presidential election, Brexit and a deteriorating health situation has resurfaced, reminding market participants that a few hurdles remain before gently riding the long-term wave of support and accommodation. Has new information surfaced that could transform the noise into a genuine signal and justify fragility, or is it just legitimate volatility ahead of non-trivial events?

The Rest Is Noise

What’s Next?

Fundamental signals remain solid

As mentioned in last week’s edition of Macro Views, the current, exceptional level of accommodation from central banks and governments has created an unprecedented tailwind which will last well past the crisis. The signal coming from observable data is clear: the recovery is strong and sustainable, although its pace has slowed lately. Our proprietary growth diffusion indices point toward a 55% to 60% ratio of improving data, in spite of a large country dispersion. Economic surprise indices are anchored in very high territories while the actual level of growth in a number of emerging countries has risen well above potential, with China leading the pack.

Global financing conditions remain extremely accommodative, on the back of unprecedented monetary stimulus. Housing has proven to be extremely resilient and the number of new homes sold in the US has jumped to 13-year highs. Production expectations are expansionary, well anchored above the 50 threshold in most major economies and employment continues to improve.

However there still remains pockets of weakness, especially in consumption: initially, helicopter money was mainly kept on the sidelines as additional savings rather than spent and injected into the real economy. In the US, national saving rates peaked at 35% of disposable income at the height of the crisis, but have now receded to low double digits. The velocity of money remains depressed, reflecting both the fact that uncertainties around future economic conditions remain strong and that the bulk of money creation has so far been used to fund central bank asset purchases (benefitting Wall Street).

This represents more of an opportunity than a threat, given the magnitude of dormant demand that will be unleashed when hurdles clear and confidence is restored.

Noise levels are increasing as hurdles come closer

Yet, market fragility seems justified over the short run. Concerns surrounding the results of the presidential elections in the US and Brexit in Europe are keeping uncertainty at elevated levels, and the risks should not be understated given the stakes involved.

Over the past few weeks, our view of the US election has shifted from a likely Biden victory with the US Senate being a toss-up to a clear majority vote for Biden and the US Senate leaning towards Democratic control. Overall, such a result should be a positive catalyst for equity markets in the short-term as Democratic control of both the executive and legislative branches would likely result in significant stimulus and less volatile foreign and trade policies. This would overcompensate the negative effects of the expected partial cancellation of corporate tax cuts and provide a long-term supportive framework for financial assets, especially within the “low for long” rates environment. The risk that election uncertainty will last well past the election date is being priced out slowly but surely, although the probability that Trump could contest the results remains a potential risk which could resurface as we get closer to the election date and polls become more volatile.

On the other side of the Atlantic, Brexit talks are raging on and it seems unlikely that both parties will come to an agreement in the days to come. The probability of a “no deal” outcome has been rising over the course of the week, with very limited market impact so far, but negotiations are set to continue past Prime Minister Johnson’s self-imposed 15 October deadline. The market seems to be expecting that there will be some sort of “soft” Brexit deal in the future although this might be complacent given time is running out and little to no progress has been made. Johnson has warned that the UK should start getting ready for a no deal-style exit in January and is currently blaming the EU for the lack of progress in the negotiations. Genuine threat or negotiation tactic? Time will tell, but for now uncertainty could continue to prevail.

Another sentiment shaker is the risk posed by a second wave of Covid-19, the increase in restrictions various governments are imposing on populations and the resulting impact on demand in terms of both corporate investment and private consumption. Despite decreasing fatality rates, there is a fine line between containing or losing control of the pandemic, which would yield completely different outcomes on the shape of the last leg of the recovery and for financial assets overall.

One key factor that would unleash full optimism would be the validation of a vaccine. Odds for an approval by the FDA were initially optimistic, leaning towards year-end, but the FDA’s two-month follow-up guideline for an Emergency Use Authorization makes it very unlikely. Data readouts are due at the end of October/early November, and the key measure to watch for will be the efficacy rates: 75% or above in the first interim results would be very encouraging for a rapid deployment and would likely be welcomed by the investment world. Production and implementation would take place towards the end of the Q1 2021, with visible impacts on growth from Q2 onward.

Pragmatism is required: the medium-term horizon looks bright

What matters the most is what lasts the longest. In that respect, we believe in central bank rhetoric that long-term support will remain as long as necessary, while other rounds of fiscal boosts are likely, at least in the US. This is what will last and what matters over the coming year. In addition, inflation remains contained, positioning has improved (at least partially) and risk appetite remains stable.

Therefore, looking past the noise, we remain tilted toward pro-growth / pro-cyclical assets, with a preference for equities. Short-term risks have already been factored into stock prices, while the positive, durable factors discussed above present upside potential in the asset class as the clouds disperse.

Unigestion Nowcasting

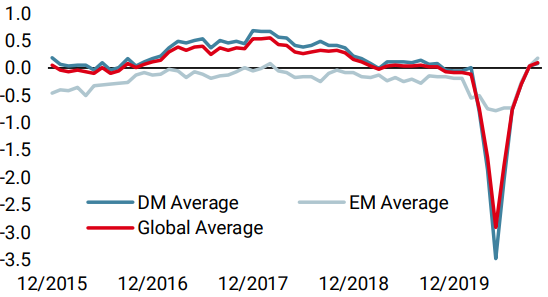

World Growth Nowcaster

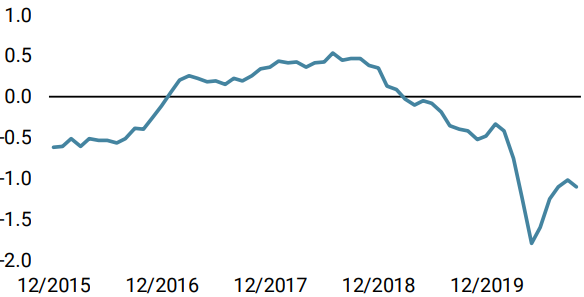

World Inflation Nowcaster

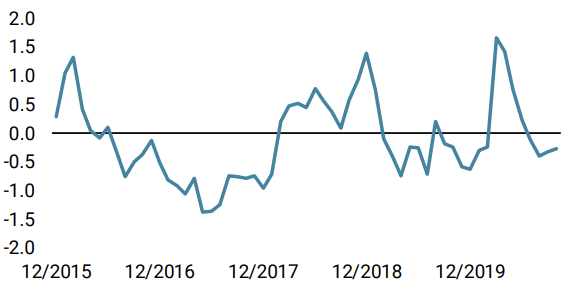

Market Stress Nowcaster

Weekly Change

- Our World Growth Nowcaster increased again last week, thanks to solid Japanese, Canadian and UK data. Emerging economies improved as well, with China still leading the pack.

- Our World Inflation Nowcaster remained stable. Overall, inflation surprise risk is very low.

- Last week, our Market Stress Nowcaster evolved within a range, as volatility proved to be changing and spreads rose at the end of the week.

Sources: Unigestion. Bloomberg, as of 19 October 2020.

Important Information

This document is provided to you on a confidential basis and must not be distributed, published, reproduced or disclosed, in whole or part, to any other person.

The information and data presented in this document may discuss general market activity or industry trends but is not intended to be relied upon as a forecast, research or investment advice. It is not a financial promotion and represents no offer, solicitation or recommendation of any kind, to invest in the strategies or in the investment vehicles it refers to. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment.

The investment views, economic and market opinions or analysis expressed in this document present Unigestion’s judgement as at the date of publication without regard to the date on which you may access the information. There is no guarantee that these views and opinions expressed will be correct nor do they purport to be a complete description of the securities, markets and developments referred to in it. All information provided here is subject to change without notice. To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks.

Data and graphical information herein are for information only and may have been derived from third party sources. Although we believe that the information obtained from public and third party sources to be reliable, we have not independently verified it and we therefore cannot guarantee its accuracy or completeness. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. Unless otherwise stated, source is Unigestion. Past performance is not a guide to future performance. All investments contain risks, including total loss for the investor.

Unigestion SA is authorised and regulated by the Swiss Financial Market Supervisory Authority (FINMA). Unigestion (UK) Ltd. is authorised and regulated by the UK Financial Conduct Authority (FCA) and is registered with the Securities and Exchange Commission (SEC). Unigestion Asset Management (France) S.A. is authorised and regulated by the French “Autorité des Marchés Financiers” (AMF). Unigestion Asset Management (Canada) Inc., with offices in Toronto and Montreal, is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario and Quebec. Its principal regulator is the Ontario Securities Commission (OSC). Unigestion Asia Pte Limited is authorised and regulated by the Monetary Authority of Singapore (MAS). Unigestion Asset Management (Copenhagen) is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Danish Financial Supervisory Authority” (DFSA). Unigestion Asset Management (Düsseldorf) SA is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Bundesanstalt für Finanzdienstleistungsaufsicht” (BAFIN).