Thus far, June has seen a continuation and acceleration of the themes observed in April and May: an improving macroeconomic situation and fast-recovering investor sentiment. Newsflow on the pandemic has materially improved, economic data is less negative and a shift out of safe assets into growth and inflation-related assets is gaining momentum. Compared to the last few weeks, the rally seems broader-based, taking the shape and form of a more traditional recovery driven by a “risk on” event, with most risk assets thriving at the expense of hedge assets.From a Narrow to a Broad-based Recovery

Rally Round

Economists are expecting 2020 to be a recessionary year, with a severe worldwide economic contraction. The April 2020 IMF WEO report puts global GDP growth for this year at -3%, with significant disparity: in the US, this number becomes -5.9%, -9.1% for Italy, -7.2% for France and -6.9% for Germany. Yet, we see a light at the end of tunnel as, for markets, the direction of the macro trend matters more than its current level. Across the different point-in-time indicators we are looking at, we see reason for hope. First, our Newscaster, which turns economic growth-related media newsflow into a growth barometer, has been reflecting an improvement for some time now. Currently, its diffusion index, which measures the percentage of improving underlying data, has reached about 70%. Our world Growth Nowcaster, which does the same purely based on economic data, has recently started picking up on this improving trend: its diffusion index has seen a rapid increase, from sub-30% levels to around 50% now. In the US and in the Eurozone, the majority of economic sectors are now showing similar signs of recovery. Last Friday’s job report is the perfect example of how markets could be surprised by the pace of the recovery: economists expected 7.5m job losses in the US but the US economy managed to create around 3m new jobs. Economic surprise indices show that this improvement extends well beyond employment yet most economists still do not expect a V-shaped recovery. Investors should keep in mind how the pace of the recovery reflects the unprecedented scale of the fiscal and monetary policy response implemented to ensure a rapid come-back of activity. Last week, Europe made another step into that “growth support” direction, increasing the size of its fiscal spending (EUR 750bn+) and its monetary policy support, with ECB President Christine Lagarde announcing an additional EUR 600bn to the bank’s pandemic-related PEPP programme. No wonder our “central bank heartbeat” – an indicator turning central bank statements into a measure of dovishness – continues to indicate an extreme level of accommodation: this combined support is here to stay. So far in June, markets have reacted very positively to this improved growth situation, with a significant recovery in sentiment. In recent weeks, participation in the rally has been limited to specific segments of growth assets: quality stocks, technology names and high quality credit. However, with confirmation that the health situation is stabilising, improvements on the macro front and renewed support from central banks, risk-taking has spread across financial assets more broadly. Laggards have outpaced early winners and safe havens suffered their worst week since the end of March. The MSCI World Value index delivered one of its largest outperformances versus its Growth counterpart in years, returning 8% and 3.2%, respectively. The Euro Stoxx 50 jumped 10% over the week, as did the oil 1st future contract, sent higher by the combination of improving demand (the global economy resuming activity) and supply (extension of production cuts). In credit, US high yield returned 5.7% while the S&P 500 delivered “only” 3.1%, buoyed by rising energy prices and lower anticipated risk of defaults. In FX, high beta currencies remained bid up, especially in emerging markets, pushed higher by systematic strategies getting squeezed out of their previous shorts, while the US dollar, the Japanese yen and Swiss franc sold off. Government bonds lost 1% globally, with 10-year yields 20bps higher on the week in most major economies. Inflation breakevens continued to gain traction, highlighting that expectations implied in both growth and inflation premiums are being repriced. This is quite a change from the earlier legs of the rally when recession fears remained anchored in defensive assets. This week, the FOMC meeting could be a key driver of sentiment. Particular attention will be paid to any changes in unconventional monetary policy measures and the economic outlook. The latest statements from Fed members indicated the need for even greater clarity in terms of forward guidance, even though the central bank could wait until September to do so, allowing time to fully grasp the effects of the COVID-19 pandemic on the real economy. We stand by the belief that the Fed is ready to do more if necessary, at any time, to prevent any disappointment on both Wall Street and Main Street. As the shape of the recovery evolves, so does the appropriate dynamic positioning. In our opinion, the various rotations observed above and below the surface have room to reverse further. A constructive view on the recovery calls for an increasing tilt toward growth-related assets, reduced short exposures to real assets and a reduction in defensive plays such as government bonds. Indeed, sovereign paper is increasingly falling out of favour, with systematic and trend-following players offloading more and more rapidly. This could pose a risk to diversified strategies in the near future, despite central bank buying. Moreover, a large repricing in rates would push equity valuations meaningfully higher and endanger the current strength of the rally. Finally, as volatility has dropped to its lowest levels since early February, driving the cost of hedging lower, we believe now is the appropriate time to monetise upside optional structures, which have helped to materially improve participation in the rally, and to implement convex protection to cushion potential short-term reversals in sentiment.What’s Next?

Increasing signs of recovery

Sentiment turns into global risk appetite

Adapting positioning to this evolving environment

Unigestion Nowcasting

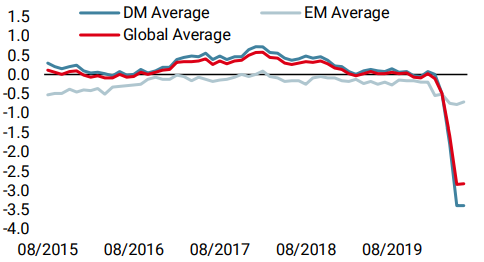

World Growth Nowcaster

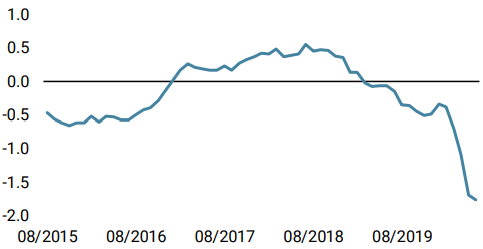

World Inflation Nowcaster

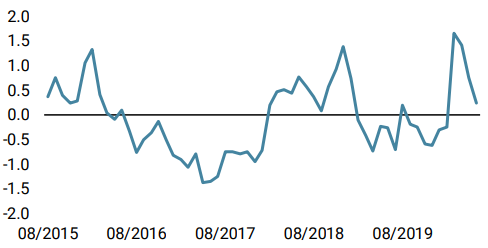

Market Stress Nowcaster

Weekly Change

- Our world Growth Nowcaster remained stable last week, as emerging market economies and the US began to improve. Our indicators are reflecting increasing signs of stabilisation.

- Our world Inflation Nowcaster is also stabilising in the wake of the growth indicator, with the US leading its evolution.

- Our Market Stress Nowcaster decreased last week as credit spreads tightened and liquidity conditions improved.

Sources: Unigestion. Bloomberg, as of 08 June 2020.

Important Information

This document is provided to you on a confidential basis and must not be distributed, published, reproduced or disclosed, in whole or part, to any other person.

The information and data presented in this document may discuss general market activity or industry trends but is not intended to be relied upon as a forecast, research or investment advice. It is not a financial promotion and represents no offer, solicitation or recommendation of any kind, to invest in the strategies or in the investment vehicles it refers to. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment.

The investment views, economic and market opinions or analysis expressed in this document present Unigestion’s judgement as at the date of publication without regard to the date on which you may access the information. There is no guarantee that these views and opinions expressed will be correct nor do they purport to be a complete description of the securities, markets and developments referred to in it. All information provided here is subject to change without notice. To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks.

Data and graphical information herein are for information only and may have been derived from third party sources. Although we believe that the information obtained from public and third party sources to be reliable, we have not independently verified it and we therefore cannot guarantee its accuracy or completeness. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. Unless otherwise stated, source is Unigestion. Past performance is not a guide to future performance. All investments contain risks, including total loss for the investor.

Unigestion SA is authorised and regulated by the Swiss Financial Market Supervisory Authority (FINMA). Unigestion (UK) Ltd. is authorised and regulated by the UK Financial Conduct Authority (FCA) and is registered with the Securities and Exchange Commission (SEC). Unigestion Asset Management (France) S.A. is authorised and regulated by the French “Autorité des Marchés Financiers” (AMF). Unigestion Asset Management (Canada) Inc., with offices in Toronto and Montreal, is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario and Quebec. Its principal regulator is the Ontario Securities Commission (OSC). Unigestion Asia Pte Limited is authorised and regulated by the Monetary Authority of Singapore (MAS). Unigestion Asset Management (Copenhagen) is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Danish Financial Supervisory Authority” (DFSA). Unigestion Asset Management (Düsseldorf) SA is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Bundesanstalt für Finanzdienstleistungsaufsicht” (BAFIN).