From “Behind The Curve” to “Policy Mistake”?

Head of Global Macro & Dynamic Asset Allocation, Cross Asset Solutions

Central banks have changed their tune from “Let’s Dance” to “The Hammer Song”, confirming that fighting inflation has become their top priority. To correct its mistake in assessing both the scale and sustainability of the inflation shock, the Fed is now set to normalise its monetary policy by combining tapering, hiking and quantitative tightening in the same year. Although removing accommodation and normalising financial conditions via tightening makes sense, given the better macroeconomic backdrop compared to a year ago, the timing and calibration has surprised financial markets and raised the risk of policy mistake. As a result, market sentiment turned in January, and the reflexivity game between the Fed and the markets is back. How do we navigate this challenging environment, where wide dispersion beneath the surface paints a more worrisome picture than global indexes show?

The Hammer Song

What’s Next?

Dispersion, dislocation, deleveraging

January was a remarkable month for the history books, to wit; the S&P500 dropped around 4% intraday on Monday the 24th before recovering its losses in the last hour of the session. This kind of event is very rare, occurring only eight times since 1928, underlining the poor liquidity over the month and the importance of systematic strategies in these kind of market conditions. Besides that, the most evident symbol of the current financial landscape has been the dispersion across sectors and styles. The spread of monthly performances between the best and worst sectors in the S&P500 reached 29% in January, a 4-sigma deviation (Figure 1).

Figure 1: Sector divergence within S&P500

Source: Bloomberg, Unigestion. As of 05.02.2022.

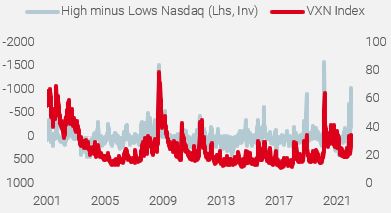

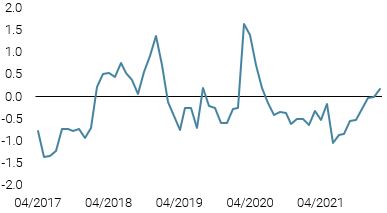

This dispersion proves that beneath the surface, some market segments underwent some great dislocations. The SPAC index, IPO ETF or Crypto complex tumbled in January, due to the negative feedback loop triggered by margin calls or mark-to-market constraints and their associated liquidity needs. When plotting the Nasdaq-100 intraday highs versus lows against its implied volatility, as represented by the VXN Index (Figure 2), we observe a clear divergence between these two measures of risk aversion. While the close-to-close volatility index only moderately increased over the month, the intraday indicator exploded, matching the worst prior panic episodes, such as March 2020 or October 2008.

Figure 2: Nasdaq intraday moves vs VXN Index

Source: Bloomberg, Unigestion. As of 05.02.2022.

Except for cyclical commodities, most assets delivered negative returns over the month, adversely affecting every diversified strategy such as a 50/50 balanced portfolio or Risk Parity. Historically, January 2022 was the worst month since March 2020 for this kind of portfolio; representing the 4% percentile of monthly return distributions since 1973. As a result, leverage for major systematic strategies declined over the month, amplifying the pressure on liquidity.

All of these elements derive from the Fed’s extraordinary and consistent communication, confirming its aim to normalise monetary policy via multiple channels (speeches, press conferences, and minutes of the December meeting) and its desire to escape from being “behind the curve”. It was a wakeup call for the markets, as reflected by the strong rise in short term rates that now price 7 to 8 hikes over the next 24 months versus 4 to 5 a month ago. The global economy’s higher sensitivity to duration and liquidity initially placed us in the “gradual tightening” camp, but we have to acknowledge that the Fed has now lowered the strike of its “put” and set the stage for a stronger and bigger normalisation than initially expected.

Following this re-pricing across and within assets via an adjustment in inflation, growth and liquidity premiums, what is the balance of risks in terms of macro factors?

The positive factors…

On the positive side, our multi-dimensional monitoring of macro risk factors shows:

1) A cleaner positioning with a low beta to equities for most flexible Hedge Funds and systematic strategies. Our CTA monitoring exhibits a neutral exposure to global equities from a long one in December.

2) Still solid fundamentals, as our Growth Nowcasters for developed and emerging countries point to a global economy growing above its potential.

3) An already well-priced tightening cycle for the next 2 years, in line with previous ones in terms of scale and timing. The US 2-year rose to 1.18% (+45 bps YTD), equivalent to five hikes priced in the Fed funds futures between now and the end of December.

4) A high level of defensiveness as represented by the record low level of AAII US investor sentiment. As an illustration, the call/put bias in small lot single-name options has fallen to its most bearish level since April 2020.

It is worth noting that these positive signals cover technical and fundamental elements, as well as market sentiment. This diversity in signals, combined with their sturdiness over time, could warrant a call for a bottom in risky assets.

…versus the negative ones

Nevertheless, the global picture is more mixed on a medium-term horizon for growth-oriented assets returns.

1) Normalising monetary policy means normalising real rates along the curve, especially on the longer end. Despite having risen by 50 basis points over the month, a US 10yr real rate currently at -0.6% is too low, given the Fed’s target to fight inflation and when compared to the historical distribution of real rates. Current pricing derived from forward real rates curves shows a 10yr real rate above 0% only by 2027. If the Fed delivers on inflation, we believe that real rates could return to neutral faster than currently priced, and this would imply a new injection of volatility in the rates complex and lead to further corrections in risky assets.

2) A flatter forward US yield curve and an inverted VIX curve at the front end historically points to an economic slowdown and a rising risk of recession.

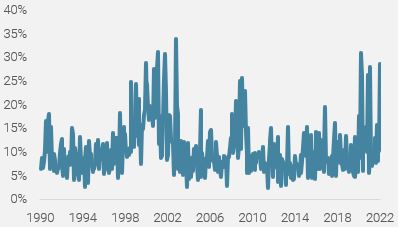

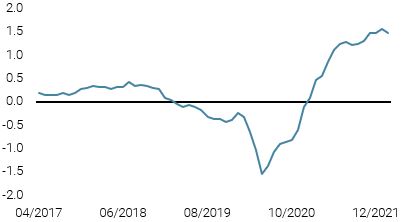

3) Finally, the Fed would start hiking while US consumer struggle with headwinds: negative real income, no more fiscal boost and a lower cushion, while saving rates have normalised from 16% to 7% in 2021. Adding the negative wealth effect felt in January due to the market’s correction and higher mortgage rates, we could have the perfect cocktail to trigger a demand recession. Since 1988, it would be the first time that the Fed hikes while US consumer confidence declines sharply (Figure 3).

Figure 3: Michigan Confidence ahead of first Fed hike

Source: Bloomberg, Unigestion. As of 31.01.2022.

The reflectivity games

The interdependent reflectivity game between the Fed and the market implies continued repricing on both sides. Over the last two months, Fed members acknowledged that they were “behind the curve” and hastened to reduce the gap between “speaking” and “acting”. By doing so, they are taking two major risks: a) hiking too much to satisfy expectations and to restore credibility and b) underestimating the sensitivity of the global economy to any change in real and nominal long-term rates. In January 2017, ahead of the first reduction of the Fed’s balance sheet, Ben Bernanke noted that, “policy communication will be made easier and the risk of market disruption minimised if the shrinkage of the balance sheet, once it begins, is passive and predictable. In particular, once the runoff of the Fed’s assets begins, the FOMC should proceed on the assumption that it will not be halted. But since the effect of balance sheet reduction on broader financial conditions is uncertain, it is prudent not to begin that process until short-term interest rates are comfortably away from their effective lower bound, leaving the Committee room to offset any unanticipated effects”

In our view, the current context is a challenging one for the timing and scale of future central bank action, as macro momentum (growth and inflation) is decelerating, while earnings growth is muted and fiscal policy no longer supportive. We consequently see the announced combination of tapering, hiking and balance sheet reduction in the same year as too risky for financial markets. Indeed, we think that only 50% of the real rates normalisation required by the Fed’s policy change has been priced in so far. Thus, the risks for US growth are greater than highlighted by the Fed, and we see little room for a strong upside in risky assets. During the 2018 taper tantrum, we first sold off on monetary policy fears, but the second bigger leg lower was really a growth wobble. We have consequently broadly reduced our exposures and the resulting risk of our multi assets strategies.

Unigestion Nowcasting

World Growth Nowcaster

World Inflation Nowcaster

Market Stress Nowcaster

Weekly Change

- Last week, our World Growth Nowcaster moved slightly lower again with less positive data from both the US and Europe.

- Our World Inflation Nowcaster ticked down slightly, largely due to easing inflationary pressures in China.

- Our Market Stress Nowcaster moved modestly lower over the week as volatilities ebbed and liquidity improved.

Sources: Unigestion, Bloomberg, as of 04 February 2022

Important Information

This document is provided to you on a confidential basis and must not be distributed, published, reproduced or disclosed, in whole or part, to any other person.

The information and data presented in this document may discuss general market activity or industry trends but is not intended to be relied upon as a forecast, research or investment advice. It is not a financial promotion and represents no offer, solicitation or recommendation of any kind, to invest in the strategies or in the investment vehicles it refers to. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment.

The investment views, economic and market opinions or analysis expressed in this document present Unigestion’s judgement as at the date of publication without regard to the date on which you may access the information. There is no guarantee that these views and opinions expressed will be correct nor do they purport to be a complete description of the securities, markets and developments referred to in it. All information provided here is subject to change without notice. To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks.

Data and graphical information herein are for information only and may have been derived from third party sources. Although we believe that the information obtained from public and third party sources to be reliable, we have not independently verified it and we therefore cannot guarantee its accuracy or completeness. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. Unless otherwise stated, source is Unigestion. Past performance is not a guide to future performance. All investments contain risks, including total loss for the investor.

Unigestion SA is authorised and regulated by the Swiss Financial Market Supervisory Authority (FINMA). Unigestion (UK) Ltd. is authorised and regulated by the UK Financial Conduct Authority (FCA) and is registered with the Securities and Exchange Commission (SEC). Unigestion Asset Management (France) S.A. is authorised and regulated by the French “Autorité des Marchés Financiers” (AMF). Unigestion Asset Management (Canada) Inc., with offices in Toronto and Montreal, is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario and Quebec. Its principal regulator is the Ontario Securities Commission (OSC). Unigestion Asset Management (Copenhagen) is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Danish Financial Supervisory Authority” (DFSA). Unigestion Asset Management (Düsseldorf) SA is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Bundesanstalt für Finanzdienstleistungsaufsicht” (BAFIN).