Inflation has been conspicuous in its absence for the past ten years. However, an analysis of recent developments in inflation drivers on both demand and supply sides suggests that it is about to make a comeback, albeit temporarily. We believe that this is a material risk and investors must respond. This is all the more the case as inflation assets are less favoured than growth assets for the moment. This inflation comeback requires preparation.

Come Back Song

What’s Next?

Inflation could normalise sooner than expected…

The economic situation in 2020 surprised on the downside in the first quarter, but also on the upside during the rapid recovery that followed. The US is a perfect example: if the Fed’s nowcaster forecasts turn out to be correct, US growth in 2020 will have been close to 0%. This is a long way from the duration of the 2008 shock, and coordinated action by central banks and states played a key role. The power of this cyclical improvement should not mislead investors: the risk for 2021 is not really on the recessionary side in our view, but rather on the side of the natural consequence of rapidly accelerating economic activity: inflation.

It is vital that investors keep sight of the bigger picture. Continuing with the example of the US, the “PCE Deflator”, so dear to the Fed, rose by just 1% in 2020, i.e. very low inflation to the despair of the central bank. The growth of this US price index was even negative for its hardest hit components such as leisure goods (-2.9%), medical equipment (-10.7%) and energy (-19%). However, this should not conceal the fact that some components have recently gained strength. Household equipment and vehicles saw their prices rise by 3.2% and 4.9%, respectively over the year. The implementation of vaccination campaigns should enable the components that are lagging behind to resume growth as energy prices rise. Given the levels reached by some components, it would not be surprising to see this US price index quickly return to its long-term average – and then exceed it.

… and even surprise to the upside in the coming months

Why do we see the risk of higher inflation increasing? Mainly for two economic reasons:

- On one hand, growth in world consumption should continue to recover and do so in a marked manner. Many investors are already well aware that household and corporate savings remain high. At the end of 2020, the wealth of American households had increased by USD 5.2trn in one year. We can expect that part of this increase in wealth will gradually be transformed into consumption as the health situation becomes clearer. Of this USD US 5.2trn, we can thus anticipate that 1trn will be gradually injected into the economy between 2021 and 2022, bringing the household savings rate to just under 10% of household taxable income, and adding 5% growth to US GDP. This additional growth should support the evolution of asset prices as well as goods and services. Our key scenario of 5% growth in world consumption should lead to global inflation of at least 4% in 2021 (against an expectation of 3%).

- On the other hand, this inflation could be accelerated by shortages reflecting the recent decline in economic activity. The strength of demand is there: the “New Order” component of the US ISM grew at a rate never seen before, the number of commercial flights soared in January and US rail freight indices returned to their December 2019 levels. It is not certain whether the disruptions that the supply side of the economic equation experienced in 2020 will allow it to cope with this rapid acceleration in demand.

Our Nowcaster and Newscaster inflation signals are not mistaken: for a few weeks now, they have been pointing to accelerating inflation, with our indicators now measuring an inflation risk that varies from “neutral” to “very high”, whereas a month earlier they were fluctuating from “very low” to “neutral”. The risk is there: how can we deal with it?

Inflation assets should gather investors’ attention now

Is a sudden and temporary acceleration of inflation a problem for investors? To answer this question, it is necessary to consider the valuation of assets that traditionally benefit from inflation alongside current investor sentiment for these assets.

As far as sentiment is concerned, the situation seems relatively clear. When one analyses the beta of different types of “macro” hedge funds with traditional inflation hedge assets (commodities and inflation breakevens), their pessimism about the prospects of these assets is clear. In the fourth quarter of 2020, our inflation “basket”, which combines these different assets into an investable portfolio, delivered a Sharpe ratio of 2.26 (compared to 3.9 for growth assets), yet this performance has made no impression on the hedge fund world. Their beta on these assets was negative and it has simply returned to zero as of late. There is therefore still plenty of room for this sentiment to continue its recovery.

On the valuation side, inflation breakevens rose sharply in the fourth quarter: 5-year-in-5-year breakeven rates, the Fed’s favourite indicator, rose from 0.85% in March to 1.96% at the end of December. The normalisation of inflation seems to be in prices. From the point of view of our valuation indicators, realised inflation being lower, breakevens even appear to be expensive. However, these same breakevens have a curious tendency to underestimate the escalation of inflation in periods of recovery: this was the case in 2009, 2012 and 2019. If there is an inflation surprise, this apparent high price still has a way to go. On the oil side, the term structure of oil does not anticipate a strong cyclical recovery: current prices (around USD52 per barrel) are perceived as temporary with expectations of a return to USD 49 by the end of 2021. Finally, gold is in firm contango, a typical sign of expensiveness. If we believe the “golden constant” of Erb and Harvey, the price of gold follows the consumer price index with remarkable consistency: when we compare them, gold is far from the high price that its contango suggests.

Inflation is making a comeback: let’s be prepared for it

The recognition of a growing inflation risk is the most important change in our investment policy in recent months. This has led us to combine growth assets with inflation assets within our dynamic allocation: our preference at this stage is for inflation breakevens as well as energy and industrial metals, without having a negative view on government bonds for the moment.

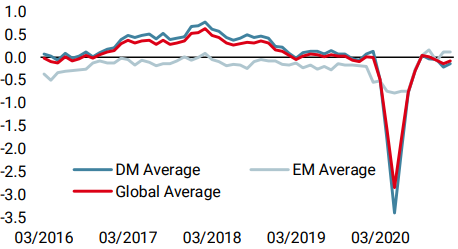

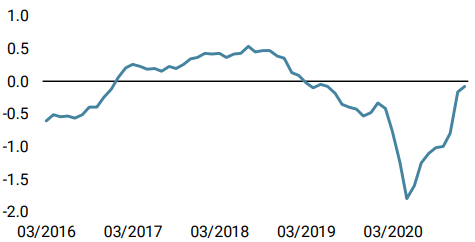

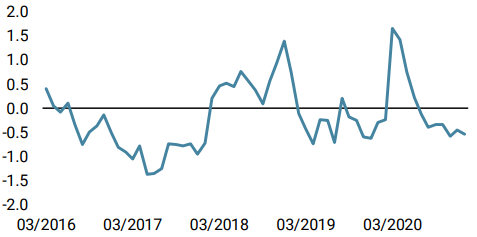

Unigestion Nowcasting

World Growth Nowcaster

World Inflation Nowcaster

Market Stress Nowcaster

Weekly Change

- Our World Growth Nowcaster increased last week, mainly as European data came out stronger, highlighting the improved growth momentum over the festive season.

- Our World Inflation Nowcaster increased again last week for most countries. Inflation risk now oscillates between high and very high.

- Our Market Stress Nowcaster declined as implied volatilities declined last week.

Sources: Unigestion. Bloomberg, as of 11 January 2021.

Important Information

This document is provided to you on a confidential basis and must not be distributed, published, reproduced or disclosed, in whole or part, to any other person.

The information and data presented in this document may discuss general market activity or industry trends but is not intended to be relied upon as a forecast, research or investment advice. It is not a financial promotion and represents no offer, solicitation or recommendation of any kind, to invest in the strategies or in the investment vehicles it refers to. Some of the investment strategies described or alluded to herein may be construed as high risk and not readily realisable investments, which may experience substantial and sudden losses including total loss of investment.

The investment views, economic and market opinions or analysis expressed in this document present Unigestion’s judgement as at the date of publication without regard to the date on which you may access the information. There is no guarantee that these views and opinions expressed will be correct nor do they purport to be a complete description of the securities, markets and developments referred to in it. All information provided here is subject to change without notice. To the extent that this report contains statements about the future, such statements are forward-looking and subject to a number of risks and uncertainties, including, but not limited to, the impact of competitive products, market acceptance risks and other risks.

Data and graphical information herein are for information only and may have been derived from third party sources. Although we believe that the information obtained from public and third party sources to be reliable, we have not independently verified it and we therefore cannot guarantee its accuracy or completeness. As a result, no representation or warranty, expressed or implied, is or will be made by Unigestion in this respect and no responsibility or liability is or will be accepted. Unless otherwise stated, source is Unigestion. Past performance is not a guide to future performance. All investments contain risks, including total loss for the investor.

Unigestion SA is authorised and regulated by the Swiss Financial Market Supervisory Authority (FINMA). Unigestion (UK) Ltd. is authorised and regulated by the UK Financial Conduct Authority (FCA) and is registered with the Securities and Exchange Commission (SEC). Unigestion Asset Management (France) S.A. is authorised and regulated by the French “Autorité des Marchés Financiers” (AMF). Unigestion Asset Management (Canada) Inc., with offices in Toronto and Montreal, is registered as a portfolio manager and/or exempt market dealer in nine provinces across Canada and also as an investment fund manager in Ontario and Quebec. Its principal regulator is the Ontario Securities Commission (OSC). Unigestion Asia Pte Limited is authorised and regulated by the Monetary Authority of Singapore (MAS). Unigestion Asset Management (Copenhagen) is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Danish Financial Supervisory Authority” (DFSA). Unigestion Asset Management (Düsseldorf) SA is co-regulated by the “Autorité des Marchés Financiers” (AMF) and the “Bundesanstalt für Finanzdienstleistungsaufsicht” (BAFIN).