From Extreme Pessimism To Complacency?

The start of the year has seen a very sharp deterioration in investor sentiment that led to choppy price action in major asset classes in the shape of a correlation shock. Initially driven by inflation fears and central banks’ shift in monetary policies, the shock amplified following Russia’s invasion of Ukraine, compounding the uncertainty on future growth expectations. More recently, a steep rebound in risk appetite pushed risk assets meaningfully higher, as if all risks had suddenly disappeared. The drivers behind this shift in investors’ mood are unclear, and we remain of the view that caution should prevail.

Not Over Yet

What’s Next?

The macro environment has deteriorated on all fronts

Economic fundamentals, at a macro level, are weaker now than a few months ago. At the end of last year, our base scenario was that both growth and inflation would normalise in 2022, with economic activity slowly reverting toward its long-term potential and inflation cooling to more “acceptable” levels.

Although this core scenario remains valid in our opinion, geopolitical woes have added, beyond their devastating humanitarian impact, an important upside risk to inflation pressures and downside risk to growth.

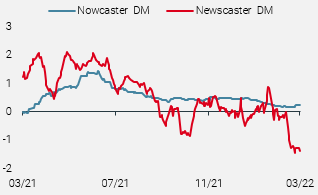

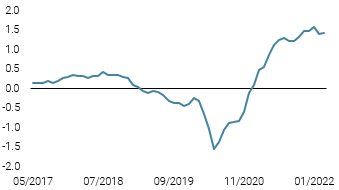

As shown in Figure 1, which compares our proprietary Growth Nowcasters (measuring the level of economic activity in real time) and Newscasters (a high frequency indicator of macro sentiment), it is still too early to measure the actual impact of the war in economic data terms. However, sentiment about future growth prospects has plunged in similar fashion to the early stages of the Covid crisis.

Figure 1: Growth Nowcaster & Newscaster comparison

Source: Bloomberg, Unigestion. As of 21.03.2022.

The question now is whether growth will decelerate further below potential, increasing the odds of stagflation, or ultimately below zero into recessionary territories. If anything, growth momentum had already turned negative and the impact of the war in Ukraine can only accelerate this trend, especially in Europe.

Obviously, the key pivot will be the trajectory and strength of inflationary pressures induced by the ongoing supply shock in the commodities complex, which will have ripple effects on demand and economic activity overall.

We had previously called a peak in inflation for Q1 2022, after a stabilisation phase observed since November last year. However, the large disruptions currently impacting the commodities complex have surely pushed the timing of this scenario forward, as well as the absolute level to which price pressures could converge to in the quarters ahead.

The latest, recently released updates of economic projections from the Fed and the ECB have already partially taken these changes into account: the Fed’s PCE Forecast for 2022 increased from 2.6% to 4.3% while the ECB now anticipates a 5.1% HICP level by year-end, vs. 3.2% previously.

The multiple variables used to produce these forecasts are subject to many uncertainties, but if these projections prove accurate, it would imply that:

- inflation will fade only slightly in the US and remain as strong as it is now in Europe and

- the impact of the war on commodity prices will ease, but

- the absolute level of prices will continue to be a headwind for economic activity.

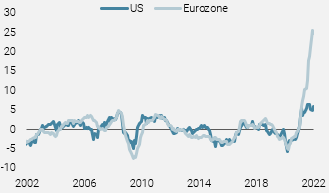

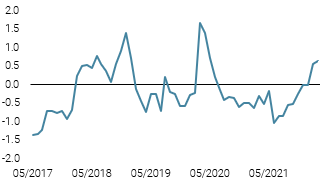

In Europe, the spread between PPI and CPI has skyrocketed following the large upswings in energy prices, especially Natural Gas, now trading at 25% as shown in Figure 2. A bad omen, as companies will have to absorb these higher input cost by either taking a hit on margins or by passing it on to consumers through higher output prices.

Therefore, there is an increased probability that inflation could decline less in 2022 than most observers – from investors to central bankers – had initially anticipated, in spite of the strong year-on-year base effects expected for Q2.

Figure 2: PPI-CPI Spreads

Source: Unigestion, Bloomberg

Central banks are resolutely on a faster tightening path

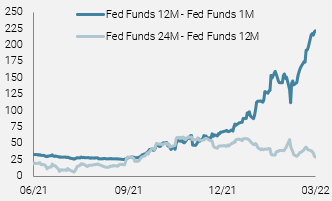

In light of the evolution of macro conditions, central banks have now committed to fighting inflation as their number one priority. The change in stance of policy makers from major economies has been swift, and market expectations have rarely been so high. The latest FOMC meeting telegraphed eight hikes for 2022, which would make this hiking cycle way more aggressive than the 2017-2018 round under Janet Yellen. As shown in Figure 3, Fed fund futures now price 225bps of hikes in a one-year period, incorporating two 50bps hikes for the May and June meetings.

Figure 3: Fed Fund futures

Source: Unigestion, Bloomberg

These expectations had reached a temporary peak prior to the invasion, in line with the inflation stabilisation that was ongoing “back then”. Now that the adjustment factoring in the additional supply chain disruptions and commodities shock has been made, we believe that peak hawkishness is around the corner in the US, and that the risks to growth are becoming significant.

As discussed in a previous publication, the consequences of tighter monetary conditions should affect demand (growth) in the first place before actually having an effect on inflation, with a four to six month lag. Therefore, the risk is that central banks’ lack of proactivity could push economic activity to undesired levels during the second part of the year, all else being equal.

Positioning: Cautiousness is key

The recovery in risk assets observed over the last two weeks looks like a bear market rally to us. Most equity markets are now trading higher than their “pre-invasion” levels, in spite of deteriorating macro conditions and heightened risks over the medium-term.

At the moment, the combination of lower growth, higher inflation and faster tightening from central banks creates a dangerous environment to deploy risk in financial markets. The contradictory signals sent by fast rising stock indices and the fixed income complex, with a US yield curve close to inversion and ever-higher inflation breakevens is yet another hint that investors might have become complacent with fundamentals, defying the central banks’ credibility.

In addition, the economic consequences stemming from the geopolitical woes between the West and Russia cannot be fully grasped for now, and the possibility of further escalation is well alive. We therefore remain cautious with reduced exposures across assets, as headwinds, risks and uncertainty have materially increased since the beginning of the year.

Over the short term, the key factor to monitor will be the evolution of the situation in Ukraine, given the impact it will have on the “inflation -> monetary policy -> growth” sequence. We could imagine a scenario under which a virtuous cycle blooms from the ashes of the war if the conflict ends sooner rather than later, but contrary to what recent price action suggests, it is nowhere to be seen for now.

Unigestion Nowcasting

World Growth Nowcaster

World Inflation Nowcaster

Market Stress Nowcaster

Weekly Change

- Last week, our World Growth Nowcaster held steady, as a slowdown in China was offset by a modest improvement in US and UK data.

- Our World Inflation Nowcaster was stable, with most countries seeing little changes in inflationary pressures.

- Our Market Stress Nowcaster was largely unchanged as lower volatilities were offset by wider spreads.

Sources: Unigestion, Bloomberg, as of 28 March 2022

Important Information

This document is provided to you on a confidential basis and must not be distributed, published, reproduced or disclosed, in whole or part, to any other person.

The information and data presented in this document may discuss general market activity or industry trends but is not intended to be relied upon as a forecast, research or investment advice. It is not a financial promotion and represents no offer, solicitation or recommendation of any kind, to invest in the strategies or in the investment vehicles it refers to. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment.

The investment views, economic and market opinions or analysis expressed in this document present Unigestion’s judgement as at the date of publication without regard to the date on which you may access the information. There is no guarantee that these views and opinions expressed will be correct nor do they purport to be a complete description of the securities, markets and developments referred to in it. All information provided here is subject to change without notice. To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks.

Data and graphical information herein are for information only and may have been derived from third party sources. Although we believe that the information obtained from public and third party sources to be reliable, we have not independently verified it and we therefore cannot guarantee its accuracy or completeness. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. Unless otherwise stated, source is Unigestion. Past performance is not a guide to future performance. All investments contain risks, including total loss for the investor.

Unigestion SA is authorised and regulated by the Swiss Financial Market Supervisory Authority (FINMA). Unigestion (UK) Ltd. is authorised and regulated by the UK Financial Conduct Authority (FCA) and is registered with the Securities and Exchange Commission (SEC). Unigestion Asset Management (France) S.A. is authorised and regulated by the French “Autorité des Marchés Financiers” (AMF). Unigestion Asset Management (Canada) Inc., with offices in Toronto and Montreal, is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario and Quebec. Its principal regulator is the Ontario Securities Commission (OSC). Unigestion Asset Management (Copenhagen) is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Danish Financial Supervisory Authority” (DFSA). Unigestion Asset Management (Düsseldorf) SA is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Bundesanstalt für Finanzdienstleistungsaufsicht” (BAFIN).